The Elusive Edge: Why Consistent Outperformance Remains the Holy Grail for Investors

NEW YORK, NY – In the high-stakes world of investment management, the quest to consistently outperform the market is a perpetual challenge, one that frequently confounds even the most sophisticated institutional investors. Despite elaborate systems designed to identify and reward top-tier talent, empirical data repeatedly demonstrates that sustained outperformance is a fleeting phenomenon, leading many to question the efficacy of traditional active management strategies and the reactive decision-making that often accompanies them.

At the heart of this dilemma lies a fundamental paradox: the very human tendency to chase past success, often leading to disappointment. While the allure of beating benchmarks remains strong, a deeper dive into market dynamics and investor behavior reveals a landscape where true long-term outperformance is an anomaly, not the norm. This reality prompts a critical re-evaluation of how both institutions and individual investors approach portfolio construction and diversification, culminating in a simple yet profound "diversification test" to guide more resilient investment choices.

The Institutional Treadmill: Chasing Green Lights

The journey into understanding the ephemeral nature of outperformance often begins in the institutional consulting arena. For years, consultants have advised endowments, foundations, and pension plans, all united by a common goal: to beat the market and their respective benchmarks. This ambition, while laudable, necessitated a rigorous framework for monitoring the myriad of active managers handling diverse asset classes – from stocks and bonds to hedge funds and private assets.

The Green, Yellow, Red System

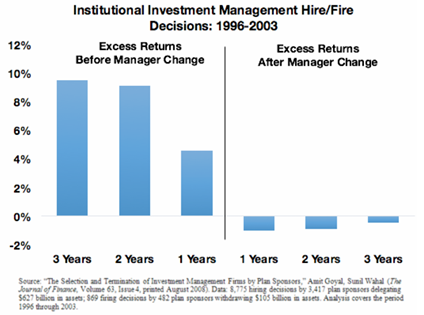

Investment committees and boards, responsible for overseeing these substantial non-profit portfolios, typically adopted a traffic-light system to grade their managers. Outperformers, those consistently delivering returns above their benchmarks, would be given a "green light." Managers with middling performance, hovering near their benchmarks, would receive a "yellow light." The underperformers, those trailing the market, would be relegated to a "red light," often placed on a "watch list" for potential dismissal. Quarterly updates on performance against benchmarks would dictate these designations, driving subsequent allocation decisions.

This system, while seemingly logical, often creates a self-defeating cycle. The instinct is to lean into the "green light" managers, increasing allocations to those showing recent strong performance, and to divest from the "red light" managers, cutting ties with those who have recently underperformed. The rationale is to ride the momentum of success and shed the drag of failure.

However, as experience and data consistently show, this momentum game can only work for so long. Markets are inherently dynamic, and outperformance, particularly for active managers, rarely persists indefinitely. Even the most celebrated and skilled investors in the world experience periods of underperformance. This leads to a common, yet often painful, scenario: a new manager is hired primarily because their recent returns look exceptional, only for them to underperform significantly shortly after being brought on board. While not universal, this pattern occurs with a frequency that challenges conventional wisdom, highlighting the pitfalls of making investment decisions based solely on backward-looking performance.

Empirical Evidence: The Persistence Paradox

The statistical reality of fleeting outperformance is rigorously documented by organizations like S&P Dow Jones Indices. Their annual SPIVA (S&P Index Versus Active) Persistence Scorecard provides an invaluable, data-driven look into how often manager outperformance in one period is followed by future outperformance. The results offer a stark counter-narrative to the common belief that past success is a reliable indicator of future returns.

SPIVA Scorecard Unveiled

The SPIVA Persistence Scorecard meticulously tracks the performance of active funds across various categories over consecutive periods. Its findings consistently demonstrate the extreme difficulty for active managers to maintain top-quartile performance. This robust, independently verified data serves as a critical barometer for the active management industry.

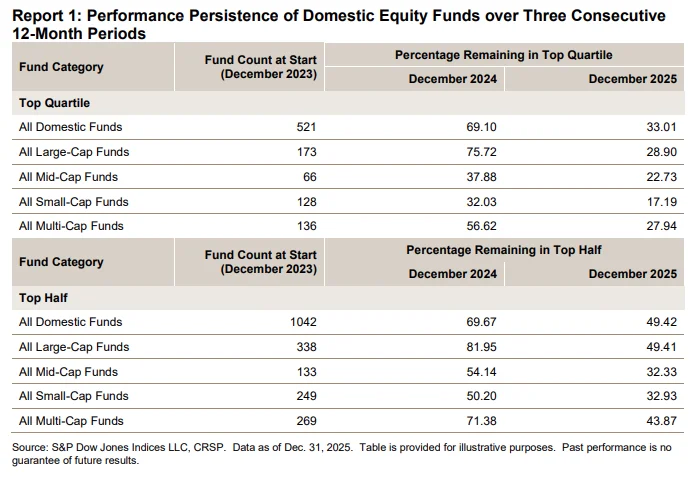

Consider the numbers for U.S. stock market funds over consecutive three-year periods, which paint a sobering picture:

- Of the funds in the top quartile of returns in 2023, approximately 69% managed to remain in the top quartile in 2024. This might seem encouraging at first glance, suggesting some degree of short-term persistence.

