Redefining Riches: America’s Exploding Millionaire Class and the Shifting Sands of Wealth

FOR IMMEDIATE RELEASE

New York, NY – July 3, 2026 – The persistent fascination with wealth metrics has once again been stirred by the release of the Capgemini 2026 Wealth Report, which, as of 2025, highlights a global surge in millionaires. However, a deeper dive into the figures for the United States reveals a nuanced landscape, sparking a crucial debate among financial experts and the public alike: In 2026, does a million dollars still signify "rich" in the United States?

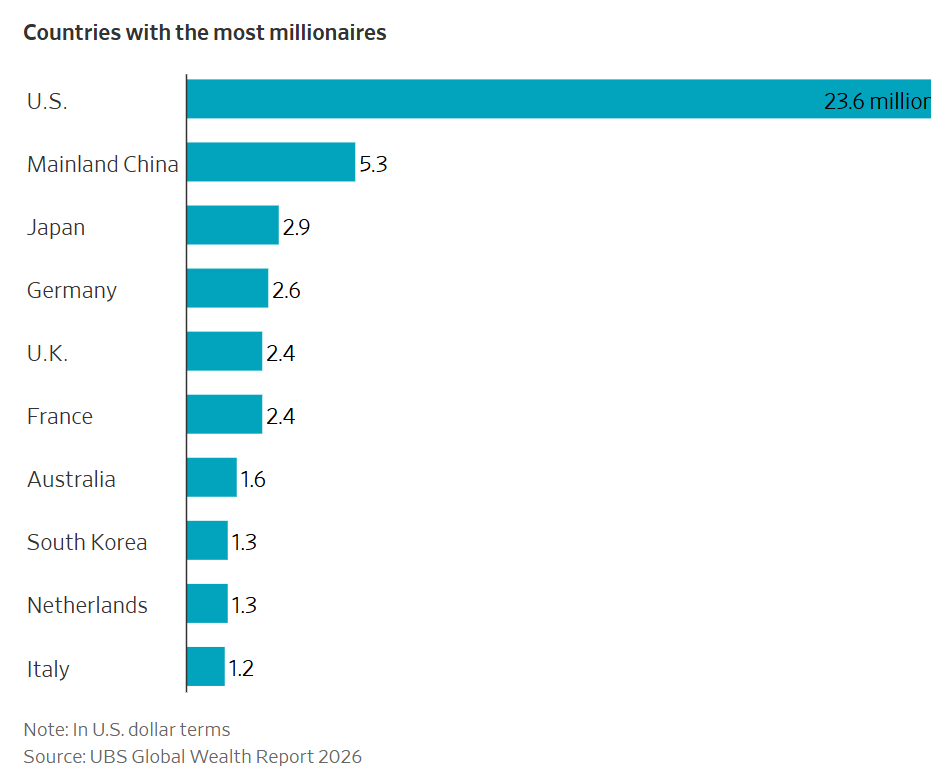

The report’s headline figures, indicating 25.3 million millionaires worldwide, present a formidable picture of global affluence. For the U.S., Capgemini identifies approximately 8.73 million individuals holding $1 million or more in investable assets. This specific qualifier – "investable assets" – is critical, as it deliberately excludes a significant component of American wealth: home equity. This distinction immediately sets the stage for a broader discussion, contrasting sharply with other recent analyses that paint an even more expansive picture of American millionaire status.

Financial commentator Ben Carlson, known for his incisive analyses on personal finance, recently revisited this very question, prompted by a reader’s query. His previous blog post, "House Rich Millionaires" from late 2025, cited reports suggesting that as many as one in five Americans now qualify as millionaires when their primary residence is factored into their net worth. The discrepancy between these figures – 8.73 million versus potentially 24 million households – underscores the complex and often subjective nature of defining wealth in contemporary America.

The Shifting Landscape of American Wealth

The concept of a "millionaire" has long been a benchmark of significant financial achievement. For generations, accumulating a million dollars represented an almost unattainable dream for many, synonymous with financial independence and a life of luxury. Yet, as the economy evolves and inflation erodes purchasing power, the symbolic weight of that round number has begun to shift.

Over the past decade, and particularly in the last eight years, the United States has witnessed an unprecedented expansion of its millionaire class. This surge is not merely an incremental increase but a profound demographic shift, driven by a confluence of factors including robust equity markets, sustained real estate appreciation, and a period of relatively low interest rates that encouraged investment and asset growth. The post-pandemic economic recovery, characterized by surging asset values, further accelerated this trend, bringing millions more into the millionaire bracket, at least on paper. This rapid ascension challenges traditional perceptions of wealth, forcing a re-evaluation of what it truly means to be "rich" in the modern era.

