The Unyielding Consumer: Navigating a Decade of Economic Turmoil with a Housing Hedge

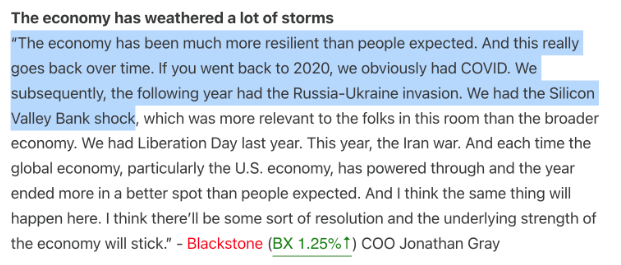

The 2020s have unfolded as a period of unprecedented economic turbulence, challenging households with a relentless barrage of financial hurdles. From a global pandemic that shattered supply chains to geopolitical conflicts fueling energy crises, and an inflationary surge not seen in four decades, the economic landscape has been fraught with peril. Yet, amidst this storm, a remarkable paradox persists: the American consumer continues to spend, demonstrating an unexpected resilience that has defied numerous recession forecasts and kept the economy afloat.

This sustained consumer strength, a cornerstone of the current economic narrative, can be largely attributed to a unique phenomenon: the "housing hedge." A significant portion of homeowners, having secured historically low mortgage rates prior to 2022, have effectively insulated themselves from the escalating costs of living, channeling their savings from housing expenses into other areas of the economy. This dynamic has created a bifurcated economic experience, where those with locked-in housing costs enjoy a substantial financial advantage, while new entrants face prohibitive barriers.

A Decade Defined by Economic Upheaval

The journey through the 2020s has been anything but smooth. Economically speaking, households have been forced to navigate a series of interconnected crises, each leaving its mark on prices and purchasing power.

The Pandemic’s Initial Shock and Unprecedented Response

The decade began with the sudden and severe onset of the COVID-19 pandemic. Lockdowns and health concerns brought global economic activity to a grinding halt, causing widespread business closures, mass layoffs, and severe disruptions to supply chains. Factories idled, ports jammed, and the intricate web of global commerce frayed. In response, governments worldwide, including the United States, unleashed an "unthinkable amount" of fiscal and monetary stimulus. The aim was clear: to prevent a complete economic collapse and keep individuals and businesses solvent. Programs like the CARES Act, the Paycheck Protection Program (PPP), and expanded unemployment benefits injected trillions of dollars directly into the economy. Simultaneously, central banks, most notably the Federal Reserve, slashed interest rates to near-zero and engaged in massive quantitative easing, pumping liquidity into financial markets. While these measures averted a deeper catastrophe, they laid the groundwork for future challenges.

