The Perpetual Pulse of Panic: Why June Ignites the Bubble Debate and What History Tells Us

Posted: June 21, 2026, by Ben Carlson

June, it seems, has become the unofficial month for seasoned fund managers and market prognosticators to sound the alarm on impending financial bubbles. With the market narrative increasingly dominated by the explosive growth of artificial intelligence (AI), a chorus of influential voices has once again risen to declare the current environment a historic bubble, reminiscent of past speculative manias. Yet, as history repeatedly demonstrates, identifying a bubble is one thing; consistently predicting its precise bursting point is an entirely different, and often elusive, endeavor.

This article delves into the latest wave of bubble calls, dissects the arguments presented by prominent figures like Jim Grant, Jim Chanos, Jeremy Grantham, and Ray Dalio, and critically examines these predictions against a backdrop of historical market cycles and unfulfilled prophecies. We will explore the characteristics commonly associated with bubbles, the psychological impact of such warnings, and the enduring challenge for investors to distinguish between legitimate concern and perennial pessimism.

The Chorus of Bubble Alarms: AI at the Epicenter

The prevailing sentiment among a segment of the financial elite points squarely at the Artificial Intelligence sector as the epicenter of the current speculative frenzy. Their warnings, delivered across podcasts, interviews, and detailed reports, paint a vivid picture of a market detached from fundamental realities.

Veteran financial observer Jim Grant, for instance, recently articulated his profound concerns on Meb Faber’s podcast, labeling the AI phenomenon as "one of the greatest bubbles of all-time." Grant, known for his contrarian views and deep understanding of financial history, draws parallels to previous eras of irrational exuberance, suggesting that the current enthusiasm for AI shares many hallmarks of unsustainable speculative growth. His pronouncements often carry significant weight, given his track record of prescient observations, even if the timing of market reversals remains notoriously difficult.

Echoing this sentiment, renowned short-seller Jim Chanos has drawn stark comparisons between the capital expenditure currently flowing into AI infrastructure and the infamous dot-com bubble of the late 1990s. Chanos posits that the sheer scale of investment in AI-related hardware, software, and data centers surpasses even the frenzied spending seen during the internet boom. His argument focuses on the possibility of overcapacity and diminishing returns on these massive investments, a common outcome in speculative cycles where capital is deployed indiscriminately. The implication is that while the underlying technology may be transformative, the economic viability of all current investments is highly questionable.

