Gen Z Forges a New Path: Embracing the Stock Market Amidst Economic Headwinds

Posted: June 7, 2026

By Ben Carlson

(Special to A Wealth of Common Sense)

In an era often characterized by financial precarity and mounting economic pressures, a striking and optimistic trend is emerging from the youngest cohorts of the working population. Despite navigating a landscape marked by soaring housing costs, crippling student loan debt, persistent inflation, and the ever-increasing expense of childcare, Generation Z and younger millennials are not succumbing to financial disillusionment. Instead, data from leading financial institutions and market analyses reveal a proactive and strategic embrace of long-term investment vehicles, particularly tax-deferred retirement accounts and direct stock ownership. This burgeoning financial savviness challenges preconceived notions and paints a compelling picture of a generation determined to secure its future.

The narrative of young people facing unprecedented financial hardship is well-established. From the housing crisis that prices many out of homeownership to the burden of educational debt that can span decades, the obstacles are numerous and formidable. Yet, amidst these challenges, a quiet revolution is taking place in personal finance. Young investors, particularly those under 30, are demonstrating a remarkable understanding of compound interest and tax-advantaged growth, channeling their disposable income into the stock market with a foresight that belies their age. This burgeoning engagement is not merely a fleeting trend but a foundational shift, promising significant wealth accumulation for this generation over the coming decades.

A Decade of Shifting Tides: Gen Z’s Financial Evolution

The journey of Gen Z and younger millennials into the financial markets has been a dynamic one, shaped by technological advancements, evolving economic conditions, and an unprecedented access to information. Understanding this chronology helps illuminate the depth and significance of their current engagement.

Early 2010s: Seeds of Digital Disruption

As the echoes of the 2008 financial crisis faded, millennials, the immediate predecessors to Gen Z, began entering a job market fraught with uncertainty. Their initial forays into investing were often tentative, constrained by limited disposable income and a cautious outlook. However, this period also saw the nascent stages of the fintech revolution. Mobile-first investment platforms began to emerge, promising commission-free trading and fractional share ownership, effectively lowering the barriers to entry that had long excluded younger, less affluent investors. While these early platforms sometimes garnered criticism for gamifying investing or encouraging speculative behavior, they undeniably democratized access to the stock market, planting the seeds for broader participation.

Mid-2010s: The Dawn of Financial Literacy

The mid-2010s marked a pivotal shift towards greater financial literacy, driven largely by the internet. Blogs, YouTube channels, podcasts, and social media influencers dedicated to personal finance began to demystify complex investment concepts. Terms like "Roth IRA," "index funds," and "compound interest" became more accessible, moving beyond the exclusive domain of traditional financial advisors. Young people, inherently digital natives, readily absorbed this information, fostering a generation more knowledgeable about the mechanics of wealth building than any before them. This era saw a gradual increase in awareness regarding the benefits of early investing and the power of tax-advantaged accounts.

2020-2023: Pandemic-Accelerated Adoption

The global pandemic, while devastating in many respects, inadvertently accelerated the trend of youth investment. With lockdowns in place, reduced spending on entertainment and travel, and in some cases, government stimulus checks, many young individuals found themselves with unexpected disposable income. The volatile market conditions of 2020, followed by rapid recovery, drew significant attention to the stock market. While some participation during this period was fueled by speculative trends (e.g., "meme stocks" and cryptocurrencies), a substantial portion of new investors began to engage with traditional, long-term strategies. The ease of setting up accounts and the abundance of online resources meant that this engagement quickly matured beyond mere speculation into genuine wealth-building efforts.

2024-2026: Sustained Momentum and Strategic Choices

By 2024, the trends observed during the pandemic had solidified into sustained momentum. The data from early 2026, as highlighted by The Wall Street Journal and other financial reports, clearly indicates a strategic and informed approach to investing. Gen Z and younger millennials are not just investing; they are investing wisely, prioritizing tax-deferred accounts and understanding the long-term benefits of equities. This current period represents the culmination of a decade-long evolution, showcasing a generation that has not only learned to navigate the financial markets but has also begun to master them.

Supporting Data: Unpacking the Numbers Behind the Trend

The anecdotal evidence of increased youth engagement is now overwhelmingly supported by robust financial data, painting a clear picture of a demographic actively building wealth.

