The Market’s Conundrum: A Tug-of-War Between Bullish Momentum and Mounting Bearish Headwinds

[City, State] – [Date] – The global financial markets currently find themselves at a critical juncture, presenting a perplexing paradox for investors. On one hand, robust economic fundamentals and a broadening bull market signal continued growth. On the other, a growing chorus of analysts points to deeply embedded risks, from unsustainable tech spending to resurgent inflation and speculative fervor, suggesting a potential inflection point. This dynamic creates a "trillion-dollar question" for market participants: which narrative will ultimately prevail?

Recent market performance has been undeniably strong. A widely cited analysis from "Chart Kid Matt" highlighted ten compelling reasons to maintain a bullish outlook, grounded in tangible data. Yet, a deeper dive into market mechanics and macroeconomic indicators reveals a darker undercurrent, prompting a critical examination of potential downside risks. This article delves into both perspectives, aiming to provide a comprehensive view of the complex forces shaping the investment landscape.

Main Facts: A Dual Narrative Unfolds

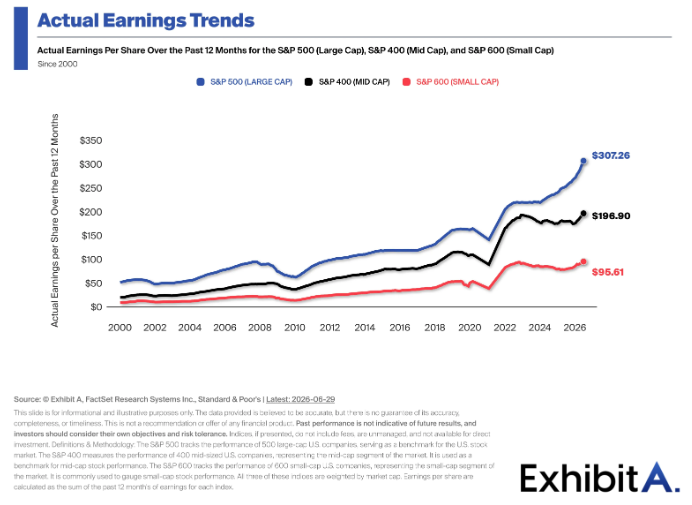

The prevailing sentiment for much of the recent past has been one of optimism. Corporate earnings growth is accelerating, margins remain robust, and the market’s leadership is reportedly broadening beyond the dominant "Magnificent Seven" tech giants. These indicators collectively paint a picture of fundamental strength driving stock market appreciation.

However, a closer inspection reveals significant vulnerabilities. A counter-narrative, often playing the role of "devil’s advocate," highlights ten key reasons why caution, if not outright bearishness, may be warranted. These include concerns about the circular nature of hyperscaler capital expenditure, the struggles of the very tech titans that have driven recent gains, the potential for an AI-led economic slowdown, and the alarming exuberance of retail investors. Furthermore, macroeconomic threats such as persistent inflation, elevated mortgage rates, and the prolonged absence of a "true" economic recession add layers of complexity and risk to the market’s current trajectory. The sheer magnitude of recent returns also raises questions about sustainability, echoing historical patterns of market overextension.

Chronology: From Post-Pandemic Rebound to Present-Day Ambiguity

The current market landscape is best understood by tracing its evolution from the lows of the 2020 COVID-19 pandemic. Following a brief but sharp downturn, unprecedented fiscal and monetary stimulus fueled a rapid recovery. This period saw the emergence of the "Magnificent Seven" (Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla, Meta Platforms) as dominant market drivers, their innovative prowess and massive scale propelling indices to new highs.

The Bullish Ascent (2020-Present):

From late March 2020, the S&P 500 has delivered spectacular annualized returns, exceeding 23%. Even from the bottom of the 2022 bear market, the index has climbed nearly 24% annually. This sustained rally, particularly pronounced in 2023 (26% gain), 2024 (25% gain), and 2025 (18% gain), culminated in a further 10% increase in the first half of the current year (2026). This performance has been underpinned by several factors:

- Accelerating Earnings Growth: Companies across various sectors have reported stronger-than-expected earnings, suggesting underlying economic resilience and efficient corporate operations.

