The Spreadsheet Renaissance: An In-Depth Journalistic Analysis of Tiller Money and the Future of Personal Finance

The landscape of personal finance management (PFM) software has undergone a dramatic evolution over the last two decades. From the early days of desktop-bound programs like Quicken to the cloud-based, automated convenience of platforms like Intuit Mint, consumers have long sought the perfect balance between automation and customization. However, as legacy platforms shut down or pivot, a growing cohort of financially savvy users is turning back to a classic tool: the spreadsheet.

At the forefront of this movement is Tiller Money, a specialized financial service that bridges the gap between modern API-driven banking automation and the infinite customization of Microsoft Excel and Google Sheets. This investigative review explores how Tiller Money operates, analyzes its core features, evaluates its security infrastructure, and examines its broader implications for the future of consumer financial technology.

Main Facts: What is Tiller Money?

Tiller Money is a financial technology platform designed to automate the collection of personal financial data directly into user-controlled spreadsheets. Unlike traditional personal finance applications that lock users into proprietary dashboards and rigid, pre-built budgeting frameworks, Tiller treats Google Sheets and Microsoft Excel as the primary user interface.

The service operates on a subscription-based model ($79 per year, following a 30-day free trial) and delivers a daily feed of cleared transactions, pending charges, and account balances directly into its users’ designated spreadsheets.

The Core Problem Tiller Solves

For decades, personal finance enthusiasts who preferred spreadsheets faced three systemic bottlenecks:

- The Data Entry Hurdle: Manually downloading CSV files from multiple bank, credit card, and investment accounts, and then formatting and pasting them into a master spreadsheet, is tedious and prone to human error.

- Template Design Fatigue: Designing an aesthetically pleasing, functionally robust spreadsheet that tracks budgets, net worth, and cash flow requires advanced formulas and significant time.

- Analytical Limitations: Creating dynamic charts, debt payoff schedules, and investment forecasting models from raw data requires high-level Excel or Google Sheets proficiency.

Tiller Money addresses these challenges by automating data aggregation while providing pre-built, highly flexible templates that users can modify at will. It offers a hybrid solution: the automation of a modern budgeting app combined with the absolute control of a personal spreadsheet.

Chronology: From Account Connection to Monthly Execution

Understanding how Tiller Money integrates into a user’s daily financial routine requires looking at the chronological workflow of setting up and maintaining the system.

[Step 1: Secure Account Aggregation (via Yodlee)]

│

▼

[Step 2: Foundation Template Deployment (Google Sheets/Excel)]

│

▼

[Step 3: Multi-Spreadsheet Mapping (Up to 5 Sheets)]

│

▼

[Step 4: Daily Automated Data Feeds (Transactions & Balances)]

│

▼

[Step 5: Rules-Based Categorization (AutoCat Engine)]

│

▼

[Step 6: Advanced Financial Analysis (Tiller Labs Add-ons)]Phase 1: Secure Account Aggregation

The process begins when a user registers on the Tiller platform and links their financial institutions. Tiller utilizes Yodlee, a premier financial data aggregation service employed by nine of the fifteen largest U.S. financial institutions.

Users search for their banks, credit card issuers, mortgage lenders, and brokerage firms, inputting their credentials through a secure, encrypted portal. Once connected, Tiller establishes a read-only data pipeline.