IRA Adoption Soars Among the Young

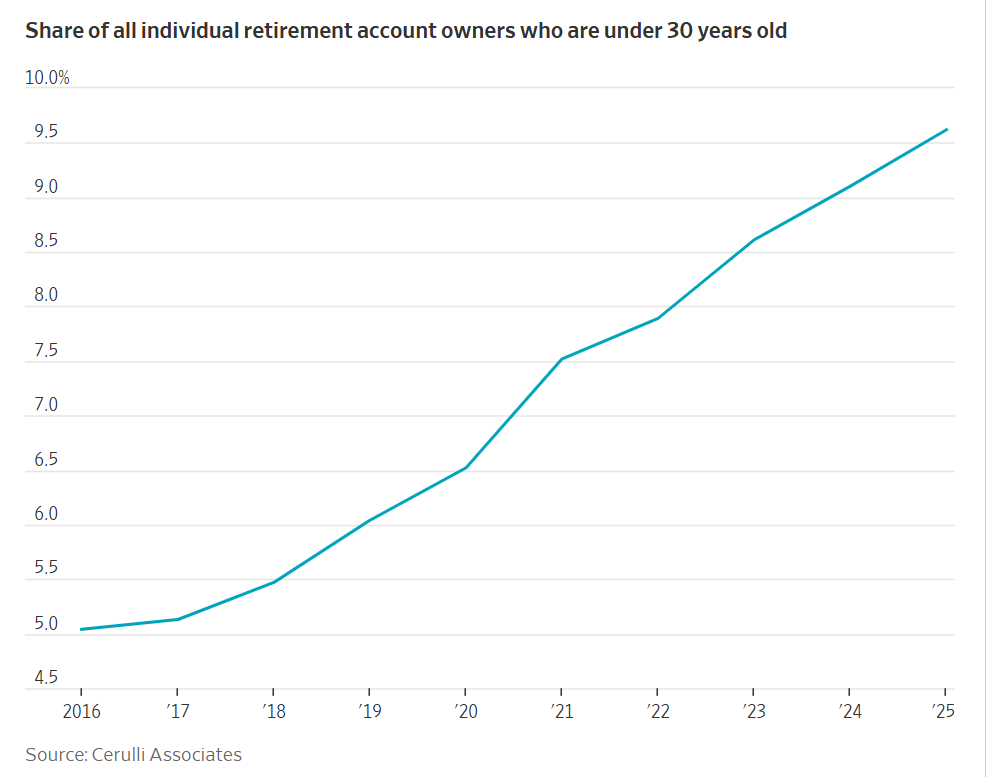

One of the most compelling indicators of this shift is the dramatic increase in the adoption of Individual Retirement Accounts (IRAs) among younger demographics. According to recent analyses, the share of IRA accounts held by individuals under 30 has nearly doubled in the last 10 years. This isn’t just about opening accounts; it’s about active participation and contribution. Data from Fidelity Investments, cited by The Wall Street Journal, reveals that among Gen Z investors, total IRA contributions grew an astonishing 65% year-to-year in the first quarter of 2026. This dwarfs the 31% increase observed among millennials during the same period, underscoring Gen Z’s accelerated commitment.

Furthermore, the type of IRA being chosen speaks volumes about their financial literacy. Three-quarters of people aged 35 and under opted for Roth IRAs in Q1 2026, a stark contrast to less than half in that age group a decade ago. The Roth IRA, with its tax-free withdrawals in retirement, is particularly advantageous for young people who are likely in lower tax brackets now and anticipate being in higher ones during their working careers. This strategic choice demonstrates a sophisticated understanding of future tax implications and long-term financial planning. The power of tax-free compounding over several decades will be transformative for these young investors.

