The Great Generational Shift: Dispelling Fears of a Looming "Relentless Ask" in Financial Markets

June 18, 2026 – For over a decade, the financial world has grappled with an intriguing paradox: the "Relentless Bid." This phenomenon, characterized by a continuous influx of capital into equity markets, has been widely credited with driving stock prices higher and dampening volatility. Yet, as the colossal Baby Boomer generation enters its twilight years of retirement, a new question emerges, casting a shadow of uncertainty: Will this "Relentless Bid" transform into a "Relentless Ask," or even a "Relentless Beg," as millions begin to divest their accumulated wealth?

A recent query posed to financial commentator Ben Carlson, published on June 18, 2026, encapsulates this growing concern: "The ‘Relentless Bid’ of 401ks has inflated stock prices and dampened volatility for years. As the population ages, target-date funds are swapping stocks for bonds, and people have to take RMDs. At what point does this cavalcade of selling drive stock prices down, and become the ‘Relentless Beg’ (or ‘Relentless Ask’ if you prefer)? Or is wealth so top-heavy that this phenomenon is just too small to make a difference?"

Carlson, a prolific voice in financial commentary, acknowledges that variations of this question have circulated for the better part of ten years. While the theoretical underpinnings of a potential market downturn due to mass selling seem plausible, his analysis suggests that the fears are largely overblown. This article delves into the core arguments surrounding this generational wealth transfer, examining historical context, current data, expert perspectives, and the broader implications for the global economy.

The Rise of the "Relentless Bid": A Chronology

To understand the current anxieties, it’s crucial to trace the origins and impact of the "Relentless Bid." The concept was notably articulated by financial advisor Josh Brown in 2014, describing a powerful, systemic force driving market behavior.

Early 2000s – 2014: The Dawn of Automatic Investing

The groundwork for the "Relentless Bid" was laid by a confluence of factors:

- Tax-Deferred Retirement Plans: The widespread adoption of 401(k)s and similar employer-sponsored plans incentivized consistent, long-term investing.

- Technological Advancements: The rise of online brokerage platforms and automated investment tools made participation easier and more accessible.

- Lower Costs: The proliferation of low-cost index funds and Exchange Traded Funds (ETFs) reduced the barrier to entry and improved net returns for investors.

- Default Enrollment: New regulations and corporate practices increasingly made automatic enrollment in retirement plans the norm, significantly boosting participation rates, particularly among younger workers.

As Carlson noted in a 2024 piece on the "automatic investing revolution," these developments represented "a glorious step forward for investors." They created a continuous, almost indifferent flow of capital into the stock market. Week after week, regardless of market news or economic headlines, advisors and automated systems funneled fresh contributions into equities. This steady, predictable buying pressure, largely from a growing pool of retirement savers, became the "Relentless Bid," providing a persistent buoyancy to asset prices and mitigating sharp downturns.

2014 Onward: Baby Boomers at the Forefront

The Baby Boomer generation, born between 1946 and 1964, was at the vanguard of this investing revolution. Having benefited from decades of economic growth, stable careers, and the power of compound interest within these tax-advantaged accounts, they accumulated unprecedented levels of wealth. As they moved through their prime earning years, their consistent contributions amplified the "Relentless Bid."

The Accumulation of Unprecedented Wealth: Supporting Data

The scale of Baby Boomer wealth is staggering, forming the bedrock of the current market anxiety.

