As millions of retirement-age individuals transition from the wealth-accumulation phase to the decumulation phase of their financial lives, the reliance on digital retirement planners has reached an all-time high. These digital tools serve a dual purpose: for younger workers, they calculate necessary savings rates; for those on the cusp of retirement, they solve the complex equation of sustainable lifetime spending.

However, a critical challenge has emerged for self-directed investors. Not all digital retirement planners are created equal. Because these platforms utilize vastly different calculation engines, tax assumptions, and market simulation methodologies, their projections can diverge significantly. A landmark academic study analyzing five popular consumer retirement planning software packages revealed stark discrepancies in their ultimate outcomes. The study’s authors concluded with a vital warning: consumers must utilize multiple planning programs to stress-test their assumptions before implementing any lifetime financial strategy.

This journalistic investigation explores the mechanics of modern retirement software, traces the historical evolution of retirement calculations, evaluates the industry’s leading platforms, and examines the profound implications of algorithm-driven financial planning.

Chronology: The Evolution of Retirement Calculation Methodology

To understand the divergence in modern software outcomes, one must examine how the science of retirement planning has evolved over the past four decades.

[Pre-1990s: Static Rules] ──> [1990s: Deterministic Spreadsheets] ──> [2000s: Monte Carlo Simulations] ──> [Present: Dynamic, Hyper-Personalized Engines]

Phase 1: The Static Rule-of-Thumb Era (Pre-1990s)

Before the ubiquity of personal computers, retirement planning relied on static, linear assumptions. Financial planners and consumers used simple mathematical formulas, such as assuming a flat 8% annual market return and a static 3% inflation rate. In 1994, financial planner William Bengen published his seminal research on the "4% Rule," establishing a historical baseline for safe withdrawal rates. These calculations were entirely paper-based or completed on early spreadsheet software, completely ignoring the real-world volatility of market returns.

Phase 2: The Rise of Deterministic Online Calculators (Late 1990s – 2000s)

With the dawn of the consumer internet, financial institutions introduced basic, free web-based calculators. These tools were highly deterministic, requiring users to input simple variables: current age, target retirement age, current savings, and expected annual return. The software would project a straight, unbroken upward curve of wealth accumulation. The fundamental flaw of these first-generation digital tools was their inability to account for "sequence of returns risk"—the danger of market downturns occurring early in retirement, which can devastate a portfolio’s longevity even if the long-term average return remains high.

Phase 3: The Integration of Stochastic Modeling (2010s)

In response to the market crashes of 2000 and 2008, financial software developers integrated stochastic modeling, commonly known as Monte Carlo simulations. Rather than assuming a constant annual return, Monte Carlo engines run a user’s portfolio through 500 to 10,000 randomized market trials based on historical volatility and asset class behaviors. The output shifted from a single deterministic dollar figure to a probability score (e.g., "an 85% chance of portfolio survival"). Platforms like Personal Capital (now Empower) popularized this methodology for retail investors.

Today’s advanced platforms have moved beyond simple portfolio simulations. Modern software models complex, real-world variables year-by-year. This includes shifting tax brackets, Medicare Part B and D premiums, Social Security claiming optimization strategies, dynamic spending curves (such as the "retirement spending smile"), and multi-stage Roth IRA conversions. The calculation engines of today are highly sophisticated, multi-variable financial models that attempt to mirror the work of high-fee wealth management firms.

Supporting Data: A Comparative Analysis of Leading Platforms

To understand how these mathematical engines function in practice, we analyze the four leading retirement planning platforms currently available to retail consumers. Each takes a fundamentally different approach to solving the retirement puzzle.

