America at 250: A Century of Market Dynamics Unveiled

By [Your Name/Journalist Alias]

Posted: July 7, 2026

As the United States proudly marks its semiquincentennial this Independence Day, a milestone that underscores 250 years of remarkable national evolution, attention naturally turns to the pillars that have shaped its journey. Among these, the U.S. stock market stands as a profound testament to the nation’s economic resilience, innovation, and enduring spirit of enterprise. Amidst the recent historical discourse leading up to this quarter-millennium anniversary, financial analyst Ben Carlson has offered a compelling visual retrospective on the U.S. stock market’s performance, drawing insights from nearly a century of data.

Carlson’s analysis, spanning from 1928 through the close of 2025, provides a panoramic view of market cycles, illustrating not just the raw numbers but the inherent temperament of American capitalism. Eschewing complex narratives in favor of clear data visualization, much like filmmaker Taylor Sheridan’s maxim to "never have a character tell me something that the camera should show me," Carlson’s work reveals the fundamental truths embedded within market history: a consistent upward trajectory punctuated by inevitable, yet often fleeting, downturns. This deep dive into the market’s past offers invaluable lessons for investors, policymakers, and anyone seeking to understand the economic heartbeat of a nation celebrating 250 years of self-governance.

Main Facts: The Market’s Enduring Rhythm

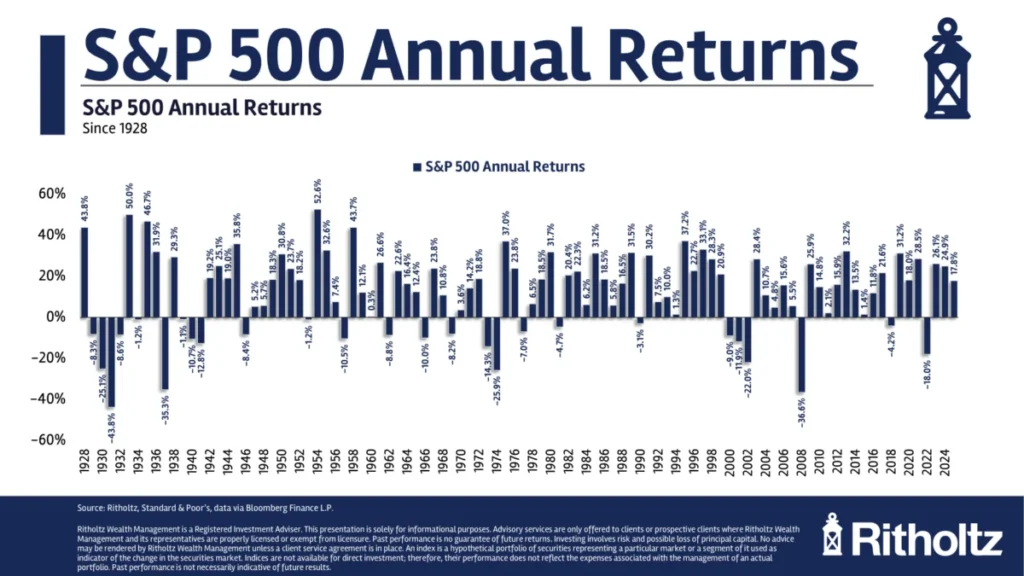

Ben Carlson’s comprehensive review of U.S. stock market performance from 1928 to 2025 illuminates several key facts that underscore the market’s long-term characteristics:

- Consistent Average Growth: Over the nearly century-long period, the U.S. stock market has delivered an impressive average annual return of 10%. This figure represents the powerful compounding effect of sustained economic growth and corporate profitability.