- However, when extended to a second consecutive year, the picture changes dramatically. Only 33% of the original top-quartile funds from 2023 were still in the top quartile in 2025. This sharp decline reveals the initial erosion of sustained outperformance.

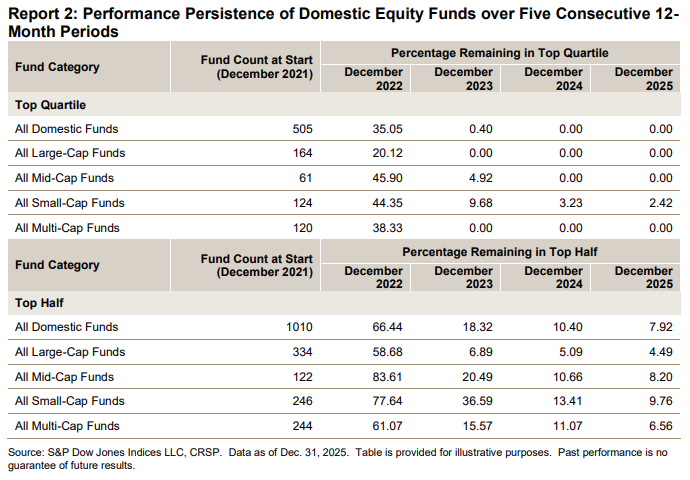

The trend becomes even more pronounced when examining performance over longer, five-year horizons:

- Starting in 2021, the data shows that virtually no funds (often less than 1%) managed to remain in the top quartile for three, four, or five consecutive years.

- Even broadening the scope to the top half of performers, less than 10% of funds could sustain a position in the top two quartiles for five consecutive years.

These statistics underscore a crucial insight: consistent outperformance is exceptionally rare. The vast majority of managers who excel in one period will, statistically speaking, revert to the mean or underperform in subsequent periods. This is not necessarily an indictment of their skill, but rather a reflection of market efficiency, the inherent randomness of short-term returns, and the competitive landscape of active management.

Why Outperformance Doesn’t Last

Several factors contribute to this pervasive lack of persistence:

- Market Efficiency: While markets are not perfectly efficient, they are highly competitive. New information is rapidly assimilated into prices, making it challenging for any single manager to consistently find undervalued assets or exploit mispricings.

- Mean Reversion: Assets and strategies that perform exceptionally well tend to revert to their average performance over time. What goes up aggressively often comes down, and vice versa. This natural tendency makes sustained streaks of extreme performance difficult.

- Luck vs. Skill: In any given period, a portion of a manager’s outperformance can be attributed to luck rather than genuine skill. Distinguishing between the two in real-time is nearly impossible, and what appears to be skill in one market cycle might simply be good fortune that doesn’t repeat.

- Fees and Costs: Active managers charge higher fees than passive index funds to cover research, trading, and operational costs. This higher hurdle means they must generate significant alpha just to break even with a benchmark, let alone consistently outperform it after costs.

- Increased Competition: The investment industry is filled with highly intelligent, well-resourced professionals all striving for an edge. This intense competition makes it harder for any single entity to maintain a durable advantage.

The conclusion is inescapable: investors must get used to the fact that nothing and no one can outperform the markets on a consistent basis. This fundamental reality is what makes active management so challenging. While stock-picking is inherently difficult, the evidence suggests that picking the managers who will consistently outperform the market might be an even harder endeavor.

Navigating the Modern Diversification Landscape

The principle that "nothing works all the time" extends beyond active management to virtually every investment strategy, whether active or passive. In an increasingly complex financial world, investors are constantly presented with new avenues for diversification, leading to both unprecedented opportunities and significant temptations.

The Lure of Novelty and "Diworsification"

In recent months, discussions with investors on various platforms have frequently revolved around the evolving concept of portfolio diversification. Common questions reflect a widespread desire to adapt portfolios to current market conditions:

- Is the traditional 60/40 portfolio (60% stocks, 40% bonds) still viable, or is it "dead"? Do we need to update this for modern times?

- What are the merits of adding alternative assets like gold or Bitcoin to a portfolio?

- Should investors consider sophisticated strategies such as trend-following or managed futures?

- How should fixed income exposure be diversified given the recent bond bear market?

- What about newer financial products like buffer ETFs or option income funds?

- Are private investments now accessible and appropriate for a broader range of investors?

The good news is that the current investment landscape offers an unparalleled array of opportunities for individual investors seeking to diversify their portfolios. Never before has there been such a wide selection of asset classes, strategies, and financial instruments available, allowing for highly customized approaches to risk management and return generation.

However, this abundance comes with a significant caveat: the temptation to overcomplicate. This can lead to what is often termed "diworsification" – a portmanteau of diversification and "worse," describing the act of adding too many funds, strategies, or obscure investments to a portfolio, thereby diluting returns, increasing complexity, and often failing to achieve true diversification benefits. This often stems from a fear of missing out (FOMO) on the latest hot trend or a relentless pursuit of the "perfect" portfolio, which by definition does not exist.

