Unpacking the Paradox: Bob the Market Timer and the Peril of Missed Opportunities

Posted July 16, 2026

A fundamental tension exists within the realm of investment wisdom, frequently challenging even seasoned financial strategists and often leaving individual investors bewildered. On one hand, the reassuring tale of "Bob, the World’s Worst Market Timer" powerfully illustrates the transformative potential of compounding and the critical importance of remaining invested, even when initial entry points appear catastrophically ill-timed. Conversely, a stark warning frequently echoes across financial discourse, championed by figures like Tom Lee: missing merely a handful of the market’s best performing days can decimate, or even entirely erase, an investor’s overall returns over a decade.

This apparent contradiction lies at the heart of a recent inquiry posed to financial expert Ben Carlson, prompting a deeper dive into the intricate interplay of market timing, long-term commitment, and the unpredictable clustering of volatility. The core question: Is Bob’s ultimate success merely a fortunate byproduct of his unwavering commitment, which inadvertently ensures he captures those crucial "best days" often nestled within the very downturns he buys into? And what would be the true cost if a hypothetical "Panic-Selling Bob" succumbed to fear, divesting at the bottom and forfeiting those vital recovery rallies? This article aims to reconcile these compelling market parables, offering a comprehensive analysis grounded in data and behavioral psychology.

The Enigma of "Bob, the World’s Worst Market Timer"

The story of Bob has become a cornerstone of long-term investing advocacy. Bob, a fictional investor, possesses an uncanny knack for making the absolute worst investment decisions imaginable: he consistently invests his lump sum at every single market peak. Whether it was the dot-com bubble’s zenith, the eve of the 2008 financial crisis, or the peak before a sudden bear market, Bob was there, putting his money in at the very top.

Intuitively, one would expect Bob to be an utter financial disaster. Yet, Ben Carlson’s original parable, "What If You Only Invested at Market Peaks?", reveals a counterintuitive truth: despite his consistently disastrous timing, Bob ends up with a substantial portfolio over the long run. His success isn’t attributed to cunning market analysis or strategic brilliance, but rather to two simple, yet profoundly powerful, principles: unwavering commitment to staying invested and the relentless power of compound interest over an extended time horizon. Bob never sells. He endures the subsequent crashes, holds through the despair, and allows his investments to recover and grow. This narrative offers immense psychological comfort to countless investors who fret over perfect entry points, demonstrating that time in the market often trumps timing the market.

The Critical Impact of "Missing the Best Days"

