The Spending Paradox: Why Consumers Are Defying Economic Gravity This Summer

By PYMNTS | June 19, 2026

As the United States steps into the heart of the summer season, underscored by the Juneteenth holiday weekend, a curious economic phenomenon has taken hold. The prevailing narrative of 2026 has been defined by persistent inflationary pressures and a general sense of unease regarding the broader economic climate. Yet, despite these headwinds, American consumer behavior is proving far more resilient—and nuanced—than standard forecasting models might suggest.

New data from PYMNTS Intelligence reveals a striking contradiction at the core of the modern "Cutback Economy." While the vast majority of consumers acknowledge the sting of rising prices, there is no corresponding mass retreat from the marketplace. Instead, we are witnessing a fundamental shift in how households categorize their spending, moving away from traditional merchant-defined labels toward a highly personalized hierarchy of priorities.

The Main Facts: A Disconnect Between Sentiment and Action

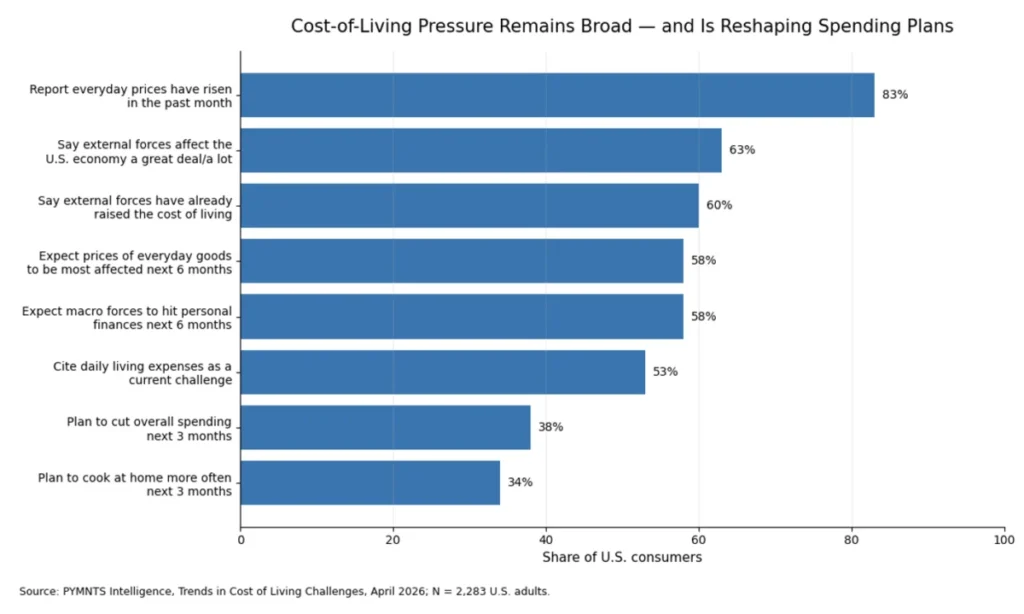

The statistical landscape of the current economy is characterized by a stark gap between perception and behavior. According to the latest research, 83% of consumers report that the cost of everyday goods has climbed over the past month. Furthermore, nearly two-thirds of the population believe that external macroeconomic forces are exerting a significant influence on the U.S. economy, with 58% of respondents expressing concern that these broader trends will directly impact their personal financial stability over the next six months.

Under conventional economic wisdom, this level of anxiety should trigger a widespread tightening of belts. However, the data tells a different story: only 38% of consumers state that they intend to reduce their spending in the coming quarter.

This creates a "spending paradox." If consumers are acutely aware of inflation and fearful of future economic volatility, why are they not preemptively cutting back? The answer lies in a departure from how economists and merchants traditionally segment budgets. Consumers are no longer viewing their expenses through the lens of "discretionary" versus "essential" as defined by market standards. Instead, they are defining these terms through the filter of their own lived experiences, family obligations, and deeply held personal values.

Chronology of the 2026 Inflationary Climate

The trajectory of the current economic environment has been a steady climb of pressure, building momentum over the first half of 2026.

- Early Q1 2026: Economic sentiment began to soften as lingering inflation in housing and services overshadowed cooling energy costs. Consumers began to signal higher levels of stress regarding future financial planning.

- April 2026: Financial institutions noted a shift in credit card utilization, with consumers increasingly relying on revolving balances for daily living expenses, suggesting that the "buffer" of pandemic-era savings had largely evaporated for the middle class.

- May 2026: PYMNTS research identified that 53% of households cited daily living expenses as their primary financial challenge, moving from a secondary concern to the top of the list for most families.