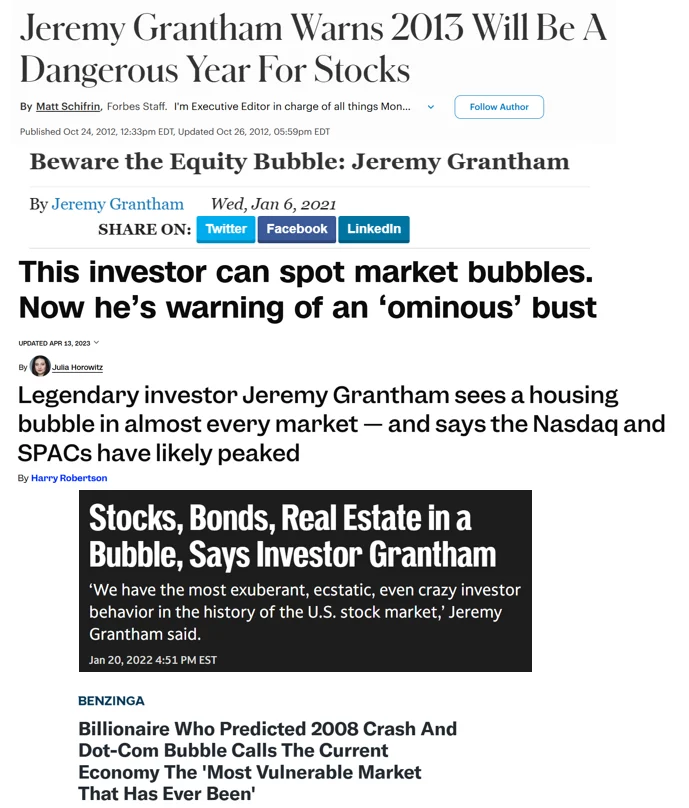

Long-time market bear Jeremy Grantham, co-founder of GMO, has consistently positioned himself as a Cassandra of financial markets, frequently warning of "super-bubbles" and their inevitable, painful deflations. Grantham’s framework for identifying bubbles often involves a blend of historical valuation metrics, behavioral economics, and a keen eye for speculative excesses. His current warnings align perfectly with his established methodology, suggesting that the current market, propelled by AI, exhibits all the classic signs of a speculative peak, from extreme valuations to widespread speculative participation. For Grantham, this isn’t merely a correction in the making but a monumental unwinding of market distortions.

Perhaps most notably, Ray Dalio, the billionaire founder of Bridgewater Associates, the world’s largest hedge fund, has recently issued a series of pronouncements that have sent ripples through the investment community. Dalio, whose insights are often sought after due to his immense wealth and the success of Bridgewater’s "All Weather" strategy, has penned articles detailing his concerns. He observes a significant "market and economic concentration in one new sector that is highly volatile and risky – and is super-popular among unsophisticated investors. That’s classic bubble stuff."

Dalio’s analysis extends beyond mere observation, venturing into explicit predictions about future returns. He asserts, "While it is indisputable that the risks are high, I am now going to give you an opinion, which could be wrong, that the prospective returns are low. That assessment of prospective future returns is based on my analytical work related to valuations and my bubble indicator’s readings: the real returns in equities over the next 5 to 10 years look to be about -5 to -10%, though there is considerable uncertainty around those numbers." Such a grim forecast, coming from an investor of Dalio’s stature, naturally sparks considerable apprehension among market participants.

The financial media, ever keen to capture clicks and attention, amplifies these warnings. Articles speculating on the next market downturn or comparing current trends to historical bubbles frequently grace the business pages, contributing to an atmosphere of uncertainty and, at times, anxiety. A recent example from the New York Times, highlighting the potential for a SpaceX IPO to signal a "stock bubble," illustrates this constant media scrutiny on any high-profile, high-valuation event.

A History of Unfulfilled Prophecies: The Pundit’s Predicament

While the current warnings from these esteemed figures sound genuinely alarming, a deeper look into their historical track records reveals a recurring pattern: the consistent difficulty, even for the most brilliant minds, in accurately timing market tops and the subsequent onset of bear markets.

