The Evolution of Wealth Management: A Comprehensive Analysis of the Empower Financial Platform

In an era defined by rapid digitization and shifting economic landscapes, retail investors are increasingly seeking centralized solutions to manage their wealth. Among the frontrunners in this financial technology revolution is Empower, a comprehensive wealth management tool designed to aggregate, analyze, and optimize an individual’s entire financial portfolio.

Formerly known as Personal Capital, Empower offers a single-dashboard experience that tracks net worth, monitors investment performance, analyzes fees, and projects retirement readiness. This journalistic analysis examines the core functionalities of the platform, its corporate evolution, security protocols, and its broader implications for the modern retail investor.

Main Facts: The Empower Ecosystem at a Glance

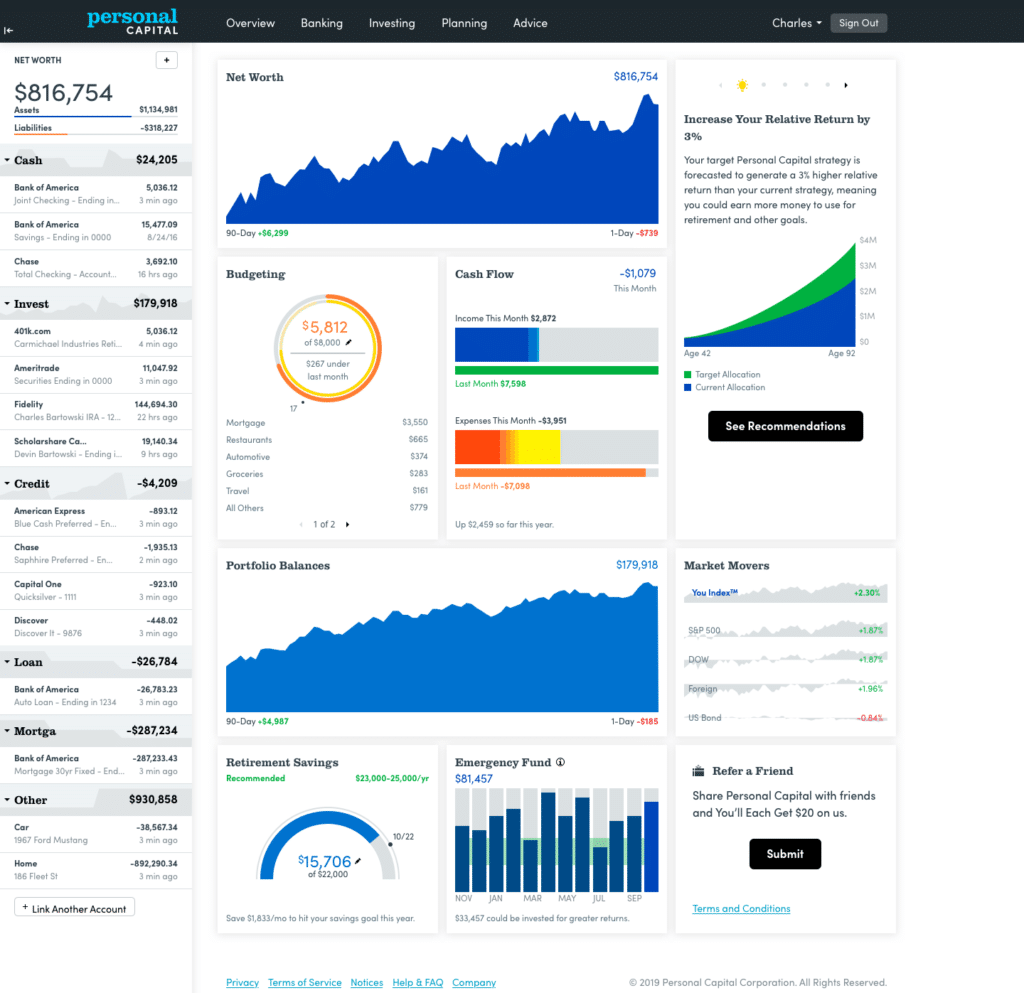

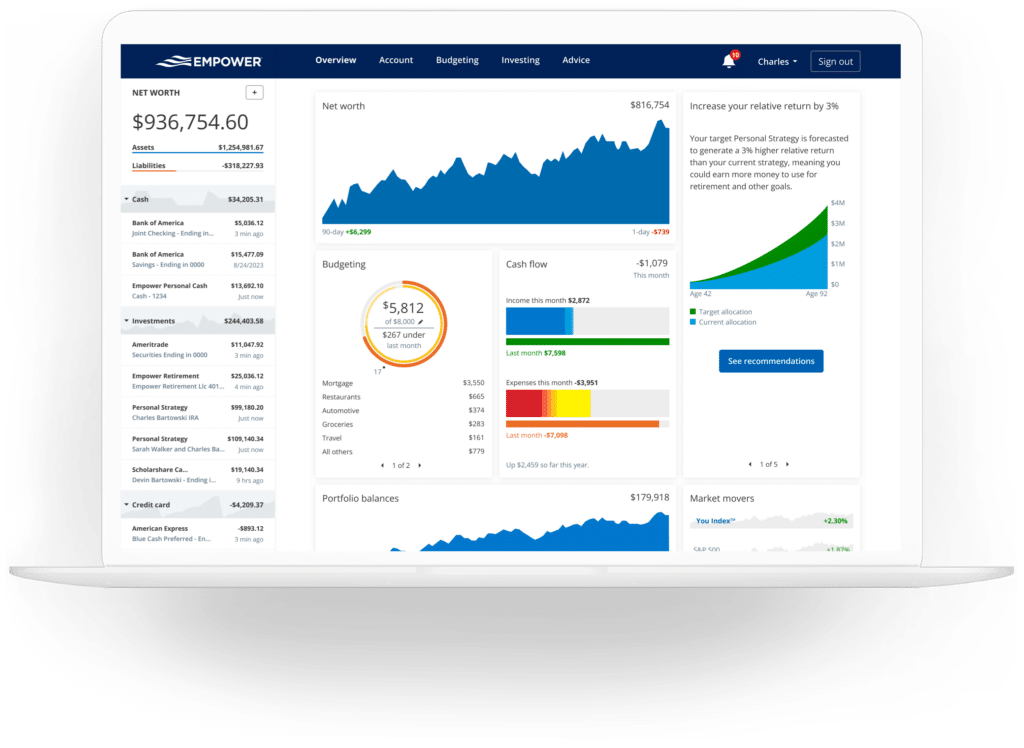

Empower functions primarily as a financial aggregator, pulling real-time data from a multitude of external accounts to construct a holistic view of a user’s financial health. Unlike basic budgeting applications, Empower’s architecture is heavily weighted toward investment analysis and long-term wealth planning.