Feature / Metric

Boldin (PlannerPlus)

ProjectionLab (Premium)

Empower

Maxifi (Premium)

Primary Calculation Engine

Cash-Flow / Tax Optimization

Historical & Monte Carlo

Monte Carlo (Asset-Linked)

Consumption Smoothing

Account Integration

Manual or Linked

Manual (Linked via Plaid)

Fully Automated Link

Manual Input

Social Security Optimizer

Yes (Highly Detailed)

Manual Inputs

Basic Assumptions

Yes (Proprietary Engine)

Roth Conversion Tool

Yes (Advanced)

Yes (Custom Rulesets)

No

Yes (Basic)

Pricing Structure

Free tier; $144/year

Free tier; $129/year or $799 lifetime

Free

$139 to $349/year

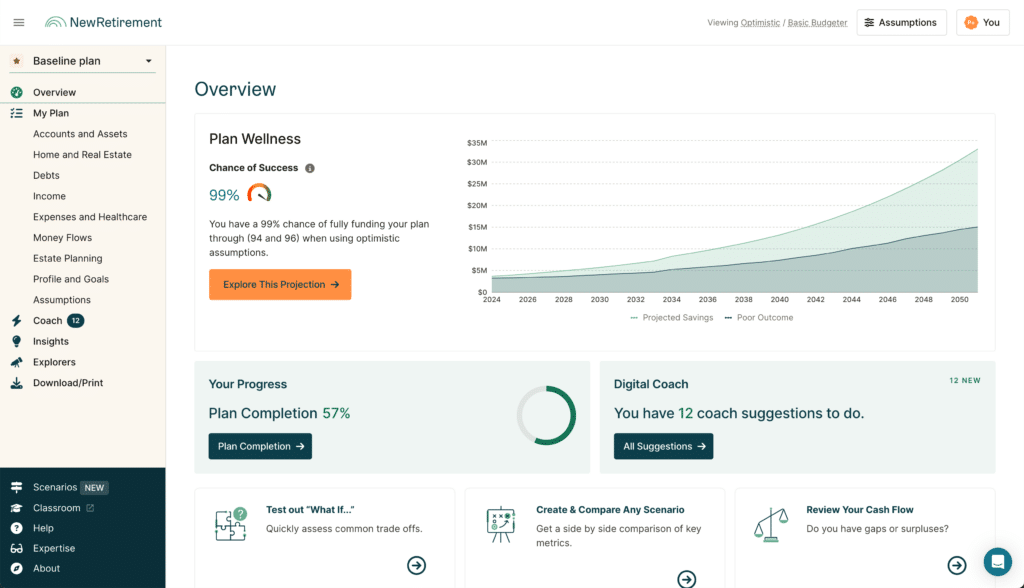

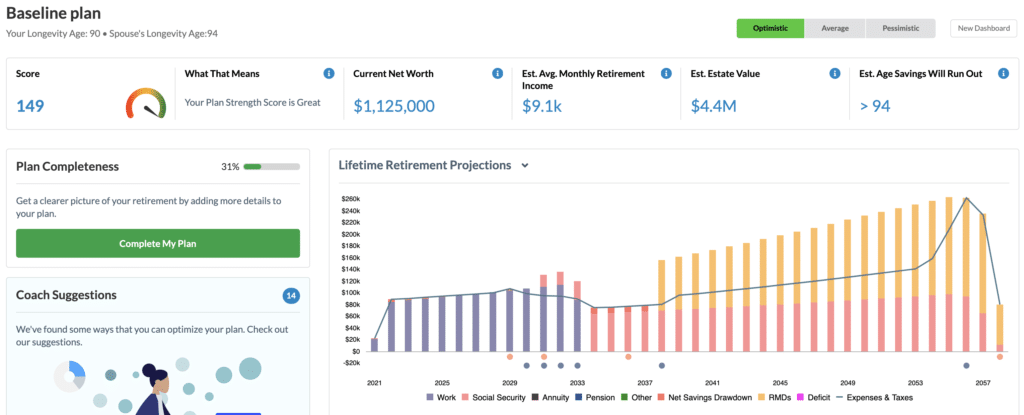

1. Boldin (Formerly New Retirement)

Highly detailed, cash-flow-centric planning optimized for tax mitigation.

