The Quest for Early Retirement: Navigating Asset Allocation in the FIRE Movement

A burgeoning movement toward Financial Independence, Retire Early (FIRE) has captivated a generation of ambitious savers and investors. Central to achieving FIRE is a meticulously crafted investment strategy, and a common dilemma often arises concerning the optimal allocation of assets, particularly between bonds and cash. A reader, mid-30s and aiming for retirement by 40, recently posed a pertinent question: Is it prudent to forgo bonds entirely in favor of a substantial cash position (equivalent to two years of expenses in a high-yield savings account) while maintaining an aggressive mix of US and international ETFs? This query cuts to the heart of asset allocation, challenging traditional diversification wisdom and prompting a deeper examination of the "barbell portfolio" approach.

Unpacking the "Barbell Portfolio": Stocks on One End, Cash on the Other

The reader’s proposed strategy aligns with what financial professionals often term a "barbell portfolio." This approach involves concentrating investments at the two extremes of the risk spectrum: highly volatile, growth-oriented assets like stocks (or equity ETFs in this case) on one end, and extremely low-risk, capital-preserving assets like cash on the other. This contrasts with a more traditional diversified portfolio that typically includes a significant allocation to intermediate-risk assets such as bonds, which are often considered to occupy the middle ground between stocks and cash.

The Core Premise: Extremes of Risk and Safety

The philosophy behind the barbell strategy, famously popularized by Nassim Nicholas Taleb, is to achieve resilience by being extremely conservative where it matters (the cash buffer) and extremely aggressive where it offers potential for high returns (the equity portion). The idea is that the "safe" end protects against catastrophic loss and provides liquidity, while the "risky" end captures market upside. For FIRE aspirants, this means ensuring a buffer against immediate spending needs and sequence of returns risk (the danger of withdrawing funds during a market downturn early in retirement) without diluting potential growth with moderate-return, potentially volatile bonds.

Cash Equivalents: The Safe Anchor

The "cash" component in such a portfolio isn’t necessarily just checking account balances. It typically encompasses a range of highly liquid, low-risk instruments. These include:

- High-Yield Savings Accounts (HYSAs): Offer better interest rates than traditional savings accounts while maintaining immediate liquidity.

- Money Market Funds (MMFs): Invest in short-term, highly liquid debt instruments, providing competitive yields with high stability.

- Treasury Bills (T-bills): Short-term debt obligations of the U.S. government, considered among the safest investments globally due to their minimal default risk and short duration, which reduces interest rate sensitivity.

- Certificates of Deposit (CDs): Time deposits that offer a fixed interest rate for a specified period, typically ranging from a few months to several years. While less liquid than HYSAs or MMFs, they offer predictable returns for specific durations.

The reader’s preference for a high-yield savings account as their cash equivalent is a common choice, valuing liquidity and a modest yield.

Historical Performance: A Look Through the Rearview Mirror

To assess the reader’s strategy, it’s crucial to examine the historical performance of these asset classes. While past performance is no guarantee of future results, it provides invaluable context regarding risk and return characteristics.