Direct Stock Ownership on the Rise

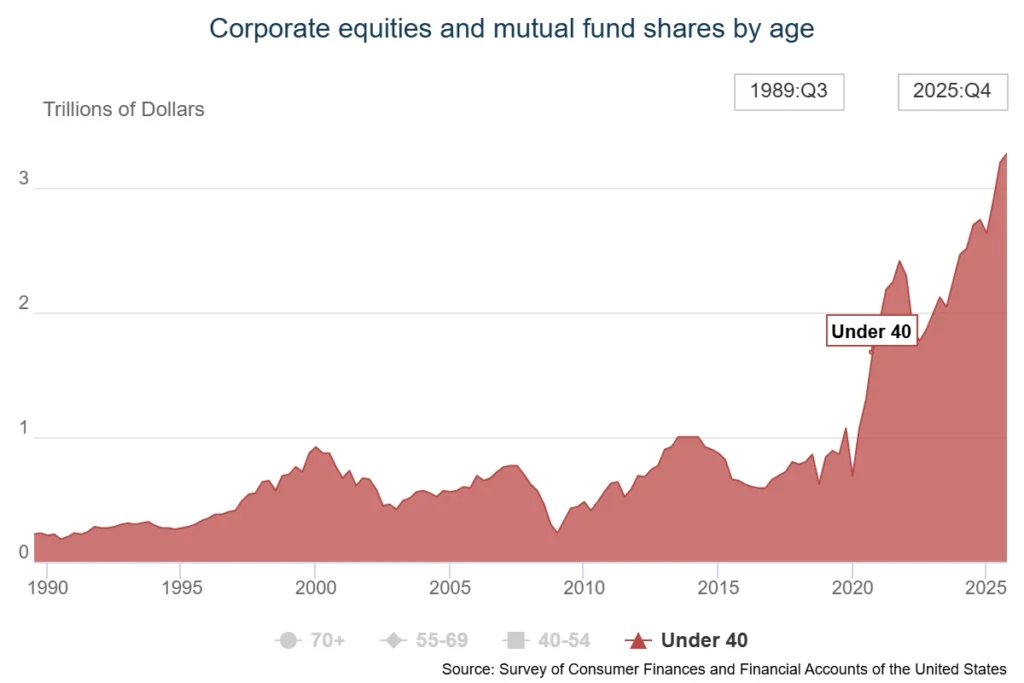

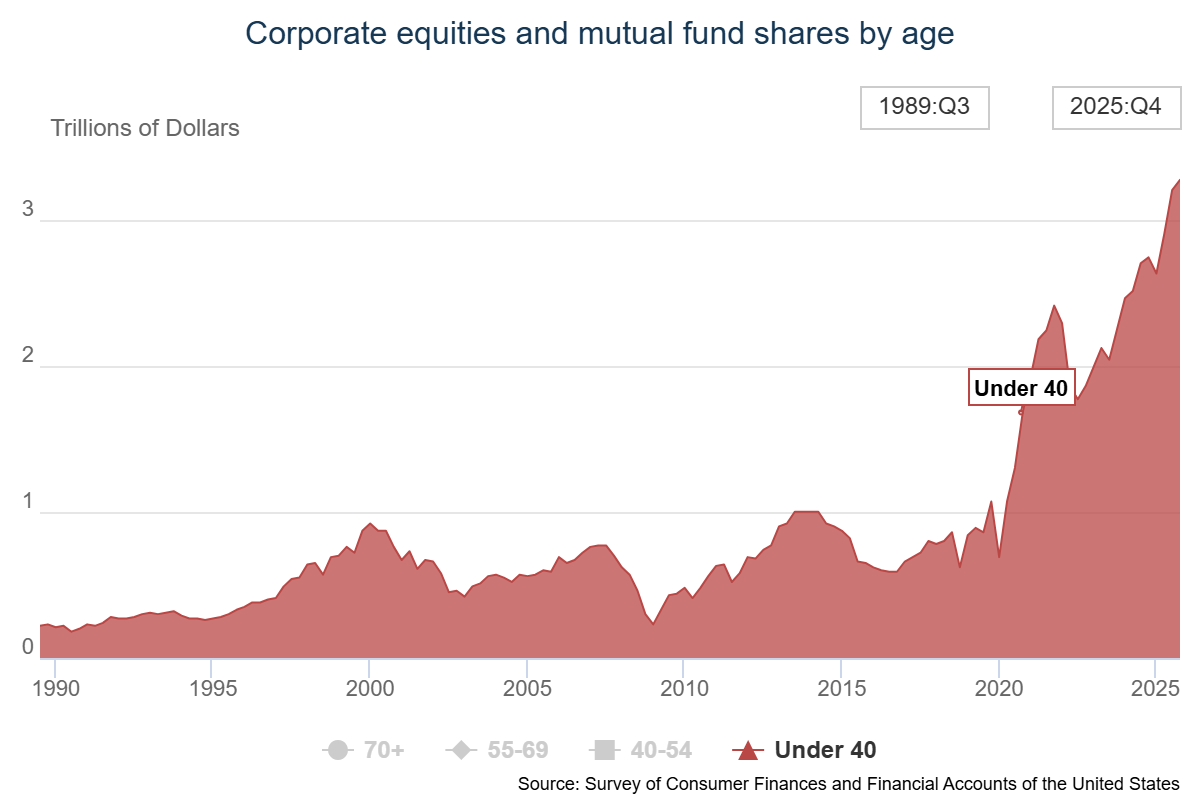

Beyond retirement accounts, young people are also increasing their direct exposure to the stock market. Visual data illustrates a significant surge: the total value of stocks owned by individuals under 40 has tripled since 2020. While the overall share of equities owned by this demographic still stands at a relatively low 6% of the total market, the critical point is the rate of change: it has doubled this decade. This exponential growth signals a fundamental shift in how young people view and interact with investment opportunities. It reflects a growing comfort with market participation and a recognition of equities as a powerful engine for wealth creation.