Boldin is designed for investors who want to model every granular detail of their financial future. Rather than relying solely on asset values, Boldin builds a comprehensive, year-by-year cash-flow model.

Methodology: The software projects future income, expenses, and net worth on a monthly or annual basis. It allows users to schedule one-off financial events, such as the sale of a home, a part-time consulting period, or a late-career inheritance.

Tax Optimization: Boldin’s standout feature is its Roth IRA conversion modeling tool. It identifies years when a retiree is in a low tax bracket (the "retirement tax valley" between career end and the start of Required Minimum Distributions) and calculates exactly how much traditional pre-tax money should be converted to tax-free Roth accounts to minimize lifetime tax liability.

Pros: Exceptional granularity; highly sophisticated tax-bracket modeling; detailed Medicare and Social Security planning modules.

Cons: The platform does not natively run historical backtesting simulations, relying instead on deterministic cash-flow projections and standard Monte Carlo probabilities.

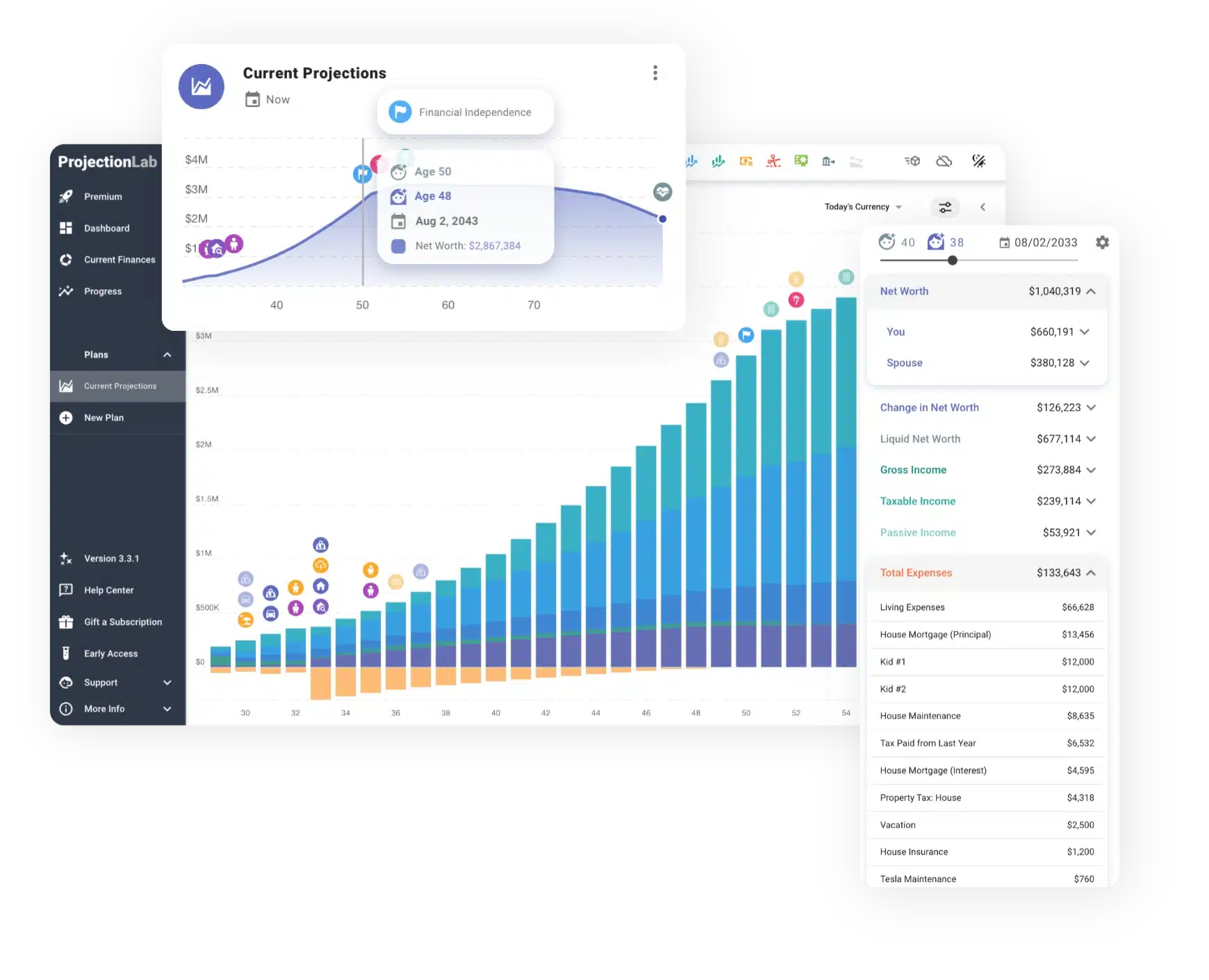

2. ProjectionLab

The modern, visual-first platform built for flexible "what-if" scenario testing.

Created by software engineer Kyle Nolan, ProjectionLab has quickly gained a reputation as the most flexible and visually stunning retirement planning tool on the market, particularly favored by the "FIRE" (Financial Independence, Retire Early) community.

Methodology: ProjectionLab allows users to create highly customized "what-if" scenarios. Users can establish complex, conditional rulesets (e.g., "If my portfolio drops by 20%, reduce discretionary travel spending by 15% and pause inflation adjustments for two years"). It supports both Monte Carlo simulations and raw historical backtesting, allowing users to see how their plan would have survived historical crises like the Great Depression or the 1970s stagflation.

Tax Optimization: While it features robust tax bracket estimation, it lacks some of the automated, step-by-step Social Security optimization wizards found in institutional tools.

Pros: Best-in-class user interface; highly modular and customizable; support for unique withdrawal strategies (e.g., Guyton-Klinger guardrails, Variable Percentage Withdrawal); available lifetime subscription option.

Cons: Lacks fully automated, guided wizards for complex tax maneuvers, requiring a slightly higher level of financial literacy from the user.

