Raising Financially Literate Children: The “Frugalwoods” Philosophy on Money Management

In an era defined by seamless digital transactions and the constant bombardment of consumer-driven marketing, the task of teaching children the value of a dollar has become increasingly complex. For many parents, the county fair—with its dizzying array of midway games, overpriced trinkets, and sugary indulgences—represents a battlefield of impulse control. However, for those who view these experiences through the lens of intentional parenting, such venues are not merely distractions; they are invaluable laboratories for financial education.

By utilizing everyday scenarios, parents can demystify the abstract nature of money. Recent insights from the "Frugalwoods" approach—a methodology centered on intentionality, chore-based compensation, and the separation of "needs" versus "wants"—offer a blueprint for raising financially literate children in a consumer-centric society.

The Core Philosophy: Needs Versus Discretionary Spending

The cornerstone of this pedagogical approach is a clear, unwavering distinction between the parent’s responsibilities and the child’s financial autonomy. At its simplest level, the "family money philosophy" establishes that parents are the providers of life’s essentials. This includes housing, clothing, healthcare, education, and nutrition. By covering these fundamental needs, parents create a stable foundation that allows children to focus their personal funds on discretionary items.

This structure is not merely about rules; it is about empowerment. When a five- or seven-year-old learns that their parents will pay for a museum entrance fee but not for a souvenir in the gift shop, they are being introduced to the concept of the "opportunity cost." This creates a scenario where the child must evaluate whether a plastic toy is worth the hours of effort required to earn the purchase price. By limiting the scope of parental spending, parents force children to prioritize, deliberate, and ultimately, take ownership of their financial decisions.

Chronology of Financial Maturity: From Chores to Contracts

Financial education is, by nature, a developmental process. It requires a scaffolding approach, where lessons are introduced only when the child possesses the cognitive maturity to grasp them.

1. The Early Years: The Mechanics of Exchange

For younger children, the initial lesson is purely mechanical. It involves recognizing coin denominations, understanding the basic concept of price, and learning the rudimentary link between labor and capital. The "Frugalwoods" method posits that children rarely consider that their parents are paid to perform their jobs. By explaining that a cart full of groceries is the tangible result of a certain number of hours worked, parents begin to bridge the gap between abstract currency and real-world effort.

