The Great Decoupling: How a New Wave of Fintech Apps Ended Quicken’s Decades-Long Reign Over Personal Finance

For nearly four decades, Quicken was the undisputed titan of household bookkeeping. Launched in the mid-1980s as a basic desktop tool for balancing checkbooks, it grew into a comprehensive financial suite that defined personal wealth management for a generation.

Today, however, the landscape of personal finance looks vastly different. Legacy desktop applications—now rebranded as "Quicken Classic"—are increasingly viewed as relics of a bygone era. They have been eclipsed by agile, cloud-native, and AI-driven software-as-a-service (SaaS) applications. Many of these modern platforms allow consumers to manage every facet of their financial lives, often at a fraction of the cost or entirely for free.

As consumers demand real-time data syncs, mobile-first interfaces, collaborative tools for couples, and automated investment tracking, a highly competitive market of Quicken alternatives has emerged. This investigative report examines the top contenders reshaping the personal finance sector in 2026, tracking the industry’s evolution, the underlying technology, and the broader implications for consumer data privacy and financial literacy.

Chronology: The Evolution of Personal Finance Technology

The migration of consumers away from desktop-bound software to modern web-and-mobile suites did not happen overnight. It is the result of three distinct waves of technological disruption:

[1980s - 1990s] Desktop Era (Quicken, MS Money) -> Local storage, manual entry, floppy disks.

│

[2000s - 2010s] Cloud & Aggregation Era (Mint.com) -> Screen scraping, ad-supported free models.

│

[2020 - 2024] The Subscription Pivot & Mint's Demise -> Mandatory paid subscriptions, security upgrades.

│

[2025 - 2026+] AI-Powered & Collaborative Era (Monarch, Origin) -> Open banking, generative AI planning.1. The Desktop Era (1983–2005)

In the early days of personal computing, software like Quicken and Microsoft Money dominated. Data was stored locally on hard drives, transaction entry was largely manual, and updates were delivered via physical floppy disks or CD-ROMs. While secure from online threats, these programs required tedious maintenance and lacked real-time visibility.

2. The Cloud and Aggregation Era (2006–2019)

The launch of Mint.com in 2006 revolutionized the sector by introducing automated bank feeds using screen-scraping technology. Suddenly, consumers could aggregate data from multiple financial institutions automatically. Mint’s business model relied on selling financial products and advertising, making the software free to the end user. This forced Quicken to develop web-facing features, though its core architecture remained anchored to the desktop.

3. The Subscription Pivot and the Mint Fallout (2020–2024)

Faced with declining software sales, Quicken transitioned to a mandatory subscription model, requiring users to pay an annual fee to maintain automated bank feeds. Meanwhile, Intuit, which had acquired Mint in 2009, made the controversial decision to shut down the service in early 2024. This sudden closure left millions of users stranded, triggering a massive migration to alternative platforms and fueling a fintech development gold rush.

4. The Collaborative and AI Era (2025–2026)

Today, personal finance tools have evolved beyond passive tracking. The modern market is characterized by secure open-banking APIs (such as Plaid, Finicity, and MX) that have replaced fragile screen-scraping methods. Modern tools now feature predictive machine learning, generative AI financial advisors, estate planning integration, and dedicated collaborative portals for multi-partner households.

Supporting Data: Evaluating the Top Quicken Alternatives

To understand which platforms are successfully capturing Quicken’s former user base, we analyzed the performance, pricing, and feature sets of the market’s leading alternatives.

| Quicken Alternative | Best For | Price / Free Trial | Key Features |

|---|---|---|---|

| Monarch Money | Collaborative Budgeting | $8.33/mo (billed annually) 7-day free trial |

Flex Budgets, multi-user collaboration, automated categorization, investment tracking |

| Quicken Simplifi | Mobile-First Bill Tracking | $6.99/mo (billed annually) 30-day money-back guarantee |

Spending Plan, calendar bill views, investment monitoring, cash flow projection |

| Empower | Net Worth & Investment Tracking | Free | Fee analyzer, retirement planner, asset allocation tools, cash flow tracking |

| Origin | AI-Integrated Wealth Planning | $12.99/mo or $99/yr 7-day free trial |