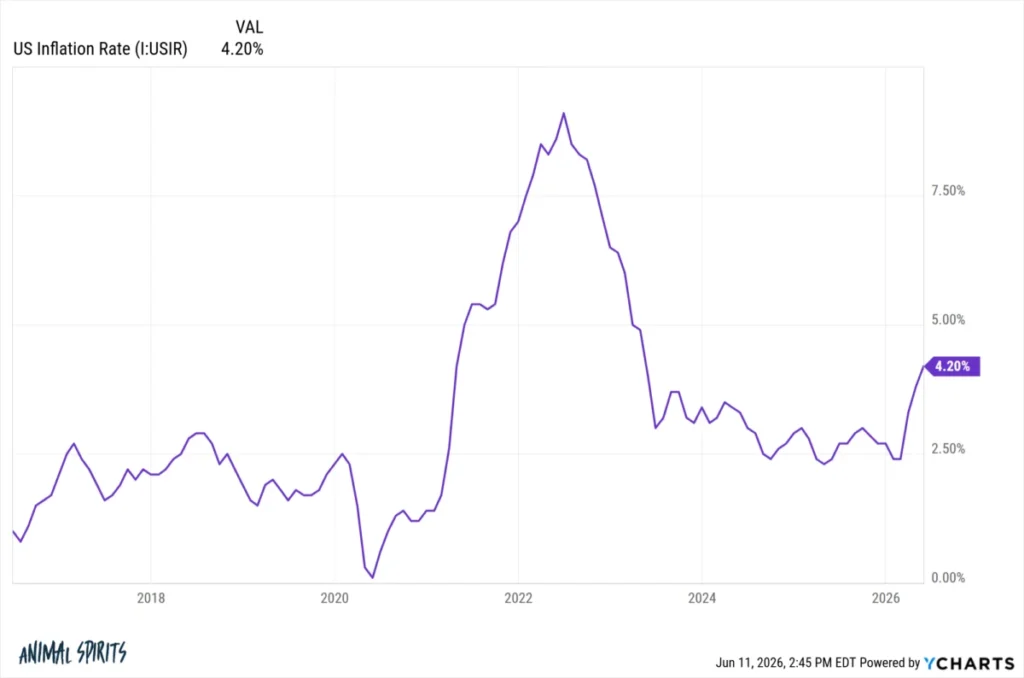

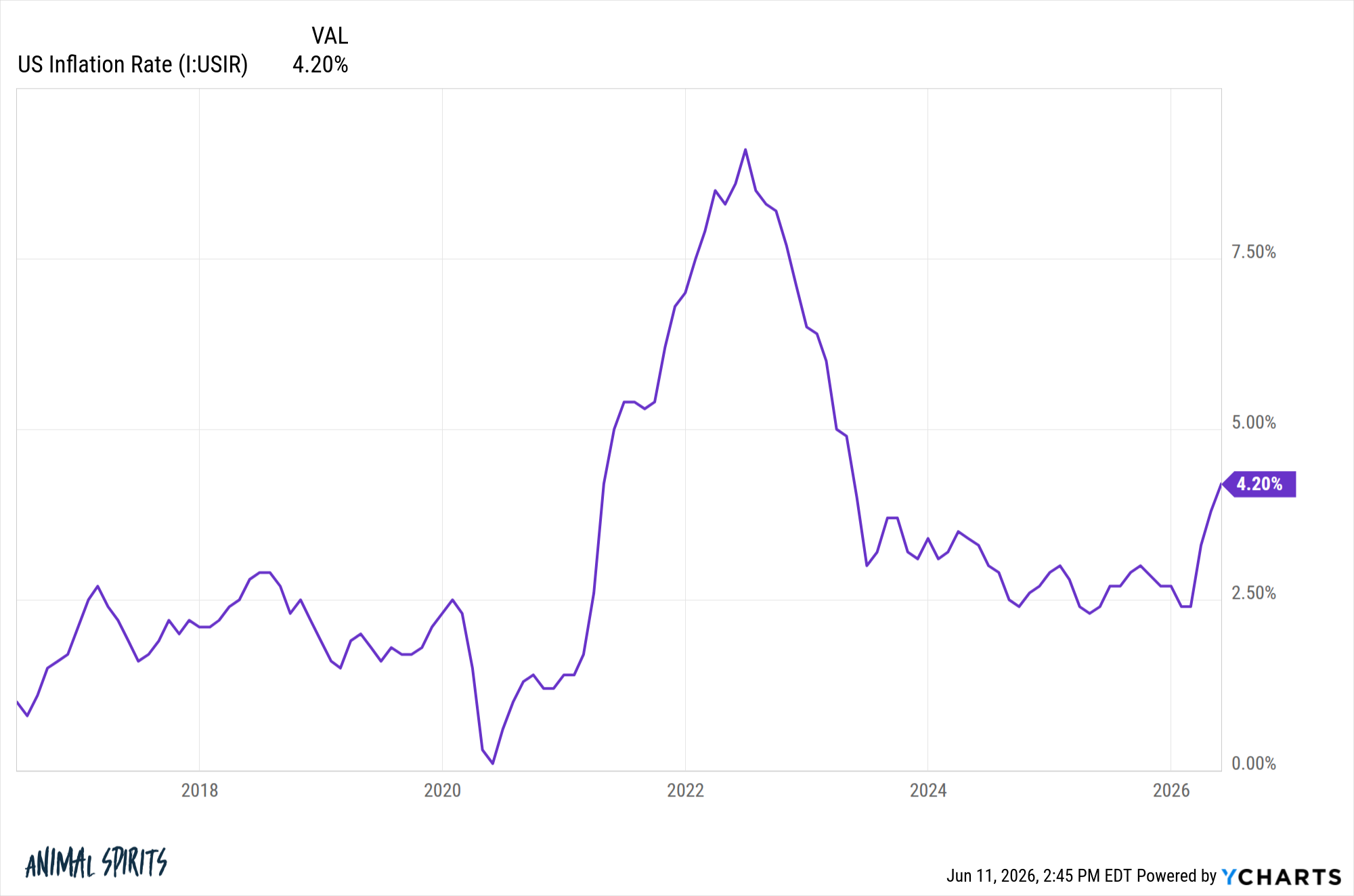

The Inflationary Spiral: A Four-Decade High

The combination of surging demand (fueled by stimulus and pent-up consumer desire post-lockdown) and constrained supply (due to persistent supply chain issues, labor shortages, and manufacturing bottlenecks) created the perfect storm for inflation. By the mid-2020s, the consumer price index (CPI) began to climb rapidly, reaching levels not witnessed in over four decades. From everyday groceries and consumer goods to durable items and services, prices soared, eroding purchasing power and sparking widespread concern among policymakers and the public alike. The initial narrative that inflation would be "transitory" proved incorrect, forcing central banks to pivot aggressively.

Geopolitical Shocks and Energy Market Volatility

Just as economies were grappling with post-pandemic recovery and inflation, new geopolitical crises emerged to compound the challenges. The Russia-Ukraine war, which began in early 2022, sent shockwaves through global commodity markets. Russia, a major exporter of oil, natural gas, and various raw materials, saw its supplies disrupted and sanctions imposed, leading to an immediate and dramatic surge in energy prices. Gas prices "shot through the roof," impacting transportation costs for businesses and households, and feeding into broader inflationary pressures.

Beyond the Russia-Ukraine conflict, other geopolitical tensions have also played a role. Last year, households contended with the economic impact of various tariffs, which, while aimed at protecting domestic industries or addressing trade imbalances, often resulted in higher import costs that were ultimately passed on to consumers. Furthermore, the specter of conflict, such as the "Iran war this year" referenced in the original analysis, has repeatedly threatened to send gas prices "shooting higher yet again," underscoring the fragility of global energy markets and their susceptibility to geopolitical events.

The Cumulative Toll: A Steep Rise in Living Costs

The cumulative effect of these myriad factors has been profound. According to the analysis, prices are now roughly 30% higher than they were at the beginning of the decade. To put this into perspective, this increase already surpasses the total price hike for the entire 2010s, which stood at around 19%. This stark comparison highlights the accelerated erosion of purchasing power experienced by households in just a few years, making it significantly more expensive to maintain the same standard of living.

Supporting Data: The Enduring Strength of the Consumer

Despite the daunting economic headwinds and the significant rise in prices, the most striking aspect of the 2020s economy has been the remarkable resilience of consumer spending. Far from retreating into austerity, consumers have largely continued to open their wallets, a phenomenon that has baffled many economists and policymakers.

