The Great Fintech Migration: How the Demise of Mint.com Reshaped the Personal Finance App Market

The landscape of consumer financial technology underwent a seismic shift when Intuit announced the official closure of Mint.com, the pioneering personal finance management (PFM) platform that had dominated the market for over a decade and a half. Launched in 2007 and acquired by Intuit in 2009, Mint was the gateway for millions of consumers to automate their budgets, track their net worth, and aggregate their financial accounts in one centralized dashboard.

For many, Mint’s free, ad-supported model was an indispensable tool for financial literacy. However, its shutdown has forced millions of active users to scramble for alternatives, triggering an unprecedented customer acquisition war among competing personal finance platforms. This report analyzes the major market alternatives, the timeline of Mint’s decline, and the broader implications for the consumer fintech industry.

1. Chronology: The Rise and Fall of a Fintech Pioneer

To understand the current state of the personal finance app market, one must look at how Mint defined—and ultimately outgrew—its niche within Intuit’s corporate portfolio.

[2007] Mint.com launches as a free, web-based automated budgeting tool.

│

[2009] Intuit acquires Mint for $170 million to bolster its consumer finance division.

│

[2021-2023] Intuit shifts corporate focus toward monetizing Credit Karma (acquired in 2020).

│

[Nov 2023] Intuit announces the official shutdown of Mint, effective early 2024.

│

[Mar 2024] Mint.com officially goes dark; users are urged to migrate to Credit Karma.

│

[Present] Competitors launch targeted discount campaigns to capture displaced Mint users.- 2007: The Dawn of Automated PFM: Mint.com launches at the TechCrunch 50 conference, instantly winning acclaim for its ability to securely aggregate bank transactions using early screen-scraping and API technologies.

- 2009: The Intuit Acquisition: Recognizing Mint as a threat to its legacy software, financial giant Intuit acquires the startup for $170 million. Over the next decade, Mint becomes the gold standard for free budgeting apps, eventually amassing over 20 million registered users.

- Late 2023: The Death Knell: In November 2023, Intuit announces it will shut down Mint.com. Rather than keeping it as a standalone service, Intuit decides to migrate users to Credit Karma, a platform it acquired in 2020 for $7.1 billion.

- March 2024: The Blackout: Mint officially ceases operations. Users migrating to Credit Karma quickly realize the latter lacks Mint’s robust, customizable budgeting features, focusing instead on credit monitoring and cross-selling financial products (such as credit cards and personal loans). This mismatch sparks a massive diaspora of users seeking true PFM replacements.

2. Supporting Data: Evaluating the Top 8 Mint Alternatives

With the market vacuum left by Mint, several specialized platforms have emerged to claim the crown. Based on extensive, multi-year testing by financial experts and consumer feedback, these eight platforms represent the best alternatives, categorized by their distinct strengths.

Summary Comparison of Leading Platforms

| Budgeting App | Target Audience | Primary Focus | Pricing Model |

|---|---|---|---|

| Monarch Money | Couples & Power Users | Comprehensive Budgeting & Goals | Paid ($99/year or $14.99/month) |

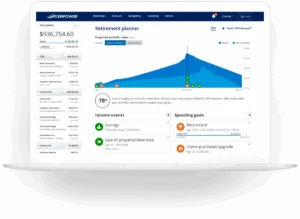

| Empower | High-Net-Worth Individuals | Investment & Net Worth Tracking | Free (Advisory upsells) |

| Rocket Money | Subscription Savers | Cash Flow & Bill Negotiation | Free / Paid ($7–$14/month sliding scale) |

| Quicken Simplifi | Mobile-First Budgeters | Automated Cash Flow Tracking | Paid ($3.49/month with annual discount) |

| Origin | Holistic Wealth Planners | Taxes, Equity, & CFP Access | Paid ($99/year or $12.99/month) |

| Tiller Money | Spreadsheet Enthusiasts | Google Sheets & Excel Automation | Paid ($79/year) |

| Quicken Classic | Legacy Desktop Users | Advanced Reporting & Offline Use | Paid (Subscription tier-based) |

| You Need a Budget (YNAB) | Zero-Based Budgeters | Intentional Spending & Envelope Method | Paid ($109/year or $14.99/month) |