- High Profit Margins: Despite inflationary pressures and supply chain challenges, many companies have maintained or even expanded profit margins, indicating pricing power and operational efficiency.

- Broadening Market Leadership: While initially concentrated in tech, there are signs that market gains are becoming more distributed across different sectors, a healthy indicator often associated with sustainable bull markets. This suggests that the rally is not solely dependent on a few large companies but reflects a wider economic recovery.

This period of sustained growth has fostered a sense of market stability, arguably leading to a degree of complacency among investors. However, beneath this surface of prosperity, several disquieting trends have begun to emerge, signaling potential vulnerabilities that could disrupt the established trajectory.

Emergence of Counter-Arguments (Recent Months):

More recently, concerns have intensified around several fronts. The massive capital expenditure (capex) by hyperscalers, while driving the AI boom, is now being scrutinized for its circularity and sustainability. The very Mag 7 stocks that led the charge are showing signs of weakness, raising questions about market breadth. Geopolitical events, such as the Iran war, have reignited inflation fears, threatening the delicate balance of monetary policy. Simultaneously, indicators of excessive retail investor speculation and the prolonged absence of a significant economic downturn have prompted a re-evaluation of market risks.

Supporting Data: A Deep Dive into Bullish and Bearish Indicators

To fully grasp the market’s current state, it is essential to examine the specific data points and arguments supporting both bullish and bearish outlooks.

The Enduring Case for Optimism

The bullish narrative is built on solid, fundamental pillars:

- Robust Earnings Trajectory: The acceleration in corporate earnings growth is a powerful stimulant for stock prices. It indicates healthy demand, effective cost management, and ultimately, increased shareholder value. Companies are not just growing revenue; they are translating it into higher profits, which historically supports valuation multiples.

- Sustained High Margins: High profit margins reflect operational efficiency and strong pricing power, allowing companies to absorb rising costs without significantly impacting their bottom line. This resilience is a key factor in navigating inflationary environments and maintaining profitability.

- Broadening Market Participation: The expansion of market leadership beyond a narrow group of mega-cap tech stocks is a crucial sign of a healthy bull market. When gains are more widespread, it suggests that the underlying economic recovery is broad-based, reducing the risk of a market correction driven by the stumble of a few heavily weighted companies. This diversification of drivers provides a more stable foundation for continued growth.

These fundamental strengths suggest that the market’s upward trajectory is not merely speculative but rooted in genuine economic and corporate performance.

The Compelling Case for Caution: Ten Bearish Indicators

While the bullish case is compelling, the counterarguments highlight systemic risks that cannot be ignored:

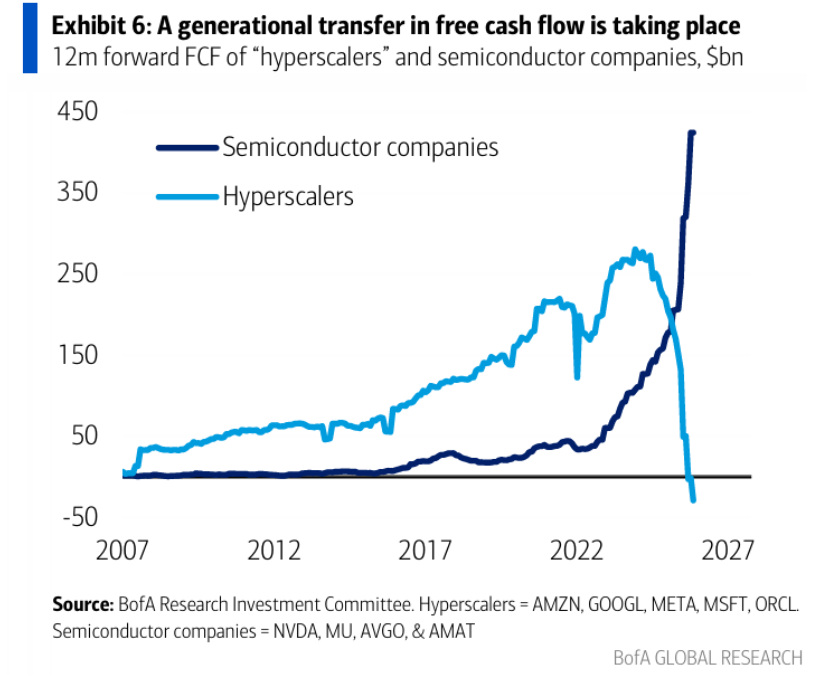

1. The Circularity of Hyperscaler Capital Expenditure:

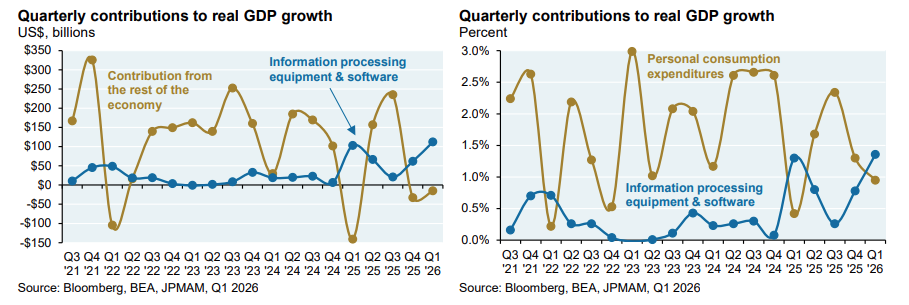

This is perhaps one of the most significant concerns. Large hyperscaler companies (cloud providers like Amazon, Microsoft, Google) are investing colossal sums in capital expenditure, primarily to build out infrastructure for Artificial Intelligence. However, a significant portion of this investment appears to be "circular" – free cash flow from these very hyperscalers is effectively being transferred to semiconductor companies (like Nvidia) to purchase the chips needed for AI development. The critical question is: what happens if this cycle slows? If the demand for AI infrastructure from external enterprises doesn’t materialize quickly enough, or if the hyperscalers themselves reach a point of diminishing returns on their AI investments, this massive capex binge could become unsustainable. A crash in free cash flow for these tech giants, driven by these investments, raises red flags about future profitability and the genuine economic impact of this AI buildout. The risk lies in an oversupply of AI infrastructure before sufficient demand from broader industries emerges, potentially leading to a sharp correction in the semiconductor and related tech sectors.