Key Platform Capabilities

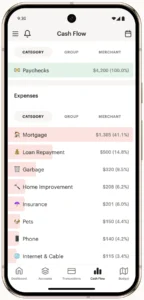

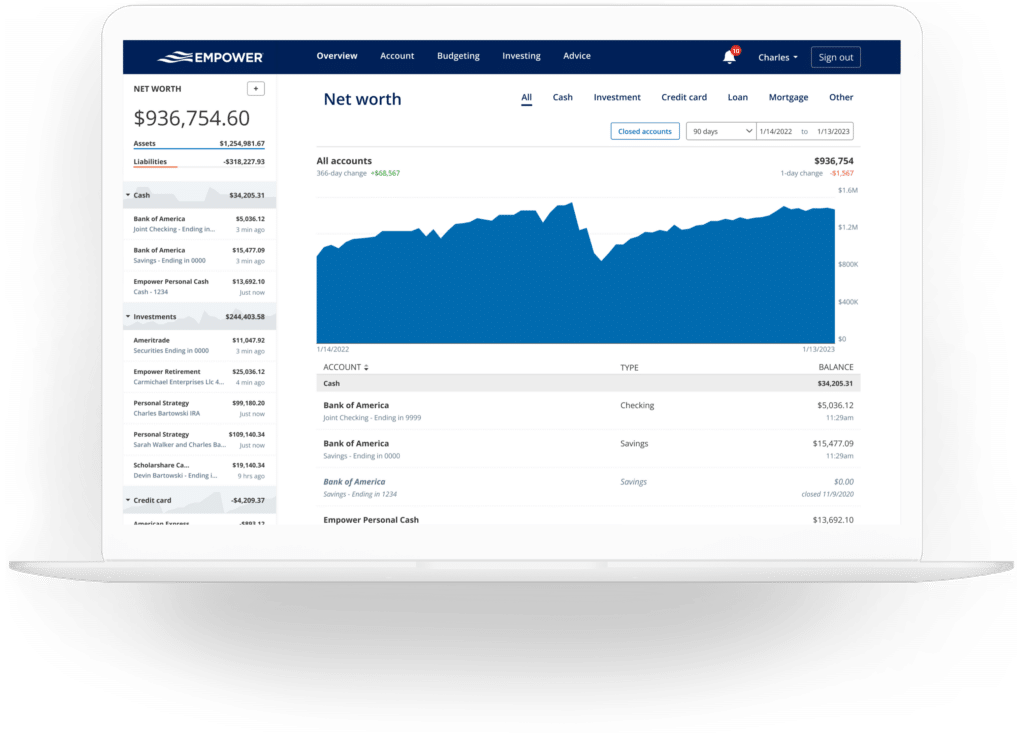

- Holistic Aggregation: Automatically synchronizes checking, savings, credit cards, mortgages, student loans, and investment accounts (including 401(k)s, IRAs, and taxable brokerage accounts).