Dissecting the Numbers: Investable Assets vs. Total Net Worth

Understanding the true scope of wealth in America requires a careful examination of how "millionaire" status is defined and measured across various reports. The distinctions are not merely academic; they fundamentally alter our perception of financial well-being.

Capgemini’s Core Findings: Focus on Liquid Wealth

The Capgemini 2026 Wealth Report, a highly respected annual barometer of global wealth, adopts a stringent definition for its "High Net Worth Individual" (HNWI) category. It focuses exclusively on individuals holding $1 million or more in investable assets. These assets typically include publicly traded equities, bonds, mutual funds, exchange-traded funds (ETFs), cash, and other liquid financial instruments. Critically, this definition excludes primary residences, collectibles, and consumer durables. According to this methodology, the United States is home to approximately 8.73 million such millionaires. This figure represents a segment of the population with substantial liquid wealth, capable of being deployed for investment or consumption without needing to sell their primary home. Globally, the report highlighted 25.3 million individuals meeting this criterion, underscoring the US’s significant contribution to the world’s investable wealth.

The Home Equity Multiplier: A Game Changer

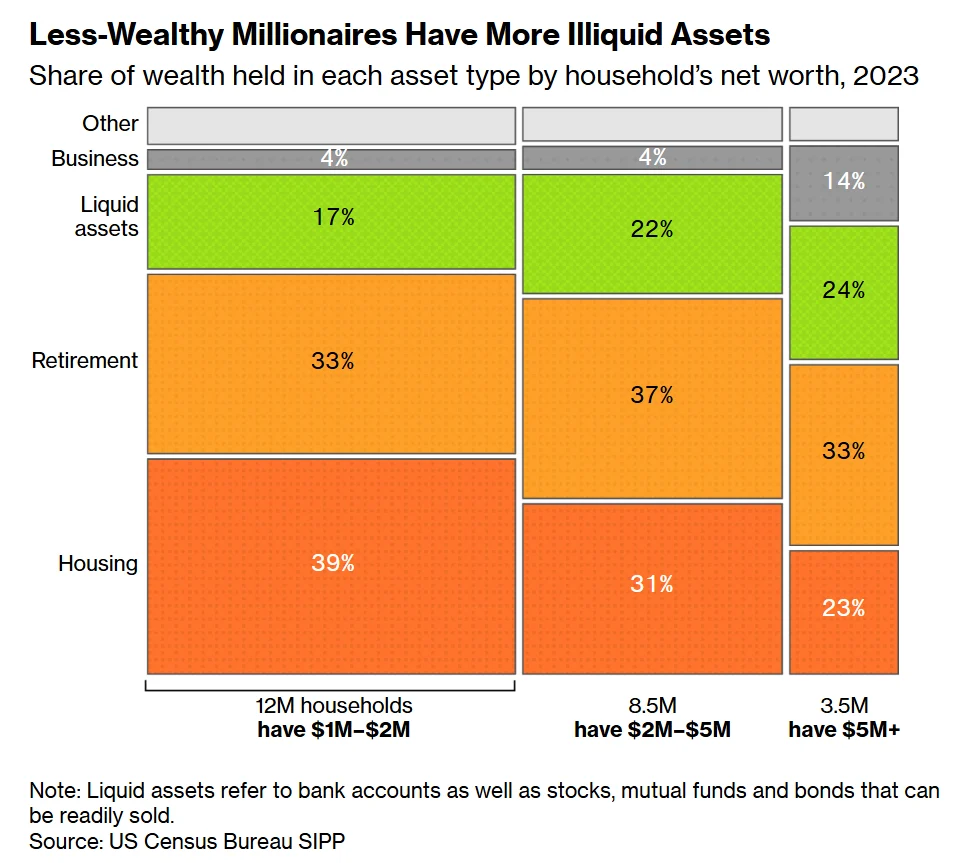

The omission of home equity from Capgemini’s calculation is a crucial point of divergence from other wealth reports. The sheer volume of housing wealth in America right now—an estimated $35 trillion—demonstrates its profound impact on total net worth. When this substantial asset is included, the number of millionaires in the United States experiences a dramatic leap.

Data from financial services firm UBS, for instance, paints a broader picture. Their analysis, widely cited by publications like The Wall Street Journal, reveals nearly 24 million millionaire households in America. This figure, which incorporates the value of primary residences, positions the United States as the undisputed leader in millionaire households globally, far surpassing any other nation. This indicates that while a significant portion of American wealth is tied up in housing, it nevertheless contributes to a household’s overall financial standing, providing security and, in many cases, a substantial equity reserve.