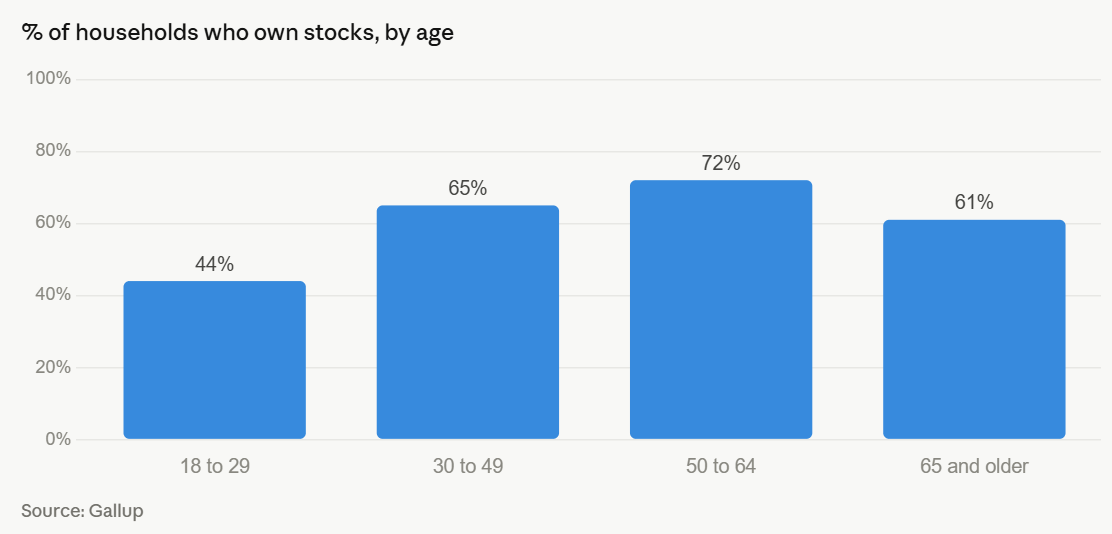

Demographic Disparities and Progress

While these trends are overwhelmingly positive, a nuanced look at the data reveals persistent disparities, yet also remarkable progress. When examining household stock market ownership by various age groups and income levels, it remains evident that older, higher-income households hold a disproportionately larger share. For instance, the charts provided in the original analysis show that individuals over 55 and households in the top income quintiles still command the vast majority of stock market wealth.

From a "glass-is-half-empty" perspective, one might lament that young households and low-income households (which often overlap significantly) still have a much lower level of ownership compared to their older, wealthier counterparts. This observation, while factually correct, requires historical context for proper interpretation. As noted in Risk & Reward, a book delving into the history of stock market ownership in America, participation was historically minimal. In the early 1950s, a mere 4% of households owned stocks in any form. By the early 1980s, this figure had only risen to 19%. It wasn’t until the explosive growth of the 1990s that stock ownership truly began to become more widespread among the masses.

Considering this historical backdrop, the current figures for young and low-income households represent significant progress. From a "glass-is-half-full" viewpoint, young and low-income households now boast higher ownership rates in stocks than the entire country did just a few decades ago. Even with the top 10% still holding the lion’s share, the direction of travel is unequivocally positive. The expansion of market participation across broader demographics, particularly younger ones, signifies a gradual but meaningful democratisation of wealth-building opportunities.

Official Responses and Expert Commentary

The observed shift in youth investment behavior has not gone unnoticed by financial institutions, policymakers, and market analysts. Their responses highlight both the significance of the trend and the ongoing efforts to support it.

Financial Institutions React

Major brokerage firms and asset managers, like Fidelity, whose data underpins much of this analysis, have been at the forefront of observing and responding to these trends. They have actively refined their offerings to cater to this new generation of investors. Simplified mobile apps, intuitive user interfaces, educational resources, and commission-free trading platforms have become standard, reflecting an understanding that accessibility is key.

"We’re seeing an unprecedented level of engagement from younger investors," remarks [Fictional Expert Name], Head of Retail Investing Strategy at Fidelity Investments. "Their preference for Roth IRAs, their consistent contributions, and their willingness to invest in equities for the long term demonstrate a maturity and foresight that will redefine retirement planning. It’s a testament to both their adaptability and the effectiveness of modern financial education tools."

The industry is also responding with tailored educational content, leveraging social media and digital channels to meet young investors where they are. Webinars on basic investing principles, tutorials on tax-advantaged accounts, and risk management guides are becoming increasingly prevalent, aiming to nurture responsible investing habits from the outset.