Detailed Analysis of the Competitors

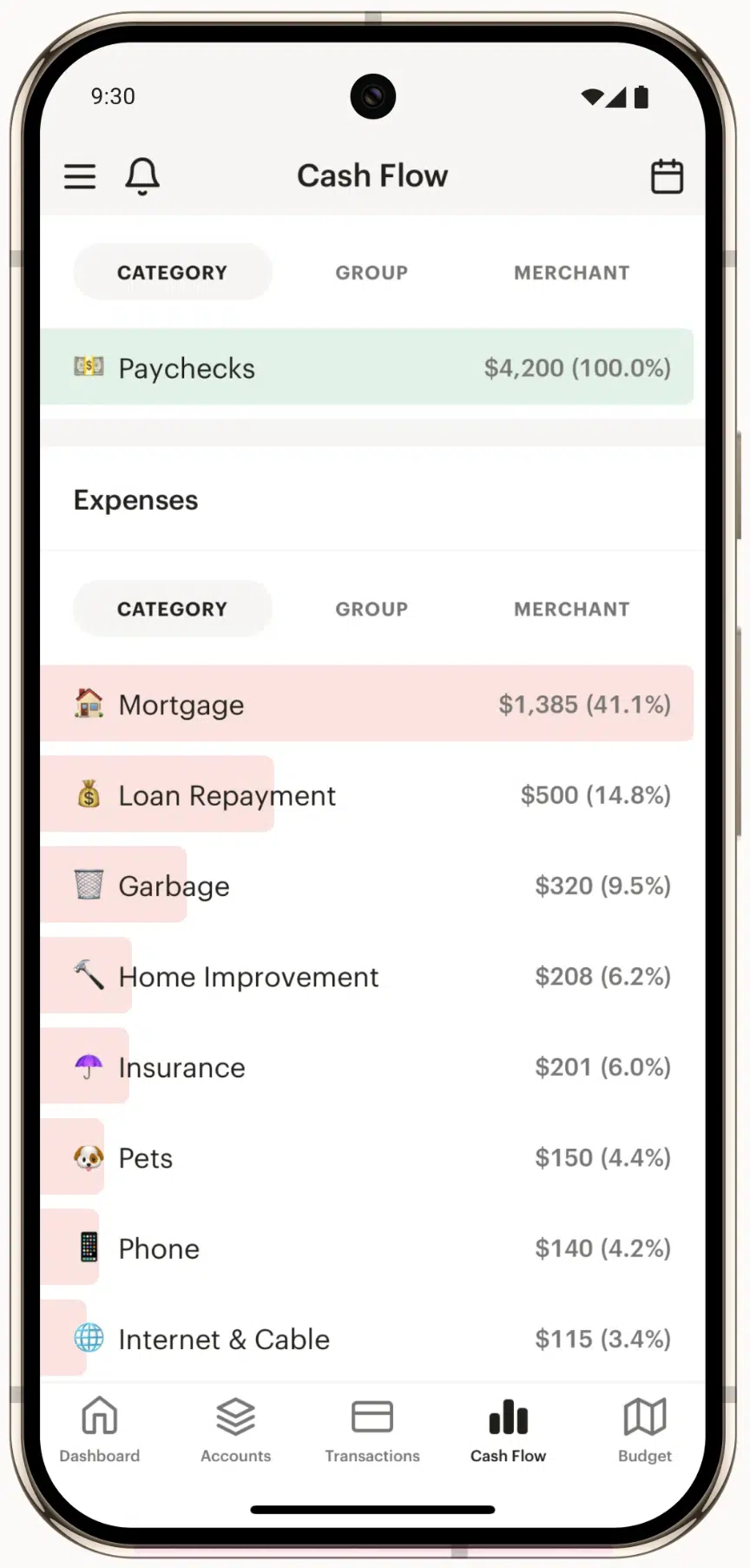

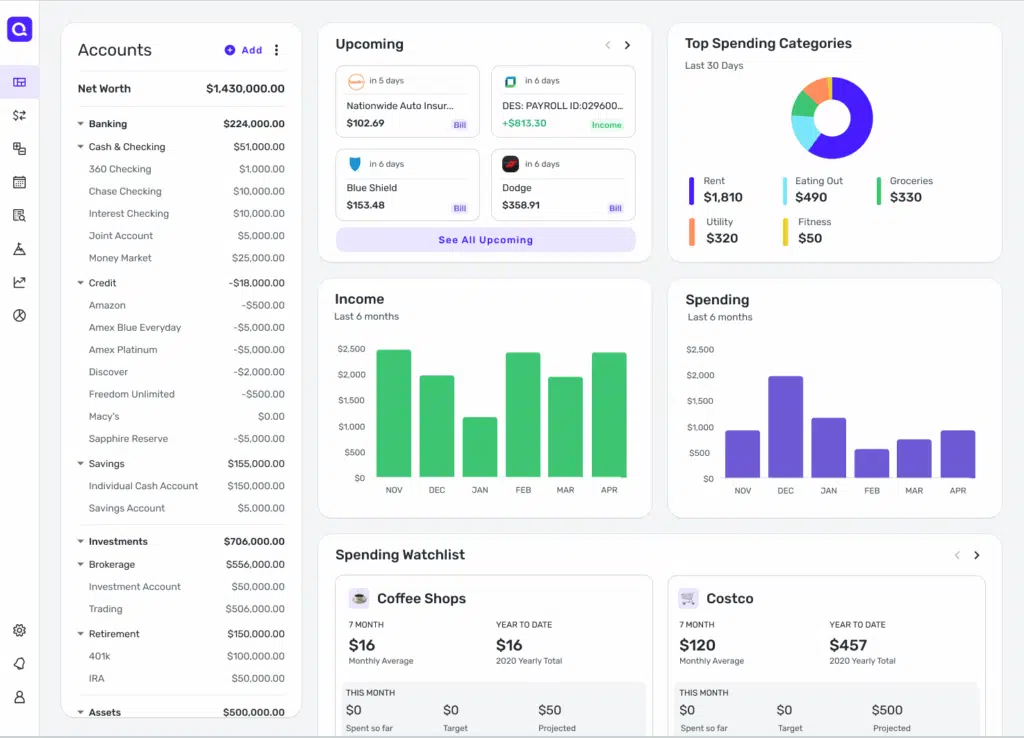

1. Monarch Money — Best Overall Budgeting App

Monarch Money has emerged as the premier choice for former Mint users, particularly couples. In a poetic twist, Monarch’s co-founder and CEO, Val Agostino, was the original product manager who helped build Mint.com.

- Platform Availability: iOS, Android, Web

- Cost: 7-day free trial, then $99/year (promotions like

ROB50offer up to 50% off the first year). - Key Strengths:

- Collaborative Design: Allows partners to manage finances together with separate logins at no extra cost.

- Flex Budgeting: Handles variable, seasonal, or fluctuating expenses gracefully.

- User Interface: Features a modern, ad-free dashboard showing net worth, transactions, and progress toward financial goals.

- Credit Monitoring: Includes free access to VantageScore 3.0.