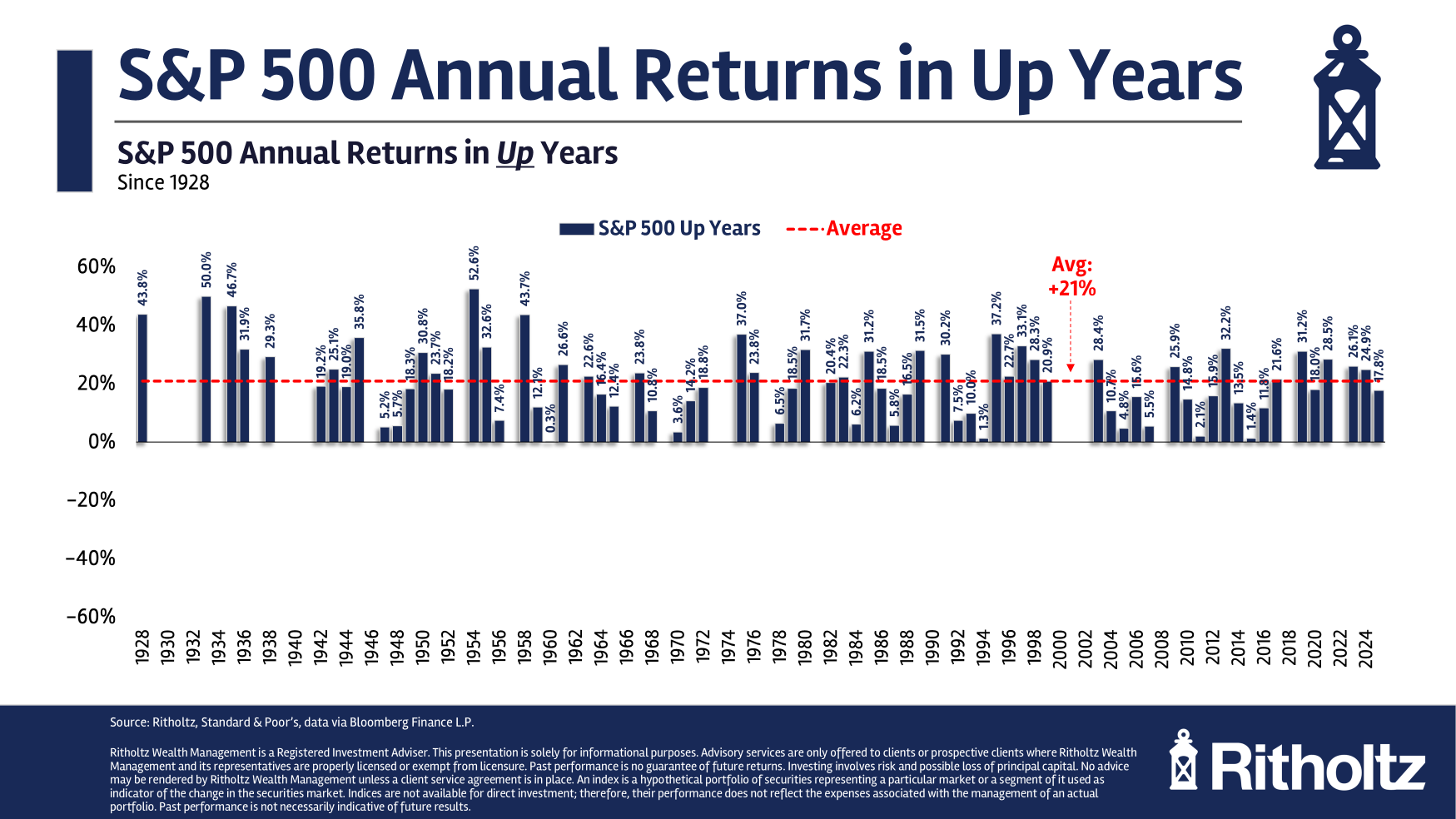

- Dominance of Up Years: Contrary to the common perception of relentless volatility, the data reveals a striking preponderance of positive annual returns. Out of the 98 calendar years analyzed (1928-2025), a remarkable 72 years concluded with positive gains. If current trends hold for 2026, this would extend to 73 positive years out of 99, a win rate exceeding 73%.

