The Unpredictable Path: Why Financial Planning is About Process, Not Prediction

Posted June 14, 2026 by Ben Carlson (A Wealth of Common Sense)

Main Facts: Navigating Financial Futures with Flexible Frameworks

Every year, as the calendar pages turn to mid-June, financial analyst Ben Carlson embarks on a personal ritual: a "back-of-the-envelope" investment planning exercise. Far from a rigid forecast, this annual review, detailed in his recent publication, serves as a vital compass for his financial journey. It’s a pragmatic process designed not to predict the unpredictable future with absolute certainty, but to establish crucial "goalposts" and "road markers" along the way. By taking stock of current net worth, savings rates, and making informed, yet flexible, assumptions about future income and return expectations, Carlson crafts a multi-decade financial model. This model, spanning 5, 10, 15, and 20 years, has been a cornerstone of his financial discipline since the age of 25, offering a structured yet adaptable framework for long-term wealth accumulation.

Carlson’s core insight, honed over years of market observation and personal experience, is that financial markets, much like life itself, are inherently "lumpy," not linear. This fundamental unpredictability renders precise forecasting an exercise in futility. Instead, the value lies in having a baseline against which actual performance can be measured, allowing for timely adjustments and a clearer understanding of whether one is "doing better or worse than my projected range of outcomes." This iterative approach acknowledges the dynamic nature of global economics and investor sentiment, moving beyond the illusion of control to embrace a strategy of informed adaptability. His methodology underscores a critical lesson for all investors: true financial resilience is built on a robust process, rather than an unwavering faith in specific, pre-determined outcomes.

Chronology: A Decade of Market Extremes

Carlson’s personal investment journey offers a compelling case study in market volatility and the psychological fortitude required for long-term investing. His detailed account provides a stark chronology of two contrasting market environments: the brutal bear market of the Great Financial Crisis (GFC) and the subsequent, unexpectedly robust, multi-year bull run.

The Crucible of the Great Financial Crisis (2005-2010)