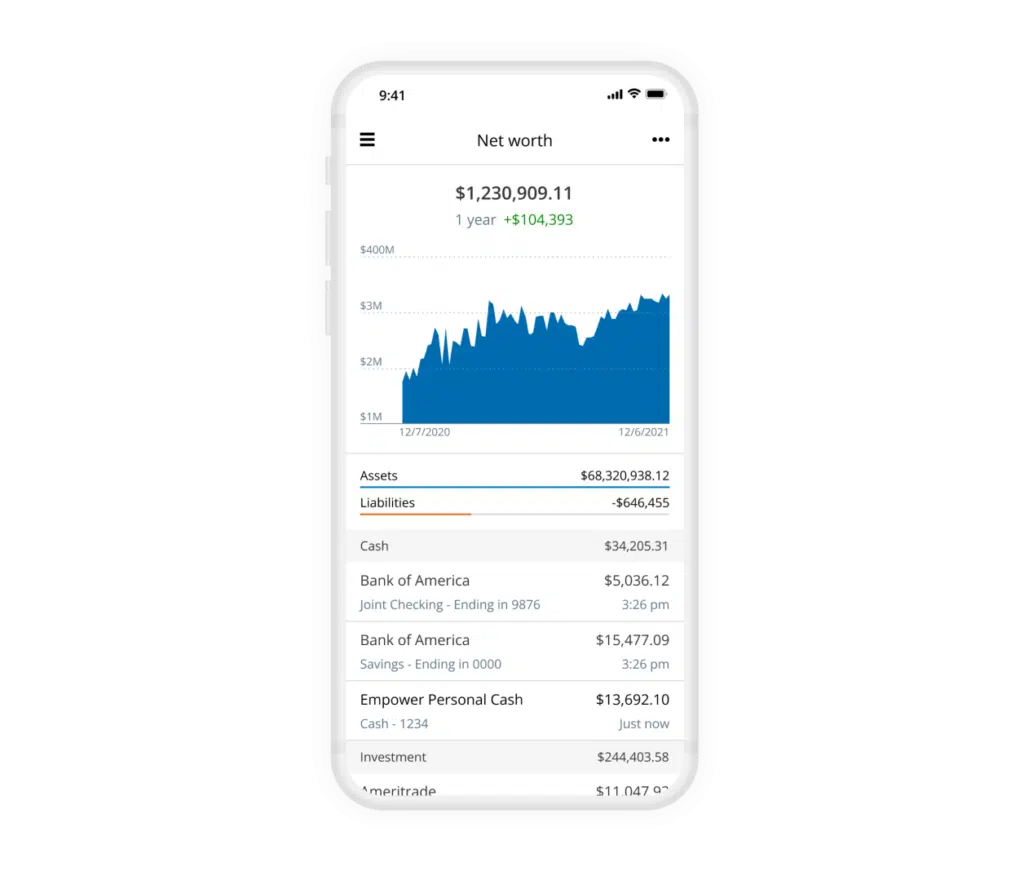

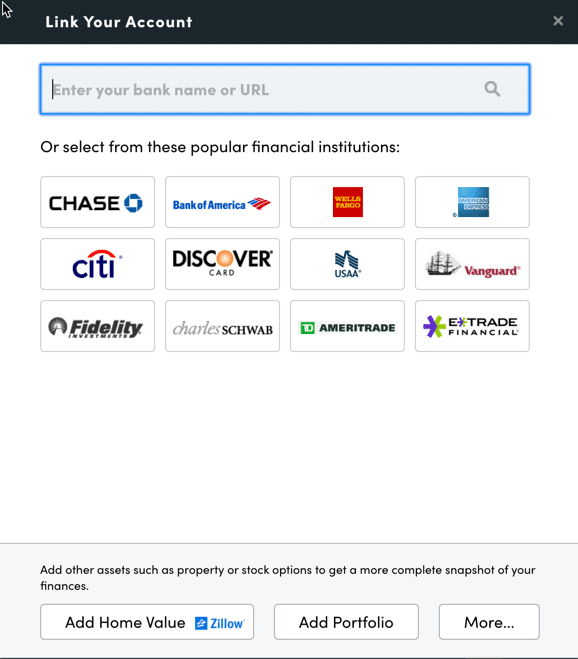

- Real-Time Net Worth Tracking: Consolidates assets and liabilities to deliver a live calculation of net worth. It also integrates with Zillow to estimate real estate asset values.

- Investment Diagnostics: Evaluates asset allocation, tracks performance against major market indices, and identifies hidden investment fees.

- Advanced Retirement Planning: Utilizes Monte Carlo simulations to calculate the probability of retirement success based on custom spending and saving scenarios.

- Cross-Platform Accessibility: Maintained via a robust web interface alongside highly-rated mobile applications.

Market Reception

The platform’s mobile applications maintain significant market penetration and highly favorable user ratings:

- iOS App Store: 4.8 out of 5 stars (compiled from over 366,000 user reviews).

- Google Play Store: 4.0 out of 5 stars (compiled from over 29,400 user reviews).

- Pricing Model: The digital dashboard and analytical tools are entirely free of charge, supported by a freemium model that promotes optional paid wealth management services.

Chronology: From Silicon Valley Startup to Financial Giant

To understand Empower’s current position in the fintech ecosystem, it is essential to trace its corporate history and the development of its feature set.

[2009] Personal Capital Founded by Bill Harris & Rob Foregger

│

[2020] Acquired by Empower Retirement for $1 Billion

│

[2023] Completed Rebranding to "Empower"

│

[Present] Expanded Integration of Digital Assets (Cryptocurrency Tracking)1. The Personal Capital Era (2009–2020)

The platform was founded in 2009 under the name Personal Capital by digital finance pioneers, including Bill Harris, the former CEO of Intuit and PayPal. The company’s goal was to bridge the gap between automated algorithm-driven "robo-advisors" and traditional, high-fee human wealth managers. Over the decade, the platform grew rapidly, gaining acclaim for its robust investment tracking and retirement planning calculators.