Unwavering Spending Habits

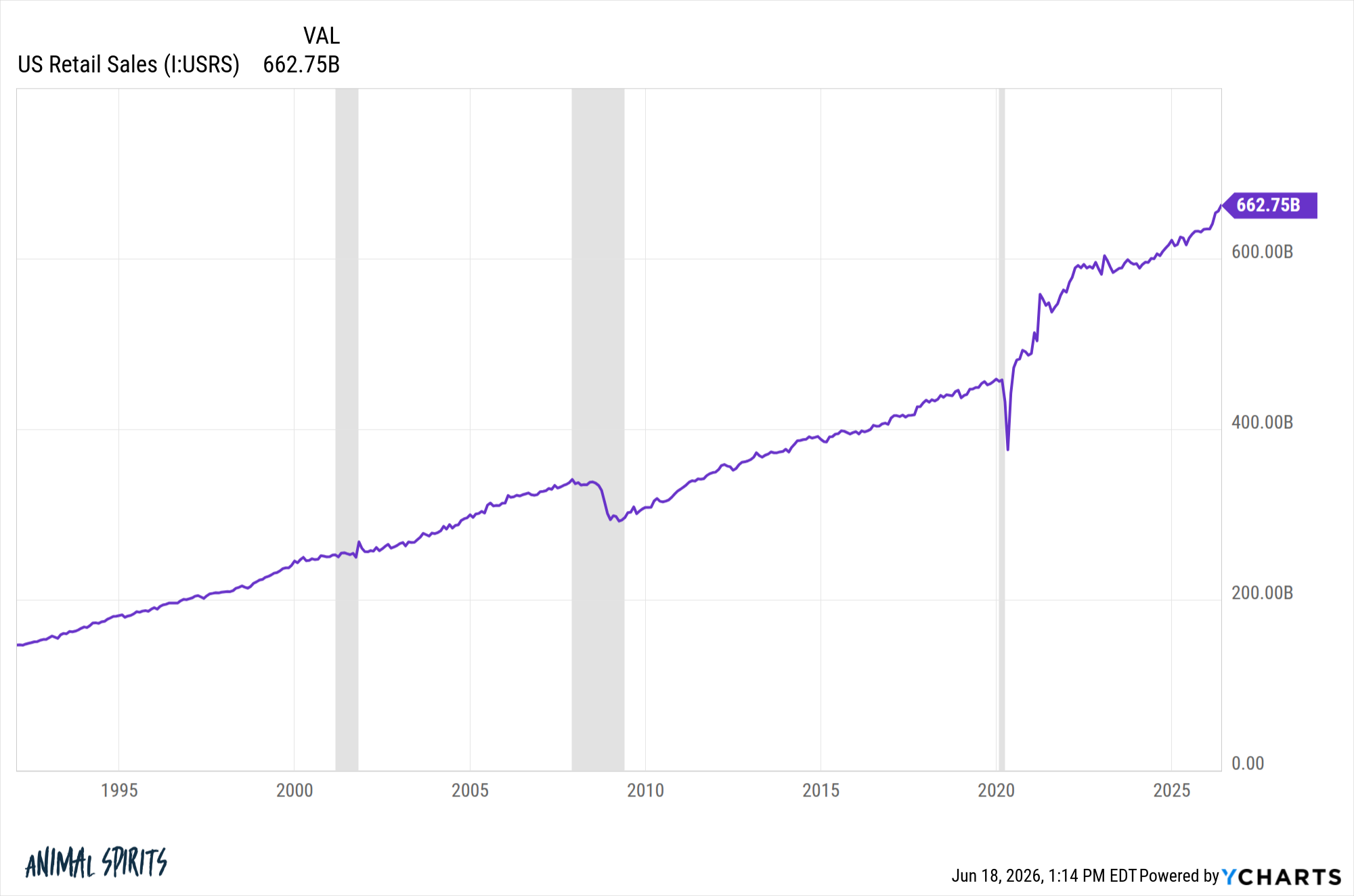

Data consistently indicates that "people continue spending money." This persistent consumer demand has been a key factor preventing a broader economic downturn. Whether it’s discretionary purchases, travel, dining out, or essential goods, the aggregate spending figures have remained robust. This trend is visually supported by charts depicting consumer spending, which show a consistent upward trajectory even in the face of inflationary pressures. The absence of a widespread recession, despite numerous forecasts predicting one, stands as a testament to this underlying strength. Many analysts had anticipated a significant pullback in spending as inflation bit into household budgets, yet this widespread contraction has largely failed to materialize beyond minor, temporary dips.

Corporate Confidence in Consumer Vigor

The strength of the consumer is not merely an abstract economic statistic; it is a sentiment echoed at the highest levels of corporate America. CEOs across various sectors have consistently reported strong consumer demand, often expressing surprise at the sustained vigor. As noted by sources like The Transcript, corporate leaders frequently highlight the "strong consumer" as a positive driver in their earnings calls and investor presentations. This anecdotal evidence from the front lines of commerce provides a qualitative confirmation of the quantitative data, indicating that businesses are experiencing firsthand the continued willingness of consumers to spend.