AI-powered planning, tax preparation, basic estate planning, high-yield savings (4.52% APY) |

| Rocket Money | Expense & Subscription Optimization | Free version available Premium: $7 to $14/mo |

Subscription cancellation, bill negotiation, spending visualizations |

| YNAB (You Need A Budget) | Zero-Based Budgeting | $14.99/mo or $109/yr 34-day free trial |

Envelope budgeting methodology, goal tracking, active cash allocation |

| PocketSmith | Calendar Cash Flow Forecasting | Free (manual entry) Paid: $9.95 to $26.66/mo |

Auto-budgeting, calendar-based projections, multi-currency support |

| CountAbout | Legacy Data Migration | $9.99 to $39.99/yr 45-day free trial |

Direct Quicken/Mint data import, customizable categories, receipt attachment |

Deep Dive: Analysis of Leading Competitors

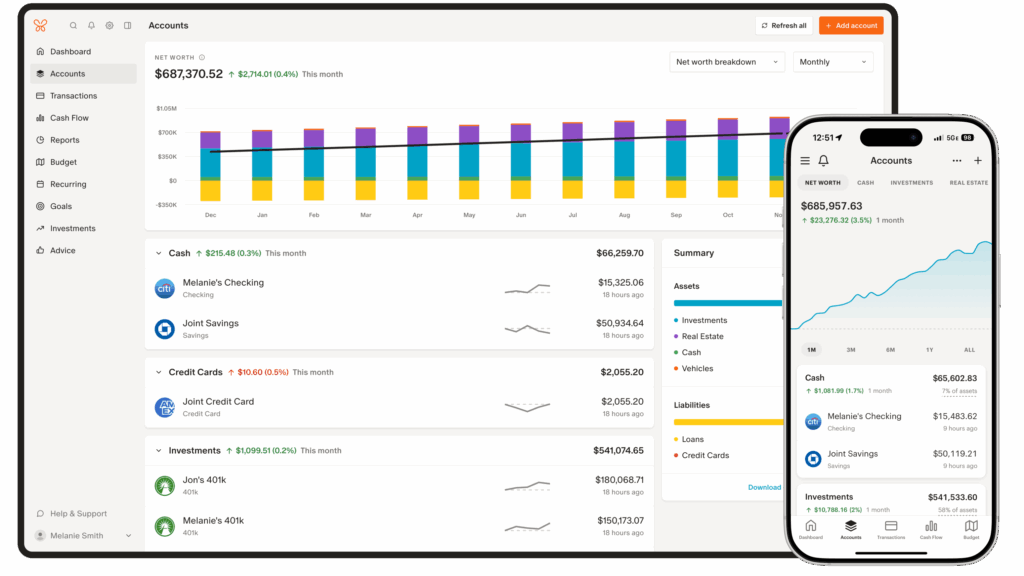