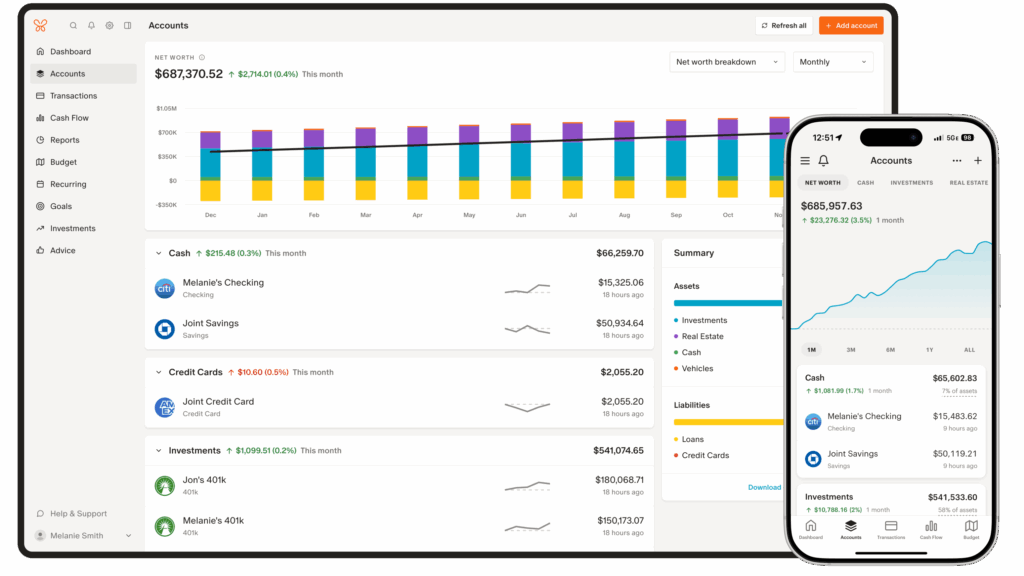

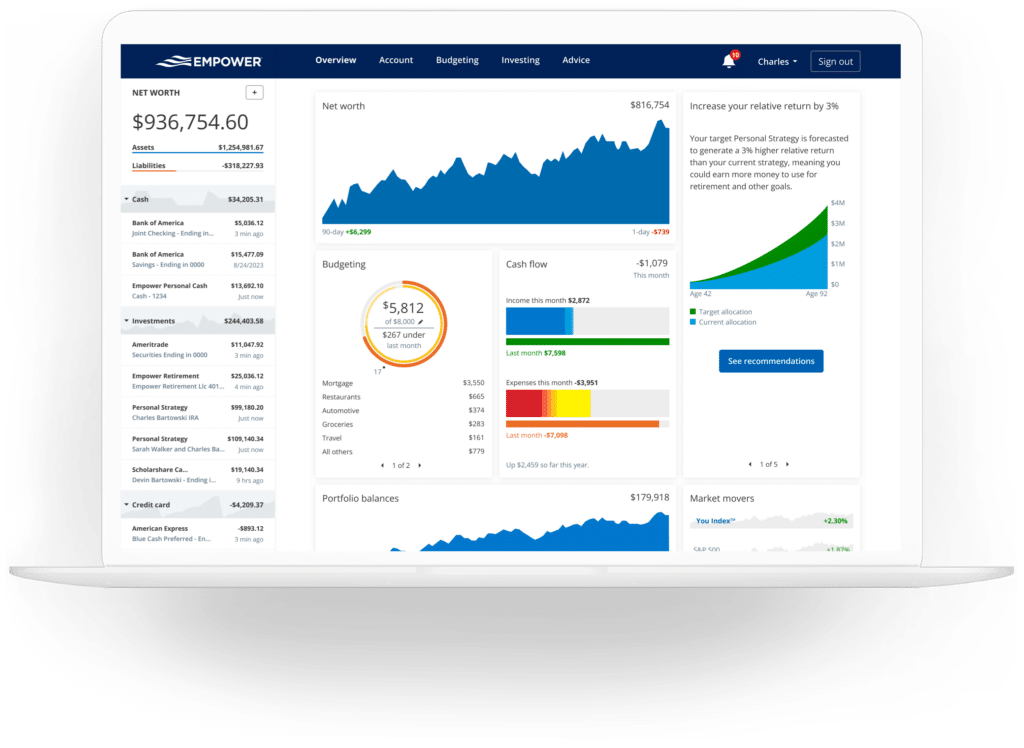

2. Empower — Best Free Investment Tracker

Formerly known as Personal Capital, Empower is the strongest free alternative to Mint, though it approaches personal finance from an investment perspective rather than a strict budgeting one.

- Platform Availability: iOS, Android, Web

- Cost: Free

- Key Strengths:

- Investment Suite: Features a robust portfolio analyzer, fee calculator, asset allocation tools, and retirement planners.

- Net Worth Tracking: Aggregates real estate, bank accounts, mortgages, and brokerage accounts seamlessly.

- Monetization Model: Instead of displaying ads, Empower makes money by offering optional, human wealth management services to users with portfolios over $100,000.