The Wealth Effect: Fueling Discretionary Spending

One significant contributor to this sustained spending is the "wealth effect." Financial assets, including stock market portfolios and housing equity, have seen substantial appreciation throughout the decade. As the value of their investments and homes rises, individuals tend to feel wealthier and more confident about their financial future. This psychological boost often translates into a greater propensity to spend, even on discretionary items, as households perceive themselves as having more disposable wealth. For many, the gains in their investment portfolios have helped offset the increased cost of living, providing a buffer that allows for continued consumption.

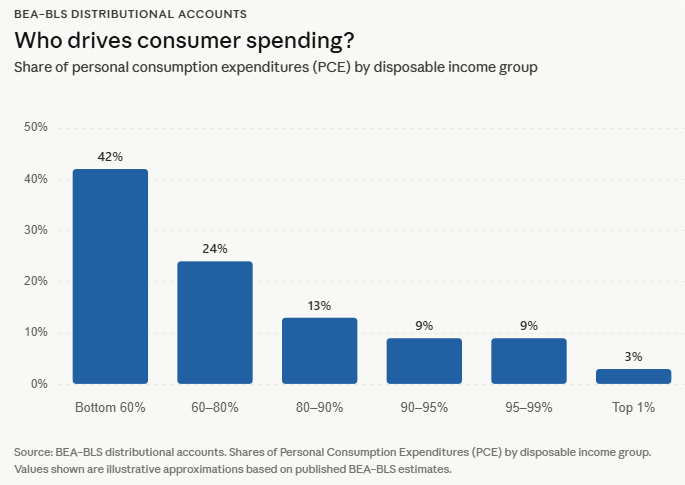

Nuancing the "K-shaped Economy" Narrative

While there has been considerable discussion about a "K-shaped economy"—a scenario where some segments of the population thrive while others struggle—data from the Bureau of Economic Analysis (BEA) suggests that consumer spending patterns are not as uneven as the media narrative often portrays. While wealth accumulation certainly has K-shaped characteristics, the distribution of spending across income groups appears to be more broadly distributed than commonly believed. This indicates that while higher-income households might have seen greater asset appreciation, spending has remained relatively broad-based, contributing to overall economic stability. This nuance is crucial, as it challenges the perception of a deeply divided consumer landscape in terms of day-to-day economic activity.

The Housing Hedge: An Unseen Economic Anchor

The most compelling explanation for the American consumer’s resilience, and indeed for the economy’s unexpected fortitude, lies in the "housing hedge" enjoyed by a large segment of the population. This phenomenon has effectively shielded many households from the worst impacts of inflation, freeing up capital for other forms of consumption and investment.

The Golden Window of Opportunity (2020-2021)

