Reassessing Retirement Portfolios: The Enduring Debate on Bond Allocation

Introduction

A recent article in The Wall Street Journal, provocatively titled “You’re Probably Overinvested in Bonds,” has ignited considerable debate among financial advisors and retirees alike, challenging long-held tenets of retirement planning. The piece, authored by Mr. Posen, suggests that a significant portion of affluent Americans may be foregoing substantial market upside by maintaining traditional allocations to fixed-income assets. This perspective has prompted numerous inquiries from readers seeking clarity on their own investment strategies, particularly regarding the delicate balance between growth and capital preservation in their later years.

The crux of the Wall Street Journal’s argument targets two large demographic groups: the estimated six to seven million Americans with over $1 million in investable assets, and other households possessing more than $100,000 in investable assets whose non-investment income comfortably covers their cost of living. For these individuals, Mr. Posen contends, the conventional wisdom advocating for a substantial bond allocation may be outdated, leading to missed opportunities for wealth accumulation.

This contentious viewpoint resonates particularly with retirees like one reader, a couple in their early seventies, who have historically maintained an aggressive 80/20 stock-to-cash split, eschewing bonds entirely. Their situation perfectly encapsulates the dilemma many face: balancing the desire for growth with the imperative of financial security during a period of life with limited income-generating capacity. This article delves into the merits and risks of such aggressive strategies, drawing upon historical market data and expert analysis to provide a comprehensive understanding of the implications for retirement portfolios.

The Core Debate: Challenging Traditional Allocations

The discussion around fixed-income allocation in retirement is not new, but Mr. Posen’s article injects a fresh, albeit controversial, perspective. Traditionally, a balanced portfolio, often exemplified by the 60/40 stock-to-bond split, has been the bedrock of retirement planning. This allocation aims to provide a reasonable return while mitigating risk, with bonds serving as a buffer against stock market volatility and a source of stable income. However, the Wall Street Journal article posits that such a conservative approach may sacrifice too much potential upside, especially for those with substantial assets or secure non-investment income.

The WSJ’s Provocative Stance

Mr. Posen’s central thesis suggests that a more aggressive equity allocation, such as a 90/10 portfolio (90% stocks, 10% cash/bonds), aligns better with the long-term historical performance of the stock market. The underlying premise is simple: over extended periods, equities have consistently outperformed bonds, delivering superior returns. For investors not reliant on immediate investment income for living expenses, or those with significant financial cushions, foregoing a larger bond allocation could unlock substantial additional wealth.

The article acknowledges that bonds still serve a crucial role for certain segments of the population. Those who are retired and subsist primarily on investment income, or individuals who would be compelled to liquidate a significant portion of their investments to cover living expenses during a downturn, are still advised to hold a substantial position in high-quality bonds. This distinction is critical, highlighting that the "overinvested" critique is not universal but targeted at specific affluent demographics perceived as having greater capacity for equity risk.

However, the very nature of an aggressive equity strategy inherently involves greater exposure to market fluctuations. Mr. Posen addresses this by stating, "Stock declines are relatively infrequent and typically are followed by increases—a recurring pattern over the past 60 years." While this statement holds a kernel of truth on average, a deeper dive into historical market volatility reveals a more nuanced and potentially challenging reality for retirees.

Historical Market Volatility: A Chronological Examination

To properly evaluate the Wall Street Journal’s assertion and its implications for retirees, a detailed examination of historical stock market behavior is essential. While the stock market’s long-term upward trend is undeniable, the path to those returns is often fraught with significant, albeit temporary, downturns.