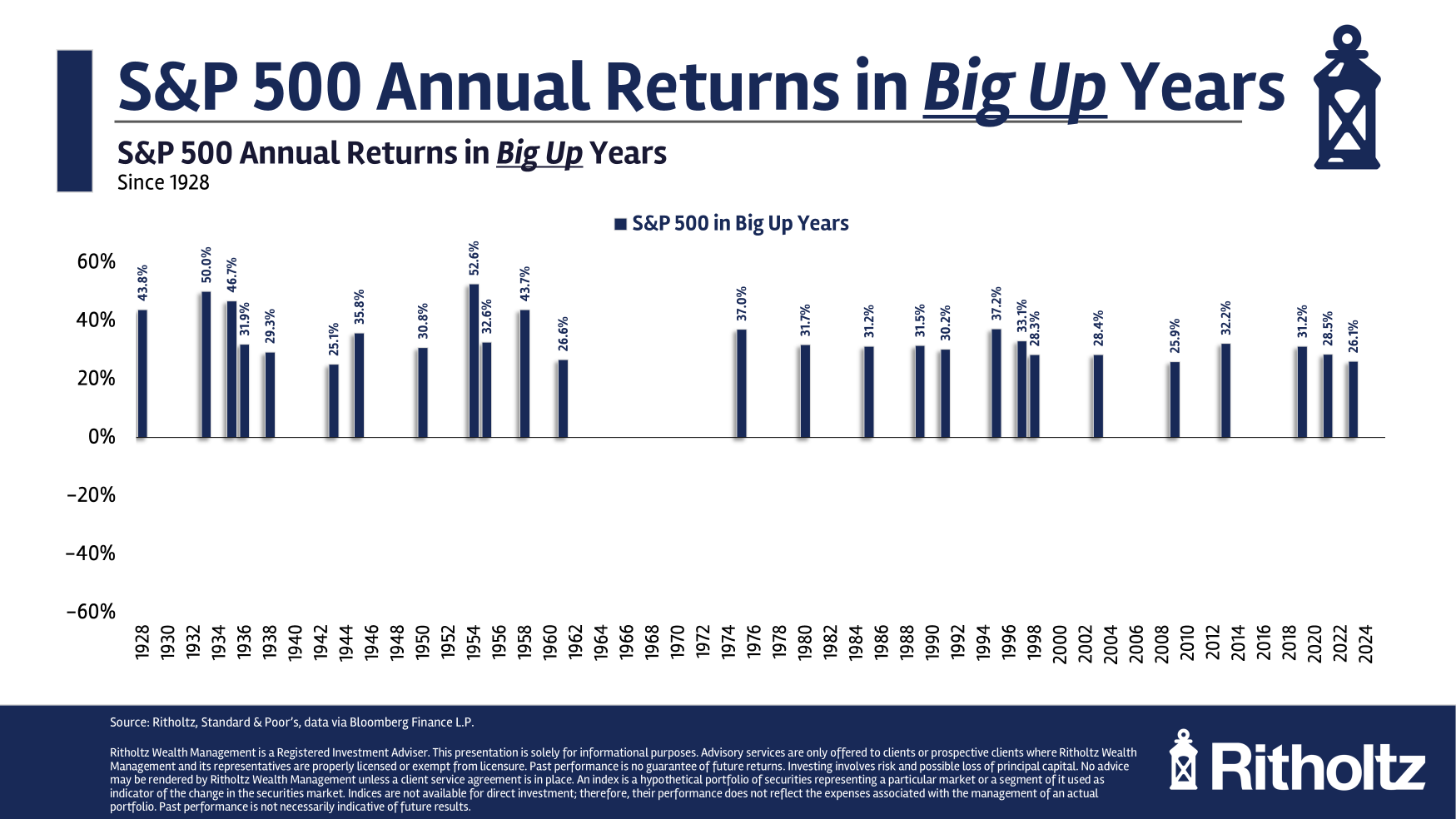

- Frequency of "Big Up Years": The market has demonstrated a strong propensity for significant growth spurts. There have been 26 calendar years where gains exceeded 25%, with 18 of these years seeing returns of 30% or higher.