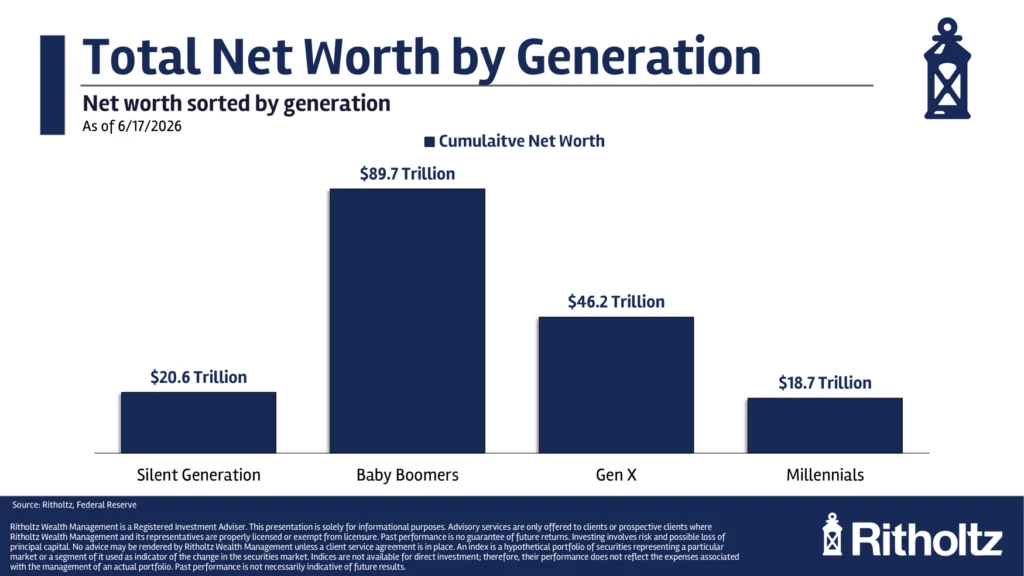

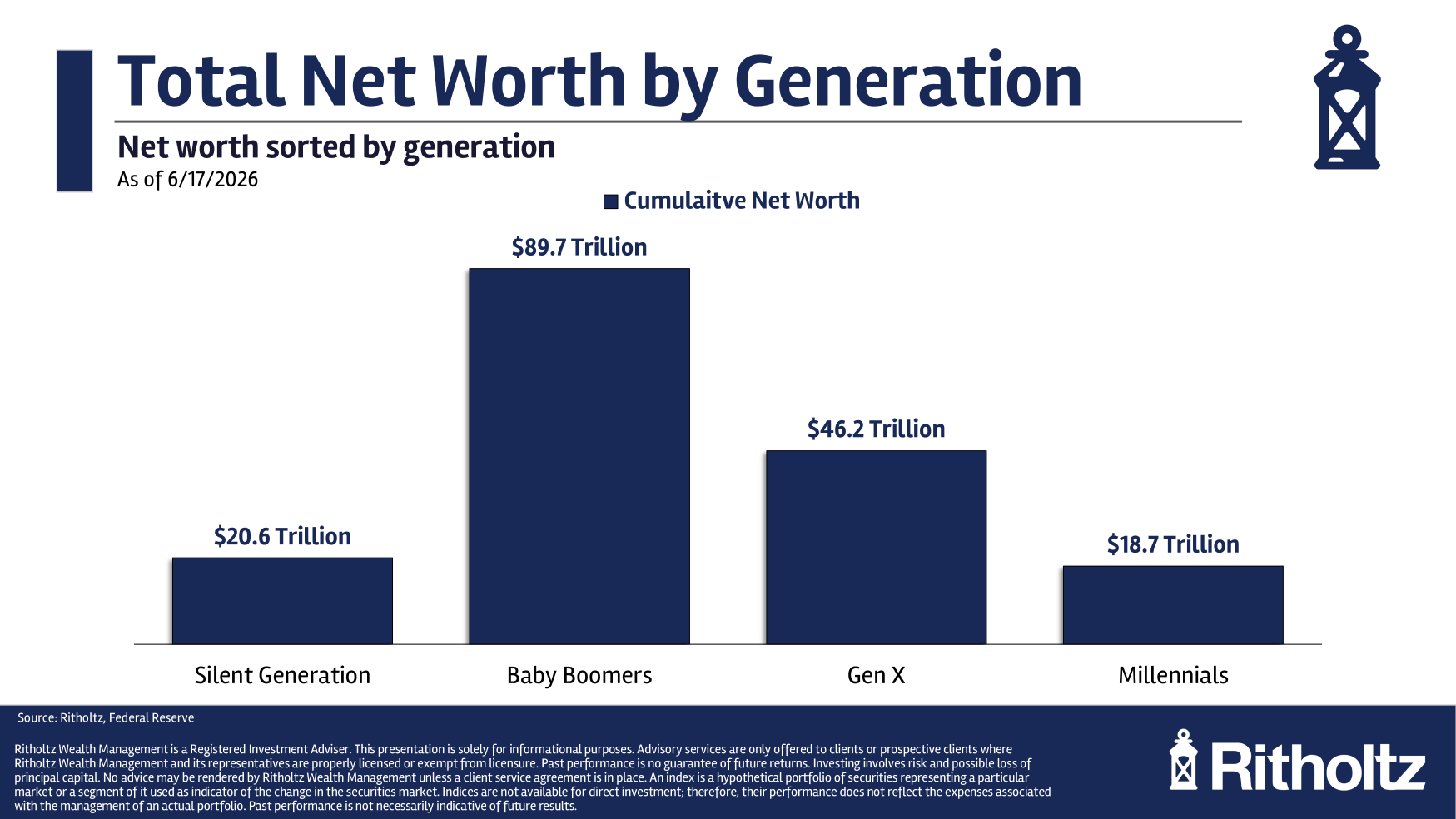

Generational Wealth Snapshot (as of 2026):

- Baby Boomers: Control an estimated $90 trillion in total net worth. This figure is likely higher, as significant wealth from the Silent Generation (those 81 and older, controlling approximately $20 trillion) is in the process of being passed down, pushing the Boomer-controlled assets closer to $100 trillion.

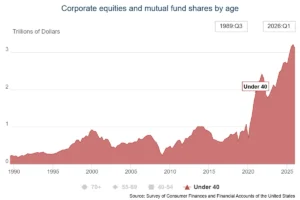

- Asset Concentration: This generation, along with their older counterparts, collectively owns nearly 70% of all stocks and half of the total housing market wealth.

This immense concentration of capital is what fuels the "Relentless Ask" hypothesis. If even a fraction of this wealth were to be systematically liquidated for retirement expenses or RMDs, the sheer volume could, in theory, overwhelm demand and trigger a market correction. The question then becomes, as Carlson articulates, why hasn’t this happened already, given that "somewhere in the range of 40 to 50 million baby boomers are already retired today?"

Official Responses and Expert Counter-Arguments

Ben Carlson, in his analysis, directly challenges the "Relentless Ask" narrative, presenting several compelling reasons why a mass sell-off leading to a market crash is an overblown fear. His arguments are representative of a segment of financial experts who advocate for a more nuanced understanding of demographic shifts and wealth dynamics.