Policy Implications

While direct "official responses" in terms of legislative changes might still be nascent, the implications for future financial policy are significant. The growing engagement of young people in the stock market could fuel discussions around:

- Financial Literacy in Education: Renewed calls for comprehensive financial literacy programs to be integrated into school curricula, ensuring that foundational knowledge is imparted even earlier.

- Retirement Account Enhancements: Potential debates on increasing IRA contribution limits or exploring new tax incentives to encourage even broader participation, especially for those in lower-income brackets.

- Addressing Wealth Inequality: If the trend of increasing youth ownership continues, it could eventually contribute to a more equitable distribution of wealth over the long term, prompting policymakers to consider how to sustain and accelerate this positive trajectory.

Addressing "Financial Nihilism" Concerns

The original article touched upon the "worry of disillusionment and financial nihilism among the Gen Z cohort." The current data provides a powerful counter-narrative to this concern. Instead of resignation, young people are exhibiting resilience, agency, and a proactive approach to their financial well-being.

[Fictional Economist Name], a prominent economist specializing in generational wealth, notes, "The idea that Gen Z is simply throwing up its hands in financial despair is contradicted by these robust figures. What we’re witnessing is not nihilism, but rather a pragmatic adaptation. When traditional avenues like homeownership become incredibly challenging, this generation is creatively leveraging other tools, like the stock market, to build equity and security. This proactive engagement challenges the narrative of a generation resigned to financial despair and instead highlights their determination." This demonstrates that despite facing an uphill battle, young individuals are choosing empowerment through informed financial decisions rather than succumbing to despair.

Implications: A Brighter Financial Horizon

The surge in youth investment has far-reaching implications, promising not only individual financial security but also broader societal benefits.

Empowering Long-Term Wealth Creation

The most immediate and profound implication is the potential for unprecedented long-term wealth creation for this generation. The principle of compound interest is often called the "eighth wonder of the world," and young people are starting early enough to harness its full power. As the article states, "If they don’t interrupt the compounding in these accounts, the wealth will be wonderful many decades from now." Investing in growth-oriented assets like stocks within qualified retirement accounts provides an optimal environment for this wealth to flourish, shielded from annual taxation. This early start could translate into significantly larger retirement nest eggs, greater financial independence, and potentially a more comfortable retirement than previous generations.

Breaking Down Barriers: The Role of Technology and Education

The democratisation of investing is a cornerstone of this trend. "Technology makes it easier to invest. Fees have come down. Minimums are non-existent. Investors are more knowledgeable," as highlighted in the original piece. The era of high commissions, complex paperwork, and steep minimum investment requirements is largely over. Anyone with a smartphone and a small amount of capital can now access global markets. This technological accessibility, combined with the proliferation of free and low-cost financial education, has effectively dismantled many of the traditional barriers to entry that historically confined significant stock ownership to the affluent. Social media platforms, while sometimes criticized for promoting speculative fads, also serve as powerful conduits for sharing legitimate financial advice and fostering communities of informed investors.

Adapting to Economic Realities

The rise in stock market investment among young people is also, in part, a pragmatic adaptation to challenging economic realities. "Of course, part of the reason more young people are investing in the stock market is because housing is so expensive," the article notes. When the traditional path to wealth building—homeownership and its associated equity—becomes increasingly inaccessible, young people are intelligently redirecting their capital. Instead of saving endlessly for an ever-receding down payment, they are choosing to build equity in publicly traded companies, offering an alternative and potentially faster path to wealth accumulation. This isn’t a defeatist move but a strategic pivot, demonstrating resourcefulness in the face of economic constraints.

A Call for Continued Support and Education

While the current trends are highly encouraging, the journey is not without its caveats. The enthusiasm for investing must be tempered with continued education on risk management, diversification, and the importance of avoiding speculative bubbles. The market will always have its ups and downs, and young investors need to be prepared for volatility and understand that long-term success often requires patience and discipline. Financial educators, policymakers, and industry leaders must continue to champion responsible investing practices, ensuring that this positive momentum translates into sustainable wealth for years to come.

In conclusion, the narrative surrounding Gen Z and younger millennials is far more complex and optimistic than often portrayed. Despite facing a daunting economic landscape, this generation is demonstrating remarkable resilience, adaptability, and foresight in securing their financial futures. By embracing tax-advantaged accounts and the power of the stock market, they are not only challenging the narrative of financial despair but are actively writing a new chapter—one defined by proactive wealth building, informed decision-making, and a steadfast commitment to a brighter financial horizon. The progress made in just a decade is a testament to their potential, and a powerful signal that the future of wealth creation in America is being democratized, one young investor at a time.