Further corroborating this expanded view, a Bloomberg report referenced by Ben Carlson also indicated approximately 24 million millionaire households in America. This means roughly one in five households now possess a net worth of $1 million or more. What’s even more striking is the pace of this growth: an estimated one-third of this group has attained millionaire status within just the past eight years, highlighting a period of exceptional asset appreciation.

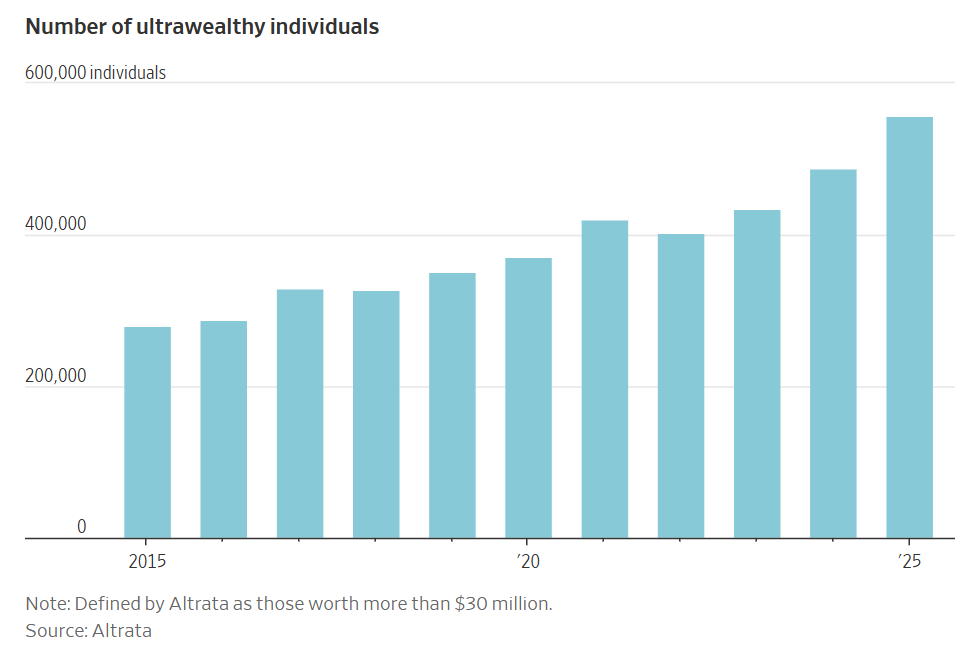

The Ultra-Wealthy: A Class Apart

Beyond the broad category of millionaires, the upper echelons of wealth have also seen remarkable growth. The Wall Street Journal has consistently reported on the burgeoning ranks of the ultra-wealthy – individuals possessing $30 million or more in net worth. This segment has grown considerably in recent years, reflecting not just a general rise in asset values but also a concentration of wealth at the very top. The expansion of this exclusive group underscores the increasing stratification of wealth, where the definition of "rich" extends far beyond the initial million-dollar threshold for an elite few.

Globally, having $1 million in liquid net worth still places an individual in the top 1% of the world’s population. Within the United States, it positions a household in the 88th percentile. These statistics provide an important comparative lens, reminding us that despite the domestic debates, a million dollars remains a substantial sum on a global scale.

Expert Perspectives on the Millionaire Threshold

The numerical data, while compelling, only tells part of the story. The true meaning of "rich" is not purely a function of digits in a bank account; it is deeply intertwined with personal circumstances, aspirations, and societal context. Financial commentators and experts offer varied insights into this complex question.

Ben Carlson, in his analysis, acknowledges his "sucker for these millionaire studies" – a testament to the enduring public interest in wealth accumulation. He delves beyond the raw figures to explore the qualitative factors that truly define affluence. His key takeaway is that while a million dollars is undeniably a lot of money, whether it makes one "rich" is entirely dependent on a series of subjective variables.

The Subjectivity of "Rich": More Than Just a Number

Carlson, drawing on common sense and expert observations, outlines five crucial factors that dictate whether a million dollars translates into a "rich" lifestyle:

-

Geographic Location: The purchasing power of a million dollars varies dramatically across the United States. In a major metropolitan hub like Manhattan or San Francisco, a million dollars might barely cover a modest apartment and a few years of living expenses. Property values, cost of living, and local tax rates in these areas can quickly diminish the perceived wealth. Conversely, in a lower-cost-of-living city such as Topeka, Kansas, or Des Moines, Iowa, a million dollars could afford a spacious home, comfortable retirement, and significantly extend one’s financial runway. The local economic landscape is a primary determinant of a millionaire’s actual lifestyle.