2. Acquisition and Rebranding (2020–2023)

In mid-2020, Personal Capital was acquired by Empower Retirement—one of the largest retirement services providers in the United States—in a deal valued at up to $1 billion. This acquisition combined Personal Capital’s cutting-edge digital interface with Empower’s massive institutional reach. By 2023, the platform had fully transitioned its branding from Personal Capital to Empower, integrating the digital dashboard into Empower’s broader suite of financial services.

3. Step-by-Step User Journey

For an individual user, the chronological onboarding process of the platform is designed for rapid integration:

- Account Creation: Users register for a free account, establishing identity and initial security parameters.

- Credential Linking: Using secure APIs, users search for their financial institutions (by name or URL) and link their accounts.

- Profile Optimization: Users input demographic data, anticipated retirement ages, income expectations, and risk tolerances.

- Dashboard Synthesis: Within minutes of account linkage, the platform aggregates years of historical transaction and investment data, presenting a unified financial snapshot.

Supporting Data: Deep-Dive into Analytical Tools

The true value of Empower lies in its diagnostic engines, which transform raw financial data into actionable intelligence.

The Retirement Fee Analyzer: Quantifying the Impact of Costs

Perhaps the most critical tool within the investment suite is the Retirement Fee Analyzer. Financial advisors and mutual fund managers frequently charge fees that appear negligible on paper—often ranging from 0.50% to 1.50%. However, when compounded over decades, these fees dramatically erode wealth.