No Universal Blueprint: Tailoring Your Portfolio

There are no universally "right" or "wrong" answers when it comes to diversification and asset allocation. The optimal portfolio is deeply personal, influenced by an individual’s financial goals, time horizon, risk tolerance, and even their behavioral tendencies.

For some investors, simplicity is paramount. A minimalist approach, such as a 3-fund portfolio comprising total market stock, total international stock, and total bond index funds, can be highly effective. Others might even prefer a single target-date fund that automatically rebalances. For these individuals, anything more complex would be overwhelming, leading to anxiety and poor decision-making.

Conversely, other investors may prefer a more comprehensive approach, seeking to cover more "bases" from a diversification perspective. They might hold a variety of different funds, strategies, and asset classes in their portfolios, driven by a desire for greater resilience across various market conditions or a belief in the long-term benefits of uncorrelated assets.

The critical insight here is that the "perfect portfolio" is not a static ideal but a dynamic construct tailored to the individual. The challenge lies not in finding a universal solution, but in discovering what works best for you.

The Diversification Test: A Guiding Principle

Given the inherent difficulties in predicting market performance and the myriad of diversification options, how can an investor make sound, long-term decisions? The answer lies not in predicting the future, but in understanding one’s own conviction and the underlying rationale for each investment. This leads to a simple yet powerful litmus test for any portfolio holding: the diversification test.

The Core Question

The diversification test poses a straightforward question: "If your investment is down in value, will you lean into the pain and buy more?"

This question cuts to the core of investment discipline. Far too many institutional investors, driven by the green/yellow/red light system, would do the exact opposite. The moment a manager underperformed, the "eject button" would be hit, and funds would be withdrawn. This reactive behavior, fueled by short-term performance metrics and the fear of falling behind, is a classic example of buying high and selling low – the antithesis of successful investing.

The ability to lean into pain and buy more when an investment is down signifies a deep understanding and conviction in that investment. It indicates that the investor comprehends why they own it, beyond just its recent performance. This conviction is crucial because every investment, no matter how sound, will experience periods of underperformance.

The Power of Understanding and Simplicity

One of the primary reasons institutional investors struggle with this test is the complexity and discretionary nature of many active management strategies. When a manager employs a highly opaque or constantly shifting strategy, it becomes incredibly difficult for oversight committees to determine whether current underperformance is a temporary blip due to the strategy being "out of favor," or a fundamental flaw indicating that the strategy no longer works. This ambiguity often leads to doubt and, ultimately, to premature liquidation.

This highlights a significant advantage of rules-based strategies and index funds. With these approaches, the underlying methodology is transparent and predictable. When a rules-based strategy or an index fund experiences a dry spell, an investor who understands its construction and long-term rationale can be more confident in leaning into the pain and buying more. There is no guesswork about the manager’s current decisions; the process is clear.

While nothing is guaranteed in the markets, having a clear understanding of what you own and why you own it empowers you to set more reasonable expectations. This clarity fosters greater confidence in your chosen process, reducing the temptation to constantly jump in and out of different investments based on short-term fluctuations. It transforms investing from a reactive chase of performance into a disciplined execution of a well-understood plan.

Implications for Investors

The lessons from the challenges of active management and the enduring value of the diversification test have profound implications for both institutional and individual investors.

Beyond Chasing Returns

The primary implication is a necessary shift in focus. For too long, the narrative in investment management has centered on the elusive goal of "beating the market." While attractive, this pursuit often leads to suboptimal outcomes due to the psychological biases it engenders and the statistical improbability of sustained success. Instead, the focus should pivot to long-term wealth creation through disciplined, patient, and unemotional investing.

This means prioritizing a robust asset allocation strategy that aligns with one’s risk profile and goals, rather than constantly seeking the next market-beating manager or strategy. It involves recognizing that consistency in process often trumps chasing transient performance. For institutional investors, this might mean a deeper commitment to fewer, more transparent strategies and a willingness to ride out periods of underperformance when conviction remains high. For individual investors, it reinforces the power of simple, broad-market index funds and a consistent saving and investing plan.

Cultivating Resilience in Your Portfolio

Ultimately, the true test of any investment strategy or allocation is not how it performs when markets are soaring and everything is going up. That’s the easy part. The real measure of its suitability, and of an investor’s discipline, is how it holds up – and how the investor holds up – when it’s falling behind.

Cultivating resilience in a portfolio means building it with the expectation of volatility and periods of underperformance for various components. It means making proactive decisions based on a well-defined investment policy, rather than reactive ones driven by fear or greed. The diversification test serves as a powerful tool to ensure that every asset, every fund, and every strategy within a portfolio is held with genuine conviction, an understanding of its role, and the mental fortitude to stick with it through thick and thin. Only then can investors truly harness the long-term compounding power of the markets, irrespective of the short-term noise.

Further Reading:

- Creating the Perfect Portfolio

- How to Own the Best Stocks

- Nothing Works All The Time