Navigating the Nuances: A Deep Dive into Record ETF Growth, Retail Trading Surge, and Evolving Wealth Dynamics

Posted: June 12, 2026, by Ben Carlson

The financial world is currently a vibrant tapestry of paradoxes, where record-breaking achievements in passive investing coexist with a surge in individual speculation, and a seemingly shrinking middle class signifies upward mobility even as wealth concentration at the very top intensifies. A recent report from Bloomberg highlighted a monumental milestone: the Vanguard S&P 500 ETF (VOO) has become the first Exchange Traded Fund (ETF) in history to amass an astounding $1 trillion in assets under management. This landmark achievement underscores a broader, relentless march towards passive investment strategies, fundamentally reshaping the asset management industry.

Yet, this triumph of systematic, low-cost investing unfolds against a backdrop of unprecedented retail trading activity, driven by a new generation of investors engaging with markets in ways previously unimaginable. Concurrently, a deeper look into wealth distribution reveals a complex narrative: while more Americans are ascending into the upper-middle class, the wealthiest echelon of society has seen its share of the national pie expand dramatically, revealing persistent, and in some cases, exacerbating, inequalities. These seemingly contradictory trends paint a nuanced picture of an economy in constant evolution, defying simplistic interpretations and demanding a more comprehensive understanding.

The Trillion-Dollar Milestone: Passive Investing’s Unstoppable Ascent

A New Era for ETFs

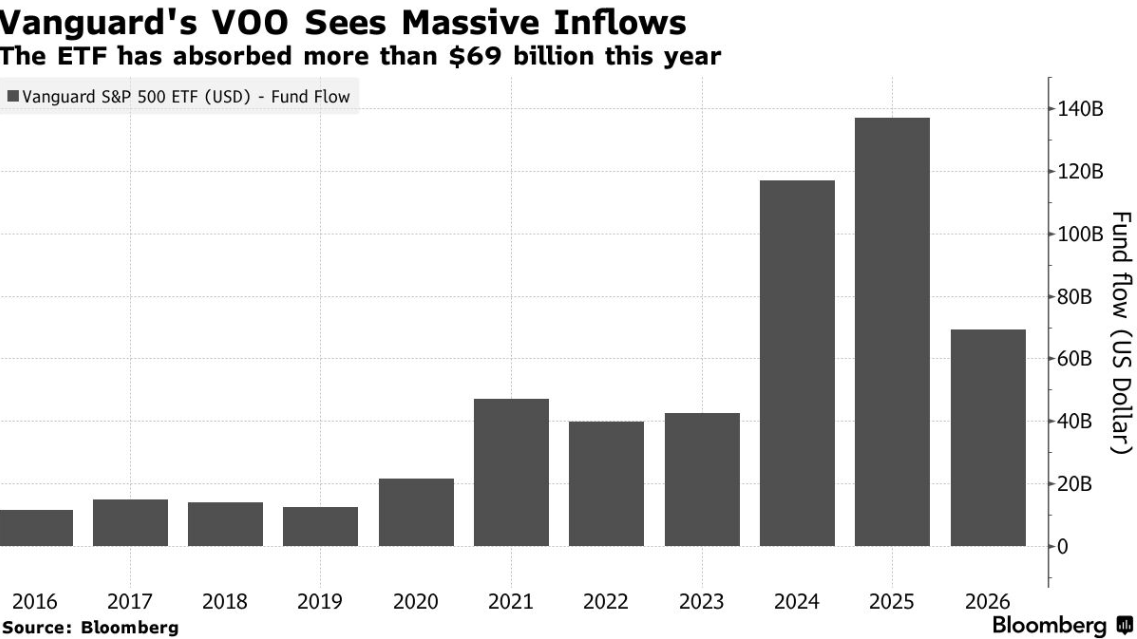

The announcement last week by Bloomberg, confirming that the Vanguard S&P 500 ETF (VOO) has crossed the $1 trillion threshold, marks a watershed moment in the history of financial products. This makes VOO not only the largest S&P 500-tracking ETF but also the first ETF of any kind to reach such a staggering valuation. Launched by Vanguard, a pioneer in low-cost indexing, VOO’s rapid ascent is a testament to the enduring appeal and effectiveness of passive investment strategies. The S&P 500 index itself, representing 500 of the largest U.S. publicly traded companies, serves as a bellwether for the American economy, and VOO’s massive asset base reflects widespread investor confidence in the long-term growth trajectory of these corporate giants.