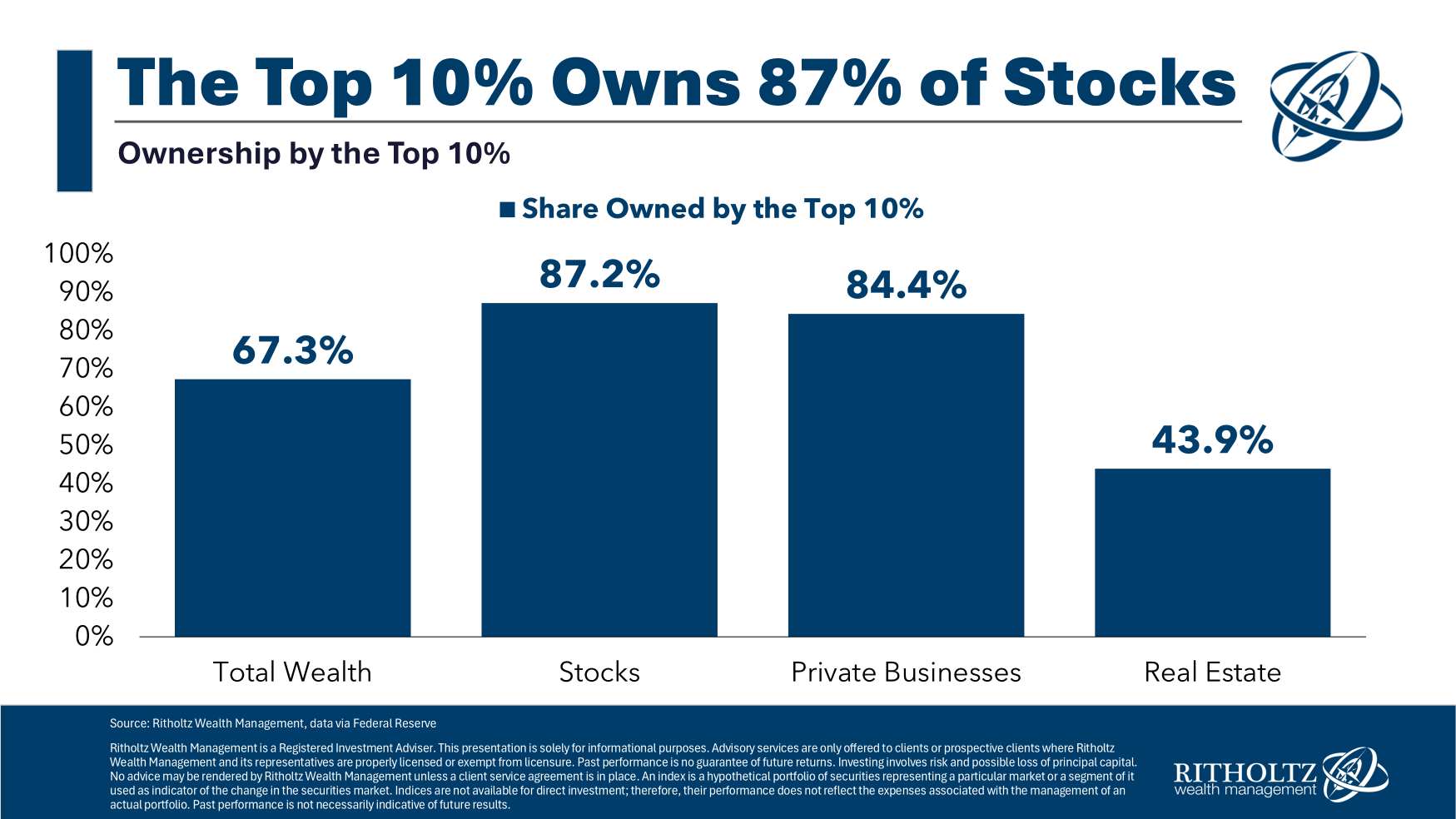

1. Stock Market Wealth is Highly Concentrated:

Carlson highlights a crucial statistic: the top 10% of the population controls a disproportionate share of wealth—87% of all stocks, nearly 85% of private businesses, and almost 70% of total wealth. This extreme concentration has profound implications for the "Relentless Ask" theory.

- Intergenerational Transfer: The vast majority of this concentrated wealth, particularly at the highest echelons, is not intended to be spent down entirely to fund retirement lifestyles. Instead, it is earmarked for intergenerational transfer, passed down to heirs. This means that upon the death of a wealthy individual, assets typically transfer ownership rather than being immediately liquidated en masse from the market. While there might be some rebalancing or diversification by the inheritors, it’s not the wholesale market exit envisioned by the "Relentless Ask."

- Glide Path Spending: Even for those who do spend down their portfolios, the process is gradual. Retirement spending occurs on a "glide path," not in a sudden, catastrophic market event. Required Minimum Distributions (RMDs), while necessitating withdrawals from tax-advantaged accounts, are typically a small percentage of overall assets and are often reinvested or spent gradually within the broader economy. This recycling of funds, as Carlson notes, can even be a positive for corporations as retirees continue to consume goods and services.

2. Retirees Still Need to Take Risk for Longevity:

The notion that retirees will simply swap all their stocks for bonds ignores a critical demographic reality: people are living longer. As highlighted by a 2026 New York Times article on longevity finances, a 65-year-old couple faces a 64% chance that at least one spouse will live into their 90s.

