The Unseen Anchor: How the Housing Hedge Defies Economic Turmoil in the 2020s

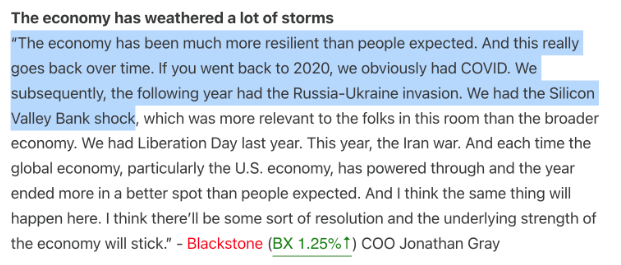

Washington D.C. – The 2020s have subjected global economies to an unprecedented gauntlet of challenges. From a devastating pandemic and subsequent supply chain breakdowns to surging inflation and geopolitical conflicts that have rattled energy markets, households have faced relentless economic headwinds. Yet, against a backdrop of rising costs—with overall prices now roughly 30% higher than at the decade’s outset—the American consumer has displayed remarkable resilience, confounding numerous recession forecasts and fueling a sustained, robust spending spree. This extraordinary defiance of economic gravity, experts suggest, is largely underpinned by a unique and powerful phenomenon: the "housing hedge" secured by millions of homeowners.

The Tumultuous Chronology of the 2020s

The current decade has unfolded as a masterclass in economic volatility, a stark contrast to the relatively stable and lower-inflation environment of the 2010s, which saw price increases of approximately 19% over its entire span. The rapid succession of shocks has created a complex economic landscape.

The Pandemic’s Initial Shock and Fiscal Floodgates

The initial economic hurdle arrived with the COVID-19 pandemic in early 2020. Widespread lockdowns, business closures, and a severe disruption of daily life brought economic activity to a grinding halt. Global supply chains, meticulously optimized for efficiency, fractured under the strain, leading to shortages across various sectors. In response, governments worldwide, including the United States, unleashed an unprecedented wave of fiscal and monetary stimulus. Trillions of dollars in government spending—through direct payments to households, enhanced unemployment benefits, and business support programs like the Paycheck Protection Program (PPP)—were injected into the economy. Simultaneously, central banks slashed interest rates to near-zero and engaged in massive quantitative easing, aiming to prevent a total economic collapse and keep individuals and businesses afloat. While successful in averting a deeper depression, these measures laid the groundwork for future inflationary pressures.

