The Unprecedented Ascent of Equities: A New Era of Financial Dominance

Posted July 14, 2026, by Ben Carlson

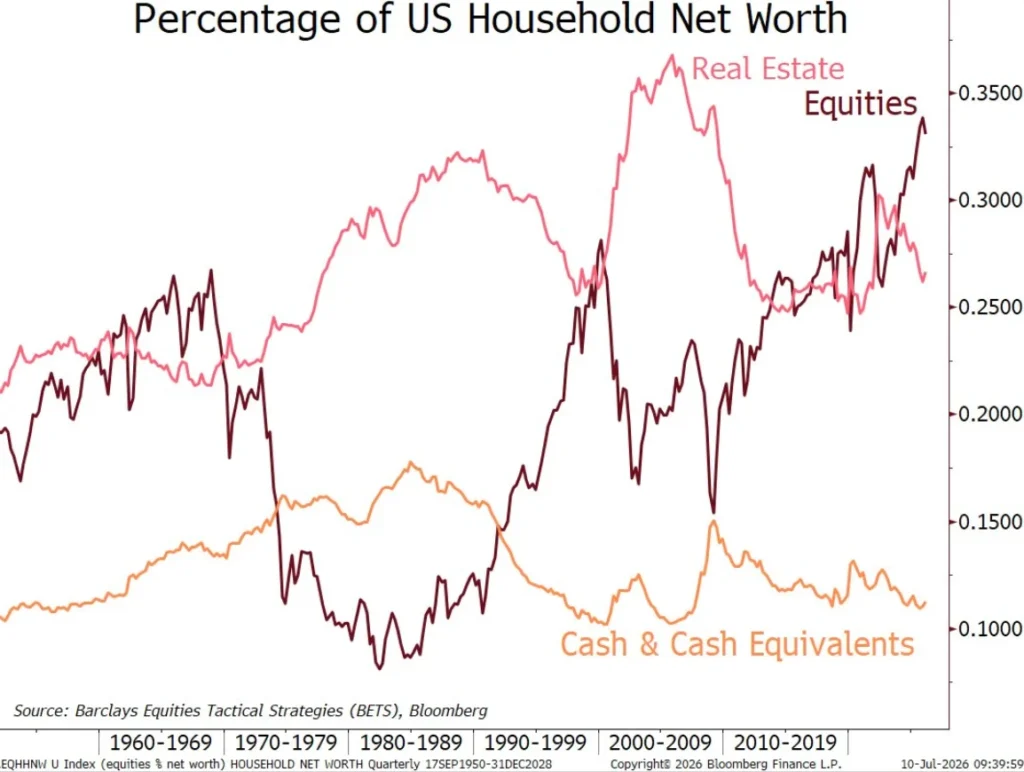

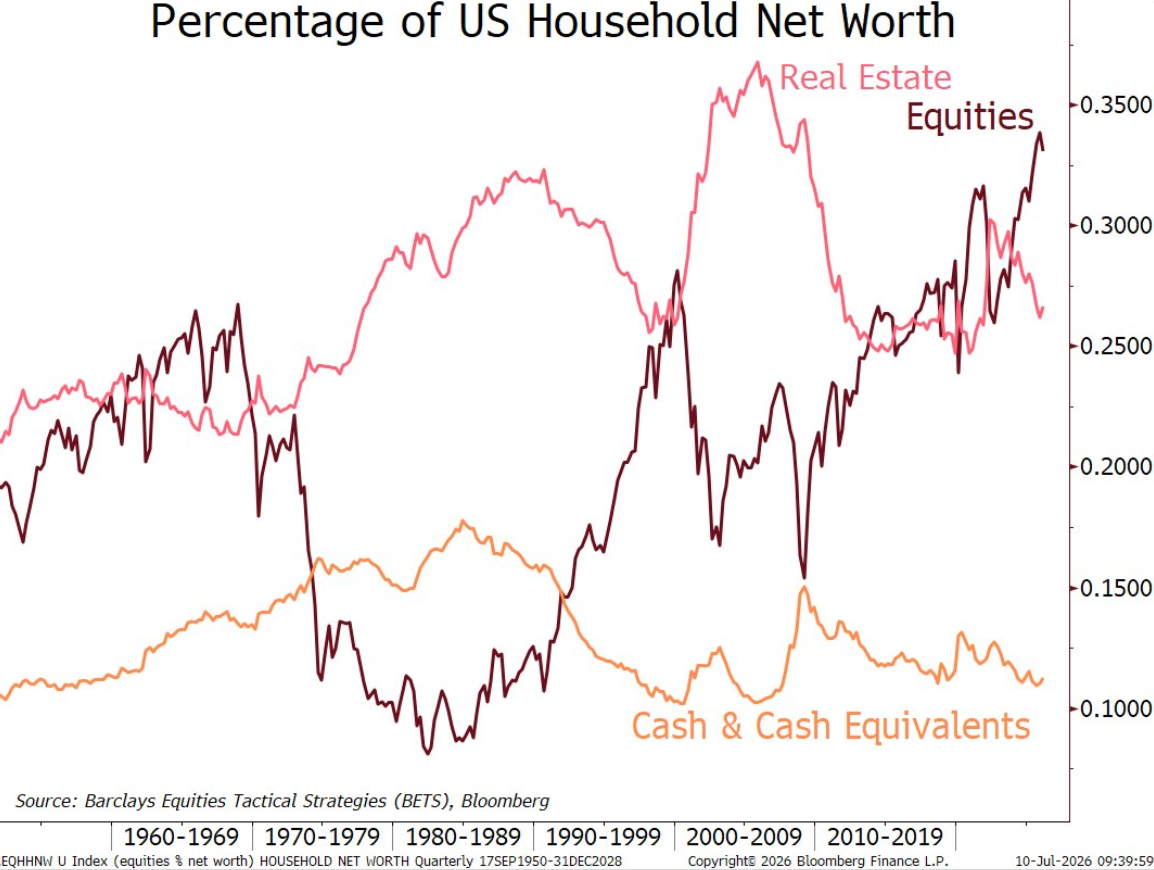

The landscape of household financial allocations has undergone a profound and arguably irreversible transformation. What was once a diversified portfolio across various asset classes now starkly highlights the overwhelming dominance of equities, particularly in the United States. This monumental shift, vividly illustrated by recent data, presents both a testament to the stock market’s enduring appeal and a potential harbinger of a new, more volatile financial order.

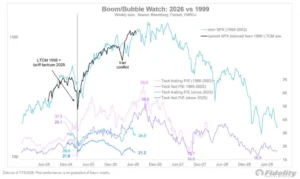

Financial analyst Joe Weisenthal recently highlighted an illuminating chart detailing household allocations to various financial assets over time. This visual, a veritable Rorschach test for market observers, clearly depicts a cyclical history of booms and busts, leaders and laggards among asset classes. However, the current period stands out with equities taking a commanding lead by an unprecedented margin. This development sparks a critical debate: does this widespread equity dominance signal an overvalued market ripe for a correction, or does it represent a fundamental, "new normal" in the structure of global finance?

This article delves into the historical evolution of household stock ownership, examines the underlying factors contributing to the current equity supremacy, explores the contentious question of central bank intervention, and analyzes the far-reaching implications of a financial system where the stock market increasingly holds the reins.

A Historical Perspective: From Scarcity to Ubiquity

The journey of the U.S. household from a largely passive observer to an active participant in the stock market is a compelling narrative of evolving economic conditions, regulatory changes, and technological innovation. For much of the 20th century, direct stock ownership was a privilege largely reserved for the affluent, the well-connected, or the institutionally mandated.

The Pre-Modern Era: Barriers and Bear Markets

In the early to mid-20th century, particularly in the pre-World War II era, the majority of American households were significantly underinvested in stocks. Several factors contributed to this phenomenon:

- Lack of Disposable Income: Economic realities for many families left little room for discretionary savings, let alone investment in complex financial instruments.