- Extended Investment Horizons: A retirement spanning 20, 30, or even more years demands continued portfolio growth to outpace inflation and maintain living standards. Simply shifting entirely to low-growth fixed-income assets risks significant erosion of purchasing power over such an extended period.

- Inflation Hedge: Equities remain a vital hedge against inflation, a persistent concern for retirees dependent on a fixed income. To maintain their standard of living and cover rising healthcare costs, a portion of their portfolio must continue to seek growth, meaning stocks will retain a significant role in many retirement plans.

3. Millennials as the Counterbalance:

Perhaps the most potent counter-argument to the "Relentless Ask" is the emergence of the Millennial generation as the next wave of asset accumulators.

- Demographic Shift: While roughly 70 million Baby Boomers are expected to decline by 16 million by 2035 and another 24 million by 2045, there are approximately 73 million Millennials. This generation is now entering its prime earning years (the largest population group in 2026 is between 33 and 37 years old), poised to become significant buyers of financial assets.

- New Investment Habits: Millennials, having grown up in the digital age, are increasingly comfortable with investing through accessible platforms, often embracing passive investing strategies similar to those that fueled the "Relentless Bid." While they face unique challenges like student loan debt and later homeownership, their sheer numbers and growing earning power position them as a natural offset to any selling pressure from older generations. If Baby Boomers sell stocks or houses, there is a large, willing cohort ready to step in as buyers.

4. Market Efficiency and Foresight:

Carlson also points out that demographic shifts, unlike sudden economic shocks, are highly predictable. The "Baby Boomer demographic cliff" is not a surprise to sophisticated market participants. Financial models, institutional investment strategies, and long-term planning already factor in these known population trends. The market, in its forward-looking nature, has likely already priced in the expected effects of this generational transition, mitigating the potential for a sudden, unanticipated crash.

Broader Implications for the Economy and Investors

The debate surrounding the "Relentless Ask" extends beyond mere stock prices, touching upon broader economic and societal implications.

For Individual Investors:

Carlson’s analysis offers a reassuring perspective. For those nearing or in retirement, it underscores the importance of a well-diversified portfolio that accounts for longevity and inflation. It discourages panic-driven decisions based on generational fears, instead advocating for a focus on individual financial plans and long-term objectives. For younger investors, it suggests that ample opportunities to acquire assets will arise as wealth transfers, reinforcing the wisdom of consistent, disciplined investing.

For the Economy:

The recycling of wealth is a critical component. Money withdrawn from retirement accounts, whether through RMDs or for living expenses, re-enters the economy through consumption. This continued spending by a large, wealthy demographic supports businesses and jobs, preventing a severe economic contraction that might otherwise accompany a massive market liquidation. The intergenerational wealth transfer also implies a shift in consumption patterns and investment priorities, which could gradually reshape economic sectors.

For Market Structure and Volatility:

While Carlson argues against a catastrophic crash, the generational shift could subtly influence market dynamics. The sheer size of Millennial and Gen Z investors, combined with their tech-savvy approach, might further solidify the trend towards passive investing. This could continue to exert a "bid" pressure, albeit from a different demographic, and potentially maintain the dampening effect on volatility that the "Relentless Bid" achieved. However, the exact balance between new buyers and retiring sellers will be a dynamic force to watch, though unlikely to lead to the dire "Relentless Beg" scenario.

In conclusion, while the idea of a massive generational sell-off holds theoretical appeal, a deeper dive into wealth concentration, longevity trends, demographic shifts, and market efficiency reveals a more nuanced picture. As Ben Carlson and other financial commentators suggest, the "Relentless Bid" may evolve, but the forces at play are complex and counterbalancing, making a sudden, calamitous "Relentless Ask" an unlikely outcome. The ongoing transfer of wealth from Baby Boomers to younger generations represents not a cliff edge, but rather a gradual, multi-faceted transition that the financial markets are already well-positioned to navigate.