Supply Chain Chaos and the Rise of Inflation

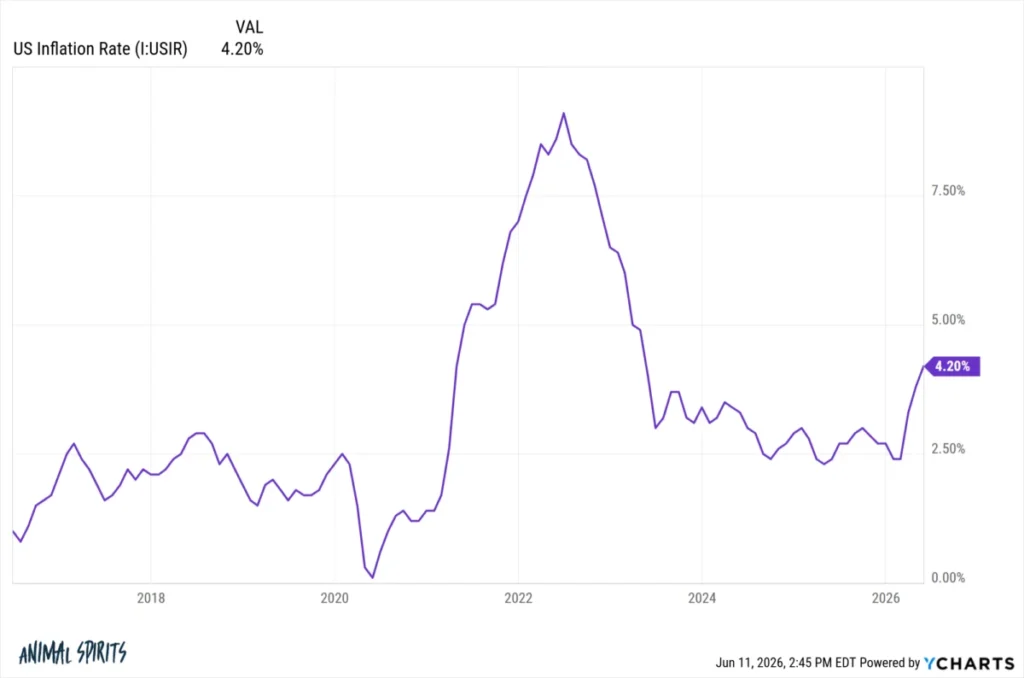

As economies began to reopen and demand surged, the crippled supply chains struggled to keep pace. Factories faced labor shortages, shipping containers were bottlenecked, and transportation costs soared. This mismatch between robust demand, fueled by accumulated savings and government stimulus, and constrained supply ignited inflationary pressures. By 2021 and 2022, inflation reached levels not seen in four decades, eroding purchasing power and creating significant financial strain for many households. The Federal Reserve, initially viewing inflation as "transitory," was forced to embark on an aggressive campaign of interest rate hikes to cool the overheating economy.

Geopolitical Shocks: Wars and Energy Volatility

Just as the global economy grappled with post-pandemic inflation, new geopolitical crises emerged, further exacerbating price pressures. The Russia-Ukraine war, commencing in early 2022, sent shockwaves through global energy and food markets. Russia, a major exporter of oil, natural gas, and key agricultural commodities, saw its supply routes disrupted and sanctions imposed, driving crude oil and natural gas prices to historic highs. This directly translated into soaring gasoline prices at the pump and increased utility costs for consumers.

Adding to this, the past year saw the implementation of various tariffs, further complicating international trade and adding costs to imported goods. More recently, heightened tensions, implicitly referred to as the "Iran war" in the original article, have yet again sent gas prices shooting higher, demonstrating the fragility of global energy markets and their immediate impact on household budgets. The cumulative effect of these sequential crises has been a relentless upward trajectory in the cost of living, with prices now hovering roughly 30% above their pre-pandemic levels in early 2020.

Defying Expectations: The Resilient Consumer

Despite the barrage of economic blows and the substantial erosion of purchasing power, the most striking economic narrative of the 2020s has been the unwavering resilience of the American consumer. Economists, policymakers, and market analysts repeatedly predicted an imminent recession, particularly as inflation soared and interest rates climbed. Yet, these forecasts largely failed to materialize, beyond the brief, sharp downturn at the onset of the pandemic.