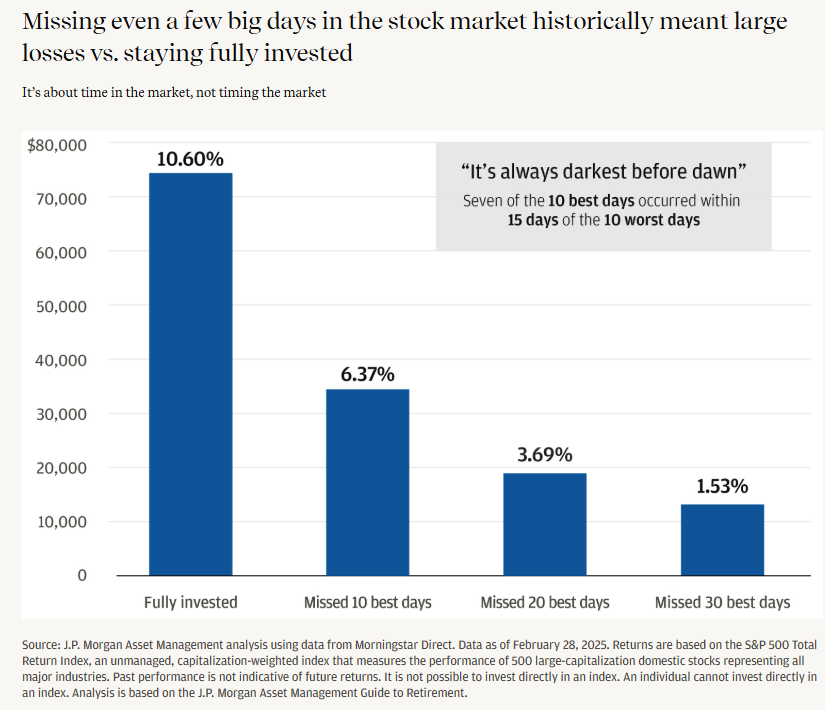

In stark contrast to Bob’s reassuring narrative stands the stark warning about the perils of market timing, often encapsulated by the statistic regarding "missing the best days." Frequently cited by strategists such as Tom Lee of Fundstrat Global Advisors, this data point highlights the disproportionate impact a few exceptional trading days can have on an investor’s cumulative returns. The premise is simple yet terrifying: attempt to time the market, get out during a downturn, and you risk missing the crucial bounce-back days that often follow the steepest declines.

Supporting data from institutions like J.P. Morgan vividly illustrates this phenomenon. Research consistently shows that if an investor misses just the 10 best performing days in the market over a given decade, their overall returns can be dramatically reduced, sometimes by as much as 40%. Extending this, missing the best 30 days can reduce returns to a mere fraction of the long-term average, effectively wiping out years of potential growth. This statistic serves as a powerful deterrent against impulsive selling during market downturns, reinforcing the mantra that staying fully invested is paramount to capturing the market’s full potential.