Impact of Fees on a $1,000,000 Portfolio Over 30 Years (Assumed 7% Annual Return)

───────────────────────────────────────────────────────────────────────────

Fee Rate Ending Portfolio Value Cumulative Fees Paid

───────────────────────────────────────────────────────────────────────────

0.10% $7,380,000 $230,000

1.00% $5,740,000 $1,870,000

───────────────────────────────────────────────────────────────────────────

Difference: Lost wealth of $1,640,000 due to a 1% fee.Empower calculates a weighted average expense ratio across all linked investment accounts. Even for disciplined index investors with a low average expense ratio (e.g., 0.06% or 6 basis points), the analyzer demonstrates the exact dollar amount that will be lost to fund managers over a set time horizon, serving as an eye-opening tool for retail investors.

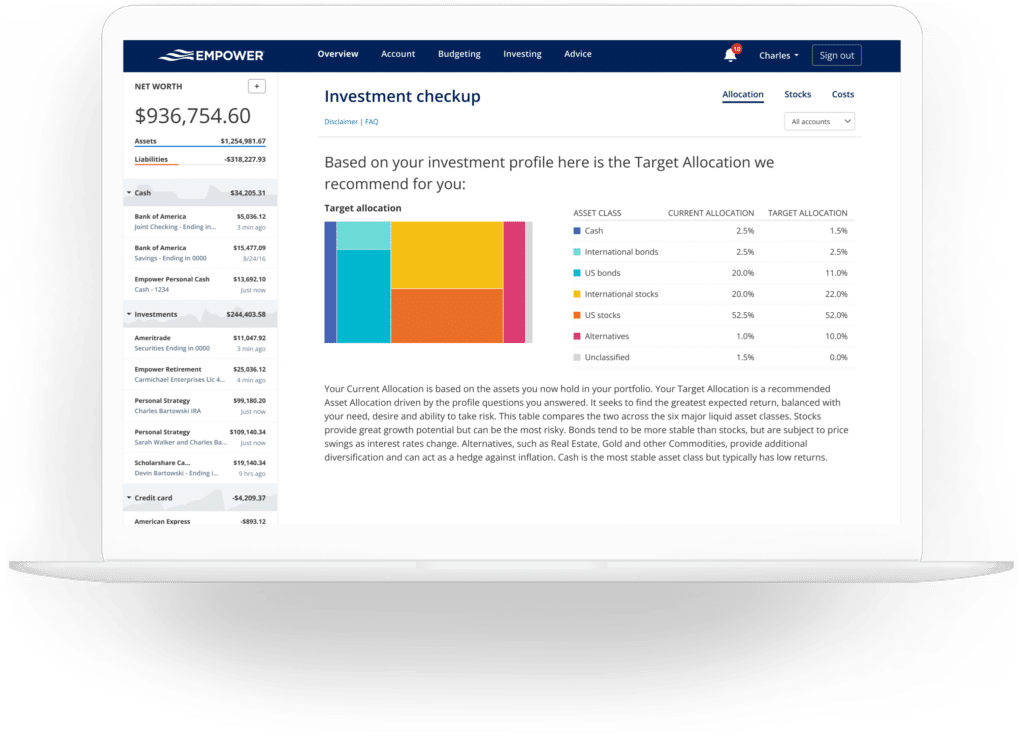

Portfolio Allocation Diagnostics

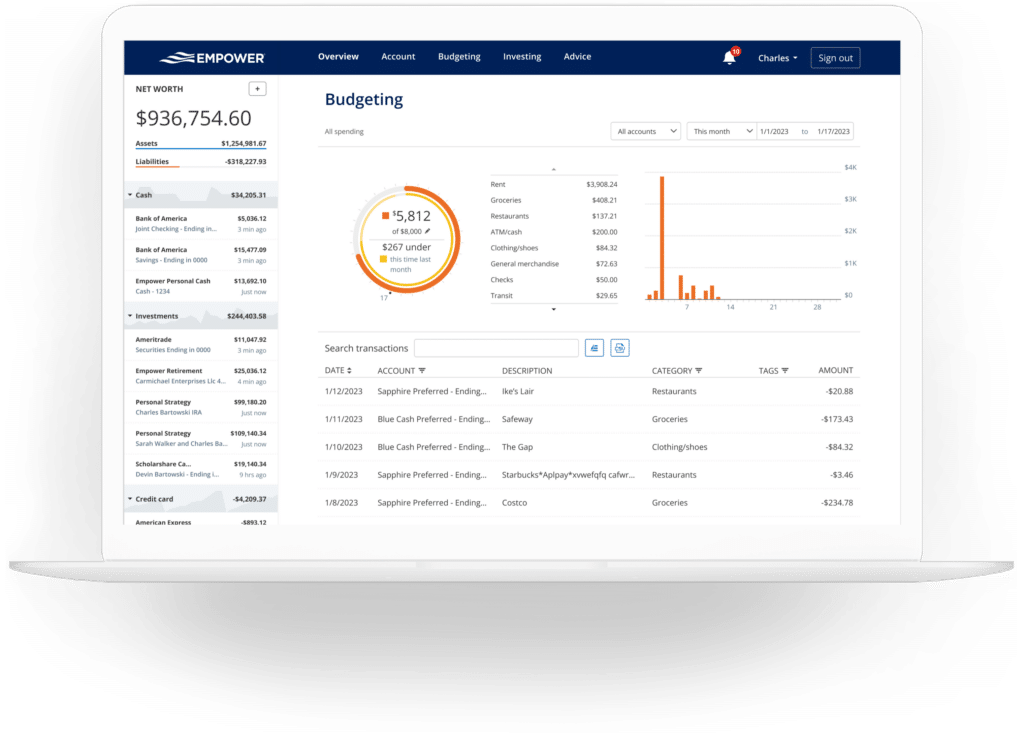

The platform provides an interactive, visual representation of asset allocation, categorizing holdings into domestic stocks, international stocks, bonds, cash, and alternatives.

Crucially, Empower’s engine "looks through" mutual funds and exchange-traded funds (ETFs) to identify their underlying holdings. For example, if a user holds an equity mutual fund that maintains a 5% cash drag, Empower reflects that cash balance in the global asset allocation chart rather than classifying the entire fund simply as "equities."

Cryptocurrency Integration

Acknowledging the maturation of digital assets, Empower has integrated cryptocurrency tracking. To maintain security, the platform does not require users to input private keys or link directly to cold wallets. Instead, users manually input their holdings by specifying:

- The token symbol (e.g., BTC, ETH, LTC)

- The exchange where it is held

- The total quantity owned

The platform then pulls live market data to track the real-time value of these digital assets alongside traditional equities and real estate.