Sustained Spending Amidst Adversity

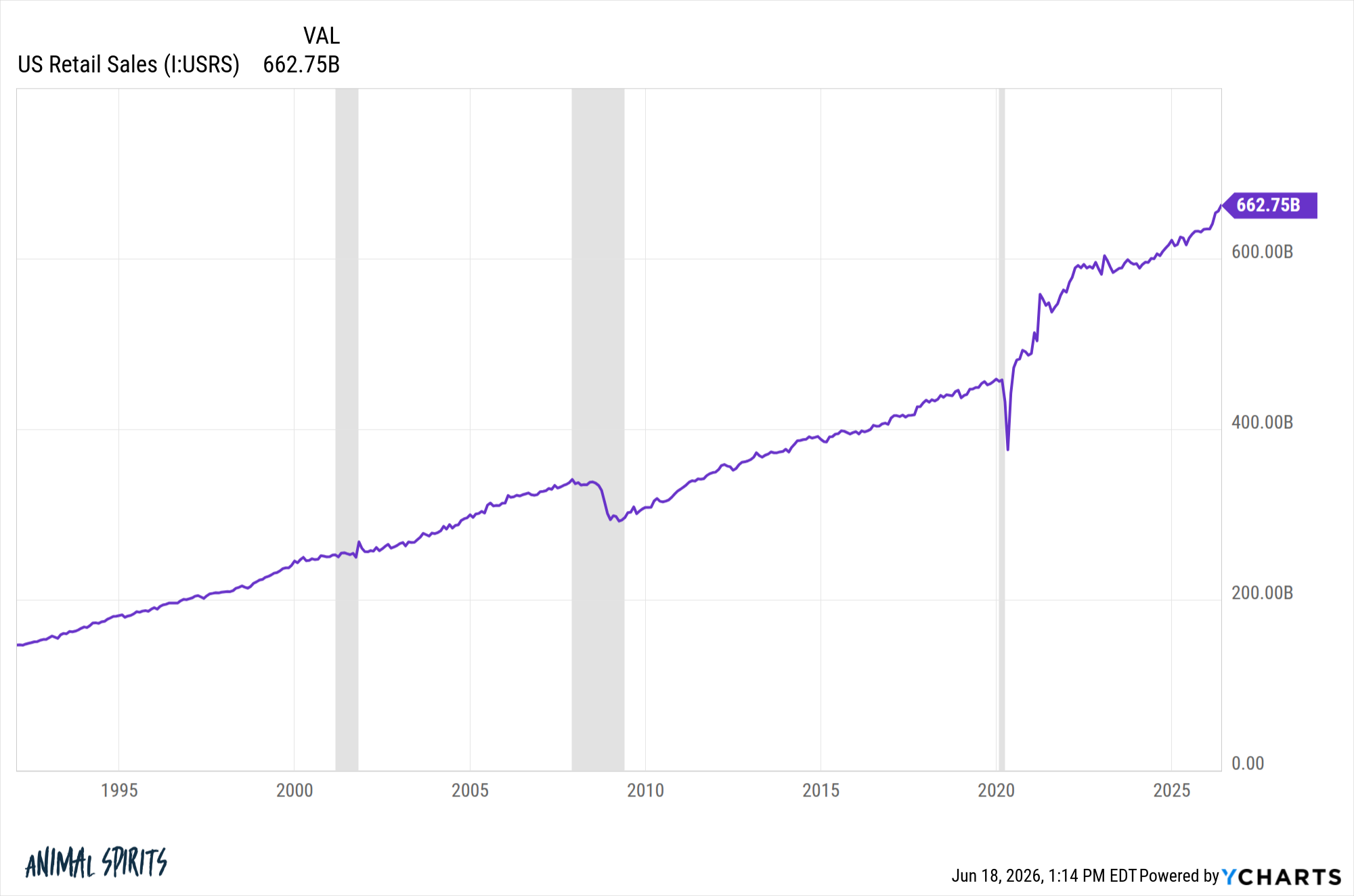

Data consistently indicates that consumer spending has not only held steady but has continued to grow, acting as a powerful engine for the economy. Whether it’s retail sales, travel, or leisure activities, households continue to open their wallets. This sustained spending has been a critical factor in preventing a more significant economic contraction, demonstrating a remarkable ability to adapt and maintain consumption patterns even in a high-cost environment. The continuous upward trend in aggregate consumer spending underscores this phenomenon, often depicted in economic charts showing robust growth since the pandemic’s initial dip.

The Elusive Recession and Corporate Confidence

The absence of a prolonged recession has been a puzzle to many. While specific sectors have faced challenges, the broader economy has demonstrated a surprising capacity for growth. This resilience is echoed in corporate boardrooms across the nation. Leading CEOs, whose companies are at the forefront of consumer interaction, consistently report strong consumer demand. Quarterly earnings calls and industry reports frequently highlight the robust health of the consumer base. For instance, statements from various corporate leaders, as compiled by industry observers, often laud the "strong consumer demand," "healthy spending patterns," and "resilient discretionary spending," painting a picture of confidence that contradicts widespread economic anxieties.

The Wealth Effect and Spending Distribution

Several factors contribute to this resilience. One significant driver is the "wealth effect." The substantial rise in financial asset values—particularly the stock market, which has seen considerable gains this decade—has made many households feel wealthier. This perceived increase in wealth often translates into greater confidence and a higher propensity to spend, even in the face of inflationary pressures.