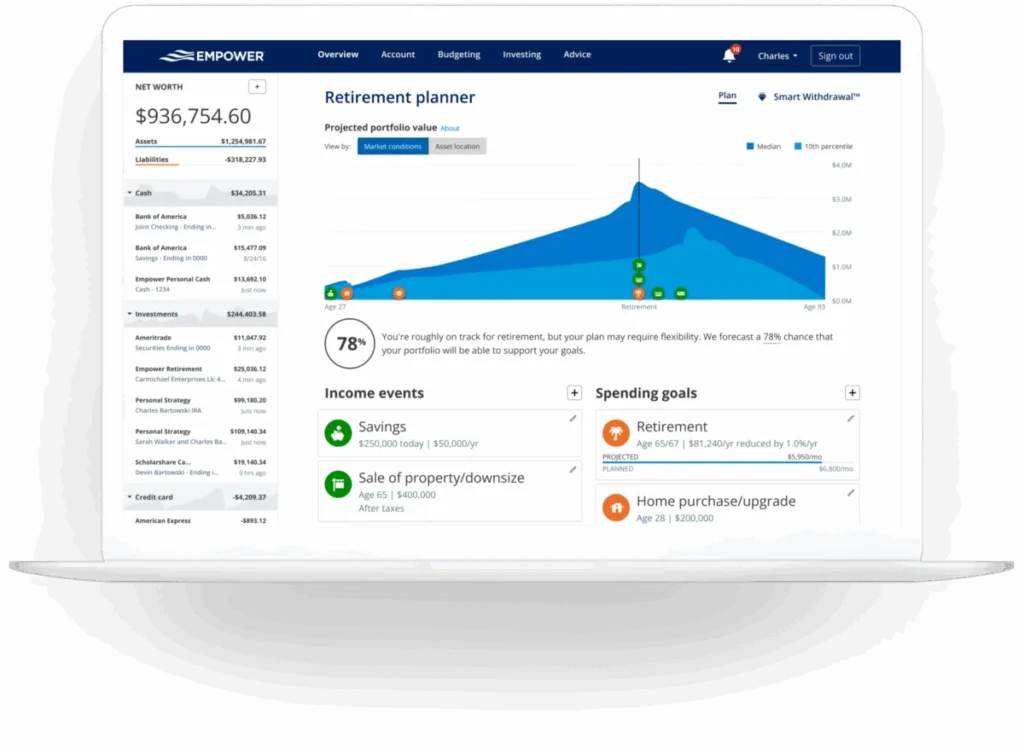

3. Empower

The industry standard for automated, asset-linked portfolio tracking and Monte Carlo modeling.

Empower (formerly Personal Capital) remains the most popular free retirement planner on the internet, functioning primarily as an automated aggregator of user accounts.

Methodology: Empower’s planner relies on real-time data. By linking a user’s actual 401(k), IRA, taxable brokerage, and bank accounts, the software analyzes the exact asset allocation (stocks, bonds, cash, alternatives) of the user’s current portfolio. It then runs these real-time allocations through a proprietary Monte Carlo engine.

Scenario Comparison: Users can easily build and compare multiple high-level scenarios side-by-side, such as retiring at age 62 versus age 67, or modeling a major real estate purchase.

Pros: Completely free; automatic daily account aggregation and asset allocation analysis; highly intuitive and easy to use.

Cons: Lacks the granular cash-flow adjustments, detailed tax-bracket modeling, and Roth conversion planning found in dedicated paid software packages.

4. Maxifi

An academic-grade tool built on the economic theory of consumption smoothing.

Maxifi, designed by Boston University economics professor Laurence Kotlikoff, approaches retirement planning from an entirely different intellectual perspective than its competitors.

Methodology: Rather than asking users how much they want to spend in retirement and calculating their probability of success, Maxifi uses an economic concept called consumption smoothing. The software analyzes a household’s total lifetime resources (current assets, future earnings, pensions, Social Security) and calculates the exact, inflation-adjusted amount the household can spend every single year of their remaining lives to ensure their standard of living remains perfectly flat—neither rising nor falling—until age 100.

Complexity: The software performs incredibly sophisticated, iterative calculations behind the scenes. Adjusting a single variable can trigger a complete recalculation of a lifetime spending plan.

Pros: Prevents retirees from over-saving and living too frugally; exceptional mathematical rigor; highly objective economic foundations.

Cons: It features a steep learning curve and a less intuitive interface. The core assumption of consumption smoothing—that individuals want to spend the exact same amount of money at age 95 as they do at age 65—runs counter to real-world spending data, which shows that retirement spending typically declines significantly as retirees age.

Official Responses and Developer Philosophies

To understand the core philosophies driving these tools, we look to the statements and design choices of their creators and the economic experts behind them.

Kyle Nolan, Founder of ProjectionLab:

Nolan developed the platform out of personal frustration with the rigid, institutional assumptions of legacy retirement calculators. His goal was to build a tool that treats financial planning as a sandbox rather than a spreadsheet:

"Traditional calculators force you into a box. They assume you work a standard W-2 job until 65 and then slowly spend down your assets. Modern savers, especially the early retirement community, need a tool that can model fluid lifepaths—sabbaticals, career pivots, real estate investing, and dynamic spending adjustments."

Laurence Kotlikoff, Creator of Maxifi:

Kotlikoff has long criticized traditional retirement planning software for its reliance on arbitrary "replacement rates" (the idea that you need 80% of your pre-retirement income in retirement). He argues that this methodology is economically incoherent:

"Most retirement planners give people bad advice. They tell them to save a random percentage of their income, which often leads to severe under-saving or unnecessary deprivation during their working years. Consumption smoothing is the only scientifically sound way to maximize lifetime living standards without running out of money."