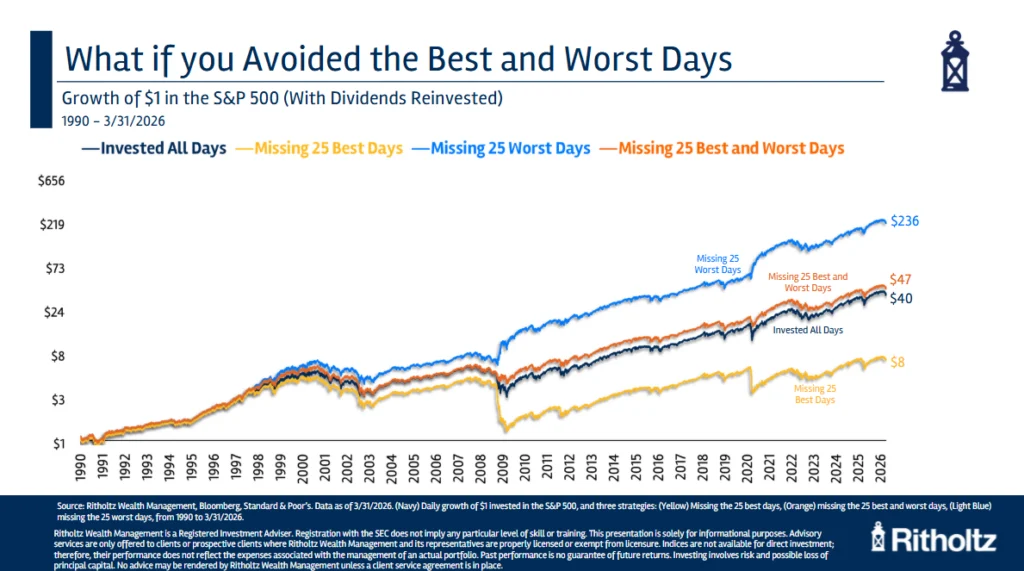

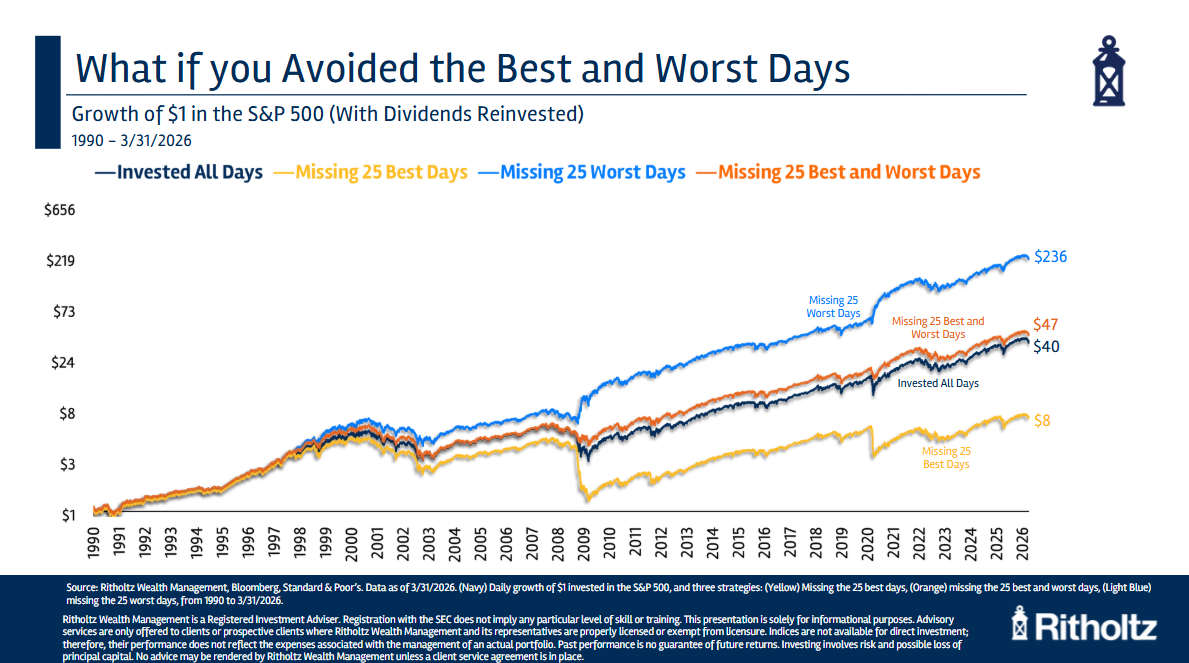

Consider the following illustrative data:

- Fully Invested: A hypothetical $1 invested since 1990 could have grown to approximately $40 if held consistently.

- Missing the Best 25 Days: If an investor missed just the 25 best trading days within that same period, that $1 would have only grown to about $8. This represents an astonishing 80% reduction in wealth accumulation.

- The Hypothetical Ideal (Missing the Worst 25 Days): Conversely, if an investor possessed perfect foresight and managed to miss only the 25 worst trading days, that same $1 would have soared to nearly $240, showcasing the immense power of avoiding downturns (a feat virtually impossible for real-world investors).

- Missing Both Best and Worst: Interestingly, if an investor managed to miss both the 25 best and 25 worst days, their returns would approximate the long-term buy-and-hold strategy, highlighting the symmetrical nature of extreme market movements.

These figures underscore the precarious balance investors navigate. The desire to avoid losses is innate, yet the attempt to do so often leads to the fatal error of missing the very recoveries that drive long-term wealth creation.

Reconciling Two Market Truths: The Interplay of Peaks, Troughs, and Rallies

The apparent contradiction between Bob’s success and the "missing the best days" warning finds its reconciliation in a critical, often overlooked, aspect of market behavior: the clustering of extreme volatility. As Ben Carlson aptly notes, "There’s no magic in Bob’s terrible market timing strategy because of how the best and worst days tend to occur."

The key insight is that the market’s most significant upswings and downswings are not randomly distributed. Instead, they frequently occur in close proximity to one another, particularly during periods of heightened market turbulence. Data from sources like Exhibit A clearly illustrates this phenomenon. An analysis of S&P 500 performance reveals that the overwhelming majority of the best and worst single-day market movements since 1990 have been concentrated around major financial crises and periods of significant economic uncertainty. This includes the dot-com bust of the early 2000s, the Global Financial Crisis of 2008, the swift COVID-19 induced crash of 2020, and the inflation-driven bear market of 2022.