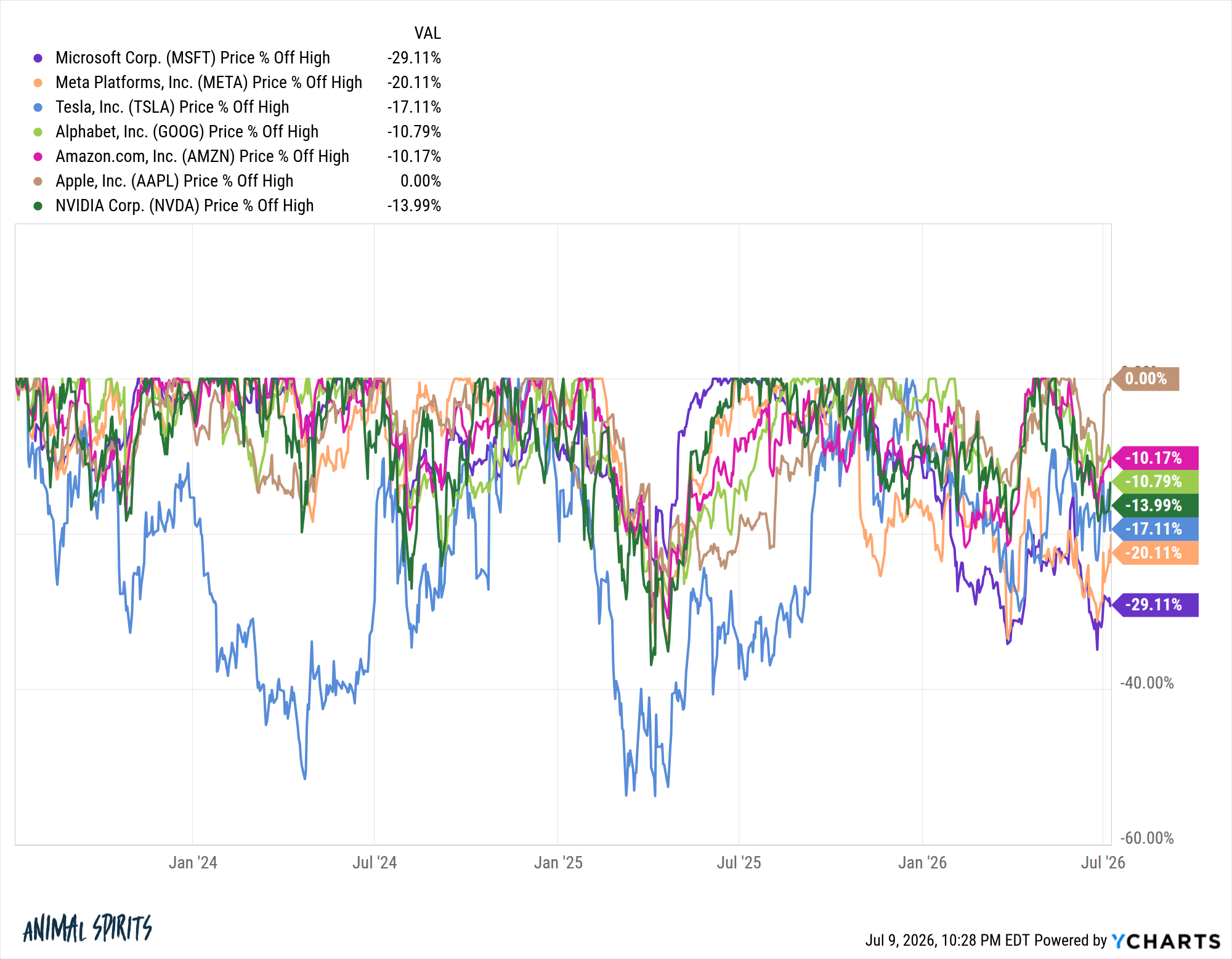

2. Underperformance of the "Magnificent Seven":

While the market leadership is broadening, the fact that the Mag 7 still constitutes roughly one-third of the S&P 500’s market capitalization makes their individual performance critically important. Alarmingly, every Mag 7 stock except Apple is currently experiencing a double-digit drawdown from its recent highs. This collective weakness, if it persists or intensifies, could significantly drag down the overall market. These companies are not just large; they are bellwethers for technological innovation and market sentiment. Their sustained struggles could signal a broader loss of confidence in high-growth tech or a shift in investor preference, impacting the wider index despite diversification elsewhere. A sustained slump in these behemoths could trigger a broader market correction, given their outsized influence.

3. AI’s Deepening Economic Interconnection:

The impact of Artificial Intelligence is no longer confined to the stock market’s speculative fervor; it is increasingly bleeding into the real economy. As highlighted by analyses from financial institutions like JPMorgan, an AI slowdown could directly translate into an economic slowdown. This is because AI investments drive demand for specific technologies, services, and skilled labor. If the pace of AI innovation or adoption falters, or if the expected productivity gains do not materialize as quickly as anticipated, it could create ripple effects across various industries that have bet heavily on AI integration. Supply chains, employment trends, and corporate investment strategies are all becoming intertwined with the trajectory of AI development, making the broader economy vulnerable to any significant disruption in this sector.