- June 2026 (Present): As the summer travel and leisure season begins, the "Cutback Economy" has matured. Consumers are now actively triaging their budgets, protecting specific categories they deem "non-negotiable" while aggressively trimming others, leading to the current paradox where total spending remains surprisingly stable despite low consumer confidence.

Supporting Data: The Anatomy of Financial Pressure

The "Cutback Economy" research paints a detailed picture of where the financial strain is concentrated. While the headline figures indicate broad discomfort, the granular data reveals where the pain is most acute:

- Daily Living Expenses (53%): The sheer cost of maintaining a household—groceries, utilities, and household supplies—remains the number one stressor for the average American family.

- The Macro Environment (44%): Nearly half of consumers feel that the systemic issues—interest rates, market volatility, and global supply chains—are dictating their personal financial outcomes.

- Housing Costs (43%): Despite cooling in some regions, the structural costs of rent and mortgages continue to absorb a disproportionate share of income.

- Future Planning and Savings (42%): A significant portion of the population is sacrificing long-term security to meet immediate, short-term needs, highlighting the erosion of the "financial safety net" for many households.

This data demonstrates that the pressure is not evenly distributed. Younger consumers and families with children are facing the highest concentration of financial stress, as they attempt to balance the immediate requirements of raising a family with the inflationary environment surrounding housing and education.

Official Perspectives: The Subjectivity of ‘Essential’ Spending

The core of the current spending mystery is a shift in psychology, a point recently underscored by PYMNTS CEO Karen Webster. As Webster has noted, "Essential isn’t a characteristic of the expense. It’s the characteristic of the person spending the money on it."

This philosophy challenges the traditional retail and banking categorization of goods. For a merchant, a purchase is a category—an airline ticket is "travel," a restaurant meal is "dining," and a subscription is "entertainment." For the consumer, these labels are often irrelevant.

For instance, consider the working parent who utilizes grocery delivery services. While a corporate analyst might flag this as a "convenience" or "discretionary" expenditure, the household views it as a "necessary" utility that facilitates their ability to work and maintain childcare. Conversely, private school tuition might be considered an "essential" investment for one household, while another family in the exact same income bracket might view it as an entirely "discretionary" luxury that could be cut at a moment’s notice.

This subjective hierarchy means that merchants and financial institutions can no longer rely on simple demographic or category-based segmentation to predict churn or loyalty.

Implications for the Future: A New Strategic Framework

The implications of this shift are profound for retailers, financial institutions, and loyalty program managers. If consumers are shielding their spending based on personal values rather than retail categories, the businesses that succeed will be those that identify these "protected" categories.

1. Reimagining Loyalty Programs

Traditional loyalty programs often reward customers for spending within a specific category, such as travel or dining. However, if a consumer has deemed "family-related expenses" as the protected pillar of their budget, a rewards program that aligns with those specific, non-negotiable expenses—such as groceries, childcare support, or home maintenance—will see significantly higher retention rates. Loyalty is no longer about the transaction; it is about supporting the customer’s self-defined priorities.

2. The Evolution of Installment Products

Buy Now, Pay Later (BNPL) and other installment solutions have historically been associated with the retail sector, specifically for discretionary purchases like fashion or electronics. The current data suggests a massive, untapped opportunity for these products to migrate into the "protected" category space. Helping consumers manage large, recurring, and essential expenses—such as childcare, healthcare, or home repairs—through flexible financing could be a lifeline for households looking to maintain their standard of living without resorting to high-interest credit cards.

3. Precision Forecasting

For retailers, the summer of 2026 serves as a warning against relying on aggregated data. A business that assumes all "discretionary" spending will drop is likely to lose market share. Instead, firms must pivot toward understanding the "why" behind the purchase. By leveraging first-party data to understand a customer’s specific spending patterns, brands can tailor their messaging to address how their product fits into the consumer’s hierarchy of priorities.

Conclusion: The Resilient Consumer

As the summer progresses, the economy remains in a state of delicate equilibrium. We are not seeing a collapse of consumer confidence, nor are we seeing a return to the carefree spending habits of years past. Instead, we are observing a more sophisticated, highly intentional consumer who is navigating the inflationary environment with a clear sense of what they value most.

The "Cutback Economy" is not a story of total withdrawal; it is a story of recalibration. By recognizing that today’s consumer is prioritizing their spending based on their own unique circumstances, businesses have a unique opportunity to provide the tools, rewards, and support that match these evolving priorities. As we look toward the remainder of the year, the winners will be those who stop looking at consumers as aggregate data points and start seeing them as individuals managing a complex, personal, and highly protected budget.