- High Barriers to Entry: Minimum investment requirements were substantial, and brokerage commissions were exorbitant, making stock market participation inaccessible for the average person.

- Limited Financial Knowledge: The intricacies of the stock market were largely opaque to the public, and widespread financial education was virtually non-existent.

- The Shadow of the Great Depression: The traumatic market crash of 1929 and the ensuing decade of economic hardship left an indelible mark on an entire generation of investors. As renowned financial historian Peter Bernstein recounted in a 1990s interview with PBS, those who survived the 1929 crisis were "terribly conservative" in their approach to money management. He noted strict legal limitations, with personal trusts in New York restricted to a mere 35% allocation to common stocks, and some state pension funds mandated to hold zero equities. This pervasive risk aversion, born from lived experience, significantly shaped investment habits and regulatory frameworks for decades.

Beyond direct ownership, pensions played a more prominent role in retirement savings. Defined benefit plans, promising a fixed income stream in retirement, were common. While these plans provided a sense of security for individuals, the plans themselves were often conservative investors, acting more like bond funds for beneficiaries rather than aggressive equity vehicles. The institutional investment landscape was far from the equity-heavy portfolios seen today.

The Democratization of Investing: IRAs, 401ks, and the Digital Age

The latter half of the 20th century ushered in a gradual but decisive shift. The introduction of Individual Retirement Accounts (IRAs) in 1974 and 401(k) plans in the early 1980s marked a pivotal moment. These defined contribution plans slowly began to supplant traditional defined benefit pensions, shifting the onus of investment decision-making and risk directly onto individuals. These vehicles provided tax incentives for saving and investing, thereby expanding the pool of potential stock market participants.

The true acceleration of retail investor involvement, however, came with the advent of the internet and subsequent technological innovations:

- Online Trading Platforms: The late 1990s and early 2000s saw the rise of online brokerages, making it easier and faster for individuals to execute trades from their homes.

- Zero-Dollar Commissions: The elimination of trading commissions by major brokerages in the mid-2010s removed a significant cost barrier, encouraging more frequent trading and smaller investment amounts.

- Robo-Advisors and Target-Date Funds: These automated investment services simplified portfolio construction and management, making sophisticated diversification strategies accessible to even novice investors. Target-date funds, in particular, offered a "set it and forget it" solution that automatically adjusted asset allocations over time.

- Gamified Investing Platforms (e.g., Robinhood): More recently, mobile-first platforms have made investing highly accessible, often leveraging user-friendly interfaces and even social elements, further lowering the psychological barrier to entry.

This confluence of factors has not only broadened access to the stock market but has also normalized its presence in everyday financial life. "Everything is a financial market now," as the original article posits, underscoring how deeply interwoven equity investments have become with personal finance.

The Unprecedented Scale of U.S. Equity Dominance

The current prominence of the stock market, particularly the U.S. market, is staggering. While the United States accounts for approximately 4% of the world’s population and roughly 25% of global GDP, it commands an astonishing 65% of the world’s total stock market capitalization. This disproportionate influence is not merely a statistical anomaly but a reflection of several deep-seated structural advantages:

- Innovation Hub: The U.S. has consistently fostered an environment of technological innovation and entrepreneurship, leading to the growth of globally dominant companies in sectors like technology, biotechnology, and consumer goods.

- Robust Capital Markets: The depth, liquidity, and regulatory transparency of U.S. capital markets are unparalleled, attracting both domestic and international investors.

- Reserve Currency Status: The U.S. dollar’s role as the world’s primary reserve currency underpins confidence in U.S. assets, including equities.

- Strong Corporate Governance: While imperfect, the U.S. legal and regulatory framework for corporate governance generally provides strong protections for shareholders, further enhancing investor trust.

This confluence of factors has created a self-reinforcing cycle, drawing immense capital into U.S. equities and solidifying their position as the "king of them all."

Who Owns the Market Now?