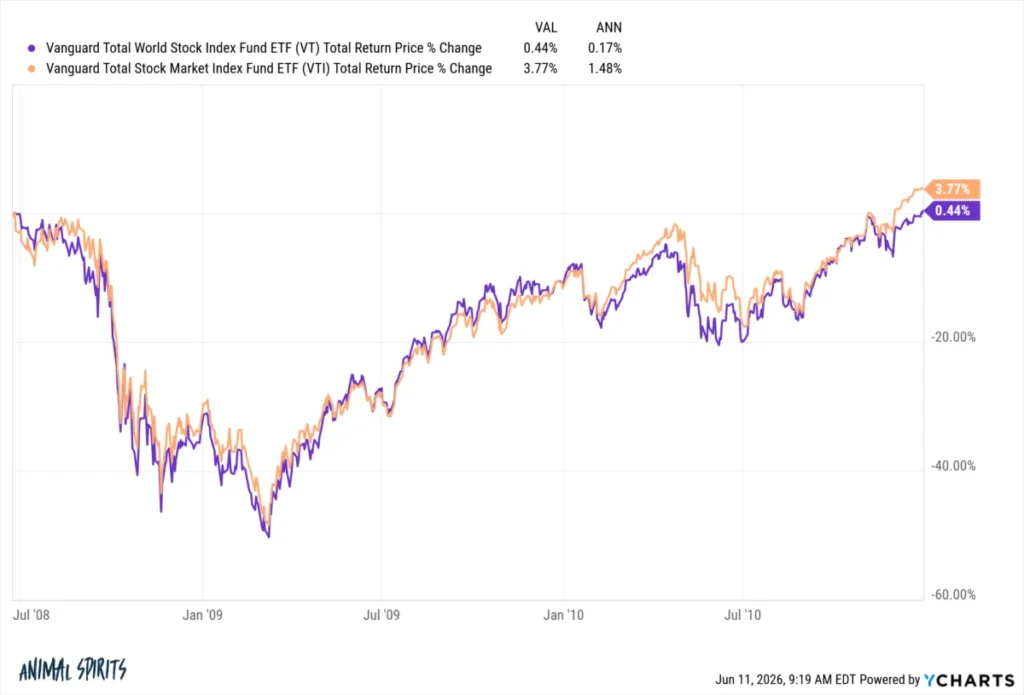

The initial phase of Carlson’s systematic planning, spanning roughly 2005 to 2010, coincided with one of the most tumultuous periods in modern financial history. Having just begun investing in his retirement accounts, he found his meticulously crafted assumptions quickly diverging from reality. The global economy, reeling from the subprime mortgage crisis, plunged into a "ferocious bear market." The S&P 500, a key benchmark for U.S. equities, plummeted by nearly 60% from its peak in late 2007 to its trough in early 2009.

During this period, Carlson observed that "the actual output fell far short of my assumptions." For many investors, this meant seeing their portfolios decimated, with little to no progress in terms of investment returns or market value. The period from 2005 to 2010 saw broad market indices, including global stock portfolios, essentially "go nowhere," as his provided chart illustrates (referencing the VT_VTI_chart.png image, which would depict flat or negative performance over this timeframe). The psychological toll on investors was immense. The constant barrage of negative news, coupled with the visible erosion of capital, made it easy to "feel dumb as an investor," questioning the very premise of long-term wealth building.

Yet, it was precisely during this challenging environment that Carlson’s commitment to his process proved invaluable. Despite the disheartening market performance, he "still dutifully made retirement contributions." This unwavering commitment to dollar-cost averaging – investing a fixed amount regularly, regardless of market conditions – allowed him to "buy periodically at lower prices in a highly volatile market." This strategy, often overlooked in the euphoria of bull markets, is a cornerstone of prudent investing during downturns, transforming market crashes into opportunities for accumulating assets at discounted valuations. While emotionally taxing, this period solidified the importance of discipline over despair, setting the stage for future gains.

The Unprecedented Bull Run (2009-Present)

The narrative shifted dramatically following the market bottom in early 2009. What followed was an astonishing and prolonged bull market that defied nearly all expert predictions. Carlson’s experience mirrors this broader market phenomenon, noting that "since then the returns have been much better." Indeed, the post-GFC recovery blossomed into one of the longest and most powerful bull markets in history.

From its nadir in early 2009, the S&P 500 has surged by more than 15% per year, demonstrating remarkable resilience and growth. A global stock portfolio, encompassing both U.S. and international equities, also delivered impressive annual returns of approximately 12%. Drilling down further, Carlson points out that the U.S. stock market specifically has generated an astounding 16.9% annual return from the depths of the GFC.

These figures dramatically outstripped even the most optimistic projections in his original planning models. Carlson candidly admits, "No one builds a financial plan with return assumptions this high. I certainly didn’t. No one in their right mind could have predicted the bull market would last as long as it has." Consequently, his portfolio today is "much larger than my original assumptions," reaching heights that "didn’t even exist in my range of outcomes."

This unexpected windfall, however, comes with its own set of psychological challenges. While gratifying, such extraordinary performance can breed a false sense of security or even lead to "overconfidence," tempting investors to attribute market success to their own superior intelligence rather than broader market forces. Carlson wisely cautions against this, stating unequivocally: "I’m not smarter because the markets have been going up… it’s not my raw intelligence that increased my portfolio to heights I didn’t plan on." He reinforces the crucial distinction: "Bull markets don’t mean you’re a genius just like bear markets don’t make you an idiot."

Supporting Data: The Behavioral Economics of Investing

Carlson’s observations are deeply rooted in the principles of behavioral economics, a field that studies the psychological factors influencing economic decision-making. His journey through market extremes provides compelling data points for understanding why "process over outcomes" is not just a slogan but a critical operational philosophy.