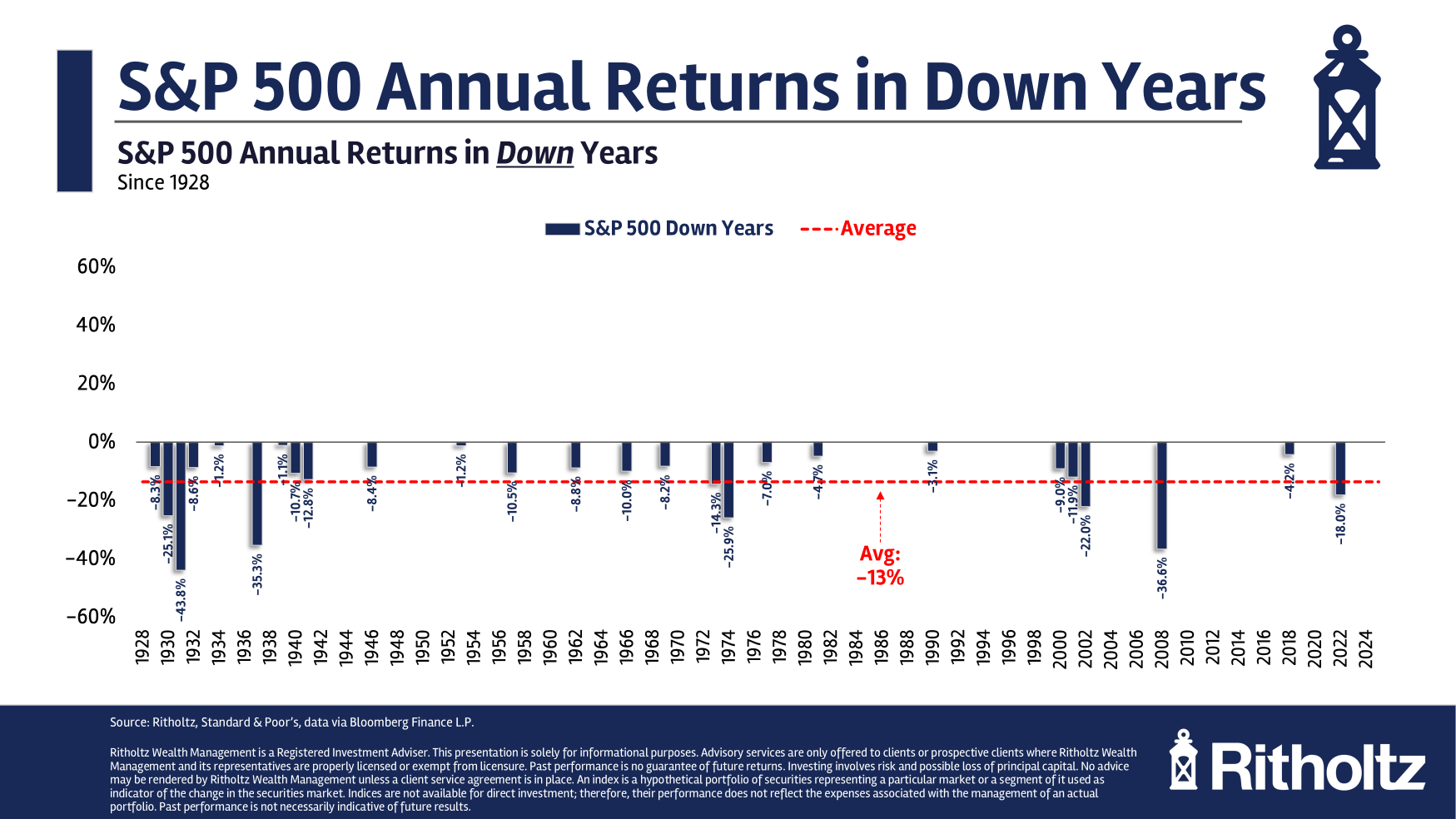

- Rarity of "Big Down Years": Conversely, severe downturns are far less frequent. Only five years in the entire period experienced losses greater than 25%. Notably, three of these occurred during the tumultuous 1930s, leaving only two such instances since the end of World War II.

- Unpredictable Short-Term, Predictable Long-Term: Carlson emphasizes that year-to-year returns are inherently unpredictable, lacking discernible patterns. However, the overarching historical trend points to a market that, more often than not, trends upwards.

These findings serve as a powerful counter-narrative to the often-anxiety-inducing headlines of daily market fluctuations, grounding investment perspectives in the tangible reality of historical performance.

A Century in Review: Chronology of Market Milestones

To truly appreciate Carlson’s data, it’s essential to contextualize these market movements within the broader sweep of American history. While his analysis begins in 1928, understanding the preceding and subsequent eras provides critical insight into the forces shaping market behavior.

The Roaring Twenties and the Great Depression (1920s-1930s)

The starting point of Carlson’s data, 1928, was the cusp of an era of unprecedented prosperity followed by economic catastrophe. The "Roaring Twenties" were characterized by rapid industrial growth, consumerism, and widespread speculative investing. The stock market, fueled by easy credit and public enthusiasm, soared to unsustainable heights.

The subsequent crash of October 1929 marked the beginning of the Great Depression, a decade of profound economic hardship. Carlson’s data starkly illustrates this period’s impact: three of the five "big down years" (losses exceeding 25%) occurred in the 1930s. These years saw immense wealth destruction, bank failures, and widespread unemployment, profoundly shaping public perception of financial markets for generations. The experience led to significant regulatory reforms, including the establishment of the Securities and Exchange Commission (SEC), aimed at preventing future excesses.

