Raising Financially Literate Children: A Masterclass in Real-World Economics

In an era where digital transactions have made the concept of money increasingly abstract, parents are finding it harder than ever to teach the tangible value of a dollar. For one Vermont-based family—the Frugalwoods—the solution to this modern parenting dilemma lies not in high-level finance theory, but in the gritty, hands-on reality of the county fair, the chicken coop, and the kitchen cabinet.

By treating money as a tool rather than a status symbol, this family has pioneered a pragmatic approach to financial literacy that transforms mundane childhood desires into critical life lessons. Their methodology, which focuses on earning, budgeting, and the painful reality of debt, offers a blueprint for parents aiming to demystify the "weird adult world" of personal finance for their five- and seven-year-old children.

The Philosophy of Necessity vs. Discretion

At the core of the Frugalwoods’ approach is a clearly defined "family money philosophy." It is a binary system designed to establish firm boundaries between needs and wants. Under this framework, parents remain the sole providers for essential living expenses: housing, clothing, healthcare, education, and nutrition.

However, the line is drawn sharply when it comes to discretionary spending. If a child desires a souvenir at a museum, a specific treat at a restaurant, or an item from a school book fair, they are required to use their own funds. This distinction is vital; it forces children to confront the opportunity cost of their purchases. By refusing to act as a bottomless ATM, parents provide their children with the autonomy to decide whether an item is truly worth the effort required to earn the money to buy it.

A Chronology of Financial Maturity

The transition from passive consumer to active money manager does not happen overnight. The Frugalwoods have implemented a scaffolded learning process, broken down into developmental stages:

- The Labor-Value Connection: Children begin by learning the basics of counting currency and identifying denominations. They are taught the foundational truth that "Mom and Dad go to work to earn money, which is then used to pay for family needs."

- The Chore-Economy: The family utilizes a market-based chore system. Tasks are assigned a specific monetary value, and payment is contingent upon completion to a high standard. This ensures children associate income with productivity rather than entitlement.

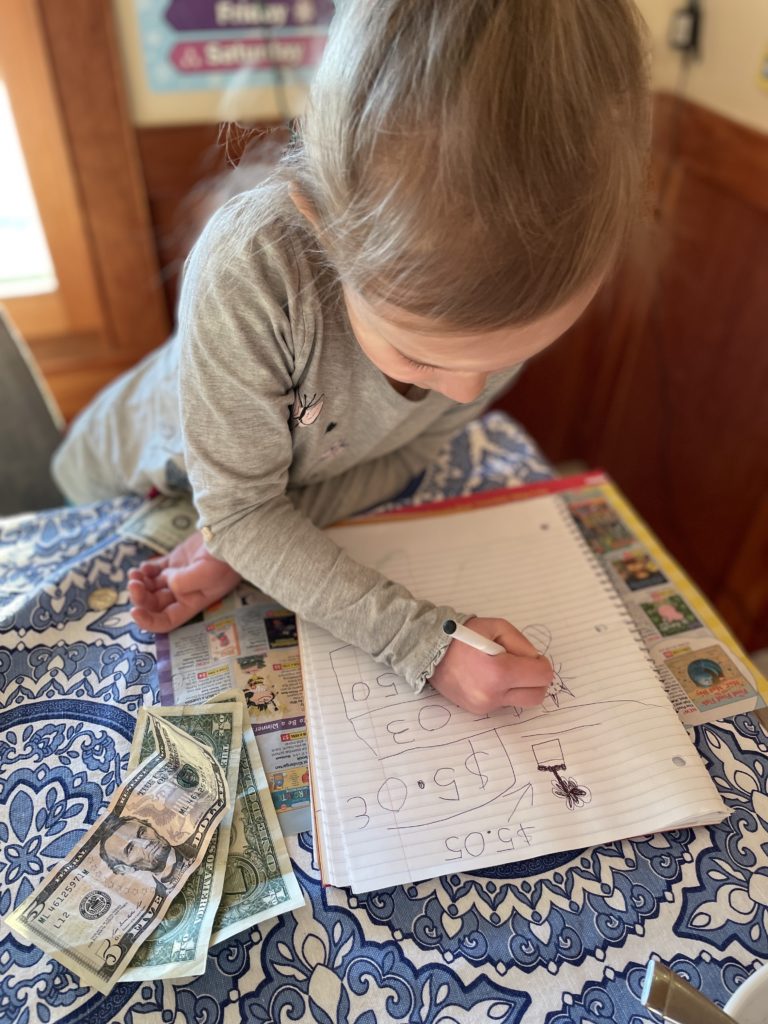

- The Debt-Experience: Perhaps the most radical step in their timeline occurred last year when a daughter was allowed to "go into debt" to purchase a $13 inflatable unicorn while possessing only $9. The parents covered the $4 difference, creating a mandatory repayment plan through additional chores.

