Navigating the FIRE Path: Cash vs. Bonds in a Barbell Portfolio for Early Retirement

Main Facts:

A burgeoning number of individuals are actively pursuing Financial Independence, Retire Early (FIRE), an ambitious movement focused on aggressive savings and investments to achieve financial autonomy decades ahead of traditional retirement age. A reader, currently in their mid-30s and on track to hit their FIRE target by age 40 with their spouse, recently posed a critical asset allocation question. Dissatisfied with traditional bond investments, the reader proposes a "barbell portfolio" strategy: maintaining a substantial cash position—equivalent to approximately two years of expenses—in a high-yield savings account, alongside an aggressive mix of U.S. and international equity exchange-traded funds (ETFs). The core inquiry: Is this strategy financially sound, or does it risk "leaving money on the table" by eschewing bonds or other low-risk alternatives?

This query delves into the intricate dynamics of asset allocation, particularly for those with unique financial timelines and risk appetites like FIRE aspirants. It pits the perceived safety and liquidity of cash against the historical role and potential returns of bonds, examining their respective merits and drawbacks within a modern investment framework. The debate transcends mere theoretical discussion, offering practical implications for how early retirees structure their portfolios to navigate market volatility, inflation, and the inherent uncertainties of a prolonged retirement.

Chronology: A Historical Perspective on Asset Performance

To adequately address the reader’s question, it’s essential to contextualize the performance of stocks, bonds, and cash through various economic cycles. The concept of a barbell portfolio, with its distinct allocation to high-risk (stocks) and "risk-free" (cash/equivalents) assets, naturally invites a comparison across these categories. While no investment is truly risk-free—as even cash is susceptible to inflation’s erosion of purchasing power—the term in finance typically refers to assets with minimal nominal price volatility.

