The Silent Tax Bomb: Why Retirement Planning Must Account for the "Widow’s Penalty" and Heirs’ Burdens

For millions of Americans, the traditional retirement strategy—contribute to a 401(k) or IRA, let it grow, and withdraw in retirement—is a cornerstone of financial security. However, this approach carries a hidden, ticking time bomb: the reality that every dollar withdrawn from a traditional tax-deferred retirement account is eventually subject to income tax. As the national debt climbs toward $39 trillion and the political landscape regarding tax policy remains uncertain, retirees are discovering that their greatest asset may also be a significant liability.

The most acute risk arises from a phenomenon often referred to by financial planners as the "widow’s penalty." When a spouse passes away, the surviving partner faces a double-edged sword: a reduction in total household income, often coupled with a transition from a favorable joint-filing tax status to a more punitive single-filer status. Without proactive intervention, this transition can force a surviving spouse into a significantly higher tax bracket, effectively turning their retirement nest egg into a source of involuntary tax leakage.

The Mechanics of the "Widow’s Penalty"

To understand the scope of the problem, one must examine the interaction between Social Security benefits and federal income tax brackets.

The Financial Shift: A Case Study

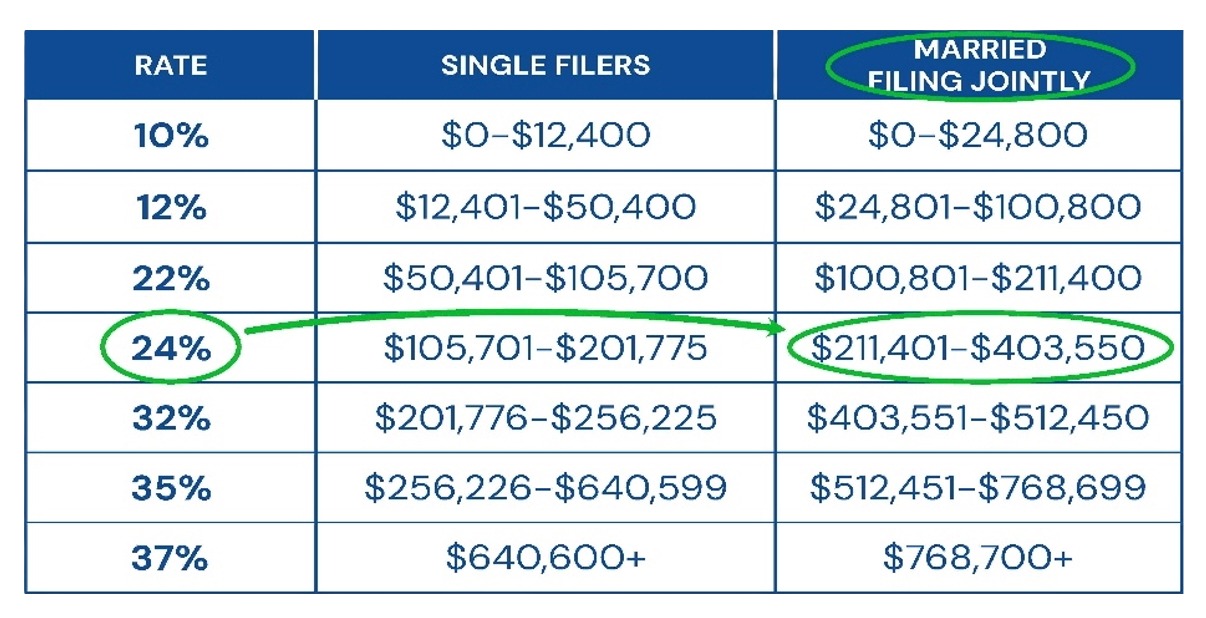

Consider a married couple with a combined annual income of $200,000. Under current tax structures, this household benefits from the wider tax brackets afforded to those filing jointly, placing them in an effective tax bracket of approximately 15%.

When one spouse passes away, the surviving spouse experiences a drop in income—typically losing the smaller of the two Social Security checks. While the income may decrease to $180,000, the tax reality changes dramatically. The survivor must now file as a single taxpayer. Because the tax brackets for single filers are narrower, that same $180,000 income can vault the survivor into a 20% or even 24% tax bracket.

This is not merely a hypothetical scenario; it is a structural reality of the U.S. tax code. As Required Minimum Distributions (RMDs) kick in and the survivor’s taxable income continues to grow, the tax rate can climb further, compounded by the possibility of future federal tax hikes intended to address the mounting national debt.