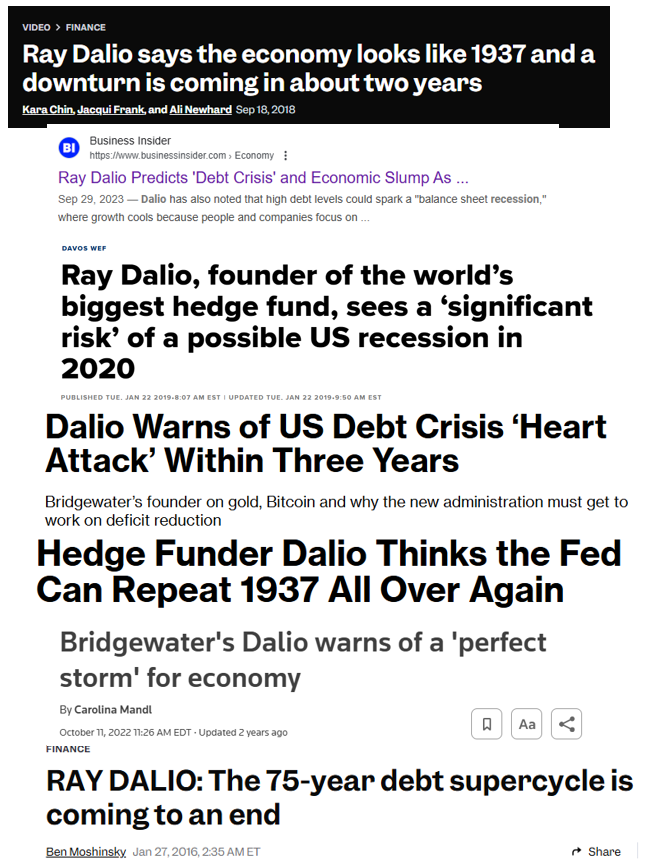

Ray Dalio, for all his intellectual prowess and wealth accumulation, has a well-documented history of making dire market predictions that have not materialized as anticipated. For well over a decade, Dalio has voiced concerns about systemic risks, the potential for a "lost decade" for investors, and the erosion of wealth. Following the 2008 financial crisis, his warnings about impending economic malaise and the challenges facing traditional asset classes were frequent. Yet, the subsequent period witnessed one of the longest and strongest bull markets in history, confounding many of his earlier pessimistic outlooks. Investors who acted solely on these warnings might have missed out on substantial gains.

Jeremy Grantham’s career has been punctuated by numerous "bubble" calls, many of which have been early or simply did not lead to the catastrophic outcomes he predicted within the anticipated timeframe. While Grantham accurately identified the dot-com bubble, he has subsequently called for the bursting of numerous other "bubbles" over the past two decades – in commodities, housing, and general equities – often ahead of significant market corrections, but rarely with the precision that allows for actionable, profitable timing strategies. His consistent bearish stance, while theoretically sound from a valuation perspective, has often placed him out of sync with prolonged market rallies.

This isn’t to diminish their intelligence or the validity of their underlying analytical frameworks. Rather, it underscores a fundamental truth about financial markets: they can remain irrational longer than many believe possible, and predicting the exact moment of capitulation is a task that has consistently humbled even the most astute observers. The original article highlights this by referencing past "tech bubble" calls stretching back to 2017 and beyond, long before the current AI boom. Many of these earlier warnings proved premature, as tech stocks continued their ascent, driven by genuine innovation and robust earnings. What felt like a bubble a "hundred years ago" (pre-pandemic) now looks like early innings in retrospect for many of these companies.

The "pundit graveyard" is indeed littered with the unfulfilled prophecies of market top callers. The incentive structure for fund managers and newsletter writers often encourages bold, contrarian predictions. Standing out from the crowd with a dramatic forecast can generate headlines, attract attention, and potentially draw in clients, even if the accuracy rate is low. However, for investors, acting on such predictions can be detrimental, leading to missed opportunities or premature exits from fundamentally sound investments.

The Intricacies of Market Cycles and Valuation: Beyond the Hype

The debate over whether AI constitutes a bubble is complex, requiring a nuanced understanding of market dynamics, valuation methodologies, and the historical context of technological revolutions.

Bubbles typically share several common characteristics:

- Rapid Price Appreciation: Assets experience an exponential increase in value over a relatively short period, often detached from underlying earnings growth.

- Speculative Fervor: Widespread public enthusiasm, often fueled by fear of missing out (FOMO), draws in a broad base of investors, including those with limited financial sophistication.

- New Paradigm Narrative: Proponents argue "this time is different," citing transformative technology or economic shifts that justify unprecedented valuations.

- Easy Credit/Liquidity: An environment of readily available capital often helps inflate asset prices.

- Concentration: A significant portion of market gains is often concentrated in a narrow group of high-flying stocks or sectors.

The AI sector undeniably exhibits several of these traits. The rapid ascent of AI-related stocks, the intense media coverage, the "transformative" narrative, and the general excitement among investors are palpable. Companies directly involved in AI development, chip manufacturing, and data infrastructure have seen their valuations soar to unprecedented levels. This certainly lends credence to the bubble callers’ concerns.

However, it’s crucial to differentiate between identifying potential overvaluation and precisely timing a market collapse. Historically, bubbles often form around genuinely revolutionary technologies – railroads, radio, the internet – that fundamentally change society and the economy. The underlying technology of AI is real, transformative, and has immense long-term potential. The challenge lies in discerning whether current valuations accurately reflect this potential or if they have overshot, incorporating future growth too aggressively.