The sheer volume of capital flowing into VOO demonstrates an unwavering commitment from investors, ranging from institutional behemoths to individual savers, to simple, diversified market exposure. These flows show no signs of abating, continuing a trend that has defined the financial landscape for over a decade. This phenomenon isn’t isolated to VOO; other major S&P 500 and broader market ETFs also command colossal asset bases. The SPDR S&P 500 ETF Trust (SPY), the oldest and most traded ETF, is rapidly approaching $800 billion in assets, while the iShares Core S&P 500 ETF (IVV) has already surpassed $800 billion. Furthermore, the Vanguard Total Stock Market ETF (VTI), which offers an even broader exposure to the entire U.S. equity market (and thus includes S&P 500 companies as its core), manages over $660 billion. These figures collectively illustrate an undeniable reality: an immense and continuously growing pool of capital is being directed towards passively managed, broad-market index funds.

The Shifting Landscape of Fund Management

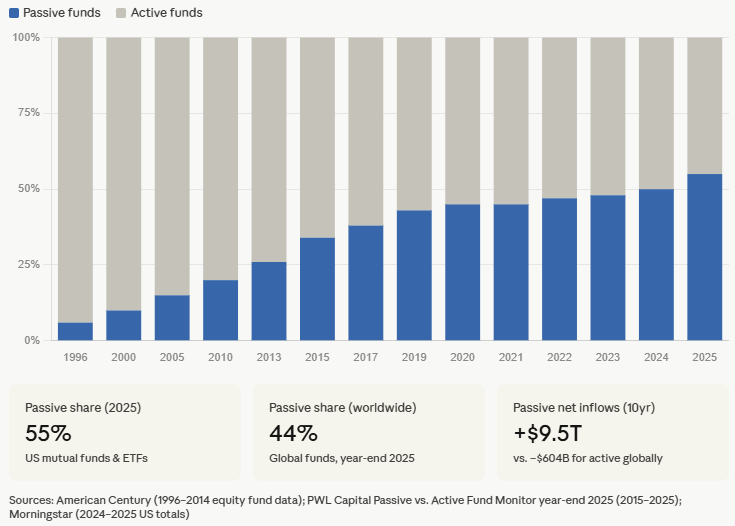

The rise of these trillion-dollar ETFs is emblematic of a seismic shift within the fund industry, where passive investment strategies are increasingly "swallowing active share." For decades, active fund managers, who attempt to outperform market benchmarks through stock picking and market timing, dominated the investment landscape. Investors paid higher fees, hoping for superior returns. However, academic research, coupled with the persistent underperformance of a significant majority of active funds after fees, gradually eroded this dominance. The allure of lower costs, broad diversification, and the simple elegance of tracking the market has proven irresistible to a growing number of investors.

This trend is starkly illustrated by data showing a relentless march of assets from active to passive management. The expectation among many financial experts is that passive funds could eventually account for 70-80% of all assets within the fund industry. The reasons are multifaceted: lower expense ratios (often a fraction of active funds), tax efficiency, transparency, and the inherent difficulty for human managers to consistently beat sophisticated algorithms and market efficiency over the long run. The transition reflects a growing understanding among investors that simply capturing market returns at the lowest possible cost is often the most effective path to wealth accumulation.