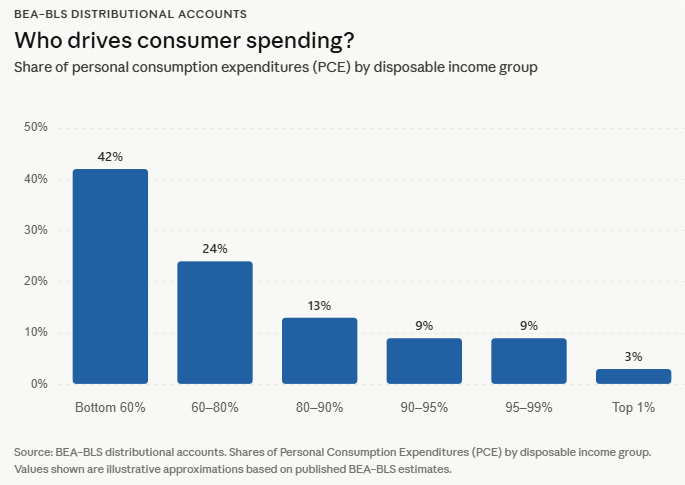

Furthermore, the narrative of a stark "K-shaped economy," where the rich thrive while the poor struggle, while capturing media attention, may not fully represent the reality of spending patterns. While wealth accumulation certainly has a K-shape, data from the Bureau of Economic Analysis (BEA) on spending distribution suggests a more nuanced picture. This data indicates that spending growth has not been as uneven across income quintiles as some narratives imply, suggesting a broader base of consumers participating in the economic expansion. This contradicts the idea that only the wealthiest are driving consumption, instead pointing to a more pervasive spending capacity across income levels.

The Unseen Anchor: The Housing Hedge

While the wealth effect and broad-based spending contribute to consumer resilience, the most powerful and often overlooked factor anchoring the economy is the "housing hedge" enjoyed by a substantial portion of American homeowners. This unique economic advantage stems from a confluence of events leading up to and during the initial phase of the pandemic.

A Generational Opportunity for Homeowners

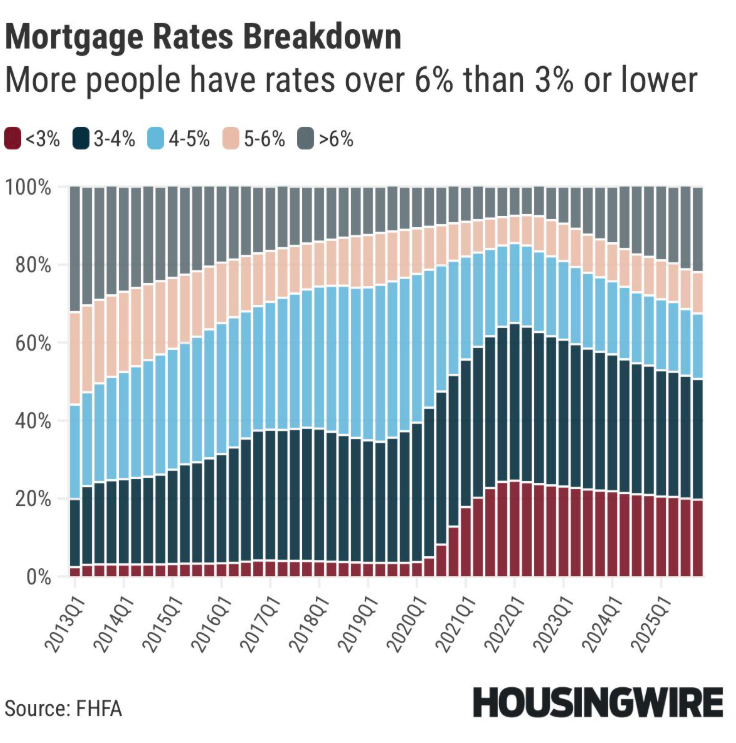

In 2020, the homeownership rate in the U.S. stood at approximately 65%, roughly where it remains today. Crucially, at that point, housing prices were significantly more affordable than current levels, and 30-year fixed mortgage rates were historically low, hovering around 3%. Millions of homeowners seized this opportunity, either purchasing homes or refinancing existing mortgages at these incredibly advantageous rates. This period offered what many now consider the "inflation hedge of the century."