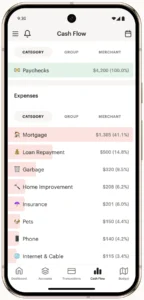

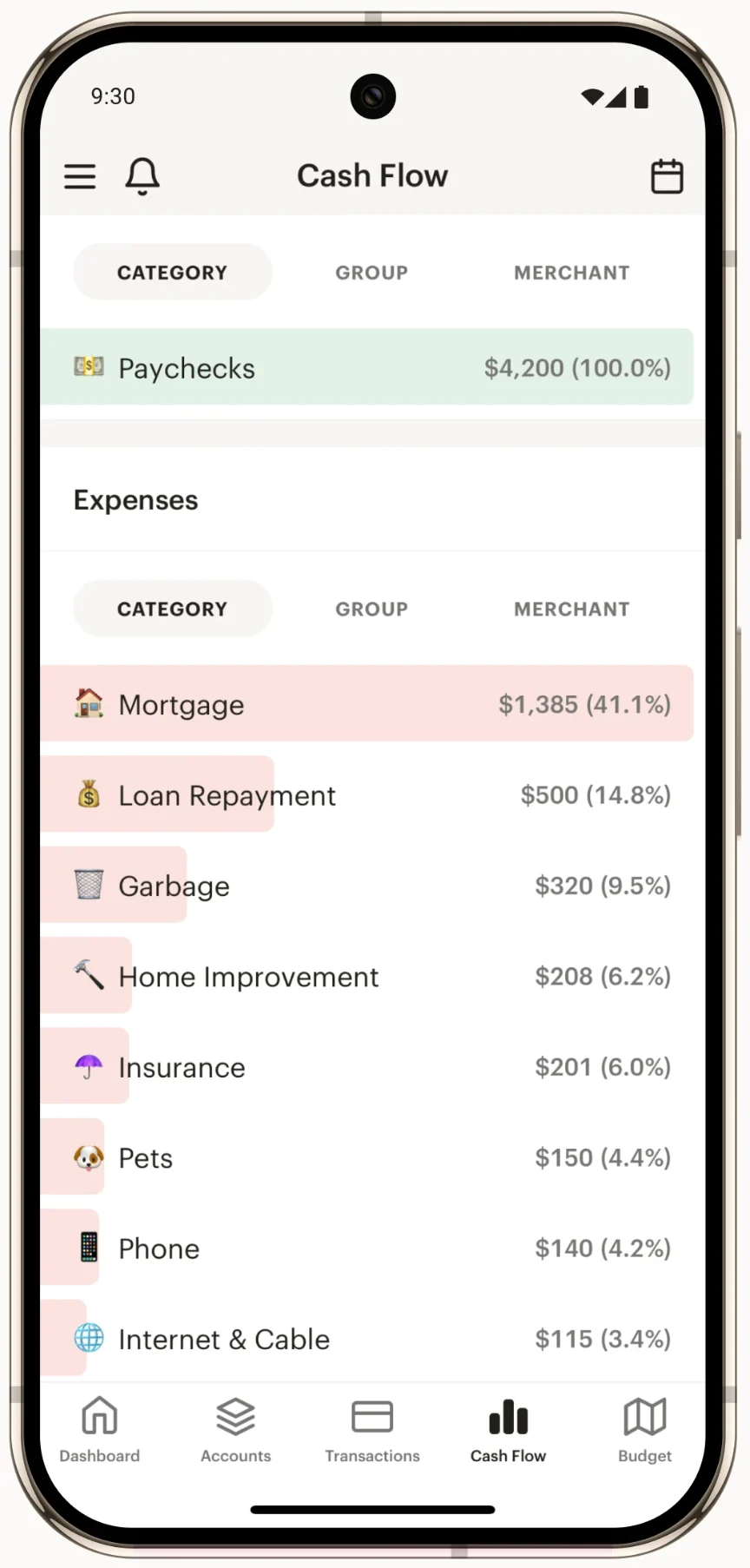

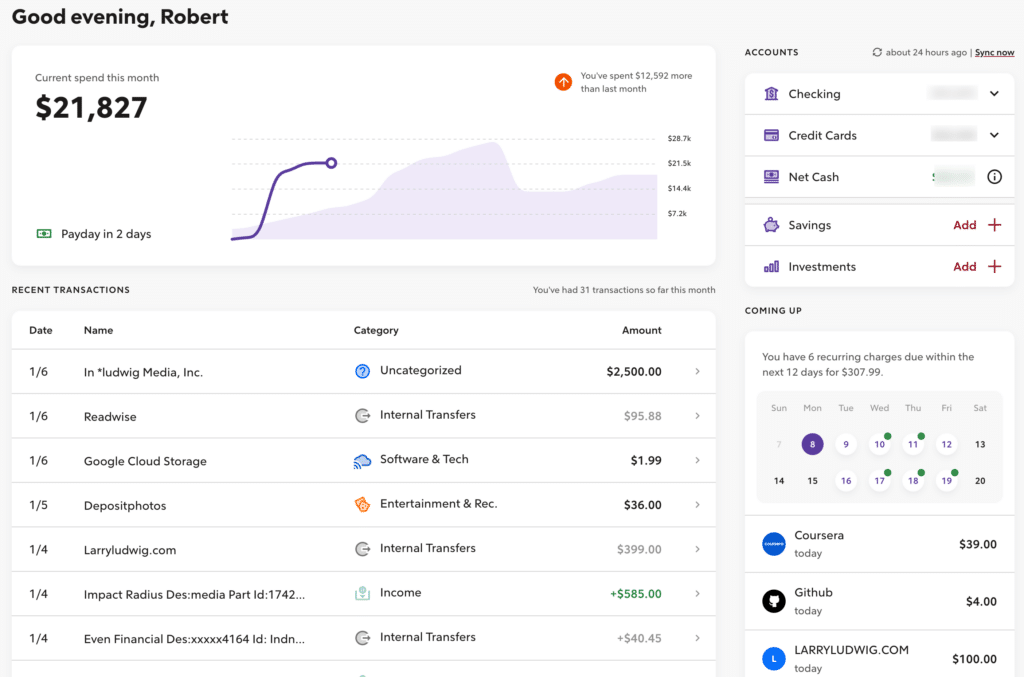

3. Rocket Money — Best for Cash Flow and Subscriptions

Originally launched as Truebill, Rocket Money focuses heavily on identifying recurring bills and helping users trim unnecessary expenses.

- Platform Availability: iOS, Android, Web

- Cost: Free tier available; Premium features cost between $7 and $14 per month (pay-what-you-want scale).

- Key Strengths:

- Subscription Cancellation: Automatically identifies recurring charges and can cancel subscriptions on the user’s behalf.

- Bill Negotiation: Rocket Money negotiates lower rates on utility and telecom bills in exchange for a percentage of the annual savings.

- Clean Visualization: Offers an intuitive calendar layout displaying when recurring bills are due.

4. Quicken Simplifi — Best Mobile-First Budgeting

Simplifi is Quicken’s modern, cloud-based mobile app, designed from the ground up to distance itself from the bloated legacy desktop software of the 1990s.

- Platform Availability: iOS, Android, Web

- Cost: $3.49/month (billed annually)

- Key Strengths:

- Automated Spending Plans: Calculates real-time discretionary spending limits after accounting for bills, savings goals, and prior spending.

- Watchlists: Allows users to track specific spending categories (e.g., dining out) without building a rigid budget around them.

- No Ads: Fully paid subscription guarantees user data is not sold to advertisers.