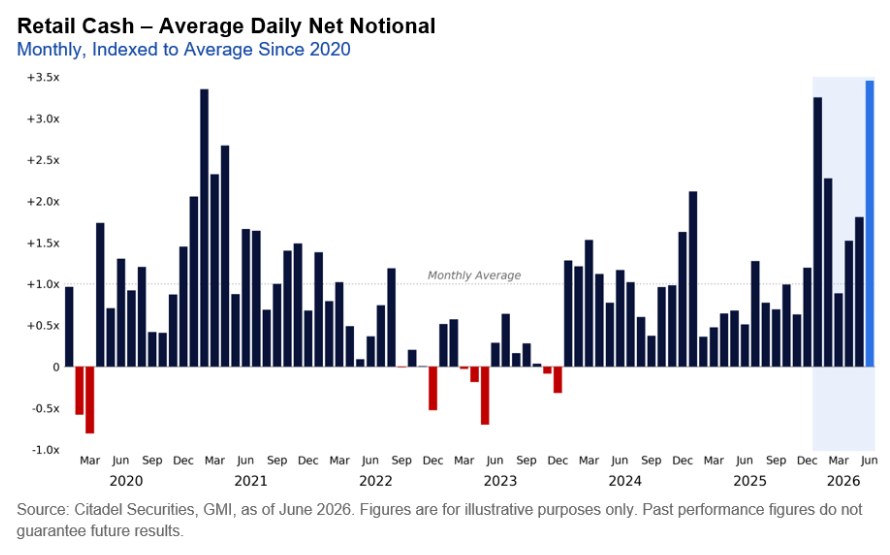

4. Record Retail Investor Exuberance:

According to data from Citadel Securities, retail investors are deploying capital at an unprecedented pace, aggressively participating in IPOs, options, futures, leveraged ETFs, and direct stock purchases. Historically, excessive retail speculation has often been a contrarian indicator, signaling market tops. When the "last dollar" rushes into the market, particularly into riskier assets and strategies, it can suggest that there are fewer new buyers to push prices higher, leaving the market vulnerable to a correction. This "all-in" mentality, fueled by FOMO (Fear Of Missing Out) and easy access to trading platforms, creates a fragile market environment susceptible to sharp downturns if sentiment shifts. It echoes the speculative frenzies seen in past bubbles, where inexperienced investors often suffer the most significant losses.