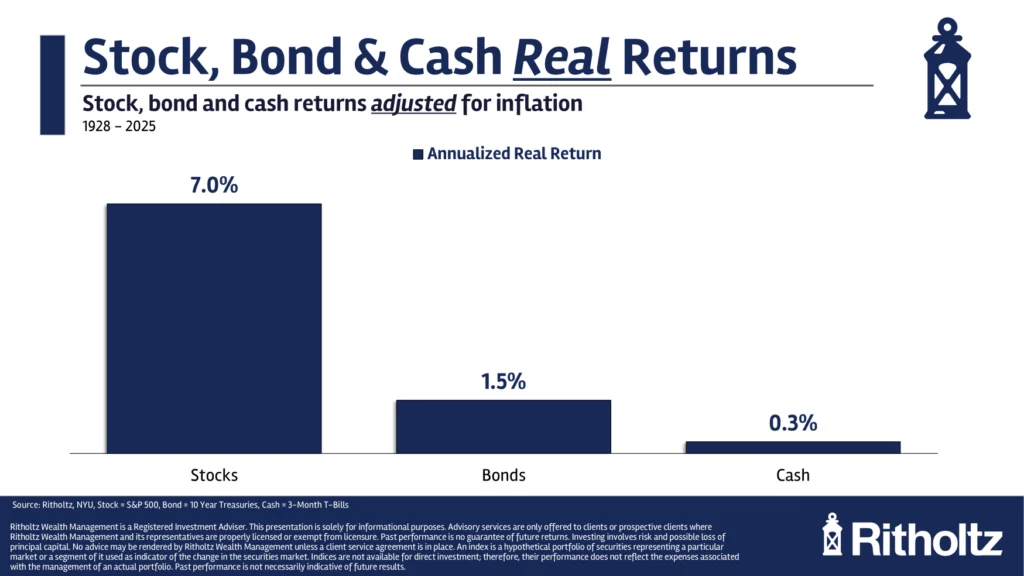

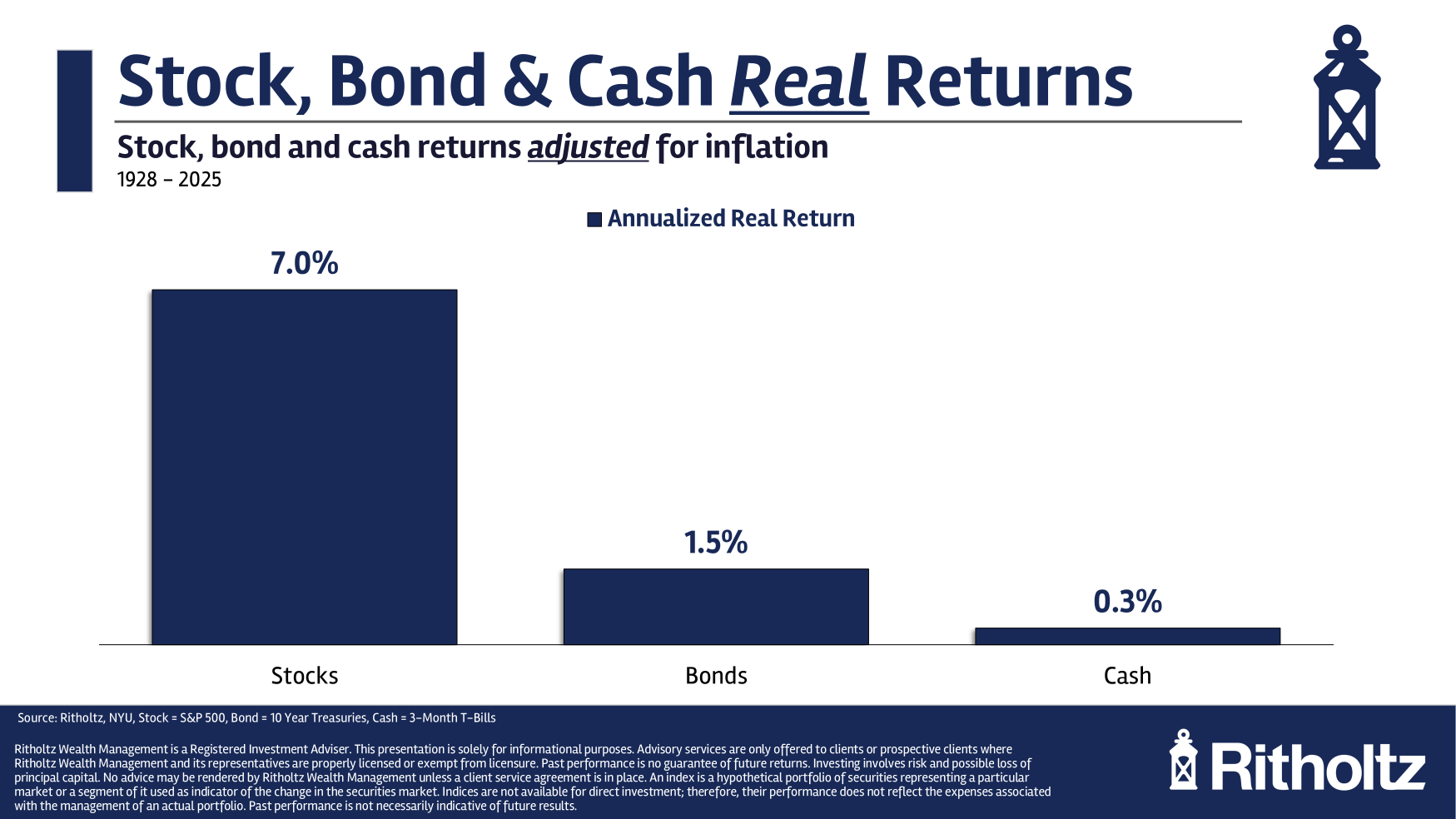

Historically, stocks have been the engine of long-term wealth creation, offering the highest nominal and real returns over extended periods. Bonds, traditionally, have served as a portfolio ballast, providing diversification, income, and capital preservation during equity downturns. Cash, or cash equivalents like short-term U.S. Treasury bills (T-bills), has primarily offered liquidity and nominal capital preservation, albeit often with lower returns.

A look at long-term historical annual returns reveals a consistent hierarchy: stocks generally lead, followed by bonds, with cash typically yielding the lowest returns. However, this generalized view becomes significantly more nuanced when adjusting for inflation. Real returns, which account for the erosion of purchasing power, demonstrate that while cash has generally managed to keep pace with inflation over the very long haul, it has rarely offered substantial growth beyond that. This critical distinction highlights one of the primary trade-offs: the perceived safety of cash often comes at the cost of significant opportunity.

The performance of these asset classes is far from static; it is deeply cyclical and influenced by prevailing economic conditions, particularly interest rate environments and inflation levels.