Nominal Returns: Stocks Lead, Bonds and Cash Compete Closely

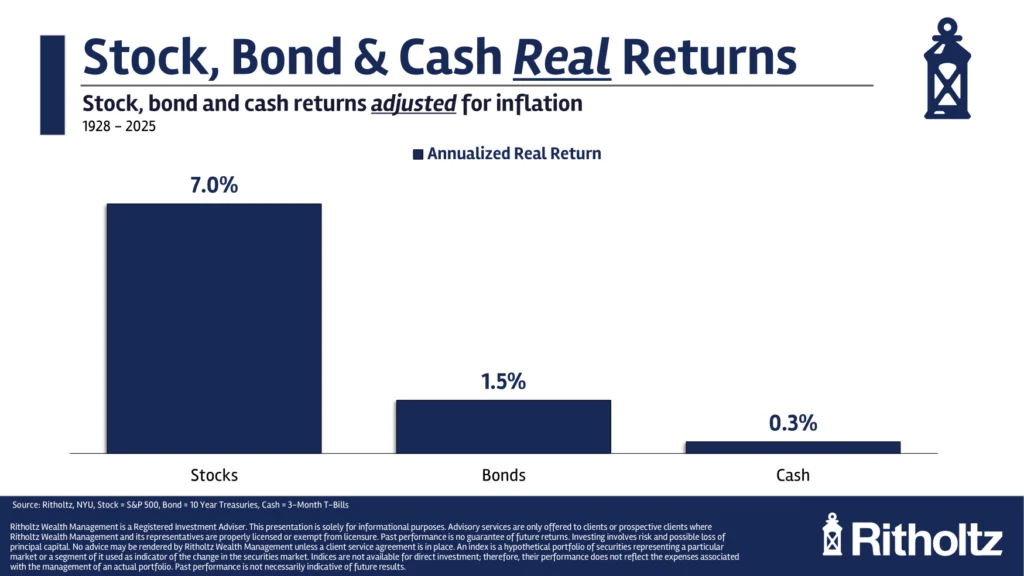

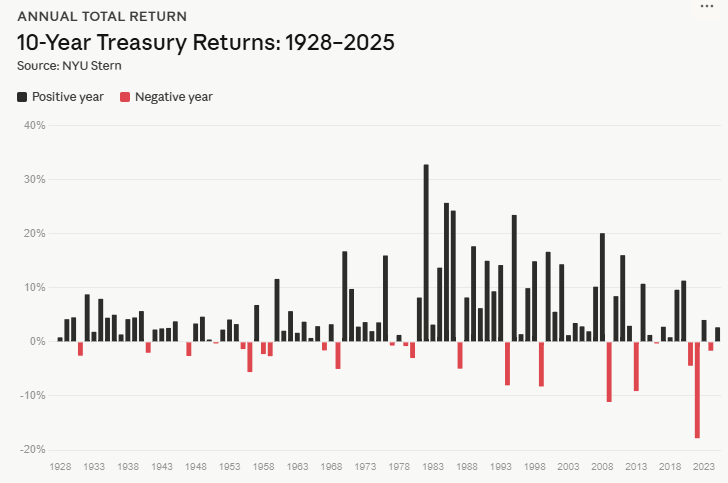

Over the very long haul, stocks have consistently delivered the highest nominal returns. However, the performance differential between bonds and cash has often been less pronounced than many investors might assume. Historically, bonds have typically offered a slight edge over cash in terms of nominal returns, but cash has not been a distant third, often keeping pace or even outperforming bonds in specific market environments. The key distinction lies in the volatility profile: cash (specifically T-bills) has historically shown remarkable stability, with virtually no "down years" in nominal terms, whereas bonds, despite their lower risk profile compared to stocks, can experience periods of significant negative returns.

The Inflationary Reality: Real Returns and Erosion of Purchasing Power

The true measure of an investment’s success is its "real return"—the return after accounting for inflation. When adjusted for inflation, the picture shifts somewhat. While cash has generally managed to keep pace with inflation over time, its real return has often been negligible, hovering just above zero. This means that while the nominal value of cash has been preserved, its purchasing power has seen only marginal growth, or in some periods, even a slight erosion. Bonds, while also susceptible to inflation, have historically offered a slightly better real return than cash, particularly longer-duration bonds in periods of stable or declining interest rates. The "leaving money on the table" concern for the reader primarily revolves around this potential for bonds to offer a superior real return compared to cash, especially when considering the opportunity cost over a multi-decade retirement horizon.

Bonds vs. Cash: A Dynamic Tug-of-War Across Economic Cycles

The decision between bonds and cash is not static; their relative attractiveness fluctuates significantly with economic cycles, interest rate environments, and inflationary pressures. Understanding these historical divergences is key to appreciating the complexities of asset allocation.

The Bond Bear Market of 2022: A Catalyst for Cash’s Appeal

The year 2022 served as a stark reminder of bonds’ vulnerabilities. Rapidly rising interest rates, coupled with surging inflation, created a "perfect storm" for many bond investors. Long-term government bonds, particularly susceptible to interest rate risk, experienced substantial declines. In contrast, short-term Treasury bills (a form of cash equivalent) performed remarkably well, offering positive returns as their yields quickly adjusted upwards with Federal Reserve rate hikes. This period highlighted the critical difference: cash-like positions, with their minimal interest rate sensitivity, offer protection when rates are rising rapidly, a scenario that can devastate longer-duration bonds. For many investors, this recent experience has fueled a skepticism towards bonds, making the barbell approach with a larger cash component seem more appealing.

Post-GFC Era (2008-2021): When Cash Was "Trash"

However, recency bias can be misleading. The period following the 2008 Global Financial Crisis (GFC) until roughly 2021 presented a dramatically different landscape. Central banks, notably the U.S. Federal Reserve, implemented unprecedented monetary policies, keeping short-term interest rates near zero for an extended period. In this environment, cash was indeed "trash," offering negligible returns that often failed to keep pace with even modest inflation. The average 3-month T-bill yield from 2008 to 2021 was a mere 0.55% annually. During the same timeframe, the 10-year Treasury bond yielded significantly more, averaging around 4% per year, making a clear case for bonds over cash. This era demonstrated the primary risk of a large cash allocation: significant opportunity cost during prolonged periods of low short-term rates.