The beneficiaries of this equity boom are diverse. While institutional investors like pension funds, endowments, and sovereign wealth funds remain significant holders, the rise of direct and indirect retail ownership is critical. Millions of individuals now participate through IRAs, 401(k)s, brokerage accounts, mutual funds, and Exchange Traded Funds (ETFs). Retirees increasingly rely on stocks to hedge against inflation, a stark contrast to the bond-heavy portfolios of past generations. Young people, often encouraged by accessible platforms, are entering the markets earlier. Furthermore, the "automatic investing revolution" – regular, often automated contributions to investment accounts – ensures a continuous flow of capital into the stock market, regardless of short-term volatility. This broad base of ownership magnifies the stock market’s importance to the financial well-being of a vast segment of the population.

Official Responses: The Central Bank’s Evolving Mandate

Given the stock market’s central role in national wealth and retirement savings, a provocative question has emerged from influential voices in finance: will the Federal Reserve eventually resort to buying stocks during the next severe financial crisis? Bloomberg’s Eric Balchunas, for instance, posed this very question, highlighting the increasing interdependence of market stability and economic policy.

Arguments for Fed Equity Purchases

The arguments supporting potential Fed intervention in equity markets are compelling, particularly in the context of extreme economic distress:

- "The Stock Market is Our Retirement Fund": With such a large portion of household wealth tied to equities, a sustained collapse could devastate retirement savings, consumer confidence, and the broader economy, necessitating extraordinary measures.

- Precedents from Abroad: The Bank of Japan (BOJ) has been a significant buyer of equities and equity ETFs for years as part of its unconventional monetary policy. Similarly, China’s "national team" of state-backed entities has intervened in its stock markets during periods of crisis. These examples demonstrate that such actions, while unconventional in the West, are not without precedent globally.

- "The Fed Put" Expectation: Years of Fed intervention, from quantitative easing (QE) to emergency liquidity facilities, have arguably conditioned markets to expect central bank support during crises. This implicit "Fed Put" creates an expectation that the central bank will step in to prevent catastrophic market declines, making non-intervention potentially more destabilizing.

- Limited Conventional Tools: With interest rates often near the zero lower bound during crises, central banks may find themselves with limited conventional monetary policy tools, forcing them to consider more unconventional approaches.

Concerns and Arguments Against

However, the idea of the Fed buying stocks is fraught with significant concerns and strong opposition:

- Moral Hazard: Direct equity purchases by the Fed could create immense moral hazard, encouraging excessive risk-taking by investors and corporations who believe the central bank will always backstop their losses.

- Distortion of Capital Allocation and Price Discovery: Central bank intervention could distort market pricing, misallocating capital, and undermining the fundamental mechanism of price discovery, which is essential for efficient markets.

- Political Ramifications and Mandate Issues: Such an action would be highly controversial, inviting accusations of socialism, favoritism, and overreach. The Fed’s mandate is typically focused on price stability and maximum employment, not directly propping up asset prices. Expanding this mandate to include equity purchases would require significant legal and political re-evaluation.

- Wealth Inequality: Direct equity purchases could disproportionately benefit wealthier individuals and institutions who hold more stocks, exacerbating wealth inequality.

- Exit Strategy Challenges: Unwinding a substantial portfolio of equities without disrupting markets would present an enormous challenge for the central bank.

While many may scoff at the notion of the Fed buying stocks, the severity of the next financial crisis could very well push policymakers to consider measures once thought unthinkable. The ongoing debate highlights the immense pressure on central banks in an era of unprecedented market importance.

Implications of an Equity-Centric Financial Landscape

Regardless of whether the Fed ever directly intervenes in equity markets, the undeniable fact is that the stock market is now more important than ever. This new reality carries profound implications for financial stability, economic policy, and investor behavior.

Accelerated Market Cycles: Flash Crashes and Faster Corrections

One significant consequence of heightened market participation and technological advancements is the likelihood of faster, more intense market corrections and bear markets. The original article points to "flash crash bear markets" as a potential recurring feature. With millions of people invested, often through automated systems, and algorithmic trading dominating institutional flows, market movements can be amplified and accelerated. News, sentiment, or even technical triggers can propagate through the system at lightning speed, leading to rapid declines that dwarf historical precedents in their velocity. This necessitates a new approach to risk management and investor psychology, as traditional "buy the dip" strategies might need to contend with more extreme and sudden drawdowns.