1. Monarch Money: The Premium Collaborative Standard

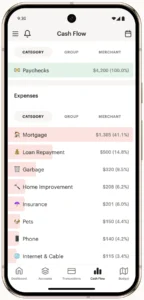

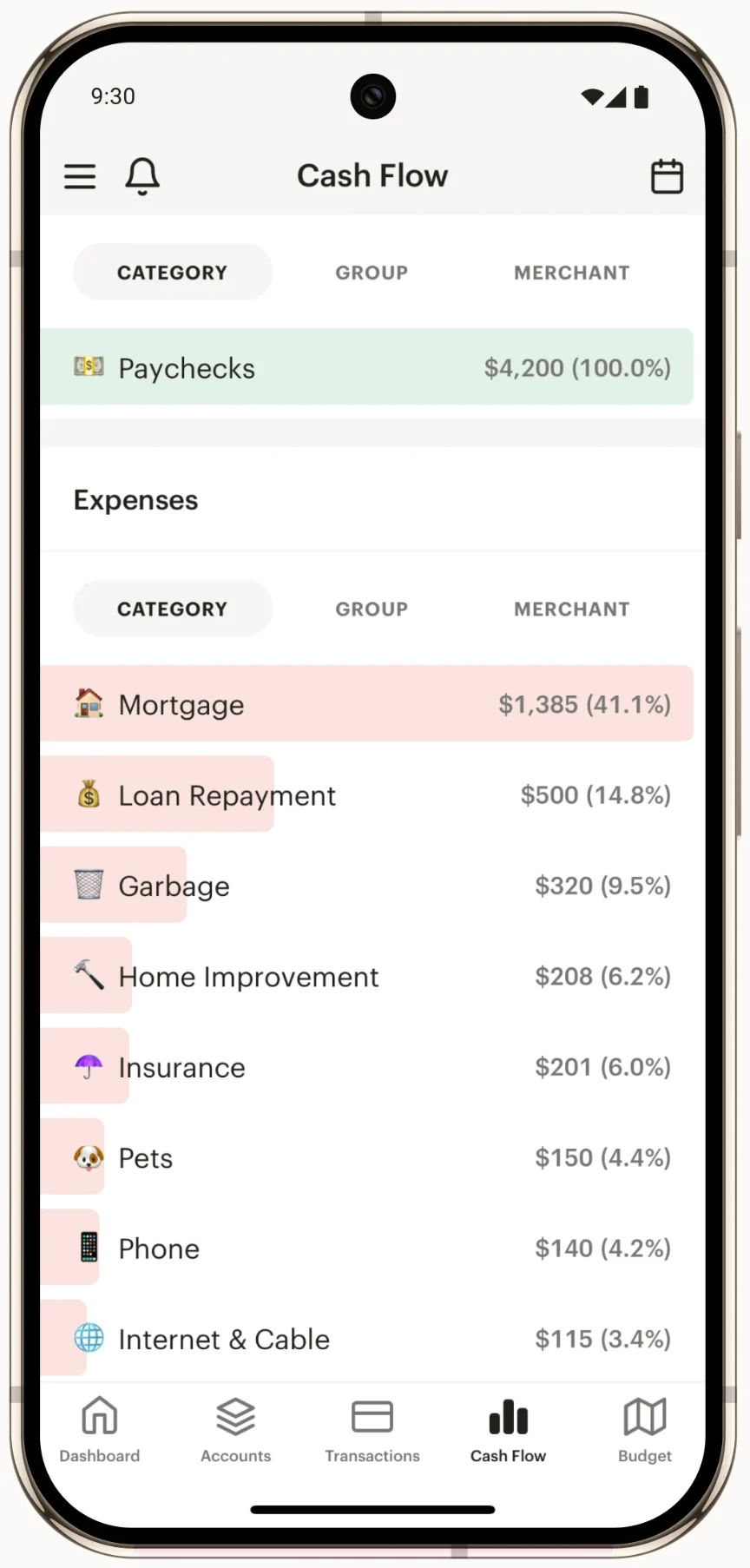

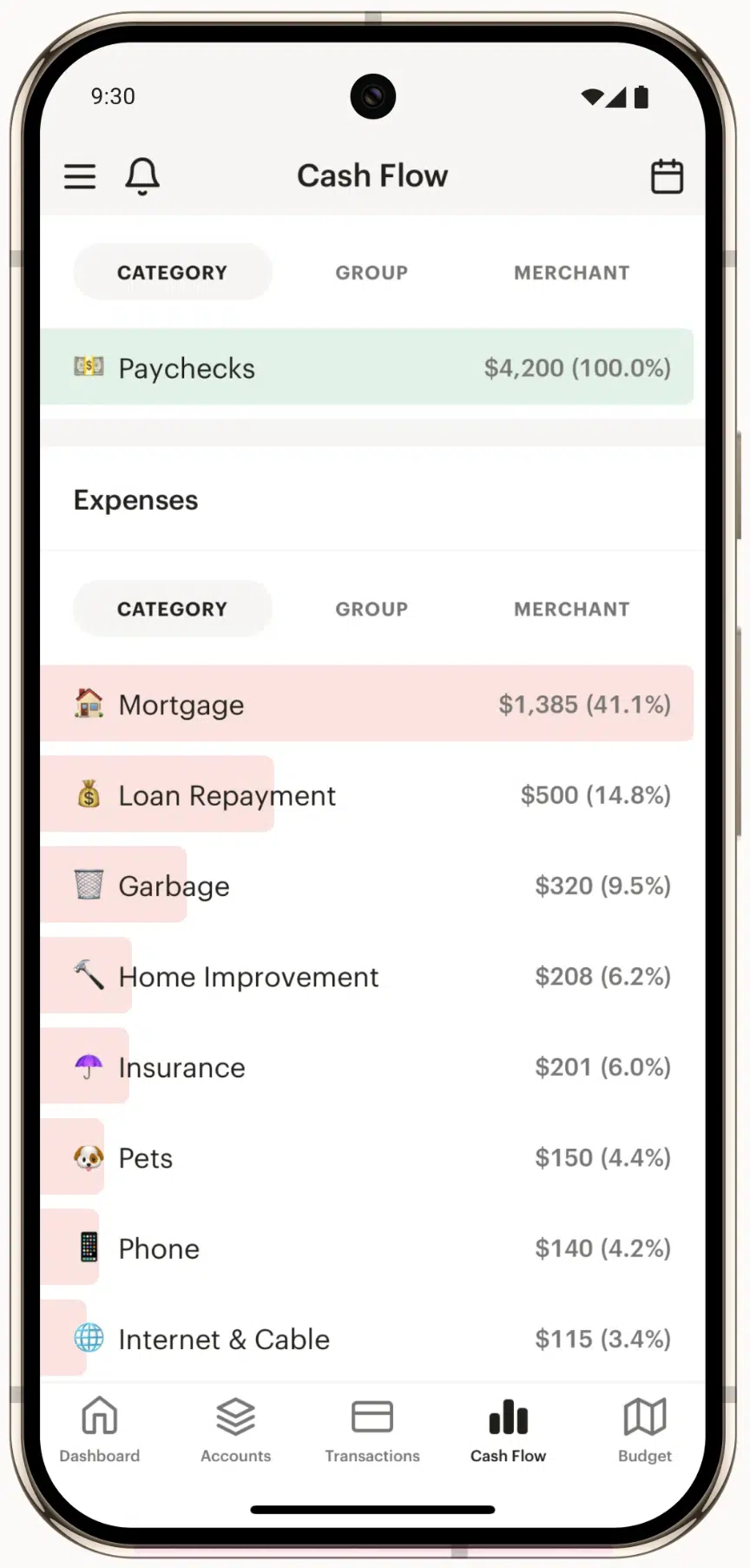

Monarch Money has emerged as one of the most popular premium alternatives to Quicken. Boasting an App Store rating of 4.9 (88,000+ reviews), the platform focuses heavily on clean user design and household collaboration.

- The Collaborative Edge: Unlike legacy platforms that require sharing login credentials, Monarch allows partners to create separate logins linked to a unified household dashboard. This approach respects individual access while providing a comprehensive view of joint finances.

- Feature Set: Monarch features "Flex Budgets," which adjust dynamically to fluctuating monthly expenses. It also offers advanced transaction rules, investment tracking, and an ad-free interface.