The Illusion of Control and Predictive Fallacy

The human brain is hardwired to seek patterns and predictability. This innate desire often leads investors to believe they can forecast market movements, identify tops and bottoms, and time their entries and exits for maximum profit. However, decades of academic research and market history consistently debunk this illusion of control. As Carlson notes, "the assumptions are almost always going to be wrong because the financial markets (and life for that matter) aren’t linear. They’re lumpy." This lumpiness is driven by a myriad of interconnected factors – geopolitical events, technological breakthroughs, shifts in consumer behavior, central bank policies, and investor sentiment – all of which interact in complex, non-deterministic ways.

Attempting to predict these short-term fluctuations is akin to gambling. Even seasoned professionals struggle to consistently outperform the market through timing. The data from Carlson’s own experience reinforces this: who could have predicted a nearly 60% drop followed by a bull run yielding 15%+ annual returns for over a decade? Such outlier events highlight the futility of precise forecasting and underscore the value of a strategy that accounts for a wide range of potential outcomes rather than a single point estimate.

The Power of Compounding and Dollar-Cost Averaging

Carlson’s success, despite the initial downturn, is a testament to the power of compounding returns and the discipline of dollar-cost averaging. During the GFC, his consistent contributions meant he was buying more shares when prices were low. When the market eventually rebounded, these deeply discounted purchases experienced significant appreciation, turbocharging his overall portfolio growth. This concept is foundational to long-term investing: time in the market, not timing the market, is the key driver of wealth. The extended bull market, even if unforeseen, allowed these accumulated assets to compound aggressively, pushing his portfolio beyond his most optimistic projections.

Emotional Biases: The Investor’s Worst Enemy

Carlson explicitly addresses the emotional pitfalls that plague investors. "Bear markets can make you question your plan. Bull markets can lead to overconfidence." These are classic examples of cognitive biases. During bear markets, fear and panic often lead investors to sell at the bottom, locking in losses. This is known as loss aversion and herding behavior. Conversely, in bull markets, recency bias (overemphasizing recent performance) and overconfidence bias can lead investors to take on excessive risk, chase speculative assets, or become complacent about their diversification.

His declaration, "Bull markets don’t make you a smarter investor. Bear markets don’t make you a dumber investor," is a direct challenge to these biases. It emphasizes that market performance is largely independent of an individual investor’s intelligence or skill. The true measure of an intelligent investor lies in their ability to maintain emotional discipline and stick to a well-reasoned plan, regardless of prevailing market sentiment.

Official Responses: Expert Consensus on Long-Term Investing

While Carlson’s article is a personal reflection, his insights resonate deeply with widely accepted principles from financial experts and investment luminaries. The "official responses" in the realm of personal finance consistently echo his emphasis on process, emotional discipline, and a long-term perspective.

The Wisdom of Value Investing and Behavioral Finance Pioneers

Legendary investors like Warren Buffett have long advocated for a patient, long-term approach, famously stating, "Our favorite holding period is forever." Buffett and his mentor, Benjamin Graham, the father of value investing, consistently stressed the importance of viewing stocks as ownership stakes in businesses, rather than mere trading vehicles. Graham’s concept of "Mr. Market" – an emotional entity who offers you prices daily, sometimes irrationally high, sometimes irrationally low – perfectly encapsulates Carlson’s observation that market fluctuations should not dictate an investor’s strategy. An intelligent investor, Graham argued, should capitalize on Mr. Market’s irrationality, buying when prices are low and holding when they are high, rather than being swayed by his mood swings.

More contemporary experts in behavioral finance, such as Daniel Kahneman (Nobel laureate for his work on prospect theory), have provided scientific backing for why human emotions so often derail rational financial decision-making. Kahneman’s research demonstrates how cognitive biases lead individuals to make suboptimal choices, confirming Carlson’s assertion that "your emotions can often grab the steering wheel." The consensus among these experts is that investors must actively work to mitigate these biases through structured planning and disciplined execution.