The Great Depression & WWII (1932-1954): Bonds Outperform in Financial Repression

Looking further back, historical data reveals other compelling cycles. The period from 1932 through 1954, encompassing the Great Depression and World War II, was characterized by "financial repression" – a prolonged era of ultra-low short-term interest rates imposed by government policy. During this time, cash significantly underperformed bonds. Bonds offered better returns, even if real returns were sometimes challenged by inflation (which averaged 2.7% per year). This scenario illustrates that government intervention and policy decisions can create prolonged environments where cash is severely disadvantaged relative to longer-term fixed income.

The Great Inflation (1966-1981): Cash Reigns Supreme

Conversely, the high-inflationary period from 1966 to 1981 saw cash emerge as the superior performer. As inflation soared and the Federal Reserve aggressively hiked interest rates (the "Volcker Shock"), longer-term bonds were severely punished. Their fixed interest payments were eroded by inflation, and their market value plummeted as new bonds offered much higher yields. Short-term cash instruments, however, benefited from the rapidly adjusting interest rates. Their yields quickly reset upwards, allowing them to better keep pace with, and in some instances even exceed, the rate of inflation, thereby preserving purchasing power more effectively than long-term bonds.

Understanding the Underlying Drivers: Interest Rates and Inflation

These historical episodes underscore the cyclical nature of fixed-income performance. The big risk for bonds, particularly those with longer durations, is rapidly rising interest rates, which erode their value. The big risk for cash is a prolonged period of the Federal Reserve (or other central banks) keeping short-term rates extremely low, leading to significant opportunity cost and potential erosion of real value due to inflation. High inflation, in general, poses a threat to both bonds and cash, though their responses differ based on duration and rate sensitivity.

The Risks and Rewards: Weighing the Trade-offs

The choice between a significant cash buffer and a traditional bond allocation boils down to a careful weighing of distinct risks and rewards.

The Allure of Cash: Liquidity, Stability, and Psychological Comfort

For the FIRE enthusiast, a substantial cash position offers undeniable advantages:

- Unparalleled Liquidity: Two years of expenses in cash provides immediate access to funds without needing to sell investments during market downturns, a critical factor for early retirees.

- Nominal Capital Preservation: Cash offers almost perfect nominal capital preservation. Barring bank failures (which are largely mitigated by FDIC insurance), the dollar amount of your cash savings will not decline.

- Psychological Comfort: Knowing that living expenses are covered for an extended period, regardless of market volatility, can significantly reduce financial stress and help investors stick to their long-term equity strategy during bear markets. This can prevent panic selling, which is often detrimental to long-term returns.

- Dry Powder: A large cash reserve can serve as "dry powder," allowing an investor to capitalize on significant market corrections by deploying capital into undervalued assets.

The Downsides of Cash: Opportunity Cost and Inflation Risk

Despite its benefits, a large cash allocation carries significant drawbacks:

- Opportunity Cost: This is the reader’s primary concern. In periods where bonds or other lower-risk alternatives offer higher real returns, holding excessive cash means "leaving money on the table." Over decades of retirement, even a seemingly small difference in annual returns can compound into a substantial sum.

- Inflation Erosion: While cash can keep pace with inflation in some environments, it frequently struggles to provide meaningful real returns. During periods of sustained high inflation, the purchasing power of a fixed cash sum can diminish significantly, even if the nominal amount remains constant.

- Low Yield Environments: As seen post-GFC, central bank policies can lead to prolonged periods of near-zero short-term interest rates, making cash a poor investment for growth or even maintaining purchasing power.

The Case for Bonds: Diversification, Income, and Deflation Hedge

Traditional portfolio theory strongly advocates for bonds due to their unique characteristics:

- Diversification and Negative Correlation: Historically, bonds (especially government bonds) have often exhibited a negative correlation with stocks, meaning they tend to perform well when stocks perform poorly. This "flight to safety" property helps dampen overall portfolio volatility and protect capital during equity market downturns.

- Income Generation: Bonds provide a predictable stream of income through interest payments, which can be a valuable component of a retirement income strategy.

- Deflation Hedge: In deflationary environments, bonds (especially high-quality government bonds) tend to perform very well. As prices fall, the purchasing power of their fixed interest payments and principal increases, and interest rates often decline, boosting bond prices.

- Lower Volatility than Stocks: While bonds can have down years, their volatility is generally much lower than that of stocks, making them a smoother ride for capital preservation.

The Vulnerabilities of Bonds: Interest Rate and Inflationary Pressures

However, bonds are not without their risks:

- Interest Rate Risk: The primary risk for bondholders is that rising interest rates will decrease the market value of existing bonds. Bonds with longer durations are more sensitive to these rate changes.