What this means for Bob, the world’s worst market timer, is profound. By consistently investing at peaks, Bob is inherently positioned to endure the subsequent downturns. And because the most powerful recovery days—the "best days"—tend to occur precisely within or immediately after these periods of steep decline, Bob’s unwavering commitment to staying invested ensures he automatically captures them. He doesn’t need to time them; his long-term discipline forces him to be present when they happen. The very crashes he initially buys into become the incubators for the rallies that ultimately fuel his long-term success.

The Mechanics of Market Volatility: Why Days Cluster

The clustering of extreme market movements is not an arbitrary pattern; it’s driven by a confluence of fundamental and behavioral factors:

-

Volatility Begets Volatility: When markets become volatile, investor emotions amplify. Uncertainty reigns supreme, and the fear of further losses often outweighs the hope of potential gains. This heightened emotional state leads to more erratic and exaggerated market movements. Rapid price swings, both up and down, become more common as market participants react swiftly to news, rumors, and their own shifting sentiments. The market’s "jitteriness" creates an environment where large daily percentage changes are more likely.

-

Panic Works in Both Directions: Market downturns are often initiated by a cascade of selling, driven by factors such as forced liquidations, margin calls, profit-taking, and widespread fear. This "panic selling" can trigger dramatic declines. However, once the market hits a perceived bottom, or when policy responses are introduced, the dynamics can quickly reverse. "Panic buying" or relief rallies emerge from short covering, bargain hunting by contrarian investors, and a sudden influx of hope. This creates a whipsaw effect where sharp drops are often followed by equally sharp, albeit sometimes temporary, rebounds. The same emotional and structural forces that drive prices down can quickly propel them back up, creating a natural clustering of extreme events.

-

Herding is Heightened When People Lose Money: The concept of "the crowd" in financial markets is not new. Gustave Le Bon, the French psychologist, eloquently described this phenomenon in his 1895 work, The Crowd: A Study of the Popular Mind. He observed that individuals, when transformed into a crowd, acquire a "collective mind" that makes them feel, think, and act differently than they would in isolation. "There are certain feelings that do not come into being, or do not transform themselves into acts, except in the case of individuals forming a crowd." In financial crises, this herding instinct is profoundly amplified. As prices fall, the perceived safety of "being with the crowd" encourages mass selling. This collective panic often pushes prices below their fundamental value. Conversely, when signs of recovery emerge, or when others start buying, the same herding mentality can lead to a rush back into the market, driving rapid price appreciation. This collective behavior, driven by fear and greed, ensures that extreme movements, both negative and positive, tend to occur in tightly packed sequences.

The Folly of Market Timing: A Deeper Dive into Bob’s Success and Failure

Understanding the clustering of best and worst days unequivocally clarifies Bob’s success and starkly illuminates the catastrophic consequences of "Panic-Selling Bob."

The reader’s hypothetical "Panic-Selling Bob" who buys at peaks but then sells at the bottom and misses the 10 best bounce-back days would face an entirely different financial reality. The math would indeed look catastrophic. If we consider the J.P. Morgan data, missing just 10 of the best days can slash returns by 40%. If Bob were to repeatedly buy at the top, endure a decline, panic-sell near the bottom, and then watch from the sidelines as the market staged its inevitable, powerful recovery (which includes those critical "best days"), his portfolio would be decimated. He would experience the full brunt of the losses without participating in any of the subsequent gains. This scenario would negate the very power of compounding that saved the original Bob.

The original Bob’s "only saving grace," as Ben Carlson emphasizes, was his unwavering commitment to a long time horizon. This commitment wasn’t magical; it was simply the mechanism that ensured his participation through the entire market cycle, including the downturns and, crucially, the subsequent, often rapid, recoveries. By never selling, he was forced to sit through the best days and the worst days which typically come after the peaks he so unfortunately chose. This involuntary participation in the full cycle is the unsung hero of Bob’s story.

The Indispensable Role of Time Horizon and Discipline

The reconciliation of these two market parables boils down to two paramount investment principles: a long time horizon and unwavering emotional discipline.