Phase 2: Deploying the Foundation Template

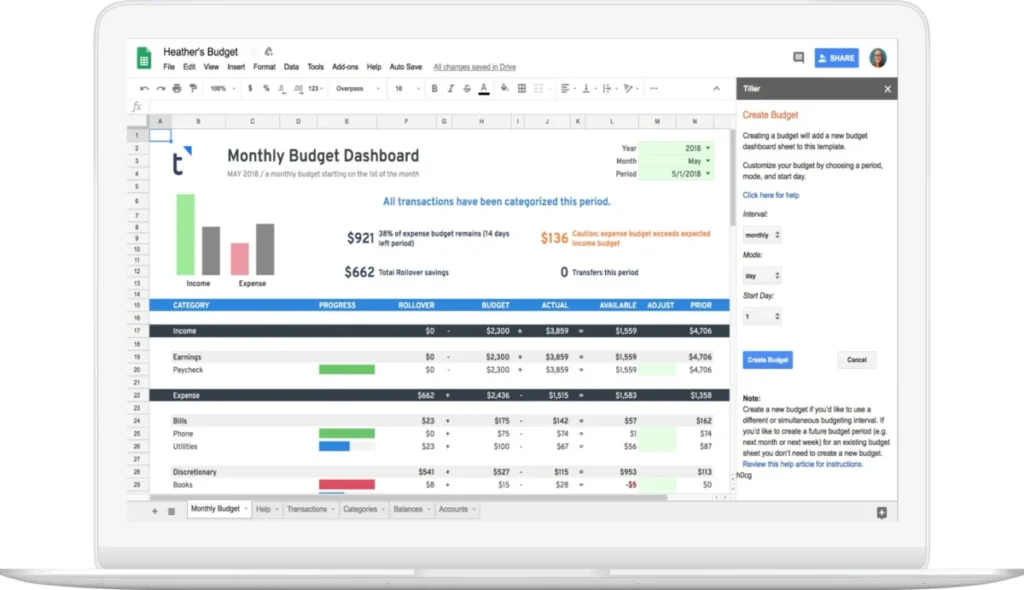

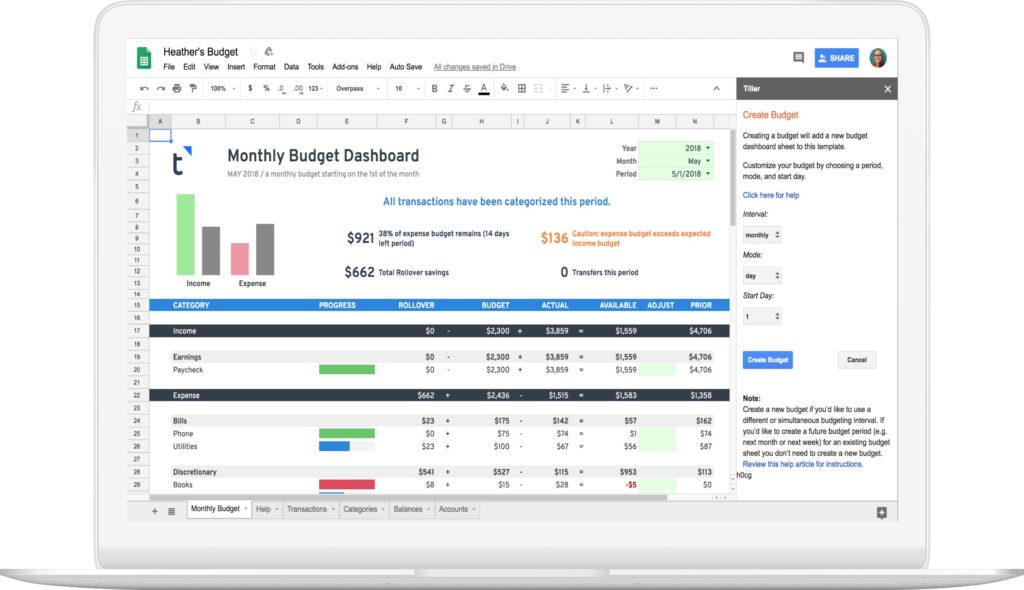

After establishing the data connections, the user launches either a Google Sheet or an Excel workbook. Rather than forcing users to build a sheet from scratch, Tiller provides the Tiller Foundation Template.

During initial setup, users authorize the Tiller add-on within their spreadsheet program. This creates a highly structured environment complete with several core tabs:

- Insights: A high-level dashboard summarizing current net worth, recent spending trends, and budget alerts.

- Transactions: A master ledger where every aggregated transaction is recorded chronologically.

- Categories: A customization page where users define their unique income and expense categories, grouping them into broader buckets (e.g., mapping "Coffee" and "Dining Out" to a "Wants" group).

- Monthly & Yearly Budgets: Dynamic sheets that automatically aggregate transaction data and compare actual spending against user-defined limits.

Phase 3: The Multi-Sheet Mapping Strategy

A key operational distinction of Tiller is that connecting accounts to the platform does not automatically dump all data into a single spreadsheet. Instead, Tiller allows users to link their connected financial accounts to up to five distinct spreadsheets.

This multi-sheet mapping capability enables clean operational segregation:

- Sheet 1 (Personal Budgeting): Linked to checking, savings, and consumer credit cards.

- Sheet 2 (Business Bookkeeping): Linked exclusively to business checking accounts and business credit cards, keeping tax-deductible expenses separate.

- Sheet 3 (Net Worth & Investment Tracking): Linked to retirement accounts, brokerage portfolios, and mortgage balances to monitor long-term wealth building without cluttering daily transaction ledgers.

Phase 4: Daily Automation and the "AutoCat" Engine

Once configured, the system runs automatically in the background. Every day, Tiller pulls cleared transactions and updated balances from the user’s linked financial institutions and writes them directly into the designated spreadsheets.

To streamline the process, users employ AutoCat (Automatic Categorization). This rules-based engine allows users to write custom criteria based on transaction descriptions. For example, a rule can dictate that any transaction containing the string "Starbucks" or "Peet’s" automatically be categorized as "Coffee" under the "Wants" group. Over time, AutoCat can automate the classification of over 90% of daily transactions, requiring the user only to review outliers.

Supporting Data: Features, Security Architecture, and Market Positioning

To understand Tiller’s value proposition relative to its competitors, we must examine its technical features, security protocols, and cost structure.