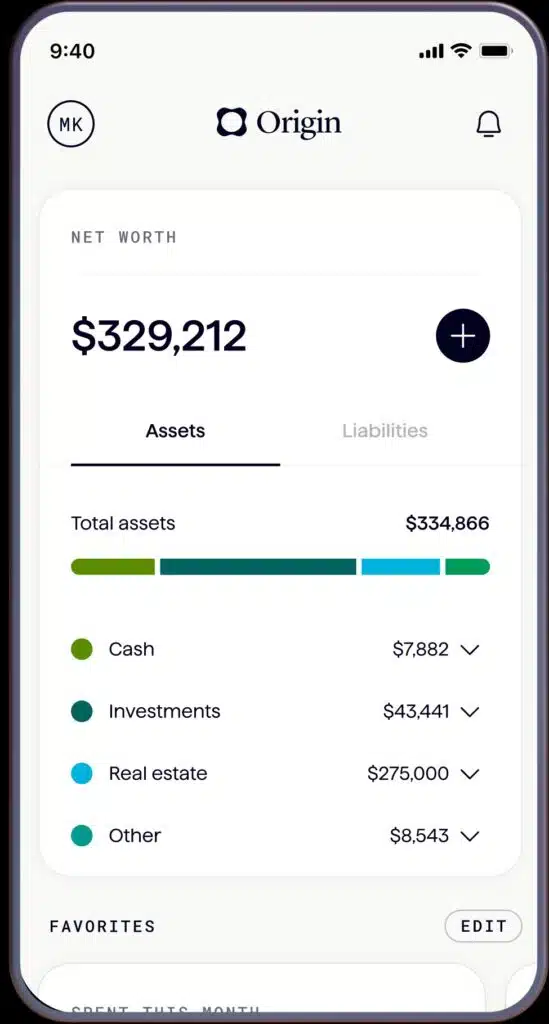

5. Origin — Most Comprehensive Wealth Management App

Origin goes beyond basic budgeting by acting as a comprehensive financial wellness platform, integrating tax preparation, equity tracking, and professional human guidance.

- Platform Availability: iOS, Android, Web

- Cost: 7-day free trial, then $12.99/month or $99/year (occasional promotional offers allow entry for $1 for the first year).

- Key Strengths:

- Integrated Tax Filing: Includes federal and state tax filing services directly in the subscription fee.

- Professional CFP Access: Provides access to Certified Financial Planners and estate planning services.

- AI Financial Assistant: Features an advanced AI chatbot that analyzes the user’s connected accounts to answer nuanced questions about emergency funds, debt payoff strategies, and savings goals.

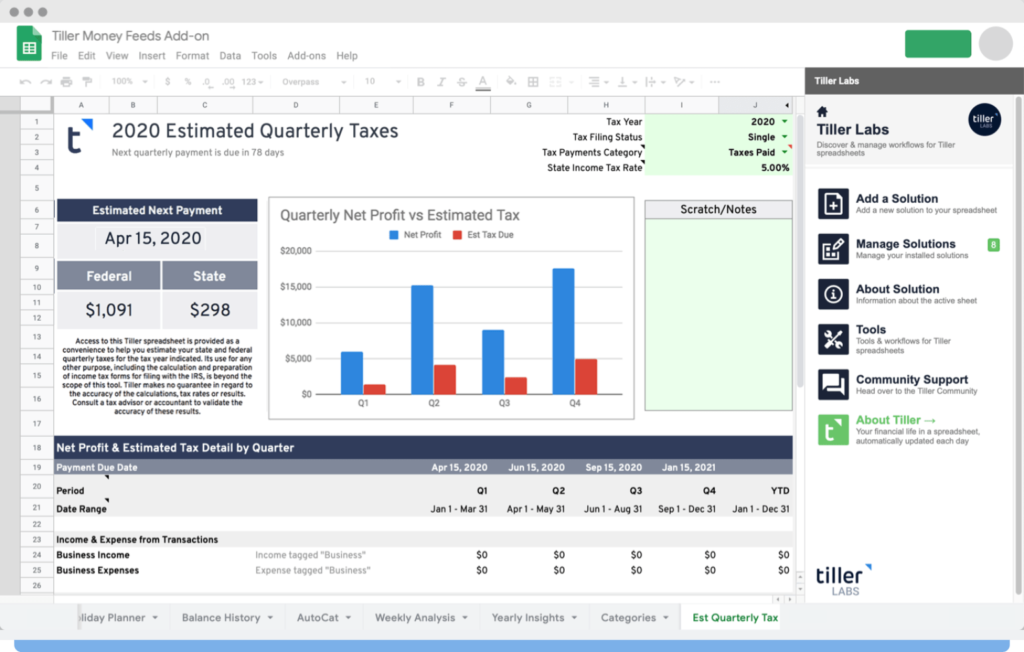

6. Tiller Money — Best for Spreadsheet Purists

For users who prefer total control over their data, Tiller Money bridges the gap between automated bank feeds and manual spreadsheet tracking.

- Platform Availability: Google Sheets, Microsoft Excel

- Cost: 30-day free trial, then $79/year

- Key Strengths:

- Data Control: Automatically feeds daily transactions and balances directly into Google Sheets or Excel.

- Customization: Users can build completely bespoke charts, pivot tables, and budget rules.

- Privacy: Because data is stored in the user’s personal Google Drive or OneDrive, Tiller does not see or sell financial profiles.

7. Quicken Classic — Best for Desktop Power Users

The legacy heavyweight of personal finance, Quicken Classic remains a powerful option for users who demand deep, offline financial reporting.