- The Cost: Priced at $8.33 per month (billed annually), it sits at the higher end of the market, though promotional offers frequently lower the barrier to entry (e.g., 50% off the first year with introductory codes like

ROB50).

Monarch Money Core Plan Cost Structure:

┌─────────────────────────────────────────────────────────┐

│ First Year Promo (with code): ~ $4.17 / month │

├─────────────────────────────────────────────────────────┤

│ Standard Annual Rate: $8.33 / month (billed yearly) │

└─────────────────────────────────────────────────────────┘2. Quicken Simplifi: Legacy’s Modern Counter-Attack

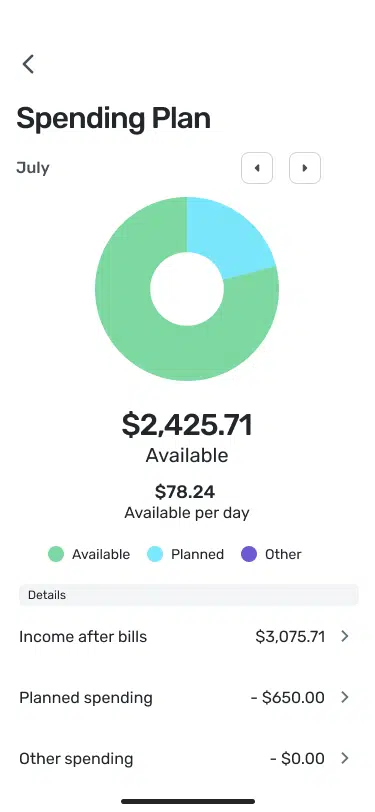

Recognizing that its desktop suite was losing ground, Quicken Inc. developed Simplifi. Built from the ground up as a mobile-first application, Simplifi balances affordability with Quicken’s historic strength in reporting.