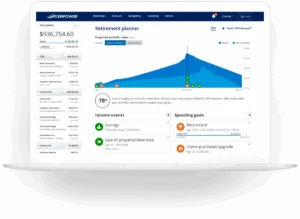

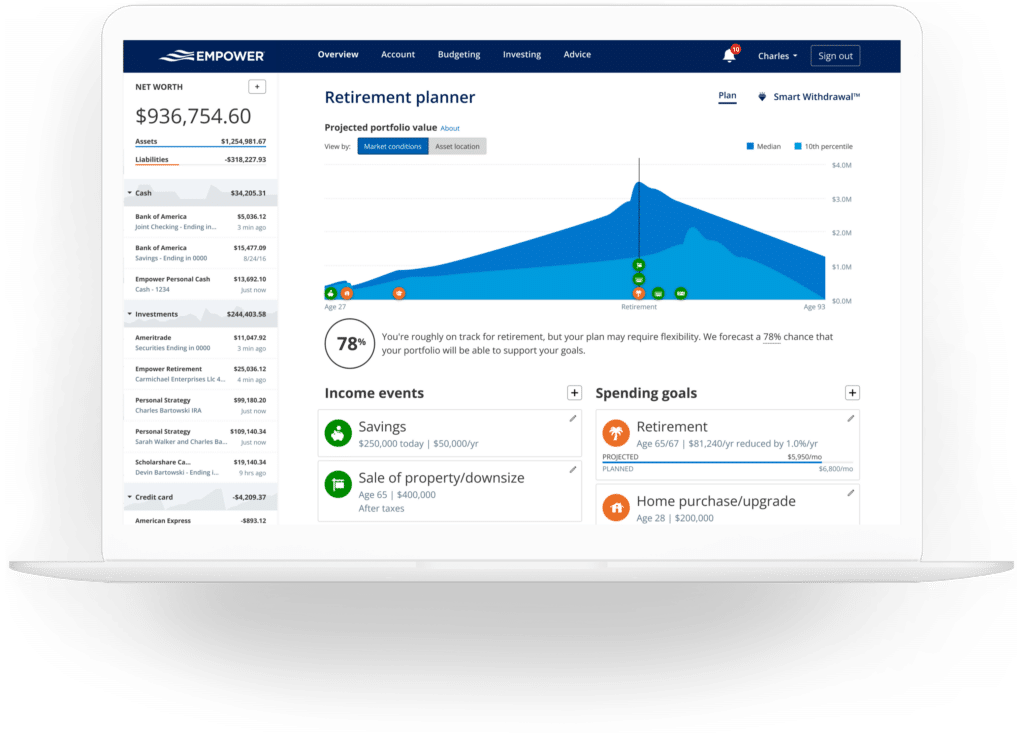

Scenario Planning in the Retirement Planner

The Retirement Planner utilizes Monte Carlo simulations to run thousands of market scenarios, determining the probability that a user’s portfolio will survive their retirement years.

Users can build and compare divergent scenarios side-by-side:

- Scenario A: Retiring at age 65 with anticipated Social Security benefits and a 4% annual withdrawal rate.

- Scenario B: Early retirement at age 55 with zero Social Security, higher initial travel spending, and a modified effective tax rate.

Corporate Structure, Security, and Business Model

A common question among consumers is how a platform as sophisticated as Empower can offer its services entirely free of charge. The answer lies in its corporate business model.

The Freemium Wealth Management Model

Empower operates its dashboard as a highly effective lead-generation tool. The software is free, but users who aggregate more than $100,000 in investable assets are typically contacted by Empower’s human financial advisors. These advisors pitch the company’s paid wealth management services.

Paid Advisory Fee Structure (Based on Assets Under Management - AUM)

───────────────────────────────────────────────────────────────────────────

Asset Tier Annual Fee Rate

───────────────────────────────────────────────────────────────────────────

First $1,000,000 0.89%

First $3,000,000 (for larger portfolios) 0.79%

Next $2,000,000 0.69%

Next $5,000,000 0.49%

───────────────────────────────────────────────────────────────────────────There is no obligation to use these paid services; users can decline the advisory offers and continue using the free dashboard indefinitely.

Security and Data Privacy Protocols

Because users must trust the platform with their financial credentials, security is a paramount concern. Empower implements several bank-grade security protocols:

- Encryption: Data is encrypted in transit and at rest using AES-256 encryption with multi-layer key management.

- Credential Isolation: No human employee at Empower has access to linked passwords or login credentials. The synchronization is handled via secure, read-only data aggregation partners.

- Multi-Factor Authentication (MFA): Access from any unrecognized device requires secondary verification via SMS, email, or phone call.

- Geofencing & Alerts: The platform can be configured to send immediate alerts if access is attempted from outside the user’s home country.

Implications: The Democratization of Wealth Management

The rise of platforms like Empower has profound implications for both individual consumers and the broader financial technology sector.

1. The Post-Mint Era and the Fintech Landscape

Following Intuit’s controversial decision to shut down its popular budgeting application, Mint, a massive void was left in the personal finance space. While platforms like YNAB (You Need A Budget), Monarch Money, and Copilot have positioned themselves as premium, subscription-based budgeting tools, Empower remains the premier free option for investment-focused users. It serves as a reminder that the fintech market is bifurcating: consumers must either pay a subscription fee to protect their data privacy or accept a freemium model where their data serves as a pipeline for financial product sales.

2. Behavioral Finance and Real-Time Tracking

The psychological impact of real-time net worth tracking is a double-edged sword. On one hand, it encourages financial discipline by making progress visible. On the other hand, during periods of extreme market volatility—such as the 2020 pandemic-induced bear market—frequent dashboard checks can induce anxiety and lead to impulsive, emotionally driven trading decisions.

3. Fee Transparency as a Disruptive Force

By exposing the compounding damage of high mutual fund expense ratios and hidden advisory fees, Empower has contributed to the massive secular shift toward low-cost index funds and ETFs. When retail investors are presented with clear, visual evidence that minor fees can cost them hundreds of thousands of dollars in retirement, they are far more likely to fire high-cost managers and opt for passive investment strategies.

Ultimately, Empower represents the modern standard of financial aggregation. By putting institutional-grade diagnostic tools into the hands of ordinary consumers for free, it has democratized wealth planning, forcing traditional financial institutions to adapt or risk becoming obsolete.