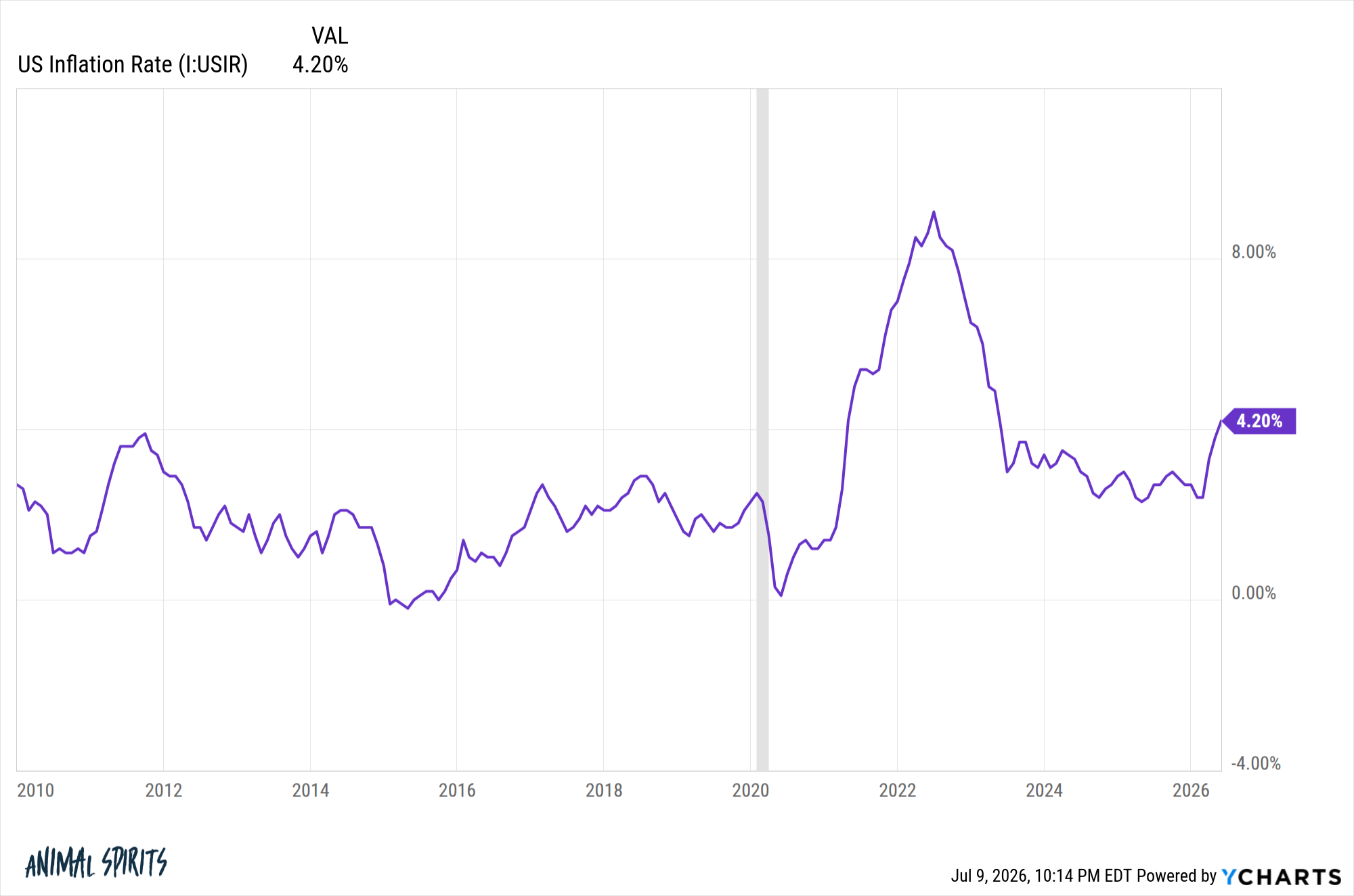

5. Persistent High Inflation:

The recent surge in inflation, pushed back above 4% following events like the Iran war, represents a significant headwind. While hopes exist that this is a temporary spike, the risk of "sticky inflation" – where price increases prove more stubborn than anticipated – is considerable. Persistent high inflation erodes purchasing power, increases business costs, and forces central banks to maintain tighter monetary policies for longer. This typically translates to higher interest rates, which can dampen economic activity, reduce corporate profits, and make equities less attractive compared to fixed-income investments. The specter of a stagflationary environment, characterized by high inflation and stagnant growth, remains a potent threat.