- Platform Availability: Windows, macOS (local installation required)

- Cost: Annual subscription tiers (varies by features)

- Key Strengths:

- Local Data Storage: Ideal for privacy-conscious users who do not want their financial history living exclusively in the cloud.

- Extensive Reporting: Offers tax schedule reports, investment tracking, and direct bill pay.

- Aesthetic: While functional, the user interface remains somewhat dated compared to modern web-native apps.

8. You Need a Budget (YNAB) — Best for Zero-Based Budgeting

YNAB is built around the "envelope method" of budgeting, where every single dollar of income is assigned a specific job (savings, bills, groceries) before it is spent.

- Platform Availability: iOS, Android, Web, Smartwatches

- Cost: $14.99/month or $109/year

- Key Strengths:

- Behavioral Shift: Forces users to budget only with the cash they currently have, rather than projecting future income.

- Overspending Protection: Dynamically adjusts categories when a user overspends in one area, pulling funds from another.

- Drawbacks: YNAB is expensive, lacks automated investment tracking, and features a steep learning curve that may frustrate users accustomed to Mint’s passive tracking.

3. Official Responses and Industry Reactions

The decision to shutter Mint was a calculated strategic pivot by Intuit, but it sparked swift condemnation from users and an aggressive land grab by competitors.

Intuit’s Official Stance

Intuit defended the closure of Mint as an evolution of its consumer ecosystem. In official communications, the company explained that consolidating personal finance tools under Credit Karma would allow users to access credit monitoring, net worth tracking, and financial product recommendations in a single platform. However, industry analysts note that the move was heavily driven by monetization: Mint’s ad-supported model yielded low average revenue per user (ARPU), whereas Credit Karma’s referral-fee model for credit cards, auto insurance, and personal loans is highly lucrative.

The Competitors’ Land Grab

Rival fintech companies immediately recognized the shutdown as a once-in-a-decade customer acquisition opportunity.

- Monarch Money quickly hired former Mint engineers and launched a dedicated "one-click" Mint data importer to let migrating users preserve their historical transaction data.

- Quicken Simplifi and YNAB launched extensive marketing campaigns, offering deep discounts to users who could prove they had a Mint account.

- Industry sources report that platforms like Monarch and Simplifi experienced record-shattering sign-up volumes in the first quarter of 2024, occasionally causing temporary server slowdowns due to the influx of data imports.

4. Implications: The Death of "Free" and the Future of PFM

The demise of Mint.com marks the end of an era for "free" financial software and signals broader structural shifts in how consumer fintech operates.

THE PFM BUSINESS MODEL EVOLUTION

[ Era of Free PFM ] [ Era of Premium PFM ]

(e.g., Mint.com) (e.g., Monarch, YNAB)

┌──────────────────────┐ ┌──────────────────────┐

│ • Free to use │ │ • Subscription-based │

│ • Monetized via ads │ VS │ • No third-party ads │

│ • User data targeted │ │ • Strict data privacy│

│ • Passive tracking │ │ • Active management │

└──────────────────────┘ └──────────────────────┘1. The Pivot to Subscription-Based Models

Mint proved that the ad-supported, free PFM model is financially unsustainable over the long term. Running secure, continuous bank APIs (via aggregators like Plaid, Yodlee, and Finicity) is highly expensive. When a service is free, the user is the product—meaning their financial data is leveraged to target them with credit card and loan offers. The market has now shifted toward paid subscription models (Monarch, YNAB, Simplifi) where users pay for utility, ad-free environments, and strict data privacy.

2. The Rise of Open Banking APIs

The migration of millions of users was made possible by the maturity of Open Banking APIs. Instead of fragile screen-scraping techniques that break whenever a bank updates its website, platforms now use secure, tokenized API connections. This transition has made financial data more portable, allowing users to move 15 years of transaction history from Mint to a competitor in a matter of minutes.

3. AI and the Next Generation of PFM

As platforms like Origin demonstrate, the future of budgeting apps lies in artificial intelligence. Passive categorization—simply labeling a transaction as "Groceries"—is no longer enough. The next generation of PFM tools will leverage AI to predict cash flow shortages, automatically negotiate bills, identify hidden subscription price hikes, and offer personalized, automated financial advice that was once only accessible through human financial advisors.