- The Autonomy Phase: Once the sting of debt is understood, children move toward independent budgeting. This includes managing their own wallets, remembering to bring their funds to outings, and negotiating shared expenses with siblings.

Supporting Data: The Anatomy of a Chore

Not all work is created equal in the Frugalwoods household. The parents differentiate between "daily living" tasks and "value-added" chores.

- Unpaid Daily Work: These tasks are categorized as the price of admission for living within a family unit. This includes making beds, cleaning up personal toys, collecting eggs from the chickens, and putting away one’s own laundry. These chores foster a sense of community responsibility.

- Paid Chores: These involve tasks that go above and beyond, such as deep-cleaning kitchen cabinets or performing specialized labor. Compensation is set at "fair market value," and the children are encouraged to negotiate the price of a "chore bundle."

The data from these experiences suggests that when children are required to "pick up each individual trashlette" they drop, the quality of their work improves drastically. Furthermore, by experiencing the ebbs and flows of a "chore sprint"—where they might clean out a parent’s wallet on a Saturday—the children learn the volatility of income and the importance of saving for future wants.

Official Perspectives on Money as a Tool

The parents argue that shielding children from the realities of money creates anxiety rather than safety. By treating money as a neutral tool—akin to exercise or nutrition—they aim to remove the emotional baggage, judgment, and stress often associated with financial discussions.

"Money is not status, self-worth, emotional wellness, happiness, or contentment," the parents note. By framing it this way, they ensure that when their seven-year-old writes a book about their job, the focus remains on the process of work—meetings, coffee, and effort—rather than the accumulation of wealth. This demystification is key to raising children who view a car full of groceries as the result of hours worked, rather than a magical occurrence provided by a grocery store shelf.

The Hard Lessons: Debt and Loss

The most profound pedagogical tool in the family’s arsenal is the "debt experience." When a child realizes that working to pay off a purchase they have already consumed is inherently unsatisfying, the lesson sticks in a way that lectures never could.

The Frugalwoods report that after the unicorn incident, neither daughter has gone into debt again. This experience taught them three critical elements of financial health:

- Temporal Awareness: Understanding that money takes time to earn.

- The Weight of Obligation: Feeling the burden of debt makes future spending decisions more cautious.

- The Reality of Loss: In one instance, a child misplaced her wallet at a museum. The parents refused to intervene, forcing the child to check with the cashier herself. The experience of nearly losing her hard-earned money provided a visceral, real-life lesson in personal responsibility that no classroom simulation could replicate.

Implications for Future Financial Literacy

Looking ahead, the Frugalwoods are preparing to introduce the "Bank of Parental Units," a savings account system that pays interest. This is the next logical step in their scaffolded approach: moving from the simple "earn-and-spend" cycle to the more abstract concepts of long-term wealth accumulation and compound interest.

The implications for this style of parenting are significant. By allowing children to fail in a controlled environment—by losing a wallet, by going into debt, or by having to split a dessert with a sibling—parents are building a foundation of resilience. These children are not just learning how to count coins; they are learning how to navigate a world that rewards foresight, hard work, and the ability to distinguish between transient desires and long-term goals.

As the children grow, these early lessons will likely evolve into complex discussions about investing, credit scores, and the power of financial independence. For now, however, the focus remains on the basics: earning, keeping track of your own stuff, and understanding that the "magic" of money is, in reality, the product of human labor.

Conclusion: The Path Forward

Teaching children about money is an ongoing, evolving dialogue. The Frugalwoods’ experiment highlights a crucial truth: financial literacy is not a subject to be taught in isolation but a practice to be lived daily. Whether through the management of a lemonade stand or the repayment of a debt for a plastic unicorn, the lessons are clear.

By encouraging independence, demanding accountability, and keeping the conversations simple, parents can effectively prepare the next generation to be masters of their own financial destiny. As the family moves toward their next milestone—the introduction of a savings account—the community of parents following their journey remains eager to see how these foundational lessons will translate into adult financial wisdom.

The question remains: how will the children apply these early lessons to their future financial endeavors? Given the discipline they have already demonstrated, the trajectory looks promising. The "weird adult world" of money is no longer a mystery to them; it is a landscape they are learning to navigate with confidence, one dollar at a time.