A long time horizon is not merely a preference; it is a necessity for navigating the inherent volatility of financial markets. It provides the crucial buffer that allows temporary setbacks (like Bob’s peak purchases) to be overcome by the long-term upward trend of equities and the compounding of returns. Over decades, market corrections and even bear markets become mere blips on a much larger upward trajectory. Without this extended timeframe, the impact of poor timing or missed recovery days becomes irreversible and devastating.

Emotional discipline is the psychological twin to the long time horizon. It is the ability to resist the primal urge to panic sell during downturns and the equally tempting (but often futile) desire to time entries and exits. Understanding that the best days often follow the worst days provides a rational framework to combat fear. It equips investors with the knowledge that selling into a panic, while emotionally satisfying in the short term, is precisely the action that guarantees the forfeiture of future gains. The successful investor, much like the original Bob, is not necessarily the smartest or the luckiest, but often simply the one who can remain steadfast and disciplined through market’s inevitable ups and downs.

Broader Implications for the Modern Investor

The lessons drawn from reconciling Bob’s story with the "missing the best days" statistic offer profound implications for every modern investor:

-

The "Stay Invested" Imperative: This is the clearest and most actionable takeaway. Attempting to time the market is a losing proposition for the vast majority of investors. The data overwhelmingly supports remaining fully invested over the long term, thereby guaranteeing participation in both the downturns and the critical recovery days.

-

Dollar-Cost Averaging: For regular investors, dollar-cost averaging (investing a fixed amount at regular intervals) is an excellent strategy that inherently benefits from the clustering phenomenon. By continuously investing, one naturally buys more shares when prices are low (during downturns) and fewer when prices are high. This systematic approach ensures participation in the market regardless of daily fluctuations and mitigates the risk of a single, ill-timed lump-sum investment.

-

Diversification as a Buffer: While not explicitly detailed in the original article, diversification across various asset classes, geographies, and sectors further enhances an investor’s ability to weather volatility. A diversified portfolio is less susceptible to the extreme movements of any single component, providing a smoother ride through turbulent periods and reducing the temptation to panic.

-

Combating Behavioral Biases: Understanding the psychological underpinnings of market behavior – volatility begetting volatility, panic working in both directions, and herding – empowers investors to recognize and counteract their own behavioral biases, such as loss aversion and confirmation bias. This self-awareness is a powerful tool for maintaining discipline.

-

The Value of Professional Guidance: As highlighted by the "Ask the Compound" episode featuring Taylor Hollis, financial advisors play a crucial role beyond mere investment selection. They act as behavioral coaches, helping clients navigate emotional decisions, stick to their long-term plans, and avoid costly mistakes driven by fear or greed. Whether it’s estate planning, managing debt, or discussing money with family, an advisor provides objective perspective and structured support.

Conclusion: The Enduring Wisdom of Patience in Volatile Markets

The seeming paradox of Bob, the world’s worst market timer, and the dire warnings against missing market rallies, ultimately converges on a singular, powerful truth: the long-term success of an investor is far less dependent on impeccable timing and far more on unwavering commitment and emotional fortitude.

The market’s most dramatic swings, both positive and negative, are intrinsically linked, clustering together in periods of intense uncertainty. This inherent characteristic means that an investor who bails out during a downturn almost invariably forfeits the subsequent, often rapid, recovery that contains the market’s most significant growth days. Bob’s success wasn’t magic; it was the inevitable outcome of his long time horizon, which compelled him to remain invested through the entire cycle, thereby capturing the critical bounce-back rallies that followed his ill-timed entries.

For the modern investor, the lesson is clear: resist the seductive allure of market timing. Embrace the power of patience, discipline, and a long-term perspective. While market volatility can be unsettling, understanding its cyclical and clustered nature provides a robust framework for weathering the storms and, ultimately, participating in the enduring growth that only time in the market can deliver. The true secret to investment success lies not in outsmarting the market, but in simply staying the course.