- The Concept: Instead of traditional envelope budgeting, Simplifi utilizes a "Spending Plan" model. This calculates how much discretionary income remains after accounting for bills, savings goals, and scheduled contributions.

- Migration Friction: While robust, migrating historical data from Quicken Classic to Simplifi remains somewhat cumbersome, requiring users to export data to a CSV file, format it to Simplifi’s specifications, and upload it manually.

- The Cost: Simplifi is highly competitive, priced at $6.99 per month, with introductory rates often dropping to $3.49 per month for the first year, backed by a 30-day money-back guarantee.

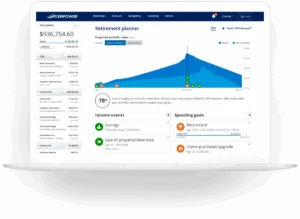

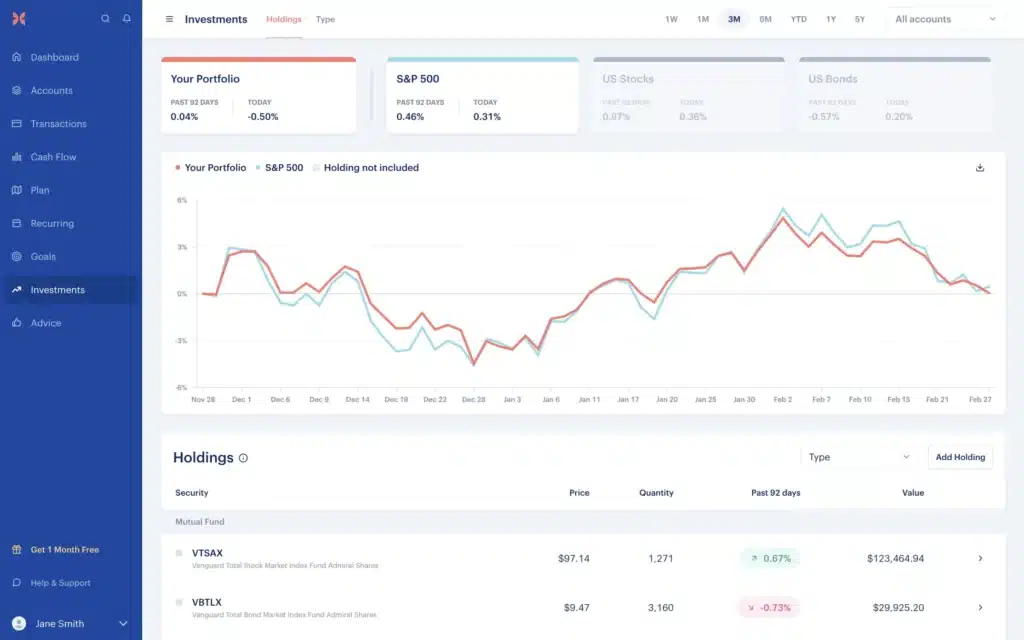

3. Empower: The Wealth-Tracking Heavyweight

For users who used Quicken primarily to monitor investment portfolios rather than track monthly grocery bills, the Empower Personal Dashboard (formerly Personal Capital) is the market’s leading free alternative.

- Investment Focus: Empower excels at analyzing investment accounts, tracking net worth, assessing asset allocation, and evaluating mutual fund fees via its proprietary Fee Analyzer.

- The Business Model: Empower offers its comprehensive dashboard entirely for free. The company monetizes the platform by offering personalized wealth management services to users with portfolios exceeding $100,000, though utilizing these advisors is entirely optional.