Steve Chen, Founder of Boldin:

Chen’s mission has centered on democratizing institutional-grade financial advice, allowing consumers to bypass the traditional 1% assets-under-management (AUM) fee charged by human advisors:

"The wealthy have always had access to sophisticated wealth-modeling software through their personal financial advisors. Our goal is to put those exact same powerful cash-flow engines, tax-optimization algorithms, and healthcare-cost estimators directly into the hands of individual consumers at a fraction of the cost."

Implications: The Future of Self-Directed Financial Planning

The rapid advancement of consumer-facing financial technology has profound implications for individual investors, the financial advisory industry, and broader retirement security.

┌──────────────────────────────┐

│ Traditional 1% AUM Fee │

└──────────────┬───────────────┘

│ Disrupted by

▼

┌─────────────────────────────────────────────────────────────────┐

│ Hybrid Self-Directed Planning Model │

│ │

│ [Dynamic Software Projections] + [Hourly Fiduciary Review] │

│ (Tax, Cash Flow, Monte Carlo) (Validation & Peace of Mind)│

└─────────────────────────────────────────────────────────────────┘

The Risk of Algorithmic Overconfidence

The primary danger of highly sophisticated retirement planners is the "Garbage In, Garbage Out" (GIGO) phenomenon. Because these tools present beautifully rendered, highly detailed charts and precise success percentages, users may develop a false sense of certainty. A user who inputs an unrealistically low estimate for future healthcare inflation or an overly optimistic long-term market return will receive a highly precise, yet fundamentally flawed, projection of financial success.

The Disruption of the Financial Advisory Industry

Historically, financial advisors justified their fees by running proprietary financial plans for clients using expensive, advisor-only software like eMoney or RightCapital. Today, tools like Boldin and ProjectionLab offer retail consumers 95% of the computational power of professional platforms for a nominal annual fee. This shift is forcing the financial advisory industry to pivot away from simple portfolio management and toward behavioral coaching, estate planning, and complex tax mitigation.

The Rise of the Hybrid Planning Model

Rather than completely replacing human advisors, modern software is fostering a hybrid approach to financial planning. Savvy consumers increasingly utilize tools like Boldin or ProjectionLab to build their baseline retirement models, map out their Roth conversion strategies, and optimize their Social Security claiming ages. They then take these digital models to an hourly, fee-only fiduciary financial planner for professional validation. This hybrid model saves the consumer thousands of dollars in ongoing asset-management fees while retaining the peace of mind that comes from a professional human review.

Frequently Asked Questions

What is the fundamental difference between a basic retirement calculator and advanced retirement planning software?

A basic retirement calculator is deterministic, utilizing a few static inputs (savings, rate of return, years to retirement) to generate a single, linear projection. It ignores market volatility, tax bracket changes, and sequence of returns risk.

In contrast, advanced retirement planning software is dynamic. It models year-by-year cash flows, integrates stochastic modeling (Monte Carlo simulations) or historical backtesting, and optimizes complex financial strategies such as Roth IRA conversions, Social Security claiming ages, and shifting Medicare premiums.

Why do different retirement planning tools produce different results?

Different tools utilize different mathematical engines and baseline assumptions. For example:

Empower bases its projections on Monte Carlo simulations of your current linked asset allocation.

Boldin relies on a highly detailed, user-defined cash-flow model.

Maxifi ignores probability percentages entirely, using consumption-smoothing algorithms to calculate a flat lifetime spending rate.

Additionally, variations in how platforms estimate future tax brackets, state taxes, and inflation rates can lead to divergent outcomes.

Is it safe to link my actual financial accounts to these software tools?

Most modern financial platforms, including Empower and ProjectionLab, use secure, read-only third-party aggregators like Plaid or Yodlee to link accounts. These services use bank-grade 256-bit encryption. The software itself never has access to your actual login credentials or the ability to move, withdraw, or trade funds within your accounts. For users who remain uncomfortable linking accounts, platforms like Boldin and ProjectionLab offer fully functional manual entry options.