Valuation metrics, such as Price-to-Earnings (P/E) ratios, Price-to-Sales (P/S), and Market Cap to GDP, can offer insights into the expensiveness of the market. Many of these indicators currently sit at historically high levels, particularly for growth-oriented sectors like tech and AI. However, these metrics alone are imperfect predictors of short-term market movements. High valuations can persist for extended periods, especially in environments of low interest rates or significant technological innovation. Furthermore, traditional valuation models often struggle to capture the full, long-term impact of truly disruptive technologies.

Navigating the Noise: Investor Responses and Market Sentiment

The constant stream of bubble warnings, amplified by financial media, creates a challenging environment for individual investors. The psychological impact can be significant, leading to a range of counterproductive behaviors:

- Paralysis: Fear of a looming crash can prevent investors from deploying capital, causing them to miss out on potential gains.

- Panic Selling: Exiting the market prematurely based on predictions can lock in losses or prevent participation in subsequent recoveries.

- Market Timing Attempts: Trying to "dodge" a bubble by selling at the top and buying back at the bottom is a strategy that rarely works consistently for anyone, let alone the average investor.

The market’s reaction to such warnings is often complex. While some institutional investors might adjust their portfolios, the broader market tends to absorb and eventually discount these predictions, especially if they are not immediately followed by a downturn. The prevailing sentiment often reflects a tension between fundamental analysis and behavioral impulses.

Instead of attempting to time the market based on expert predictions, a more robust and historically proven approach is to focus on building a durable, diversified portfolio. This involves:

- Asset Allocation: Spreading investments across different asset classes (equities, bonds, real estate, commodities) to reduce concentration risk.

- Diversification within Asset Classes: Investing in a broad range of companies and sectors, rather than concentrating heavily in a single "hot" area.

- Long-Term Perspective: Focusing on long-term growth and compounding, rather than short-term market fluctuations.

- Regular Rebalancing: Periodically adjusting the portfolio back to its target allocations, which often means selling assets that have performed well and buying those that have underperformed.

- Emotional Discipline: Resisting the urge to make impulsive decisions based on fear or greed.

Wealth, for the vast majority of successful investors, is built not through perfect timing or dramatic market calls, but through consistent participation, disciplined saving, and a commitment to a well-thought-out investment strategy. The people who genuinely get rich in the market rarely do so by picking tops or calling bubbles; rather, they achieve it by staying invested through market cycles, weathering the inevitable storms, and allowing compounding to work its magic.

Implications: The Enduring Lesson for Investors

The ongoing debate about whether AI represents a historic bubble serves as a powerful reminder of several enduring lessons for investors. Firstly, making accurate and consistently profitable market timing calls, particularly regarding market tops, remains an exceptionally difficult, if not impossible, endeavor, even for the most experienced and intelligent financial professionals. The "fund manager pipe dream" of predicting the next top is a seductive one, but history shows it’s an inconsistent strategy.

Secondly, while the characteristics of bubbles are often identifiable in hindsight, the market’s capacity for irrationality, coupled with genuine technological breakthroughs, can sustain elevated valuations for longer than most anticipate. The real challenge is not just recognizing potential overvaluation, but enduring the period where that overvaluation continues to expand.

Finally, and perhaps most importantly, the most effective strategy for long-term wealth creation lies not in prognosticating market movements, but in constructing a resilient portfolio. A durable portfolio, diversified across various assets and designed to withstand the inevitable tops, bottoms, and middles of market cycles, is the investor’s best defense against uncertainty and the most reliable path to achieving financial goals. As explored in depth in publications like "Risk & Reward," understanding and managing risk within a long-term framework is paramount.

While someone, through a combination of skill and luck, might indeed "call" the next market top and even profit from it, their ability to replicate that success consistently is highly improbable. For the vast majority of investors, the prudent path is to tune out the perpetual pulse of panic and focus on what they can control: their savings rate, their diversification, and their long-term investment horizon.