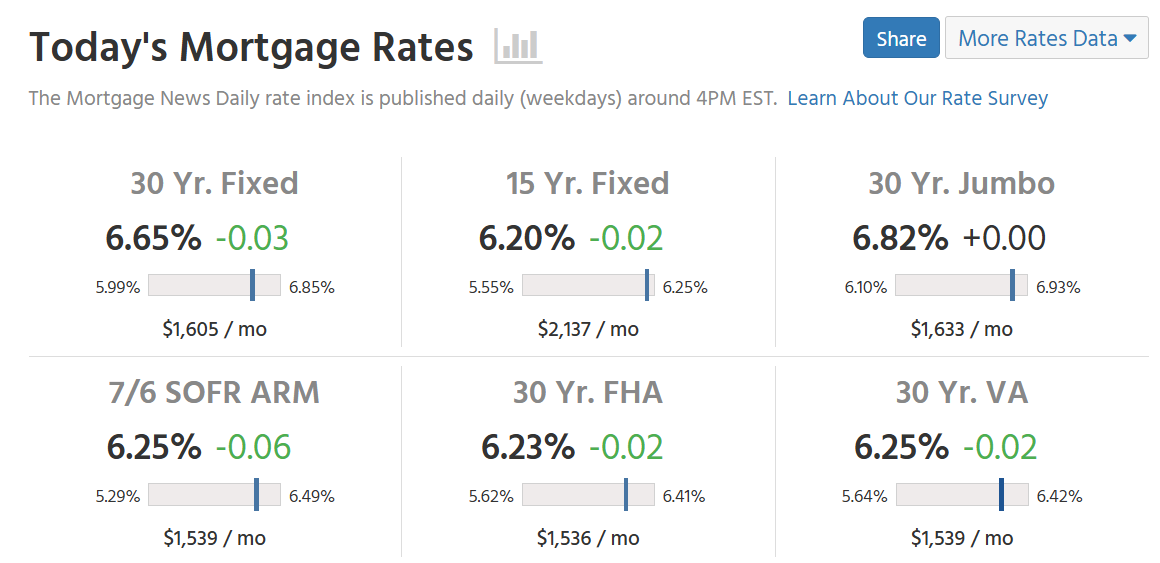

6. Elevated Mortgage Rates:

In tandem with persistent inflation, mortgage rates have remained stubbornly high, with the 30-year fixed rate once again approaching 7%. Housing is a foundational pillar of the economy, often serving as a significant driver of consumer spending and wealth. Prolonged high mortgage rates severely impact housing affordability, dampening sales, new construction, and home equity utilization. While the "housing recession" hasn’t yet caused widespread economic damage, the question remains: how long can this last? A sustained slump in the housing market could eventually spill over into broader economic weakness, affecting construction, manufacturing, retail, and financial services. The "lock-in" effect, where existing homeowners are reluctant to sell due to their low historical mortgage rates, further exacerbates supply issues and affordability challenges.

7. Growing Market Complacency:

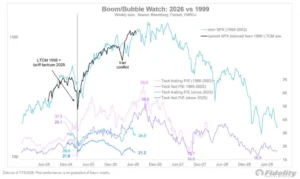

The S&P 500’s impressive gains over recent years – 10% in the first half of this year, following 18%, 25%, and 26% in the preceding three years – could be fostering a dangerous sense of complacency. As economist Hyman Minsky theorized, prolonged periods of stability can paradoxically breed instability. When markets perform consistently well, investors tend to take on more risk, underestimate potential downside, and rely on ever-increasing leverage. This creates a fragile system, vulnerable to a "Minsky moment" – a sudden, sharp market correction triggered by a minor event that exposes underlying vulnerabilities built up during periods of perceived calm. The absence of significant volatility can lull investors into a false sense of security, setting the stage for a more dramatic unwinding of risk.

8. AI Exhibiting Classic Bubble Characteristics:

Artificial Intelligence, while transformative, is increasingly checking all the boxes for a speculative bubble. The narrative includes:

- Technological Revolution: A genuine paradigm shift, but often accompanies overvaluation in its early stages.

- Capex Binge: Massive capital investments, often driven by competitive pressure rather than immediate profitability.

- Bull Market in Stocks: Driven by future promises rather than current fundamentals.

- Leverage in the System: Investors using borrowed money to amplify returns, increasing systemic risk.

- FOMO Kicking In: A pervasive fear among investors of missing out on perceived exponential gains.

- Retail Speculation: Widespread participation from individual investors, often chasing quick profits.

While AI’s long-term potential is undeniable, the short-term exuberance and speculative elements bear striking resemblance to historical bubbles like the Dot-Com era, raising concerns about a potential correction.

9. Overdue for a Recession:

Excluding the two-month, government-mitigated downturn of spring 2020 (which many argue wasn’t a "true" economic cycle due to its artificial nature and rapid reversal), it has been an unprecedented 17 years since the last genuine recession in America. Economic cycles are a fundamental aspect of capitalism, characterized by periods of expansion followed by contraction. The idea that recessions have been "outlawed" is economically naive. Prolonged expansions often lead to imbalances – overinvestment, excessive debt, and inflationary pressures – that eventually require a corrective downturn. The sheer length of the current expansion suggests that the economy may be due for a slowdown, which could trigger a market correction.