Understanding Stock Market Corrections

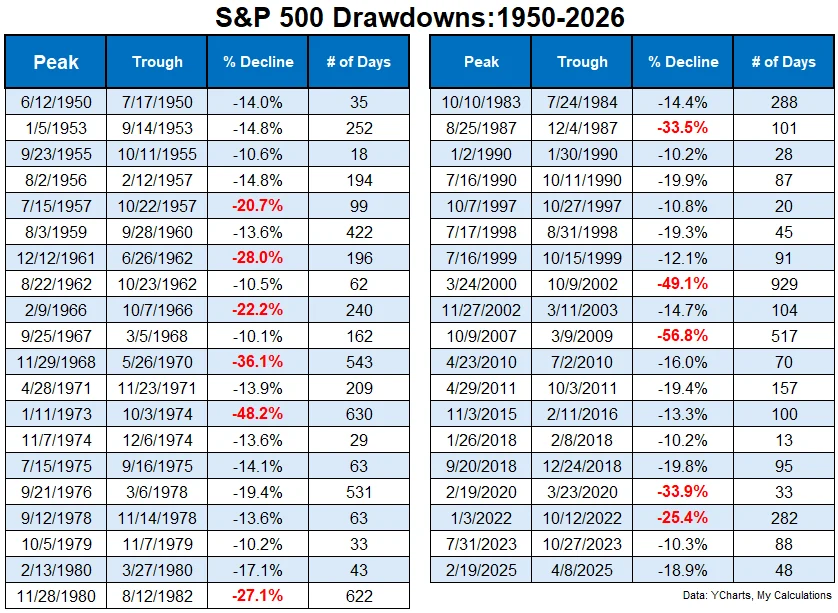

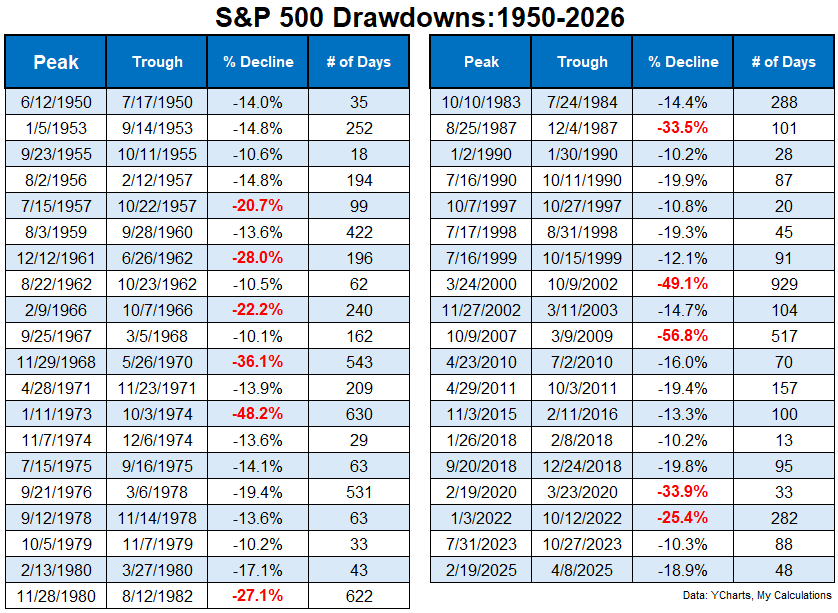

An analysis of the S&P 500 index since 1950 reveals a pattern of regular, double-digit corrections. By historical count, there have been 39 such corrections over the past 70-plus years, averaging roughly one significant downturn every two years. This frequency challenges the notion that stock declines are "relatively infrequent."

The average drawdown experienced during these corrections has been approximately -20%. From the market’s peak to its trough, these declines typically span around 193 days. While a 20% drop might not sound catastrophic in isolation, and a recovery period of less than a year for the market bottom to be reached might seem manageable, these figures represent only a partial picture for investors, especially those in retirement.

Crucially, the time it takes for a portfolio to recover its previous high after a correction is often significantly longer than the time it takes to hit the bottom. On average, investors have had to wait approximately 306 additional days to breakeven, meaning their portfolio value returned to its pre-correction level. Combining the peak-to-trough decline with the recovery period, an investor could realistically face nearly 500 days—over a year and a quarter—in a state of being "underwater," where their investments are worth less than their previous high. This prolonged period of stagnant or declining value can be particularly challenging for retirees who are actively drawing income from their portfolios.

The Graver Threat: Bear Markets

While corrections are common, the more severe and prolonged downturns known as bear markets pose a far greater risk, particularly for retirees. Bear markets are characterized by a decline of 20% or more from recent highs and often involve significantly steeper drawdowns and longer recovery periods than average corrections.

Since 1950, the U.S. stock market has experienced several notable bear markets, each presenting unique challenges:

- The 1973-74 Bear Market: This period saw a substantial decline, with investors waiting nearly six years to recover their losses and reach new highs. For a retiree relying on their portfolio, six years of underperformance and capital erosion could have devastating consequences.