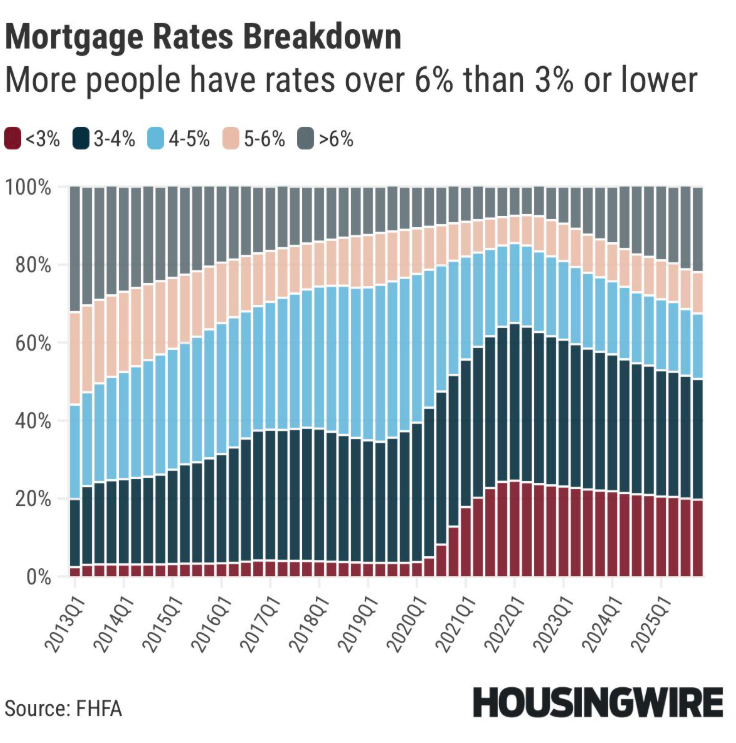

At the onset of the 2020s, specifically around 2020, the homeownership rate in the U.S. stood at approximately 65%, a level largely maintained to this day. Crucially, at that time, housing prices were significantly more affordable than they are now, and 30-year fixed-rate mortgage rates hovered around a historically low 3%. This period presented an unprecedented opportunity for both existing homeowners to refinance and for new buyers to enter the market with incredibly favorable borrowing terms.

Those who purchased or refinanced their homes before 2022, locking in these "ridiculously low mortgage rates," inadvertently secured "the inflation hedge of the century." Housing costs, typically the largest budget item for most households, became fixed at a historically low level. This meant that while the cost of groceries, gas, and other goods soared, a significant portion of their monthly expenditures remained stable and predictable.

Inflation’s Silver Lining for Fixed-Rate Mortgages

The current inflationary environment, with the inflation rate once again climbing above 4% (due to a resilient economy and ongoing geopolitical factors), further highlights the immense advantage held by these homeowners. For someone with a 3% mortgage, the real (inflation-adjusted) cost of borrowing is effectively zero, or even negative. In essence, they are "borrowing for free" in real terms, as the value of their fixed payments diminishes relative to the general increase in prices. This translates into substantial savings each month compared to what they would be paying if their mortgage rate adjusted with inflation or if they had to secure a new mortgage today.

The Depth of the Housing Hedge

The data underscores the widespread nature of this advantage. Approximately half of all borrowers currently hold mortgage rates of 4% or lower. This means a vast segment of the mortgaged homeowner population is benefiting from this inflation hedge. Furthermore, the situation is even more advantageous for the roughly 40% of homeowners who own their homes "free and clear," meaning they have no mortgage payments whatsoever. When these two groups are combined, it becomes clear that a substantial majority of American households are either free from housing debt or have significantly reduced housing costs compared to current market rates.

Economic Ripple Effects: Fueling the Broader Economy

The money saved on housing payments does not simply disappear; it is redirected into other areas of the economy. This surplus capital allows households to maintain strong spending levels on consumer goods and services, directly contributing to robust retail sales figures. It also enables many to continue investing, with "flows continuing to go into the stock market," further bolstering financial assets and the wealth effect. This sustained flow of capital, insulated from inflationary pressures by the housing hedge, is a critical, yet often underappreciated, factor explaining why many economic forecasts, particularly those predicting a recession, have been consistently proven wrong throughout this decade. The ability of so many people to effectively "hedge their biggest budget item" has provided a powerful and durable economic stimulus.

Official Responses and Policy Dilemmas

The remarkable economic resilience, particularly the role of the housing market, has presented policymakers with a complex set of challenges and opportunities.

Central Bank’s Battle Against Inflation

The Federal Reserve, initially slow to react to rising inflation, embarked on an aggressive campaign of interest rate hikes starting in 2022. The goal was to cool down an overheating economy, curb demand, and bring inflation back to its 2% target. While these rate hikes have had a significant impact on borrowing costs for new loans – particularly mortgages – they have had a more muted effect on the large segment of homeowners with locked-in low rates. This creates a policy dilemma: the Fed’s tools primarily impact new economic activity and borrowing, leaving a substantial portion of the economy relatively insulated, thereby prolonging inflationary pressures in some sectors and making a "soft landing" more challenging to achieve. The central bank continues to grapple with the balance between taming inflation and avoiding a severe recession, with each interest rate decision scrutinized for its potential impact on consumer behavior and economic growth.