Chronology of Tax Exposure: From Retirement to Legacy

The lifecycle of a retirement account involves three distinct phases where tax exposure shifts, often in ways that catch retirees off guard.

Phase 1: The Accumulation and Joint-Filing Years

During the peak of their careers and the early years of retirement, couples often enjoy the benefits of joint filing. They maximize standard deductions, including the $32,200 standard deduction for married couples, and utilize additional senior-specific deductions for those over age 65. Under current law, seniors over 65 receive an additional $1,650 per spouse in standard deductions, plus a potential $12,000 "bonus" deduction, providing a significant shield against taxable income.

Phase 2: The Transition of Widowhood

The sudden death of a spouse serves as a trigger event. The immediate loss of the "married filing jointly" status often results in a massive tax bracket jump. For example, a couple with $250,000 in taxable income might comfortably sit within the 24% bracket. Upon the death of the husband, the surviving wife, now filing as a single person with that same $250,000 income, could see her marginal tax rate leap to 32% or higher.

Phase 3: The Legacy Burden

When a retiree passes away and leaves a traditional IRA to their children, the burden shifts to the next generation. Under current IRS regulations, heirs are subject to the "10-year rule," which mandates that inherited IRAs must be fully emptied within a decade of the account owner’s death.

If an IRA grows at 4% annually, an heir might be forced to withdraw approximately 14% of the balance each year to satisfy the 10-year depletion requirement. If that heir is already in their peak earning years, this influx of taxable income could push them into an even higher tax bracket, effectively forcing them to pay a premium to access the inheritance.

Supporting Data and Strategic Mitigation

The core of the problem lies in the "tax-deferred" nature of traditional accounts. While deferring taxes allows for growth on the gross amount, it essentially creates a tax debt that is guaranteed to come due.

The Case for Partial Roth Conversions

Proactive tax planning, specifically through partial Roth IRA conversions, offers a way to mitigate these risks. By converting a portion of a traditional IRA to a Roth IRA, a taxpayer pays income taxes on the converted amount today. While this creates a current tax bill, it serves two critical long-term functions:

- Locking in Tax Rates: By paying taxes now, the taxpayer secures today’s tax rates. If tax rates rise in the future to combat national debt, the Roth conversion acts as a hedge.

- Tax-Free Growth for Survivors: Once funds are in a Roth IRA, they grow tax-free, and withdrawals—both for the original owner and eventually for the heirs—are generally tax-free.

The Role of Technology in Tax Optimization

Modern financial planning now utilizes sophisticated software, such as Holistiplan, to perform "tax bracket harvesting." These tools allow advisors to model exact withdrawal amounts year-by-year, ensuring that retirees fill up lower tax brackets without unnecessarily pushing themselves into higher ones. This level of precision is essential for implementing a "Strategic Roth Integration" (SRI) plan, which aims to optimize the tax impact over the long term rather than focusing on short-term gains.

Implications for Heirs and State Tax Exposure

The burden of an inherited IRA is not limited to federal income tax. State income taxes can compound the issue significantly. In states like New York, where the top state income tax bracket can reach 10.9%, an heir could face a combined federal and state tax hit of over 40% on inherited retirement assets.

For parents looking to leave a meaningful legacy, the prospect of having nearly half of that legacy eroded by taxes is a powerful motivator for pre-death planning. Converting traditional assets to Roth assets while the original owner is alive—and perhaps in a lower tax bracket than their high-earning children—can be one of the most efficient ways to transfer wealth.

Official Guidance and Professional Oversight

The complexity of these tax maneuvers underscores the necessity of working with qualified financial advisors and tax professionals. The IRS does not provide exceptions for the loss of a spouse, and the 10-year rule for non-spouse beneficiaries is strictly enforced.

Investors are encouraged to verify the credentials of any advisor proposing these strategies. The SEC’s Investment Adviser Public Disclosure (IAPD) website and FINRA’s BrokerCheck are essential tools for ensuring that the person providing advice has a clean regulatory history and the necessary expertise to handle complex tax-integration strategies.

Conclusion: The Case for Proactivity

The "widow’s penalty" and the tax trap faced by heirs are not inevitable consequences of retirement, but they are common outcomes of passive financial planning. As tax policies evolve and the fiscal pressure on the federal government increases, the traditional strategy of "defer, defer, defer" may prove to be a costly mistake.

By transitioning from a mindset of simple accumulation to one of deliberate tax management, retirees can protect their surviving spouses and their children from unnecessary tax burdens. Whether through partial Roth conversions, strategic income planning, or a comprehensive review of tax brackets, the goal is clear: to ensure that the wealth you built is preserved for your family, rather than surrendered to the government through structural tax traps.