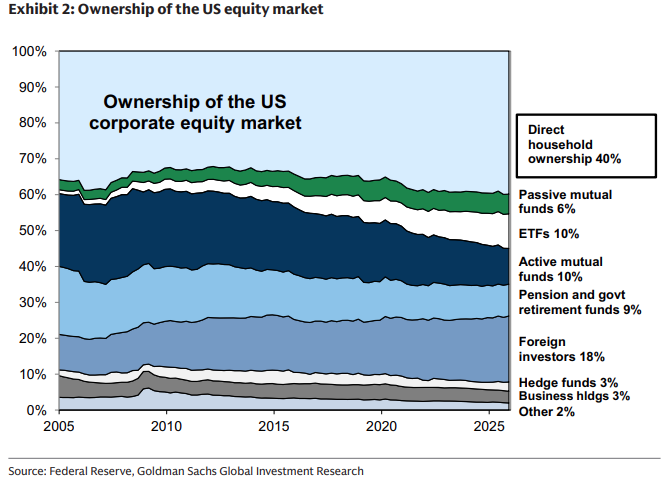

It is crucial, however, to contextualize this shift: the statistics reflecting passive dominance primarily pertain to the fund industry. This does not equate to the entire stock market overall. A significant portion of the stock market is still owned directly by individuals, corporations, private equity firms, and other entities that do not fall under the umbrella of publicly traded funds. While passive funds’ ownership share of the overall market has grown, it remains a smaller percentage than its dominance within the fund industry suggests. This distinction is vital for understanding market dynamics, particularly concerning issues like corporate governance and price discovery, where active managers traditionally played a more direct role.

The Retail Renaissance: A Surge in Individual Speculation

The Rise of the DIY Investor

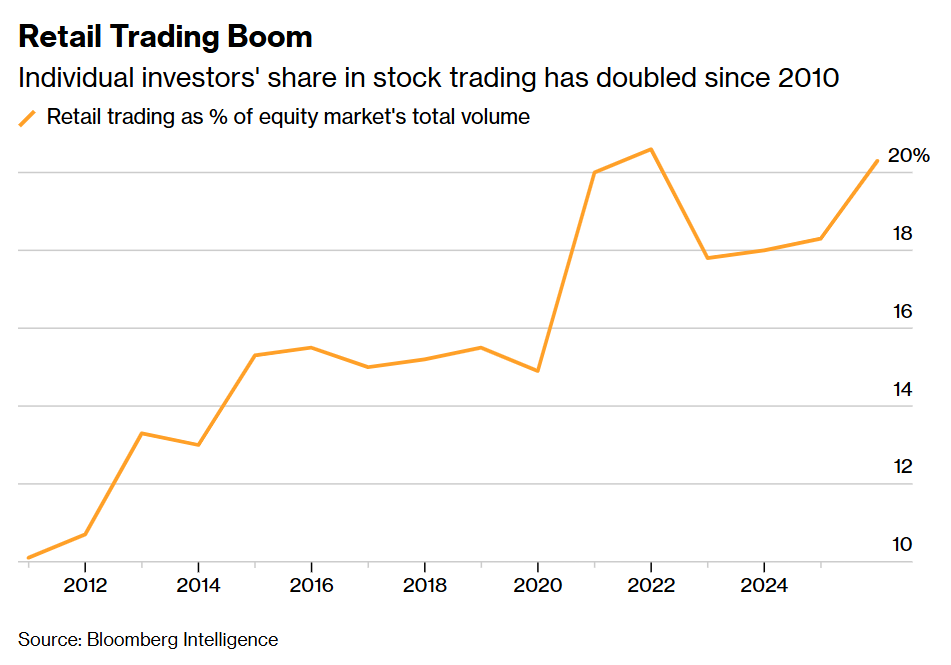

Parallel to the institutionalization of passive investing, the current decade has witnessed an unprecedented explosion in retail trading activity. Individual investors now constitute a significantly larger share of overall market trading volume than they did in the 2010s. This dramatic leap began around 2020, catalyzed by a confluence of factors: government stimulus checks providing disposable income, widespread lockdowns fostering more time for financial exploration, and the proliferation of commission-free trading platforms like Robinhood. These platforms, often featuring gamified interfaces and easy access to complex financial instruments, lowered the barrier to entry for millions of new investors.

The result has been a vibrant, and at times volatile, retail trading community. Social media platforms have become de facto trading desks, with communities forming around "meme stocks," cryptocurrencies, and other speculative assets. This democratized access has empowered individuals to participate directly in markets, moving beyond traditional mutual funds and advisory services. While this increased participation can be viewed as a positive step towards financial inclusion, it also brings a heightened level of speculative activity, sometimes driven by sentiment and online trends rather than fundamental analysis.