The Market as a Policy Lever: Forcing the Hand of Policymakers

Perhaps the most potent implication of the stock market’s current dominance is its newfound ability to influence, and at times dictate, government policy. The market has effectively gained a "veto power" over certain political decisions, as evidenced by several recent historical events:

- TARP Vote (2008): When the House initially rejected the $700 billion Troubled Asset Relief Program (TARP) bailout fund during the 2008 financial crisis, the stock market plummeted nearly 9% the following day. This immediate and severe market reaction arguably pressured lawmakers to reconsider, leading to the bill’s eventual passage.

- COVID-19 Stimulus (2020): The rapid 35% fall in the stock market in a matter of weeks during the early days of the COVID-19 pandemic undoubtedly played a crucial role in galvanizing bipartisan support for trillions of dollars in government spending and unprecedented monetary policy interventions. The economic and social cost of allowing the market to continue its freefall was deemed too high.

- Tariff Policies (Pre-2020): Periods of escalating trade tensions and tariff announcements often led to swift, negative market reactions. The original article notes tariffs being "walked back" following a sharp 19% drop in the stock market. Policymakers became acutely aware of the market’s sensitivity to trade policy, influencing the pace and severity of such measures.

- Geopolitical Conflicts (e.g., Iran): Even in geopolitical arenas, the stock market’s influence can be felt, particularly through commodity prices. The original article highlights how "energy prices spiking have played a role in how the Iran conflict has played out." Disruptions to oil supplies, for instance, immediately impact global energy markets, feeding back into equity prices and influencing diplomatic calculations.

These instances demonstrate a powerful feedback loop: policymakers understand the stock market’s importance to national wealth and economic stability, making them highly sensitive to its movements. Rapid declines create immense political pressure for intervention, effectively "forcing their hand." This dynamic fundamentally alters the relationship between financial markets and government, suggesting that policy decisions will increasingly be scrutinized through the lens of their immediate market impact.

The "New Normal" for Investors and the Economy

This era of equity dominance is undeniably "the new normal." For investors, it means navigating a landscape where:

- Volatility is Inherent: Faster corrections and bear markets will demand greater resilience and a long-term perspective.

- Participation is Crucial: Given the market’s central role in wealth creation and retirement, "don’t fight the stock market" becomes a guiding principle, encouraging continuous participation despite short-term fluctuations.

- Automatic Investing Reinforces Momentum: The continuous flow of capital from automatic investment plans creates a baseline demand for equities, potentially buffering downturns but also contributing to upward momentum.

For the broader economy, the implications are equally profound:

- Increased Vulnerability to Market Shocks: A highly concentrated and interconnected financial system means that market downturns can have more immediate and widespread economic consequences.

- Challenges to Traditional Valuation: The sheer scale of capital flowing into equities, combined with low interest rates, may challenge traditional valuation metrics, making it harder to discern genuine value from speculative bubbles.

- Policy Constraints: Policymakers may find their options constrained by the need to maintain market stability, potentially leading to less independent economic policy and an overreliance on market-pleasing measures.

The trillion-dollar question remains what truly unforeseen consequences will emerge from this new paradigm. While the benefits of accessible investing and wealth creation are clear, the potential for increased systemic risk, accelerated market cycles, and an altered relationship between markets and governance are significant.

In conclusion, the stock market’s journey from a niche domain to the undisputed driver of household wealth and economic policy is complete. The historical barriers have fallen, technological advancements have democratized access, and the sheer scale of U.S. equity capitalization now exerts immense influence globally. This is a powerful, dynamic, and potentially fragile new normal, where the stock market is not just a reflection of the economy, but increasingly, its master. Investors, policymakers, and citizens alike must adapt to this reality, understanding that the stock market is, more than ever, in the driver’s seat.