Post-War Boom and Mid-Century Stability (1940s-1960s)

The end of World War II ushered in an era of unprecedented economic expansion in the United States. Returning soldiers, fueled by the GI Bill, spurred a housing boom, and industries retooled from wartime production to consumer goods. This period saw sustained economic growth, a burgeoning middle class, and a generally robust stock market. While there were occasional corrections, the underlying trend was overwhelmingly positive, characterized by several of Carlson’s "big up years" as the nation solidified its position as a global economic powerhouse. The market’s resilience during this time helped restore investor confidence after the trauma of the Depression.

Stagflation and Volatility (1970s)

The 1970s presented a unique challenge to the U.S. economy: "stagflation," a perplexing combination of high inflation and stagnant economic growth. Energy crises, geopolitical tensions, and shifting global economic dynamics led to significant market volatility. This decade served as a reminder that economic conditions could shift dramatically, impacting corporate earnings and investor sentiment. While not characterized by the extreme "big down years" of the 1930s, it was a period where market gains were harder to come by, and inflation eroded purchasing power.

The Rise of the Internet and Modern Markets (1980s-2000s)

The latter part of the 20th century saw a dramatic transformation of the U.S. economy, driven by technological innovation and globalization. The 1980s and 1990s witnessed extended bull markets, particularly with the advent of the personal computer and the internet. The "dot-com bubble" of the late 1990s exemplified both the exuberance and the eventual overvaluation that can characterize periods of rapid technological change. Its burst in the early 2000s resulted in a significant, though not "big down year" by Carlson’s 25% threshold, correction, primarily impacting technology stocks.

The Global Financial Crisis and Beyond (2008-2025)

The Global Financial Crisis of 2008-2009 was the most severe economic downturn since the Great Depression. Triggered by a collapse in the housing market and subsequent failures in the financial system, it led to widespread panic and a significant market decline, marking one of Carlson’s rare "big down years" post-WWII. However, this crisis also highlighted the market’s capacity for recovery, albeit with substantial government intervention. The subsequent decade, characterized by low interest rates and quantitative easing, saw a sustained bull market, punctuated by the brief but sharp pandemic-induced downturn of early 2020, which quickly recovered. The period leading up to 2025 has seen continued adaptation to new economic realities, including inflation and geopolitical shifts, yet the overall trajectory, as Carlson’s data suggests, remains upward.

Supporting Data: Visualizing Market Realities

Carlson’s decision to use visual data — "show, don’t tell" — is crucial for understanding the market’s true nature. The average annual return of 10% is a powerful long-term statistic, but it rarely reflects the actual experience of investors in any given year.

The Reality of Annual Fluctuations

The initial chart of annual calendar year returns from 1928 through 2025 vividly displays the market’s jagged path. While the average is 10%, individual years rarely hit this mark precisely. Returns swing wildly, from significant gains to notable losses. This volatility is the "price of admission" for the long-term rewards offered by equity investing. It underscores the importance of a long-term investment horizon, allowing time for compounding returns to smooth out short-term turbulence.

The Power of Positive Momentum

By separating "up years" from "down years," Carlson’s subsequent charts offer a compelling perspective. The visual representation of predominantly green bars (up years) far outnumbering red bars (down years) is a powerful psychological anchor. The fact that roughly three out of every four years end in positive territory is a fundamental, yet often overlooked, characteristic of the U.S. stock market. This high "win rate" is a testament to the underlying engine of corporate innovation, productivity growth, and adaptive economic policies that have propelled American enterprise for centuries. It suggests that patience and consistent investment, rather than attempts to time the market, are often rewarded.

The Asymmetry of Extremes

Perhaps the most reassuring aspect of Carlson’s data is the stark contrast between "big up years" and "big down years." The visual evidence of numerous tall green bars representing gains of 25% or more, compared to the sparse, short red bars indicating losses of 25% or more, is striking.

- Frequent Windfalls: The 26 years with gains exceeding 25% (including 18 years with 30%+ returns) highlight the market’s capacity for substantial wealth creation. These periods often coincide with technological revolutions, post-recession recoveries, or robust economic expansions. For instance, the post-WWII boom, the Reagan era, and the late 1990s tech surge all contributed to multiple "big up years."

- Rare, but Painful, Declines: The extreme rarity of "big down years" (only 5 in 98 years, with 3 in the 1930s) underscores their historical significance. These events, like the 1929 crash, the 1973-74 bear market, and the 2008 financial crisis, are deeply etched into collective memory precisely because of their infrequency and severity. Their infrequency means that while they are psychologically challenging, they are not the norm, and the market has historically recovered from each of them.