Locking in an Inflation Shield

The mechanism of this hedge is straightforward yet profound. By locking in a fixed-rate mortgage at 3% or lower, homeowners secured their largest monthly expense at a historically low cost. As inflation subsequently soared to over 4% (and at times, significantly higher), the real cost of these mortgage payments effectively diminished. In an environment where the annual inflation rate surpasses the fixed interest rate on a mortgage, homeowners are, in essence, borrowing money for free on an inflation-adjusted basis. Their debt is being repaid with dollars that are worth less than when they were borrowed, providing a substantial financial buffer against rising costs elsewhere. The recent resurgence of inflation, pushing rates back above 4% due to the resilient economy and geopolitical events, only accentuates the benefit for those with ultra-low fixed mortgages.

Statistical Underpinnings of the Hedge

The scale of this phenomenon is significant. Approximately half of all borrowers currently hold mortgage rates of 4% or lower, a testament to the refinancing boom and low-rate environment of the early 2020s. Furthermore, an impressive 40% of homeowners in the U.S. own their homes free and clear, meaning they have no mortgage payment at all. When these figures are combined—nearly 90% of homeowners either have a low-rate mortgage or no mortgage at all—it becomes clear why household budgets, for a substantial segment of the population, are far less constrained than headline inflation figures might suggest.

Diverted Funds Fueling Other Sectors

The financial relief provided by these low housing costs has a ripple effect throughout the economy. Money that would otherwise be consumed by higher mortgage payments or rent can now be directed towards other forms of consumption and investment. This disposable income has fueled robust retail sales, supported the travel and hospitality sectors, and contributed to the continued flow of capital into the stock market. In essence, the housing hedge has acted as a significant stimulus, allowing millions of households to maintain their spending habits and absorb inflationary pressures on other goods and services without drastically altering their overall financial behavior. This dynamic explains why many economic forecasts, which failed to adequately account for this structural advantage, have proven inaccurate this decade.

Official Responses and Economic Interpretations

The unique economic conditions of the 2020s have presented complex challenges and opportunities for policymakers, central banks, and industry leaders.

Central Bank’s Dilemma

The Federal Reserve, tasked with managing inflation and employment, has been keenly aware of the robust consumer spending, even as it aggressively raised interest rates. Its communications have often highlighted the strength of the labor market and consumer balance sheets, while also acknowledging the persistent inflationary pressures. The "housing hedge" adds another layer of complexity to monetary policy, as higher interest rates aimed at cooling the economy have a diminished impact on the vast segment of homeowners with locked-in low rates, potentially requiring even more aggressive action to achieve desired disinflationary effects.

Government Agencies’ Economic Outlook

Government agencies like the Bureau of Economic Analysis (BEA) and the Bureau of Labor Statistics (BLS) meticulously track the data points that illustrate this paradox. Their reports on personal consumption expenditures, retail sales, and inflation rates provide the granular detail behind the consumer’s resilience. While these agencies don’t explicitly endorse the "housing hedge" theory, their data on housing costs versus other spending categories implicitly supports the idea that fixed, low housing expenses free up capital for other economic activity.

Industry Voices on Consumer Trends

The consistent reporting from CEOs, as noted earlier, serves as a powerful industry response. Whether from retail giants, travel companies, or entertainment conglomerates, the message is clear: consumer demand remains strong. These statements, often accompanied by strong revenue figures, indicate that the spending capacity extends beyond essential goods to discretionary purchases, reflecting underlying consumer confidence and financial stability for many.

Analyst Perspectives on the Housing Market

Economists and housing market analysts have increasingly focused on the "lock-in" effect of low mortgage rates. While acknowledging its positive contribution to economic stability by supporting consumer spending, they also highlight its negative implications for housing affordability and supply. New buyers face significantly higher interest rates and elevated home prices, creating a stark divide between those who entered the market pre-2022 and those attempting to enter now.