- The Dot-Com Bust (2000-2002): Following the tech bubble’s burst, the market took approximately four-and-a-half years from its bottom to regain its previous peak. This extended recovery period tested the patience and financial resilience of many investors.

- The Great Financial Crisis (2007-2009): The market peak in the fall of 2007 was not breached again until 2013, illustrating another prolonged recovery phase of roughly six years.

These examples starkly contrast with rapid recoveries, such as the COVID-19 crash in early 2020, which saw the market rebound to new highs in less than 150 days. While the speed of modern markets might suggest shorter downturns in the future, relying solely on this possibility is a significant gamble for a retiree. The average recovery time for bear markets is measured in years, not months, presenting a fundamental challenge to the aggressive equity strategy proposed for retirees.

The Retiree’s Dilemma: Navigating Risk with Limited Margin for Error

The historical data underscores a critical distinction between accumulating wealth and preserving it during retirement. For investors in their working years, market downturns, even severe bear markets, can be viewed as opportunities. Regular contributions allow them to buy shares at lower prices, leveraging the power of dollar-cost averaging to build a larger portfolio when the market eventually recovers. However, the dynamics shift dramatically for those in retirement.

The Imperative of a Back-up Plan

For retirees, the "margin of safety" significantly shrinks. There is no longer a regular paycheck to fund new investments during a market dip. Instead, retirees are typically drawing down their portfolios to cover living expenses. This creates a critical vulnerability: if a retiree is heavily invested in stocks and a prolonged bear market strikes, they may be forced to sell assets at a loss to generate necessary income. This phenomenon, known as "sequence of returns risk," can severely impair the longevity of a retirement portfolio, especially if significant downturns occur early in retirement.

An aggressive 90/10 stock-to-cash/bond allocation, while potentially lucrative in favorable market conditions, carries substantial risk if a robust back-up plan is not in place. The 10% cash component, intended as a buffer, could quickly be depleted during an extended drawdown. Once that "dry powder" is gone, the retiree is faced with the agonizing decision of selling depreciated stocks, locking in losses and further eroding their capital base. This forces them to effectively "replenish" their cash allocation by selling low, a cardinal sin in investing.

Psychological and Financial Strain

Beyond the purely financial implications, the psychological toll of prolonged market drawdowns cannot be overstated. Watching a significant portion of one’s life savings diminish, coupled with the uncertainty of when a recovery might occur, can lead to immense stress and poor decision-making. For a retiree, who has spent decades building their nest egg, the idea of waiting six years or more to breakeven, while simultaneously drawing down funds, can be terrifying and lead to abandoning a well-conceived plan at the worst possible time.

The original article’s author agrees with Mr. Posen on one crucial point: retirees likely need to embrace some equity risk. With increasing longevity, many individuals can expect to live 20 to 30 years or more in retirement. Over such an extended period, inflation can significantly erode purchasing power, making it essential for a portion of the portfolio to continue growing. However, the disagreement lies in the degree of risk and the necessary safeguards.

Expert Commentary and Nuance: A Balanced Perspective

While acknowledging the potential for higher returns with an aggressive equity allocation, expert analysis emphasizes the critical need for a nuanced approach to retirement planning, particularly concerning risk management. The consensus among many financial planners leans towards a more cautious strategy for retirees compared to accumulators.

The primary counter-argument to Mr. Posen’s aggressive stance is not that stocks are inherently bad for retirees, but rather that a high concentration in equities without sufficient liquidity or a robust spending plan is a recipe for potential disaster. For those still contributing to their portfolios, lengthy drawdowns are indeed opportunities. But for those drawing income, they are existential threats.

The Importance of "Dry Powder"

A well-structured retirement portfolio often includes a substantial allocation to highly liquid, low-volatility assets—be it cash, short-term bonds, or other fixed-income instruments. This "dry powder" serves multiple critical functions:

- Income Generation During Downturns: It provides a source of funds for living expenses, allowing the retiree to avoid selling stocks when their value is depressed. This is the primary defense against sequence of returns risk.