Supporting Data: Deciphering Returns Across Economic Eras

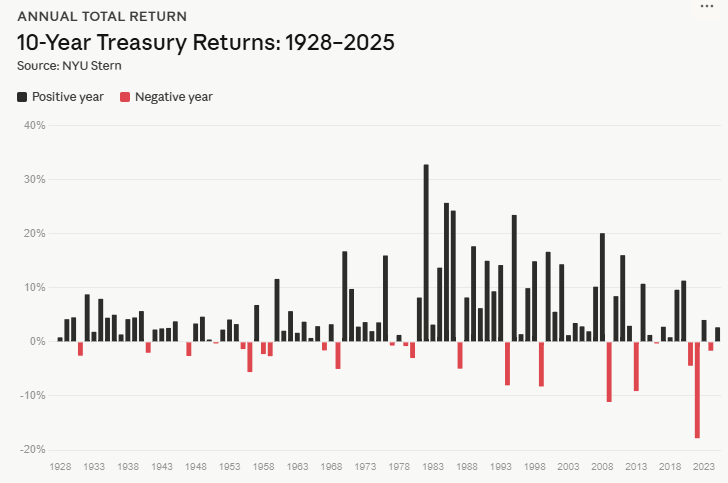

The core of the reader’s question lies in understanding the relative performance and risks of bonds versus cash. While bonds are generally considered fixed-income assets, positioning them closer to cash than stocks on the risk spectrum, they exhibit distinct characteristics. Bonds, especially longer-duration instruments, carry interest rate risk—their prices move inversely to interest rates. Cash, primarily short-term instruments like T-bills or high-yield savings accounts, is far less susceptible to interest rate fluctuations in terms of nominal value, as its yields adjust more rapidly to market rates.

Consider the stark contrast of 2022: a year marked by rapidly rising interest rates and persistent inflation. This environment proved particularly challenging for government bonds, with many experiencing significant negative returns. In stark contrast, short-term T-bills performed commendably, largely insulated from the interest rate sensitivity that plagued longer-duration bonds. This period highlighted a key advantage of cash: its immunity to interest rate risk on its nominal principal.

Further historical data underscores this difference:

- Bond Performance: Over a long historical span, bonds have exhibited periods of strong positive returns, often outpacing cash. However, they have also experienced a decent number of down years, meaning their nominal value could decrease. Data suggests a "win rate" (years with positive returns) for bonds around 80%.

- Cash Performance (T-bills): In contrast, short-term cash equivalents like T-bills have historically recorded virtually no down years in nominal terms. This unparalleled stability of principal is a cornerstone of their appeal for conservative allocations.

This difference in volatility and principal preservation is a primary driver behind the growing interest in a cash-heavy barbell portfolio. Investors, particularly those nearing or in early retirement, prioritize the certainty of nominal capital over the potentially higher, but more volatile, returns of bonds.

However, a closer look at specific periods reveals that the "cash is king" mantra isn’t universally true:

- Post-Global Financial Crisis (2008-2021): This era saw central banks, notably the Federal Reserve, maintain exceptionally low interest rates for an extended period. During this "cash was trash" phase, the average 3-month T-bill yield hovered around 0.55% annually, offering negligible returns and often failing to keep pace with even modest inflation. In the same timeframe, the 10-year Treasury bond yielded significantly better, appreciating by approximately 4% per year, demonstrating the opportunity cost of holding excessive cash during prolonged low-rate environments.

- Great Depression and World War II (1932-1954): This protracted period of "financial repression" saw ultra-low short-term interest rates. Cash underperformed bonds significantly and, with an average annual inflation rate of 2.7%, also lost real purchasing power. Here, longer-term bonds, despite lower yields by today’s standards, offered superior performance.

- High Inflationary Period (1966-1981): During this era of rampant inflation, cash emerged as the superior performer. Bonds, particularly longer-duration instruments, were "smoked" by rapidly rising interest rates and sky-high inflation, leading to substantial real and often nominal losses. Short-term rates, to which cash instruments are tied, adjusted more quickly to the inflationary environment, allowing cash to offer better protection against inflation compared to fixed-rate bonds whose yields were locked in at lower levels.

These historical snapshots illustrate a crucial point: the relative attractiveness of cash versus bonds is highly dependent on the prevailing economic regime. Rapidly rising interest rates tend to favor cash, while prolonged periods of low rates or stable, moderate inflation may favor bonds.

Official Responses: Expert Analysis on the Barbell Strategy

The barbell portfolio, in its essence, is an intentional divergence from traditional diversified portfolios that typically blend stocks and bonds across the risk spectrum. It’s a strategy that embraces extremes: a highly aggressive growth component (stocks) paired with an ultra-conservative, liquid component (cash). For a FIRE investor, this approach holds both allure and significant considerations.

The primary appeal for a FIRE candidate is the liquidity and stability offered by a large cash buffer. Two years’ worth of expenses in a high-yield savings account provides an unparalleled safety net against sequence of returns risk—the danger that poor investment returns early in retirement could prematurely deplete a portfolio. If a market downturn occurs, the investor can draw from their cash reserves, allowing their equity holdings time to recover without being forced to sell at a loss. This psychological comfort and practical flexibility can be invaluable for early retirees who face a potentially very long withdrawal period.

However, the "leaving money on the table" concern is valid. While cash provides nominal stability, it often sacrifices potential yield and inflation protection that bonds, particularly Treasury Inflation-Protected Securities (TIPS) or I-Bonds, can offer.

- Yield: Over the long term, bonds have generally offered higher yields than cash, meaning a greater return on the conservative portion of the portfolio. By foregoing bonds, an investor might miss out on this incremental return, which can compound significantly over decades.