Implications and Future Outlook

The housing hedge, while a boon for current homeowners and a driver of economic stability, carries significant implications for the future, exacerbating existing inequalities and posing challenges for long-term economic planning.

The Widening Divide in the Housing Market

The most significant implication is the creation of a "real K-shaped" economy within the housing market itself. On one branch, existing homeowners with low fixed-rate mortgages benefit from appreciating asset values and effectively lower real debt burdens. On the other branch, prospective homebuyers, particularly first-time buyers, face an increasingly daunting landscape of high home prices, historically high mortgage rates, and limited inventory. This creates a severe affordability crisis for a new generation and exacerbates wealth inequality, making homeownership, once a cornerstone of the American dream, increasingly out of reach for many. Renters also face rising costs, further widening the gap.

Sustaining the Economic Momentum

The critical question now facing economists and policymakers is: how long can this housing hedge sustain robust consumer spending? While the benefits are substantial, they are not infinite. Factors such as aging mortgages (as homes are eventually sold), potential shifts in the job market, or rising property taxes and insurance costs could gradually erode the financial advantage. The longevity of these low-rate mortgages means that a significant portion of the population will continue to benefit for years, if not decades. Mike Simonsen’s analysis of housing activity suggests that the effects of this hedge could persist for a considerable period, indicating that the structural advantage is deeply embedded in the economy.

The Fading Hedge: A Critical Juncture

The "when does this hedge begin to fade?" question is central to understanding future economic trajectories. While homeowners benefit from lower monthly payments, their ability to move or upgrade is severely hampered by the prospect of trading a 3% mortgage for a 7%+ mortgage. This "golden handcuff" effect restricts housing supply, further pushing up prices for the limited available homes. As the demographic landscape shifts and existing homeowners eventually sell or refinance at higher rates, the collective economic benefit of the hedge will slowly diminish. This transition will be a critical juncture, potentially leading to a rebalancing of consumer spending priorities and a different economic growth trajectory.

Lessons from Housing Cycles

The housing market’s journey through the 21st century offers a cautionary tale about timing and luck. The 2000s began with a speculative housing bubble, fueled by loose lending practices, which subsequently burst, triggering one of the most severe financial crises in history. The 2010s, in contrast, were characterized by a period of relative housing affordability as the market recovered. The pandemic then dramatically pulled forward an enormous amount of demand and price growth, leading to the current, highly unusual situation. This historical context underscores the volatile nature of housing and how individual financial fortunes can become heavily predicated on the precise timing of market entry and leveraging opportunities. Those who "lucked into" lower prices and historically low mortgage rates received a generational financial advantage, while others now contend with a far more challenging and expensive landscape.

Policy Challenges and Economic Foresight

The current economic environment presents profound challenges for policymakers. How do you cool an economy without punishing those who are already struggling with high costs, while simultaneously addressing the structural advantages enjoyed by a large segment of the population? The difficulty of accurate economic forecasting in this unique and historically unprecedented period is immense. Understanding the nuances of the housing hedge is crucial for developing effective monetary and fiscal policies that promote broad-based economic stability and address the widening disparities in wealth and opportunity.

Conclusion

The 2020s have tested the limits of economic endurance, yet the American consumer has largely emerged unbowed. This unexpected resilience, defying numerous recessionary predictions, finds its most potent explanation in the "housing hedge." Millions of homeowners, having locked in historically low mortgage rates before the inflationary surge, have secured their largest household expense at an effectively discounted real cost. This unique advantage has freed up disposable income, sustaining consumer spending across various sectors and providing a vital anchor for the broader economy.

However, this powerful economic engine is not without its costs. It has created a stark divide within the housing market, making homeownership increasingly inaccessible for new generations and exacerbating wealth inequality. As the decade progresses, the longevity of this hedge and its eventual fade will become critical determinants of future economic stability. Understanding this complex interplay of historical timing, financial savvy, and market dynamics is paramount for navigating the ongoing economic turbulence and preparing for the inevitable shifts that lie ahead. The question is not just if the hedge will fade, but how the economy will adapt when it does.