- Inflation Risk: Fixed-rate bonds are vulnerable to inflation, as rising prices erode the purchasing power of their future interest payments and principal. This is particularly true for longer-term bonds without inflation protection.

- Credit Risk: While government bonds carry minimal credit risk (default), corporate bonds and high-yield (junk) bonds carry the risk that the issuer may default on their payments.

Implications for FIRE Enthusiasts: Crafting a Robust Retirement Strategy

For individuals pursuing FIRE, the asset allocation decision is particularly acute due to the longer time horizon in retirement and the critical need to manage various risks.

The Sequence of Returns Risk: A Critical Consideration for Early Retirees

Sequence of returns risk is paramount for early retirees. If a significant market downturn occurs early in retirement, heavy withdrawals from a portfolio primarily composed of stocks can permanently impair the portfolio’s ability to recover, potentially leading to premature depletion of funds. A substantial cash buffer, like the two years of expenses the reader proposes, directly addresses this risk. It allows the retiree to draw from cash during downturns, avoiding the need to sell equities at depressed prices, thereby giving the equity portion of the portfolio time to recover.

The Role of a Cash Buffer: More Than Just a Savings Account

The proposed two-year cash buffer serves a vital function beyond simple liquidity. It acts as a defensive shield, providing stability and flexibility in the initial, most vulnerable years of retirement. This aligns with "bucket strategies" where retirees segment their assets into different risk categories based on when the funds will be needed. The first bucket, covering immediate expenses, is typically held in cash or cash equivalents.

Beyond Simple Returns: The Importance of Personal Risk Tolerance

Ultimately, the "best" strategy is highly personal. While historical returns and financial theory provide a framework, individual risk tolerance, psychological comfort, and specific retirement goals play a dominant role. For an investor who is genuinely uncomfortable with bond market volatility, even if it’s less than stock volatility, and prefers the absolute stability of cash, then a barbell approach with a larger cash component might lead to better long-term outcomes because it increases the likelihood they will stick to their plan during stressful times. The "best" portfolio is one you can stick with.

Official Responses and Expert Perspectives

While the original article is itself an expert’s response, it’s worth noting how this barbell approach fits within the broader financial planning community. Traditional financial planning, rooted in Modern Portfolio Theory (MPT), often advocates for diversification across a range of asset classes, including a significant bond allocation, to optimize risk-adjusted returns. MPT suggests that combining imperfectly correlated assets (like stocks and bonds) can achieve a higher return for a given level of risk, or a lower risk for a given level of return, than either asset class alone.

However, the barbell strategy, while a deviation from strict MPT, is gaining traction among certain practitioners, especially for those in or near retirement. The logic of extreme safety for immediate needs and extreme growth for long-term capital appreciation resonates with many, particularly in light of recent bond market performance. Many financial advisors now incorporate a substantial cash buffer into retirement planning, recognizing its role in mitigating sequence of returns risk and providing psychological comfort. The debate isn’t necessarily about bonds or cash, but rather the optimal blend and duration of fixed-income exposure versus highly liquid cash. For some, short-duration bonds (which behave more like cash) might replace longer-duration bonds, providing a modest yield premium with less interest rate risk.

The consensus remains that some form of defensive asset is crucial. Whether that is a large cash allocation, short-term bonds, or a mix, depends on the individual’s specific circumstances, their proximity to retirement, their personal conviction in their strategy, and their ability to withstand potential opportunity costs. The "leaving money on the table" argument is valid, but the "peace of mind" and "risk mitigation" arguments for cash are equally powerful, especially for those stepping away from a regular paycheck.

Conclusion: A Personalized Approach to Financial Independence

The reader’s question highlights a sophisticated understanding of investment choices for FIRE. While the historical data unequivocally shows that stocks offer the highest long-term returns, the composition of the "safe" portion of a portfolio—whether cash or bonds—is a nuanced decision. Both asset classes carry distinct risks and offer unique advantages depending on the prevailing economic climate and the investor’s individual circumstances.

The barbell portfolio, with its emphasis on a substantial cash reserve for liquidity and downside protection combined with aggressive equity exposure for growth, presents a compelling alternative to traditional bond allocations, especially for FIRE adherents facing sequence of returns risk. While it might involve "leaving money on the table" in certain periods where bonds outperform, it could equally prevent catastrophic losses during market downturns or provide the psychological fortitude needed to remain invested in equities.

Ultimately, there is no single "right" answer. The decision should be informed by a deep understanding of historical performance, current market conditions, and a frank assessment of personal risk tolerance, liquidity needs, and the specific goals of the FIRE journey. For the diligent FIRE aspirant, a strategy that offers both robust growth potential and peace of mind in volatile markets is priceless, even if it means foregoing some potential yield from bonds in favor of the unwavering stability of a well-funded cash buffer.