Deep-Dive: Tiller Money Labs

Beyond the standard Foundation Template, Tiller offers an experimental but highly stable ecosystem called Tiller Money Labs. This add-on directory provides users with modular, one-click templates designed to solve specific financial problems:

| Tool / Dashboard | Primary Function | Ideal User |

|---|---|---|

| Split Transactions | Divides a single transaction (e.g., a Target receipt) across multiple budget categories. | Detail-oriented budgeters |

| Net Worth Dashboard | Generates dynamic 12-month net worth charts and historical trend tables. | Wealth builders |

| Debt Planner | Employs debt snowball or debt avalanche methodologies to calculate payoff timelines. | Users working toward debt freedom |

| Bill Payment Tracker | Monitors recurring liabilities and projects upcoming cash flow demands. | Busy households |

| FIRE Retirement Planner | Projects future investment growth based on customizable real-rate-of-return scenarios. | Financial Independence, Retire Early adherents |

Security Architecture and Data Privacy

When dealing with automated financial aggregation, security is paramount. Tiller’s architecture is built on a "read-only" philosophy, meaning the platform can read transaction data but lacks any capability to initiate transfers, make payments, or modify account settings.

┌────────────────────────┐ ┌───────────────────┐ ┌────────────────────────┐

│ Financial Institution │ ──────> │ Yodlee Aggregator│ ──────> │ Tiller Money API │

│ (MFA / Bank Security) │ <────── │ (Read-Only Token) │ <────── │ (256-bit AES Encr.) │

└────────────────────────┘ └───────────────────┘ └────────────────────────┘

│

▼

┌────────────────────────┐

│ User's Google Drive / │

│ Microsoft OneDrive │

└────────────────────────┘Key security specifications include:

- Bank-Grade Encryption: Tiller utilizes 256-bit AES encryption to secure all data in transit and at rest.

- Multi-Factor Authentication (MFA): Tiller supports and encourages MFA for user login credentials. When aggregating accounts that require MFA, the system prompts the user to enter their one-time passcode securely via the Yodlee interface.

- Credential Protection: Tiller never stores or even sees bank login credentials; these are handled directly by Yodlee.

- Data Sovereignty: Unlike many free financial apps that monetize user data by serving targeted advertisements or selling anonymous consumer spending trends to third-party market research firms, Tiller’s subscription model ensures that user data is never sold or shared. The data resides entirely within the user’s private Google Drive or Microsoft OneDrive account.

Pricing and Cost-Benefit Analysis

Tiller’s pricing structure is straightforward: a $79 annual subscription (approximately $6.58 per month).

When compared to its direct and indirect competitors in the personal finance space, Tiller occupies a distinct pricing tier:

- Empower (formerly Personal Capital): Free. Highly effective for investment and net worth tracking, but lacks granular, customizable budgeting tools.

- Quicken Classic: $48 to $120+ annually. Powerful, but relies on legacy desktop software architectures that lack the collaborative, cloud-native flexibility of Google Sheets.

- Monarch Money / Copilot: $100 to $120+ annually. Modern, highly polished mobile-first interfaces, but users are entirely locked into their proprietary software ecosystems.

Official Responses and Market Reception

The personal finance community has responded enthusiastically to Tiller’s developer-centric, open-ended philosophy. At major industry gatherings, such as FinCon (the premier national conference for digital personal finance content creators), Tiller has consistently been praised for its commitment to data transparency.

In reviews published by prominent financial analysts, Tiller is frequently cited as the ultimate destination for "Excel refugees"—individuals who spent years maintaining manual spreadsheets but abandoned them due to data entry fatigue, as well as users of legacy platforms like Mint who found modern alternatives too restrictive.

On developer and personal finance forums like Reddit’s r/PersonalFinance and r/TillerMoney, users frequently praise the platform’s community-driven template library. Because Tiller operates within open spreadsheet standards, advanced users routinely build and share custom dashboards, macro scripts, and complex financial projection models that any Tiller subscriber can easily import into their own sheets.

Implications: The Macro Shift in Personal Finance Technology

The rise of Tiller Money highlights a broader, systemic shift in consumer financial technology: the return to data sovereignty and the growing demand for modularity.

The Death of the "One-Size-Fits-All" PFM

For years, financial software developers operated under the assumption that consumers wanted sleek, gamified, mobile-first interfaces that made financial decisions for them. However, this approach often fails because personal finance is deeply personal. A gig-economy worker, a real estate investor, a corporate W-2 employee, and a retired individual pursuing the FIRE movement have fundamentally different analytical needs.

By utilizing spreadsheets as the canvas, Tiller acknowledges that no single development team can design an interface that perfectly suits every demographic. The spreadsheet remains the world’s most versatile analytical tool; by automating the data feed, Tiller preserves that versatility while eliminating its primary drawback.

The Open Banking Revolution

Tiller’s success is also intrinsically tied to the ongoing evolution of open banking APIs. As regulatory frameworks globally shift toward giving consumers explicit ownership of their financial data, services that facilitate the frictionless export and manipulation of that data will continue to gain market share.

Ultimately, Tiller Money represents a mature, highly secure, and deeply empowering tool for those who refuse to let proprietary software dictate how they visualize, manage, and project their financial futures. For the analytical consumer, the modest $79 annual fee is a small price to pay for absolute control over their financial data.