Government Fiscal Policy and Long-Term Stability

Beyond monetary policy, government fiscal policy has also been a subject of intense debate. The initial pandemic-era stimulus, while effective in preventing a collapse, contributed to the inflationary pressures. Subsequent legislative efforts have focused on targeted investments, such as infrastructure bills, which aim to boost long-term productivity and employment. However, ongoing deficit spending and the national debt remain significant concerns, with policymakers weighing the need for continued economic support against the imperative of fiscal responsibility. The housing market’s dynamics, with its embedded "hedge," add another layer of complexity to these fiscal considerations, as it influences wealth distribution and the overall economic capacity of different demographic groups.

Addressing Housing Market Disparities

The widening gap between existing homeowners and aspiring buyers has also drawn attention. While there haven’t been explicit "official responses" to the housing hedge itself, policymakers are increasingly discussing strategies to address housing affordability and supply shortages. Initiatives aimed at increasing housing construction, streamlining zoning regulations, and providing assistance to first-time homebuyers are being considered to alleviate the pressures on those who haven’t benefited from the low-rate environment. However, these are complex, long-term challenges with no easy solutions.

Implications: An Uneven Future and Persistent Questions

The unique economic dynamics of the 2020s, particularly the powerful housing hedge, carry significant implications for the future of the American economy and society. While it has underpinned current resilience, it also points to potential vulnerabilities and widening disparities.

When Does the Hedge Begin to Fade?

The central question looming over this narrative is: "when does this hedge begin to fade?" The longevity of this advantage is critical for the sustained strength of consumer spending. While existing homeowners will retain their low rates as long as they stay in their homes, factors like increasing property taxes, rising insurance costs, and the eventual need to move or downsize could gradually erode the benefit. Mike Simonsen’s analysis, from the perspective of housing activity, suggests that this hedge could persist "for a while," indicating that a significant portion of homeowners will continue to benefit from their low rates for years to come, especially given the current disincentive to sell and forfeit a sub-4% mortgage. This structural entrenchment of low housing costs for many homeowners suggests that the economic effects could be long-lasting.

The Real K-Shaped Economy: The Housing Market Divide

While overall spending might not be as K-shaped as some believe, the housing market itself presents a starkly divided reality. This is arguably "the real K-shaped part of the economy." On one side are the "haves": individuals who owned a home before 2022, locked in low mortgage rates, and have seen their home equity soar. They are insulated from current housing costs and benefit from the inflation hedge. On the other side are the "have-nots": aspiring homeowners, first-time buyers, and young families who are now confronted with a brutal market characterized by significantly higher prices, elevated mortgage rates (often more than double the pandemic lows), and severely limited housing supply.

This disparity creates profound challenges. For those unable to enter the market, wealth accumulation through homeownership—historically a primary driver of middle-class prosperity—becomes increasingly out of reach. This widens the intergenerational wealth gap and exacerbates social inequalities, creating a deeply uneven playing field for economic advancement.

Historical Context and the Prospect of Future Shocks

The history of the housing market in the 21st century serves as a cautionary tale against complacency. The 2000s began with a housing bubble that subsequently burst, leading to one of the biggest housing crashes in history. Prices were "extremely affordable" throughout the 2010s, allowing for a period of recovery and accessibility. Then, the pandemic triggered an "enormous amount of demand and price growth," leading to the current situation. This cyclical volatility underscores that the housing market is susceptible to external shocks, whether they be economic downturns, changes in monetary policy, or unforeseen global events, which could once again alter its trajectory.

The current situation, where "timing and luck" have played such a pivotal role in determining a household’s financial standing, highlights the precarious nature of economic advantage. While many households "lucked into lower prices and mortgage rates," securing a "hedge of a lifetime," others "haven’t been so lucky." They must now contend with a market designed to challenge their aspirations, facing lower supply, higher borrowing rates, and much higher prices.

Ultimately, the American economy of the 2020s is a testament to both resilience and disparity. The robust consumer spending, fueled significantly by the housing hedge, has kept recession at bay. However, this strength masks an underlying tension, as the benefits of this hedge are unevenly distributed, creating a distinct and challenging environment for those on the outside looking in. The ongoing question remains how long this unique economic dynamic can sustain growth, and what the long-term implications will be for economic equality and stability in the years to come.