Contrasting Investment Philosophies

This juxtaposition creates a fascinating dichotomy in today’s financial markets. On one hand, trillions of dollars are systematically flowing into "boring" index funds, representing a long-term, low-risk approach to wealth building. This segment of the market embodies a belief in broad market efficiency and the power of compounding over time. On the other hand, a growing cohort of retail traders is actively speculating, seeking quick gains through often high-risk ventures in individual stocks, options, and volatile digital assets.

This simultaneous existence of vastly different investment philosophies within the same market ecosystem raises questions about market stability, price discovery, and investor behavior. Are these two groups entirely separate, or do individuals often engage in both strategies – using passive funds for their core long-term savings while allocating a smaller portion to speculative trading? The answer is likely the latter, reflecting a pragmatic approach by many to balance prudence with the pursuit of higher, albeit riskier, returns. This dynamic environment suggests that the market caters to a "narrative for everyone," from the patient, long-term indexer to the agile, speculative day trader.

Wealth Distribution in Flux: A Tale of Two Trends

The Shrinking Middle Class: An Upward Migration

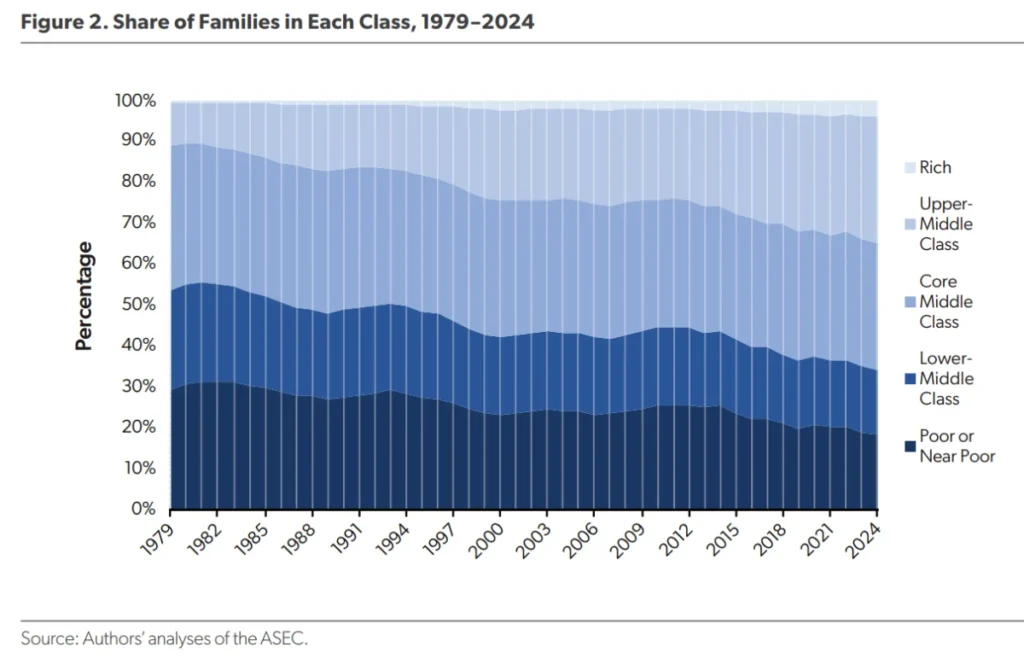

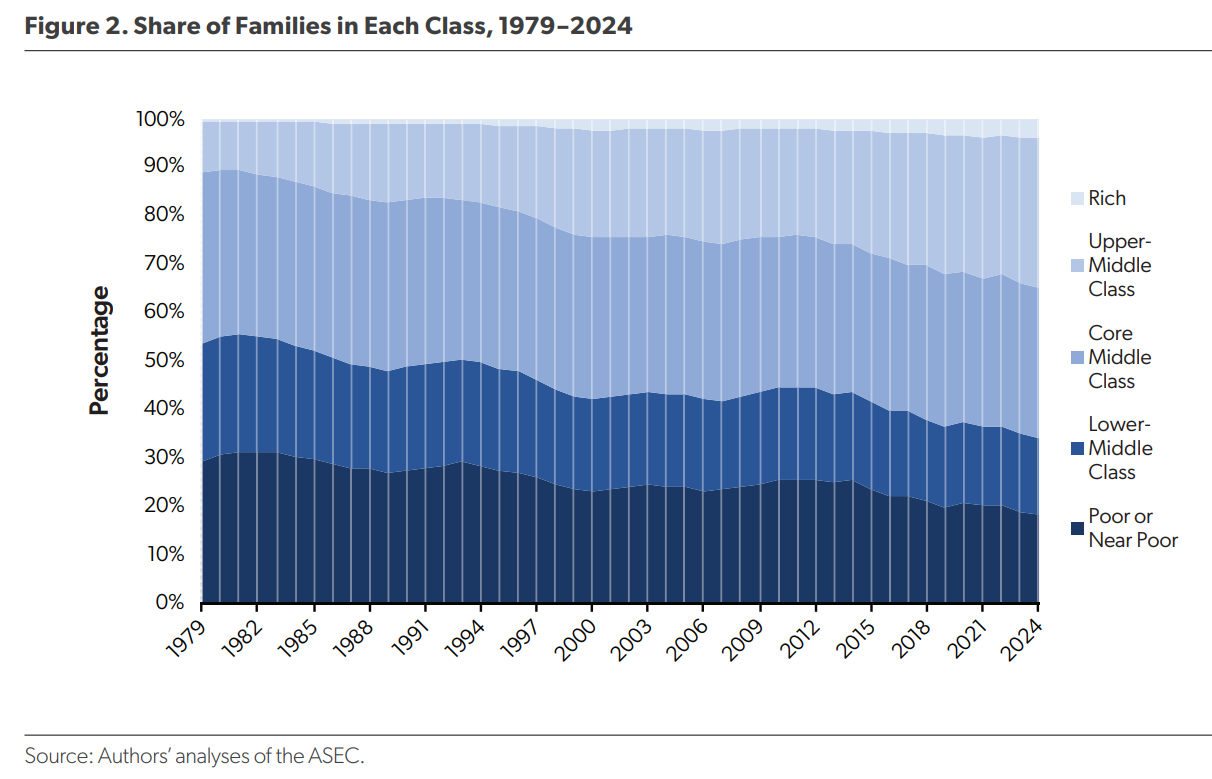

Beyond the financial markets, a similarly nuanced picture emerges when examining wealth distribution in the United States. A recent report from the American Enterprise Institute (AEI) highlights a long-term trend of a shrinking middle class. However, the report’s key finding provides a crucial reinterpretation: the middle class is shrinking primarily because more households are moving up into the upper-middle class, rather than down into lower economic strata. This represents a significant and positive societal development, indicating a degree of upward mobility and general economic progress for a substantial portion of the population.

The data presented by AEI illustrates this migration clearly. In 1979, 24% of American households were categorized as lower-middle class, while 30% were classified as poor or near-poor. By the latest reading, these numbers had significantly dropped to 16% and 19%, respectively. Concurrently, the upper-middle class has experienced a dramatic expansion, swelling from just 10% of households in 1979 to a robust 31%. This means that the upper-middle class is now as large as the traditional "core" middle class and nearly equals the combined total of the lower-middle class and poor segments of society. This upward shift signifies genuine progress in household wealth and living standards for millions of Americans, challenging simplistic narratives of universal economic stagnation or decline.

The Concentrated Gains at the Top

Despite this encouraging upward mobility, another critical aspect of wealth distribution simultaneously reveals a widening chasm at the very apex of the economic pyramid. An op-ed in The New York Times, referencing the same underlying study on wealth distribution, brought to light the disproportionate gains accumulated by the wealthiest families. While the overall economic "pie" has grown, and most groups have seen an increase in their absolute wealth, the share of that pie held by the middle and even upper-middle classes has decreased, while the ultra-rich have seen their slice expand dramatically.