The Importance of a Written Investment Policy Statement

Financial planning organizations and fiduciaries universally recommend the creation of a written Investment Policy Statement (IPS) or a similar personal financial plan. This aligns precisely with Carlson’s recommendation to "write stuff down." An IPS typically outlines an investor’s goals, risk tolerance, asset allocation strategy, rebalancing rules, and investment philosophy. It serves as a personal constitution, a document to refer back to when market turbulence or euphoria threatens to trigger emotional reactions.

As Carlson suggests, articulating "Here’s what I’m going to do and why I’m going to do it. Here’s what I think might happen" within a written plan creates a powerful anchor. It establishes a rational framework that can be revisited during times of stress or excitement, helping to keep investors "grounded and avoid being outcome-based." The act of writing forces clarity and intentionality, making it harder for impulsive decisions to override a well-considered strategy.

Diversification and Asset Allocation

While not explicitly detailed in the original snippet, Carlson’s mention of a "global stock portfolio" implicitly supports the expert consensus on diversification. Spreading investments across different asset classes, geographies, and sectors is a fundamental risk management strategy. It ensures that no single market event or company failure can disproportionately impact an entire portfolio. An effective asset allocation, tailored to an individual’s risk tolerance and time horizon, is considered far more impactful on long-term returns than attempts at market timing or stock picking.

Implications: Cultivating Financial Resilience Through Process

Ben Carlson’s candid reflection offers profound implications for individual investors, encapsulating the wisdom required to navigate the inherent uncertainties of financial markets. His experience underscores that true financial resilience is forged not in predicting the future, but in mastering a consistent, disciplined process.

Separating Self-Worth from Market Performance

Perhaps the most crucial takeaway is the emphatic distinction between an investor’s intelligence and market performance. The ease with which individuals conflate their self-worth with their portfolio’s fluctuations is a significant psychological hurdle. Carlson’s narrative powerfully illustrates that being a "smart" investor is not about making prescient calls on market direction or riding every bull market to its peak. Instead, it’s about adhering to a sound investment strategy, maintaining emotional equilibrium, and understanding that market cycles are an inevitable part of the financial landscape. His experience during the GFC, where he "felt dumb" despite doing everything correctly, serves as a powerful reminder that negative outcomes do not equate to poor decision-making when the process is sound. Similarly, outsized gains in a bull market should not inflate one’s ego or lead to reckless behavior.

The Enduring Power of a Written Plan

The advice to "write stuff down" is deceptively simple yet profoundly effective. A personal investment policy statement or a similar written document serves as an invaluable anchor in the stormy seas of market volatility. It codifies an investor’s philosophy, objectives, risk parameters, and strategic approach. When fear grips the market during a downturn, or irrational exuberance takes hold during a rally, this document acts as a rational guide, reminding the investor of their long-term goals and preventing impulsive, emotion-driven decisions. It shifts the focus from chasing ephemeral outcomes to diligently executing a well-considered process.

Embracing Uncertainty and Maintaining Perspective

Carlson’s journey highlights the futility of seeking certainty in an uncertain world. Rather than striving for infallible predictions, investors should embrace the inherent "lumpiness" of markets. This acceptance fosters a healthier, more realistic perspective. It encourages investors to build portfolios that can withstand a wide range of future scenarios, rather than those optimized for a single, imagined outcome. Diversification, regular rebalancing, and a clear understanding of one’s risk tolerance become paramount in such a framework.

The Future: A Call for Continued Discipline

As Carlson concludes, the duration and trajectory of the current bull market remain unknown. "I don’t know when the current bull market will end or why." This admission of humility is a hallmark of wise investing. Whether the market continues its upward climb for another five years or experiences a sharp correction tomorrow, the core message remains unchanged: investor intelligence is measured by adherence to process, not by the short-term whims of the market. By internalizing this lesson and committing to a disciplined, long-term approach, individual investors can cultivate the resilience needed to navigate the unpredictable path of financial markets and achieve their wealth-building aspirations, regardless of the challenges that lie ahead. The ultimate goal is not to predict the future, but to be prepared for it.