2. Intermediate Lessons: The Reality of Debt

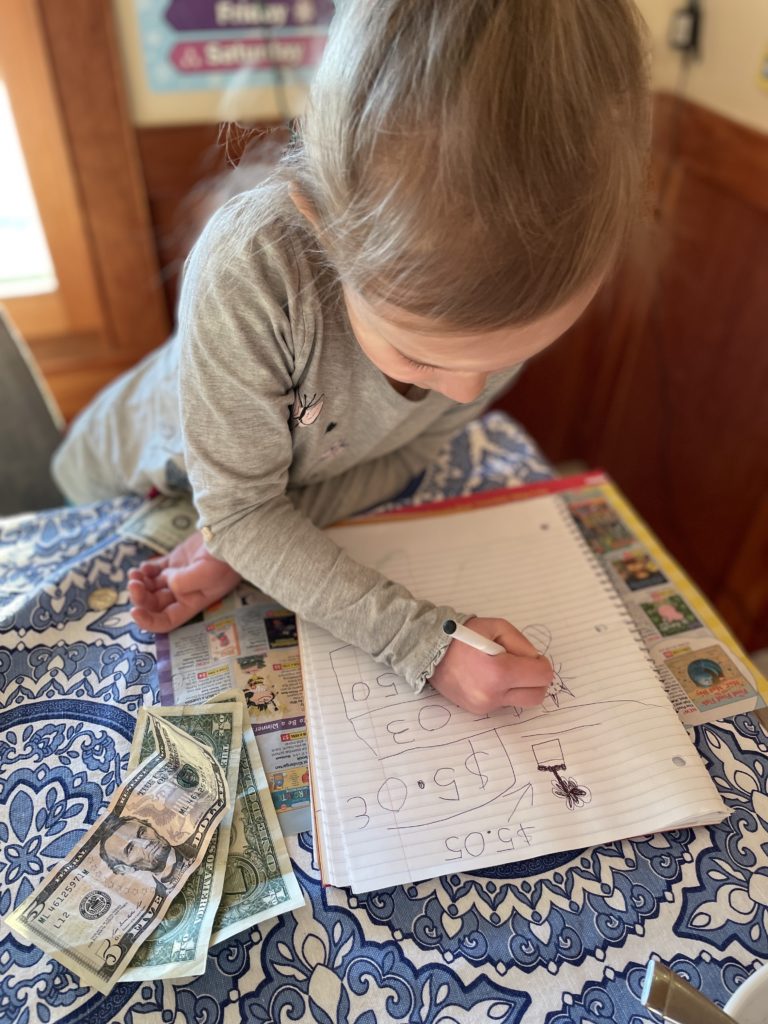

A pivotal moment in this education occurs when a child attempts to spend more than they possess. In one documented instance, a child opted to go into debt to purchase a desired toy, agreeing to pay back the difference through future labor. The experience of working off a debt—a process that the child described as "not fun" because they were working for something they already owned—served as a visceral, formative lesson. It taught the child that debt is not an abstract concept but a constraint on one’s future time and freedom.

3. Advanced Autonomy: Real-World Transactions

As children grow, the complexity of their financial interactions increases. This involves allowing them to handle their own money in public spaces, such as ordering and paying for their own dessert at a restaurant. By forcing the child to navigate the social and mathematical pressures of a transaction, parents prepare them for adult independence.

Supporting Data: Why Direct Experience Matters

Research in child development consistently suggests that children learn best through experiential, hands-on activities rather than lectures. When a child misplaces a wallet at a museum and is tasked with finding it, they learn the importance of asset management in a way that no amount of cautionary advice could achieve.

The "chore-based compensation" model serves as the primary data-gathering tool for these children. By differentiating between "daily life chores" (which are unpaid contributions to family well-being) and "value-added chores" (which are paid projects like organizing a pantry), parents provide a clear look at how labor markets function. This structure also prevents children from becoming entitled to payment for basic domestic participation, maintaining a healthy balance between household duty and individual enterprise.

Implications for Future Financial Well-being

The long-term implications of these early lessons are significant. By stripping away the anxiety and judgment that often surround money, parents can frame currency as a tool—much like exercise, nutrition, or sleep. When money is demystified, it ceases to be a source of status or emotional validation and becomes a mechanism for achieving life goals.

The transition from a "spending-only" mindset to a "savings-oriented" mindset is the next hurdle. Introducing the concept of a "Bank of Parental Units" that pays interest is an effective strategy for transitioning from short-term gratification to long-term wealth accumulation. This evolution allows children to see how their money can grow over time, introducing the foundational concept of compounding interest in a low-stakes, highly supervised environment.

Expert and Parental Perspectives on Early Education

While the "Frugalwoods" approach emphasizes autonomy, it is not without its critics. Some child psychologists argue that tying money to chores can undermine intrinsic motivation—the desire to do a job well simply because it is helpful. However, proponents argue that in a capitalist society, understanding the "fair market value" of labor is a prerequisite for success.

The consensus among modern financial educators is that the "how" matters more than the "what." Whether parents use a physical piggy bank, a digital ledger, or a "Bank of Mom and Dad," the primary goal remains the same: to reduce the mystery of money. By bringing children into the conversation early, parents remove the shame associated with financial mistakes. If a child loses their money, the loss is painful but limited; if they learn that lesson at age 30, the consequences are far more severe.

Conclusion: Preparing for an Independent Future

Teaching children about money is an ongoing, iterative process. It is not about turning children into junior financiers, but rather about ensuring they are not surprised by the mechanisms of the world when they reach adulthood.

By consistently reinforcing that money is a limited resource gained through effort and spent through choice, parents provide their children with the most valuable asset of all: financial agency. As children move from the county fair midway to the real-world economy, they will carry with them the lessons of their childhood—that value is earned, that debt is a burden, and that money, ultimately, is just a tool to be managed with wisdom and foresight.

As we look toward the future, the integration of long-term savings strategies, such as interest-bearing accounts, will mark the next chapter in this journey. By the time these children reach adulthood, they will not only understand how to spend money; they will understand how to build a life around their values, using their financial resources to support their goals rather than being controlled by them.