- Psychological Comfort: Knowing there are readily available funds for several years of expenses can alleviate anxiety during volatile market periods, helping retirees stick to their long-term investment plan.

- Opportunity to Buy Low: In some cases, a well-funded cash reserve can even enable retirees to selectively buy more stocks during significant market dips, turning a crisis into an opportunity, much like younger investors.

Without a sufficient fixed-income position, a retiree loses the ability to weather extended downturns gracefully. The temptation, and often the necessity, to sell depreciated equities becomes overwhelming, potentially converting temporary paper losses into permanent capital destruction.

Balancing Risk and Longevity

The need for retirees to take some equity risk to combat inflation and ensure their money lasts through a potentially multi-decade retirement is widely accepted. However, this risk must be calibrated against the individual’s specific financial situation, spending habits, and risk tolerance. An outsized allocation to stocks, without a meticulous understanding and control over spending, can become exceedingly dangerous.

The author of the initial commentary emphasizes that while one might leave "money on the table" by taking less risk, the consequences of taking too much risk at the wrong time can be far more severe. Retirement planning is not merely about maximizing returns; it’s about optimizing the probability of financial security throughout one’s remaining life. As the expert poignantly notes, "you only get one shot at it." Unlike younger investors who can recover from significant setbacks over decades, retirees have a much shorter time horizon to make up for substantial losses.

Implications for Retirement Planning: Beyond Simple Rules

The debate sparked by the Wall Street Journal article highlights the complex, highly individualized nature of retirement planning. There are no universal rules that apply to every retiree, and a blanket recommendation for aggressive equity allocation, even for the affluent, overlooks crucial factors.

The Role of Spending and Financial Flexibility

A key implication is the paramount importance of a retiree’s spending habits and their flexibility. For those with highly discretionary spending that can be significantly curtailed during a market downturn, a higher equity allocation might be more feasible. However, for retirees with high fixed expenses and limited flexibility, a more conservative approach with a robust fixed-income buffer is almost certainly warranted. A "really good handle on your spending" is not just a recommendation; it’s a prerequisite for any aggressive equity strategy in retirement.

Diversification Beyond Stocks and Bonds

While the core debate focuses on stocks versus bonds, effective retirement planning often involves a broader perspective on diversification. This can include:

- Cash Buckets: Segmenting cash into different "buckets" for immediate needs (1-2 years), short-term needs (3-5 years), and emergency funds.

- Income Annuities: For a portion of the portfolio, annuities can provide guaranteed income streams, reducing reliance on volatile market returns for essential living expenses.

- Real Estate: While not explicitly discussed in the original text, paid-off housing can offer stability and reduce living costs, indirectly supporting a more aggressive investment portfolio.

The "4 Year Rule For Retirement Spending" referenced in the original text is another crucial concept that underpins responsible drawdown strategies. It suggests having enough liquid assets to cover 4 years of living expenses, allowing equity portions of the portfolio to recover during downturns without forced selling. This directly contradicts the spirit of an aggressive, minimal bond/cash approach.

Conclusion

The Wall Street Journal’s article serves as a valuable catalyst for discussion, prompting retirees and financial professionals to critically re-evaluate conventional wisdom regarding bond allocations. While the historical outperformance of stocks over the long term is undeniable, and the need for retirees to take some equity risk to combat inflation and ensure longevity is valid, the blanket recommendation for an aggressive, bond-light portfolio, even for the affluent, warrants caution.

Historical data clearly demonstrates that market corrections and bear markets are not infrequent anomalies but recurring features of the investment landscape. For retirees, who lack the income-generating capacity of their working years and operate within a shorter time horizon, the financial and psychological impacts of prolonged drawdowns can be severe, jeopardizing their financial security.

Ultimately, the decision of how much to allocate to bonds in retirement is deeply personal. It requires a meticulous assessment of individual circumstances, including net worth, non-investment income, spending flexibility, and a realistic understanding of one’s ability to withstand significant market volatility without panic-selling. While foregoing a traditional bond allocation might indeed leave "money on the table" in a perpetually rising market, the potential for catastrophic portfolio damage during an "outlier bear market" represents a risk many retirees cannot afford to take. In the complex landscape of retirement planning, prudence, a robust back-up plan, and a firm grasp on personal finances remain paramount.