10. Unsustainably High Returns:

From the COVID-19 lows in March 2020, the S&P 500 has annualized returns of 23%, and from the 2022 bear market bottom, nearly 24%. While these figures are "cherry-picked" from market troughs, they underscore the spectacular nature of the current bull market. Historically, periods of exceptionally high returns are often followed by periods of more modest, or even negative, returns as markets revert to their long-term averages. The argument here is that future returns have, in a sense, been "pulled forward," implying that investors should temper their expectations. Sometimes, the most significant reason for stocks to decline is simply that they have risen too much, too fast, creating an imbalance between price and intrinsic value.

Analyst Perspectives and Policy Considerations

The conflicting signals present a formidable challenge for central banks, policymakers, and market analysts alike.

Central Bank Dilemmas: Monetary authorities, such as the Federal Reserve, face a tightrope walk. Persistent inflation, exacerbated by geopolitical events, necessitates a hawkish stance to curb price pressures. However, tightening too aggressively risks stifling economic growth, potentially tipping the economy into recession and exacerbating the very market vulnerabilities discussed. The debate centers on whether the current inflation is primarily demand-driven (requiring higher rates) or supply-side (less responsive to monetary policy).

Corporate Strategy: Hyperscaler executives are navigating immense pressure to continue AI investments while demonstrating sustainable returns. The circular capex model requires external adoption to validate the investment. Corporate leaders across sectors are evaluating how quickly AI can translate into tangible productivity gains and cost efficiencies to justify the current market valuations. Any slowdown in enterprise AI adoption could lead to a re-evaluation of investment plans.

Market Analyst Consensus (or Lack Thereof): The investment community is deeply divided. Some analysts dismiss the bearish indicators as temporary fluctuations or necessary market corrections that ultimately pave the way for further growth. They point to the transformative potential of AI, resilient consumer spending, and robust corporate balance sheets. Others warn of an impending correction, citing historical precedents of bubbles and economic cycles. The retail investor phenomenon, in particular, draws parallels to previous speculative eras, leading some to advise caution against chasing returns in highly leveraged or speculative assets.

Implications: Navigating the Uncertainty

The current market environment demands a nuanced approach from investors. The "trillion-dollar question" – whether to believe the bullish or bearish indicators – underscores the profound uncertainty.

For Investors:

- Risk Management: In an environment where complacency is a concern and speculative activity is high, robust risk management strategies are paramount. This includes diversification across asset classes and geographies, avoiding overconcentration in single sectors or stocks, and carefully assessing personal risk tolerance.

- Long-Term Perspective: Attempting to time market tops or bottoms is notoriously difficult. A long-term investment horizon, focused on fundamental value and disciplined investing, often proves more effective than reacting to short-term market noise.

- Diversification Beyond Tech: While technology remains a powerful force, the broadening market leadership and the underperformance of the Mag 7 suggest that a diversified portfolio across various sectors (e.g., industrials, healthcare, financials, consumer staples) could offer more stability.

- Monitoring Macroeconomic Data: Paying close attention to inflation trends, central bank policies, and housing market indicators will be crucial. These macroeconomic forces have the potential to override micro-level corporate performance.

- Avoiding Speculative Excess: The signs of retail investor exuberance in high-risk assets serve as a warning. Investors should exercise caution with highly leveraged products, IPOs, and speculative options trading, especially if not fully understanding the underlying risks.

For the Economy:

The interplay between these bullish and bearish forces will determine the trajectory of the broader economy. A soft landing, where inflation is tamed without triggering a recession, remains the ideal scenario. However, the confluence of high inflation, elevated interest rates, and potential overinvestment in AI, coupled with a complacent market, raises the risk of a harder landing. An AI slowdown could have significant ramifications for productivity growth, employment, and global competitiveness. The housing market’s resilience will also be a key indicator of consumer health and overall economic stability.

Ultimately, the market is a complex adaptive system, constantly reacting to new information and evolving narratives. While the current bullish momentum is strong, the emerging bearish signals highlight underlying fragilities that cannot be dismissed. The coming months will likely test the market’s resilience, revealing whether the foundation of current gains is as solid as it appears, or if the seeds of instability have been sown. Investors who approach this environment with a critical eye, a balanced perspective, and a disciplined strategy will be best positioned to navigate the unpredictable path ahead.