- Inflation Protection: While cash has historically kept pace with inflation, its ability to outperform inflation consistently is limited. Certain types of bonds, like TIPS, are explicitly designed to protect against inflation by adjusting their principal value. Conventional bonds also offer a yield component that, in moderate inflationary environments, can provide a buffer.

- Diversification: Traditional bonds offer a negative or low correlation with stocks during downturns, providing a genuine diversification benefit. While cash offers a similar stability, bonds can still offer a return while providing that stability, whereas cash’s primary benefit is simply not losing nominal value.

The decision to choose cash over bonds is also influenced by interest rate expectations. If an investor anticipates a prolonged period of rising rates, or believes current bond yields are unattractive, then holding cash (which can be reinvested at higher short-term rates as they rise) might seem more prudent. Conversely, if rates are expected to fall, locking in higher bond yields now could be advantageous, as cash yields would likely decline.

The "risk-free" designation of cash, while common jargon, should be critically examined. While T-bills carry virtually no default risk from the U.S. government and minimal interest rate risk over their short duration, they are undeniably exposed to inflation risk. If inflation outpaces cash yields, the purchasing power of those reserves erodes. The author’s footnote correctly highlights that every investment carries some form of risk, and for cash, opportunity cost and inflation are significant considerations.

Implications: Crafting a Resilient FIRE Portfolio

For the FIRE practitioner, the choice between a bond allocation and an expanded cash buffer is not merely academic; it has profound implications for the sustainability and psychological resilience of their early retirement.

-

Mitigating Sequence of Returns Risk: A substantial cash buffer is an excellent antidote to sequence of returns risk, which is particularly acute for early retirees. Having 1-3 years of living expenses in cash allows an investor to avoid selling depreciated assets during market downturns, preserving their long-term growth potential. This strategy provides critical flexibility in withdrawal planning.

-

Psychological Comfort and Simplicity: For some investors, the clarity and simplicity of a barbell portfolio are highly appealing. Knowing that a significant portion of their funds is safe and readily accessible can reduce anxiety during market volatility, making them less likely to panic sell their equity holdings. The aversion to bonds, often stemming from complex mechanics or recent poor performance (like 2022), can be sidestepped.

-

Opportunity Cost and "Leaving Money on the Table": This is the central tension. By opting for cash over bonds, the investor is implicitly accepting a lower potential long-term return on that portion of their portfolio. Over decades, even a small difference in annual returns between cash and bonds can accumulate into a substantial sum. This opportunity cost must be weighed against the perceived benefits of cash’s stability.

-

Inflationary Environments: While cash can adjust quickly to rising rates during inflationary periods, its real returns often hover around zero. If long-term inflation averages higher than current cash yields, the purchasing power of the cash reserve will erode. For a retirement that could span 50+ years, this is a significant concern. Diversifying the "safe" allocation to include inflation-protected securities (like TIPS or I-Bonds) or even shorter-duration bond funds might offer better real returns without significantly compromising liquidity or stability.

-

Deflationary Environments: Bonds, particularly high-quality government bonds, tend to perform well during deflationary periods as their fixed coupon payments become more valuable in real terms and interest rates typically fall, increasing bond prices. Cash, while stable in nominal terms, may not offer the same capital appreciation benefits in a deflationary environment as bonds.

-

Personal Risk Tolerance and Preferences: Ultimately, the "best" asset allocation is deeply personal. The reader’s stated "not a big fan of bonds" indicates a preference that should not be ignored. If an investor is uncomfortable with an asset class, they are less likely to stick with it through challenging times, which is a greater risk than any theoretical underperformance.

In conclusion, the reader’s proposed barbell portfolio—aggressive equities balanced by a two-year cash buffer—is a defensible strategy, especially for FIRE aspirants prioritizing liquidity and sequence of returns risk mitigation. It offers significant psychological and practical advantages by simplifying the conservative allocation and providing a robust safety net. However, it is crucial to acknowledge the trade-offs: the potential for lower long-term returns on the conservative allocation, and the vulnerability to sustained periods of low interest rates or higher inflation where cash’s real returns may stagnate.

For an early retiree, a nuanced approach might involve a hybrid: maintaining a significant cash buffer for immediate needs (e.g., 1-2 years), and then allocating additional conservative funds to a mix of short-duration bonds, inflation-protected securities, or even a laddered certificate of deposit (CD) strategy to capture potentially higher yields while still managing interest rate risk. This allows for both robust liquidity and a degree of inflation protection and yield that pure cash might miss. The economy is cyclical, and so too will be the relative performance of fixed income assets. A thoughtful FIRE strategy adapts to these cycles, always balancing present needs with long-term aspirations.