-

Life Stage and Age: The age at which one accumulates a million dollars is paramount. A 40-year-old with $1 million has the significant advantage of decades of potential compounding growth ahead, offering ample time for that sum to multiply into several million by retirement. This early accumulation provides immense financial flexibility and security. In contrast, a 60-year-old with $1 million, while still financially sound, has a much shorter time horizon for growth and may need the funds to cover immediate retirement expenses, making it feel less "rich" in terms of long-term security. The runway for investment and consumption is drastically different.

-

"Burn Rate" and Lifestyle Inflation: Perhaps the most insightful perspective comes from Scott Galloway, who, in his book The Algebra of Happiness, offers a poignant definition of "richness": "having passive income greater than your burn." This means true wealth isn’t about the size of one’s assets, but the ability to cover one’s expenses through passive income, without actively working. Galloway illustrates this with a stark contrast: his father, receiving $50,000 annually from dividends, pension, and Social Security while spending $40,000, is "rich" because his passive income exceeds his "burn rate." Conversely, Galloway describes friends earning $1 million to $3 million annually, yet spending most, if not all, of it on Manhattan private schools, Hamptons homes, ex-spousal support, and lavish lifestyles. These individuals, despite their high incomes, are "poor" by his definition because their expenses outstrip their earnings, leaving them perpetually on the treadmill. This concept highlights the insidious nature of lifestyle inflation, where rising income often leads to rising expenses, trapping individuals in a cycle where they feel anything but rich.

-

Social Comparison and Peer Groups: The human tendency to compare oneself to others significantly impacts the perception of wealth. Living in an affluent neighborhood or working in a high-earning profession where many peers possess multi-million-dollar net worths can make a single millionaire feel relatively less wealthy. This constant exposure to greater affluence can distort one’s own sense of financial accomplishment, leading to a feeling of not being "rich enough," even when objectively well-off. The "keeping up with the Joneses" phenomenon is particularly potent in wealth perception.

-

Personal Definition of a "Rich Life": Ultimately, the most subjective yet most important factor is an individual’s personal definition of a "rich life." For some, it might mean boundless luxury and material possessions. For others, it could be the freedom to pursue passions, spend time with family, contribute to charity, or simply live without financial stress. A rich life might prioritize experiences over possessions, or time over money. People with significant net worth might find themselves miserable due to overwhelming commitments or lack of personal fulfillment, while others with modest means might experience profound richness through strong relationships, community involvement, or meaningful work. Round numbers, in this context, often fail to tell the whole story.

Implications and The Future of Wealth

The ongoing debate about what constitutes "rich" in 2026 carries significant implications, not only for individuals but also for broader economic and societal discussions.

The Erosion of the "Millionaire" Status Symbol

While statistically, a millionaire is still a rare and wealthy individual, the sheer increase in their numbers, coupled with inflation, has arguably diminished the iconic status once associated with the term. A million dollars today does not command the same purchasing power it did fifty, or even twenty, years ago. What once bought a sprawling estate and a life of leisure might now barely cover a comfortable retirement in a moderately priced area. This erosion means that while the numerical goal of $1 million remains a popular aspiration, its practical implications for lifestyle and freedom have evolved.

Wealth Inequality and Societal Dynamics

The rapid growth in the number of millionaires, particularly the ultra-wealthy, also brings to the forefront discussions about wealth inequality. While a growing middle class of millionaires might suggest broader prosperity, the simultaneous concentration of immense wealth at the very top raises questions about economic distribution and opportunity. This trend can fuel debates around taxation, social mobility, and the fairness of economic systems.

Financial Planning in a New Era

For financial advisors and individuals alike, these shifting definitions underscore the importance of personalized financial planning over arbitrary milestones. Instead of fixating on a round number like $1 million, the focus should be on achieving financial independence tailored to individual needs and aspirations. This involves understanding one’s "burn rate," defining personal values, and creating a plan that ensures passive income can cover desired expenses, regardless of the headline net worth figure. The goal shifts from merely having a million dollars to what that million dollars can do for one’s specific life goals.

In conclusion, while various reports consistently demonstrate a robust and expanding millionaire class in the United States, the question of whether $1 million still makes one "rich" is far from settled. It is a nuanced query, subject to geographical realities, life stages, personal spending habits, social comparisons, and ultimately, an individual’s unique definition of a fulfilling life. As Ben Carlson aptly notes, there are people with "boatloads of money who aren’t actually rich," and conversely, those "who wouldn’t be considered wealthy in net worth terms but have a rich life in other ways." The true measure of wealth, it seems, remains profoundly personal.

Further Resources:

For a deeper dive into these discussions, readers are encouraged to explore Ben Carlson’s previous analysis, "House Rich Millionaires," and watch the latest episode of "Ask the Compound," where Carlson and Bill Sweet celebrate the 4th of July by answering audience questions on saving priorities, small business finances, real estate allocation, and stock sales for home purchases.