This asymmetry reinforces the idea that while losses can be painful, the market’s historical tendency is to deliver larger and more frequent positive returns over the long run.

Official Responses and Expert Commentary: Navigating the Market’s Currents

While there aren’t "official responses" to a historical data analysis in the traditional sense, Carlson’s findings resonate deeply with established financial wisdom and the perspectives of leading economists and investment strategists.

Financial academics and practitioners have long emphasized the importance of a long-term perspective in equity investing. Figures like Nobel laureate Eugene Fama, whose work on efficient markets underpins much of modern finance, would acknowledge that while short-term movements are unpredictable, long-term trends are driven by fundamental economic growth and risk premiums. The market’s consistent average return of 10% over nearly a century is often cited as evidence of the equity risk premium – the extra return investors demand for taking on the higher risk associated with stocks compared to safer assets like bonds.

Behavioral economists, such as Daniel Kahneman, whose work highlights cognitive biases, would explain why "down years" feel disproportionately worse than "up years" feel good. This phenomenon, known as "loss aversion," means investors often react more strongly to losses, leading to panic selling at precisely the wrong time. Carlson’s visual evidence of more up years than down years, and more big up years than big down years, serves as a powerful antidote to this emotional bias, providing a rational basis for maintaining composure during market corrections.

Investment strategists consistently advocate for diversification, regular rebalancing, and maintaining a consistent investment strategy regardless of short-term market noise. They would point to Carlson’s data as empirical proof that "time in the market" generally outperforms "timing the market." The market’s high "win rate" and the powerful effect of compounding over decades are the cornerstones of successful long-term investing. Moreover, the historical resilience of the U.S. market, recovering from wars, pandemics, and financial crises, speaks to the adaptive capacity of American enterprise and its capital markets.

Implications: Lessons for the Next Quarter-Millennium

Carlson’s analysis, presented on the occasion of America’s 250th anniversary, carries profound implications for investors, economic observers, and the nation’s financial future.

For Investors: The Virtue of Patience and Perspective

The most significant implication for individual investors is the reinforcement of a long-term, patient approach. The data unequivocally demonstrates that:

- Market corrections are normal, but growth is the default. Investors who panic and sell during downturns often miss the subsequent recovery, which, as history shows, is more frequent and often more robust than the preceding decline.

- Compounding is powerful. An average annual return of 10% over decades can transform modest investments into substantial wealth. This power is only realized by staying invested through both good times and bad.

- Embrace volatility. While uncomfortable, market fluctuations are a feature, not a bug, of healthy capital markets. They create opportunities for those with a disciplined investment strategy, such as dollar-cost averaging, to buy assets at lower prices.

- Focus on the long game. Trying to predict year-to-year returns is futile. Instead, investors should focus on their financial goals, asset allocation, and risk tolerance, allowing the historical tendency of the market to work in their favor over time.

For the Economy: A Resilient Engine of Wealth Creation

Beyond individual portfolios, the historical performance of the U.S. stock market reflects the dynamism and resilience of the American economy itself. It serves as a vital mechanism for capital allocation, channeling savings into productive enterprises, fostering innovation, and creating jobs. The market’s consistent long-term growth is a direct reflection of:

- Corporate ingenuity: American companies, from startups to multinationals, have consistently adapted, innovated, and generated profits, driving economic expansion.

- Adaptive policies: While not always perfect, economic policies have generally supported growth, free markets, and property rights, creating an environment conducive to investment.

- Demographic and technological tailwinds: Over the past century, population growth, technological advancements, and increasing productivity have provided fundamental support for economic and market expansion.

The market’s ability to recover from severe shocks, as seen repeatedly throughout history, underscores the fundamental strength and adaptive capacity of the American economic system.

Looking Forward: The Enduring Rule of Thumb

As America steps into its next quarter-millennium, the lessons from its financial past remain incredibly relevant. While the future will undoubtedly bring new challenges – technological disruptions, environmental shifts, geopolitical complexities – the fundamental historical pattern of the U.S. stock market offers a powerful guiding principle.

Ben Carlson’s concise concluding rule of thumb encapsulates this wisdom perfectly: "Sometimes the stock market goes down but most of the time it goes up." This simple truth, backed by nearly a century of empirical data, should serve as a bedrock principle for navigating the ever-evolving landscape of investment and economic progress. The semiquincentennial is not just a moment to reflect on the past, but to draw strength and lessons from it, particularly in understanding the enduring potential of the American economy and its capital markets.