Specifically, the share of wealth held by the middle class fell drastically from 24% in 1989 to a mere 8% in 2022. Even the upper-middle class, which has grown in size, saw its share of overall wealth decline from 50% to 39% over the same period. In stark contrast, the wealthiest families – a group comprising just 3% of all households in 2022 – saw their share of national wealth more than double, soaring from 26% to an astonishing 53%. This means that a minuscule segment of the population now controls over half of the nation’s total wealth. This stark redistribution of wealth towards the very top, even amidst overall economic growth and middle-class expansion, highlights a critical challenge of modern capitalism. It suggests that while many are doing better, the rich are getting "much, much richer" at an accelerated pace, leading to unprecedented levels of wealth concentration.

Official Responses and Expert Commentary

Navigating Economic Realities

The complex interplay of these financial and economic trends naturally draws the attention of policymakers, economists, and market analysts. The explosive growth of passive investing, while lauded for its efficiency and low costs for everyday investors, also sparks debates about its long-term implications for market structure, corporate governance, and price discovery. Some experts voice concerns that if passive ownership becomes too dominant, it could lead to less active oversight of corporate management and potentially exacerbate market bubbles or crashes due to herd mentality. Regulators are closely watching, seeking to balance the benefits of accessibility with potential systemic risks.

The surge in retail trading, while empowering individual investors, also raises questions about investor protection and market stability. The speculative nature of some retail-driven phenomena, such as "meme stock" rallies or volatile cryptocurrency trading, has prompted calls for increased financial literacy education and clearer regulatory guidelines to safeguard less experienced investors from potential significant losses. Conversely, proponents argue that increased retail participation fosters a more inclusive financial system and can provide valuable liquidity to markets.

Regarding wealth distribution, the AEI report’s optimistic view of an expanding upper-middle class offers a counter-narrative to traditional discussions of middle-class stagnation. However, the accompanying data on extreme wealth concentration among the top 3% fuels ongoing political and economic debates. Policymakers grapple with how to address this growing disparity without stifling economic growth or innovation. Discussions often revolve around progressive taxation, wealth taxes, inheritance laws, access to quality education, and opportunities for skill development as potential levers to promote greater equity. The challenge lies in finding policies that support broad-based prosperity without hindering the dynamism that drives economic advancement. As Ben Carlson aptly concludes, "Nuance is a lost art in a world filled with outrage. Things are rarely black and white but rather a shade of gray." This perspective is crucial for understanding these multifaceted economic realities.

Broader Implications and Future Outlook

The Interplay of Forces

The intricate relationship between these trends has profound implications for the future of capital markets, individual financial well-being, and societal cohesion. The ascendance of passive investing, by channeling vast sums into the largest, most established companies, could inadvertently contribute to the concentration of wealth by disproportionately benefiting the owners of these dominant enterprises. Simultaneously, while the rise of retail trading democratizes market access, it also presents a double-edged sword: for those who navigate it successfully, it can be a path to wealth, but for others, particularly those engaging in high-risk speculation without adequate knowledge, it could lead to significant financial setbacks, potentially widening individual wealth gaps.

The fact that more people are moving into the upper-middle class suggests a baseline of economic improvement, yet the ever-increasing share of wealth held by the ultra-rich points to fundamental structural issues. This dynamic could fuel social and political tensions if not carefully managed. The financial landscape of tomorrow will likely be shaped by how these forces continue to interact. Will the efficiency of passive investing eventually clash with the need for active market governance? Will the exuberance of retail speculation be tempered by a greater emphasis on long-term planning? And critically, can societies find a way to foster widespread economic opportunity while mitigating the corrosive effects of extreme wealth inequality?

Shaping the Financial Landscape of Tomorrow

Looking ahead, the financial industry will continue to innovate, offering new products and platforms to cater to diverse investor appetites. The ongoing debate between efficiency and equity will remain at the forefront of economic discourse. For individuals, the challenge will be to navigate an increasingly complex financial ecosystem, making informed decisions that align with their personal goals and risk tolerance. Whether through disciplined passive investing or strategic engagement in specific market opportunities, financial literacy and critical thinking will be more vital than ever. The future will demand not just an understanding of these individual trends, but a comprehensive appreciation for their interconnectedness and the nuanced truths they reveal about our evolving economic world.