4. Origin: The AI-Powered Frontier

Origin represents the cutting edge of the 2026 fintech wave, integrating artificial intelligence throughout its platform to automate financial planning.

- Bundled Services: Origin positions itself as a comprehensive financial platform. Beyond budgeting, it provides automated tax preparation, basic will and trust creation, a built-in robo-advisor, and a high-yield savings account (yielding 4.52% APY as of late 2025).

- AI Financial Planning: The app’s integrated AI can draft custom strategies to help users build emergency funds, pay down debt, or plan for retirement based on their real-time transaction data.

5. YNAB: The Discipline Engine

For consumers focused strictly on debt reduction and strict budgeting, You Need A Budget (YNAB) remains a popular choice.

- Methodology: YNAB is built on zero-based budgeting principles, requiring users to "give every dollar a job." This approach is highly effective for breaking the paycheck-to-paycheck cycle, though it lacks the advanced investment tracking features found in Monarch or Empower.

Official Responses and Industry Perspectives

The rapid shift in consumer preferences has forced both legacy financial software companies and newer fintech startups to reevaluate their market positioning.

Quicken Inc.’s Dual-Track Strategy

In press statements regarding the coexistence of Quicken Classic and Quicken Simplifi, executives have emphasized a "dual-track" strategy. Quicken Classic continues to target "power users"—such as real estate investors, small business owners, and individuals who require complex tax scheduling or offline, local data storage. Meanwhile, Simplifi is positioned to capture younger, mobile-first users who prioritize automation and clean design over deep, granular spreadsheets.

The Shift Away from the "Free" Ad-Supported Model

Fintech executives have noted that the closure of Mint marked the end of the "free, ad-supported" personal finance era. Founders of subscription-based platforms like Monarch Money and YNAB argue that when a product is free, the user’s data becomes the product.

By charging a transparent subscription fee, these platforms commit to strict data privacy standards, promising never to sell user transaction history to third-party advertisers. This value proposition has resonated with consumers who are increasingly wary of data breaches and targeted financial advertising.

Fintech Business Models: A Comparison of Incentives

┌─────────────────────────────────────────────────────────┐

│ Legacy "Free" Model (e.g., Mint) │

│ - Revenue: Selling leads, credit card sign-ups, ads │

│ - Incentive: Maximize screen time and click-throughs │

├─────────────────────────────────────────────────────────┤

│ Modern "Paid" Model (e.g., Monarch, YNAB, Origin) │

│ - Revenue: Direct user subscriptions │

│ - Incentive: Maximize utility, data privacy, and UX │

└─────────────────────────────────────────────────────────┘Implications: The Future of Consumer Wealth Management

The transition from localized desktop software to connected cloud platforms has several long-term implications for consumer financial behavior and the broader economy.

1. The Open Banking Revolution and Security

The reliability of modern budgeting apps depends on secure bank connections. The industry’s transition to open banking standards via OAuth tokens represents a significant security upgrade. Instead of storing username and password credentials on third-party servers, apps now receive secure, read-only data tokens directly from financial institutions. This significantly reduces the risk of credential theft.

2. The Bundling of Wealth and Legal Services

As demonstrated by platforms like Origin, the boundaries of "personal finance apps" are expanding. What began as simple ledger tracking has evolved into full-suite financial planning. By bundling budgeting with estate planning (wills and trusts), tax preparation, and high-yield savings, fintech applications are challenging traditional local accounting and legal firms, democratizing access to complex financial planning tools.

3. AI-Driven Autonomy vs. Human Agency

As generative AI becomes more deeply integrated into these tools, the role of the user is shifting from active planner to passive supervisor. While AI-driven recommendations can help optimize cash flow and automate savings, industry analysts warn against over-reliance on automated financial planning. Consumer advocacy groups emphasize that while algorithms can provide excellent guidance, they cannot replace human judgment when navigating complex, emotional life events like estate planning, divorce, or purchasing a home.

Ultimately, the decline of Quicken’s monopoly has fostered a highly competitive, innovative ecosystem. Whether consumers choose the collaborative design of Monarch Money, the investment-centric dashboard of Empower, or the AI-integrated suite of Origin, they now enjoy unprecedented control over their financial futures.