Navigating the Digital Wealth Horizon: A Comprehensive Analysis of Modern Retirement Planning Software

Retirement planning has transitioned from a straightforward exercise in savings into a complex discipline of financial engineering. In the past, workers relied on simple rules of thumb, such as the classic "4% rule" or basic linear calculators, to estimate their readiness for life after work. Today, the landscape is dominated by sophisticated, cloud-based retirement planning software. These platforms aim to help individuals navigate the dual phases of wealth management: the accumulation phase (saving and growing assets) and the highly complex decumulation phase (spending down assets without running out of money).

However, as technology has advanced, so too has the realization that not all retirement tools are created equal. Different platforms utilize distinct algorithms, make varying assumptions about tax structures, and employ diverse forecasting methodologies. This comprehensive analysis evaluates the current state of retirement planning software, explores why different tools yield conflicting results, and provides an in-depth review of the market’s leading platforms.

Main Facts: The Evolution and Discrepancies of Retirement Projections

The primary utility of a retirement calculator changes depending on the user’s proximity to retirement. For those decades away, these tools serve as motivational guides, helping to determine target savings rates and asset allocations. For those on the doorstep of retirement, the software becomes a critical risk-management tool, calculating sustainable annual spending limits, optimizing tax strategies, and modeling the timing of Social Security benefits.

Despite their utility, these digital planners can produce widely divergent projections. A seminal study examining five of the most popular retirement planning software packages revealed stark differences in outcomes when presented with identical financial profiles. The discrepancies stem from how different programs handle variables such as inflation, investment returns, tax brackets, healthcare costs, and longevity risk.

Because a single software engine can suffer from systemic bias—either overestimating or underestimating a user’s financial longevity—industry experts strongly recommend that individuals utilize multiple independent planning programs before executing a long-term retirement strategy. Relying on a single program introduces a single point of failure into a process where mistakes can take decades to manifest.

Chronology: The Lifecycle of Retirement Planning Needs

An individual’s relationship with retirement planning software evolves chronologically through three distinct phases of their financial lifecycle:

[ Phase 1: Accumulation ] ----> [ Phase 2: Transition ] ----> [ Phase 3: Decumulation ]

- Focus: Savings Rate - Focus: "What-If" Scenarios - Focus: Drawdown Optimization

- Tool: Simple Calculators - Tool: Hybrid Platforms - Tool: Sophisticated EnginesPhase 1: The Accumulation Phase (Early to Mid-Career)

During this stage, the user’s primary goal is capital growth. The mathematical inputs are relatively simple: current savings, expected annual contributions, estimated rate of return, and years until retirement. At this point, basic, linear retirement calculators are often sufficient to keep savers on track.

Phase 2: The Transition Phase (5 to 10 Years from Retirement)

As retirement approaches, the planning horizon shrinks, and the margin for error narrows. Users must transition from simple calculators to robust planning software. This phase requires modeling "what-if" scenarios, such as early retirement, career changes, purchasing a second home, or funding a child’s education. The chronological focus shifts from savings rates to asset preservation and tax-deferred growth optimization.

Phase 3: The Decumulation Phase (At and During Retirement)

This is the most mathematically complex phase. The retiree must determine which accounts to draw from first (taxable, tax-deferred, or tax-free), how to manage required minimum distributions (RMDs), when to claim Social Security, and how to mitigate sequence-of-returns risk. At this stage, static calculators fail entirely, necessitating the use of advanced, dynamic planning software that can run Monte Carlo simulations and historical backtests.

Supporting Data: Detailed Evaluations of the Top Planning Platforms

To assist investors in choosing the right tools for their specific chronological phase, we have evaluated the four leading retirement planning platforms on the market today.

| Feature / Metric | Boldin (PlannerPlus) | ProjectionLab (Premium) | Empower | Maxifi |

|---|---|---|---|---|

| Annual Cost | $144 / year | $129 / year | Free | Paid (Varies) |

| Primary Strength | Granular decumulation & Roth conversions | Exceptional UI & "What-If" scenarios | Automated asset tracking & simplicity | Economic consumption smoothing |

| Simulation Types | Deterministic projections | Monte Carlo & Historical backtesting | Monte Carlo simulations | Deterministic & Stochastic |

| Account Syncing | Yes (Manual or Linked) | Yes (Manual or Linked) | Yes (Automated linking) | Yes (Manual/Import) |

| Platform | Web | Web | Web / Mobile | Web |

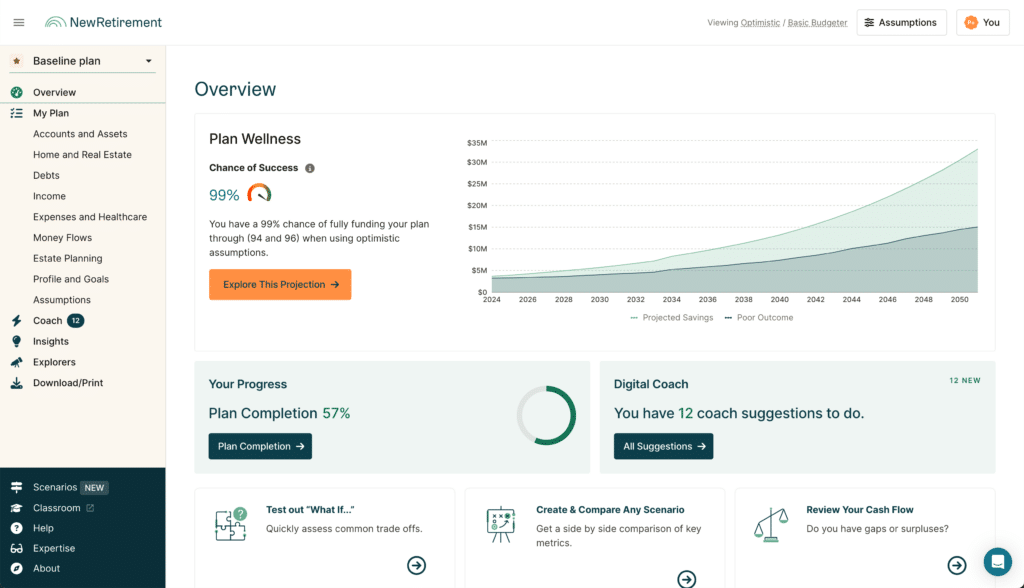

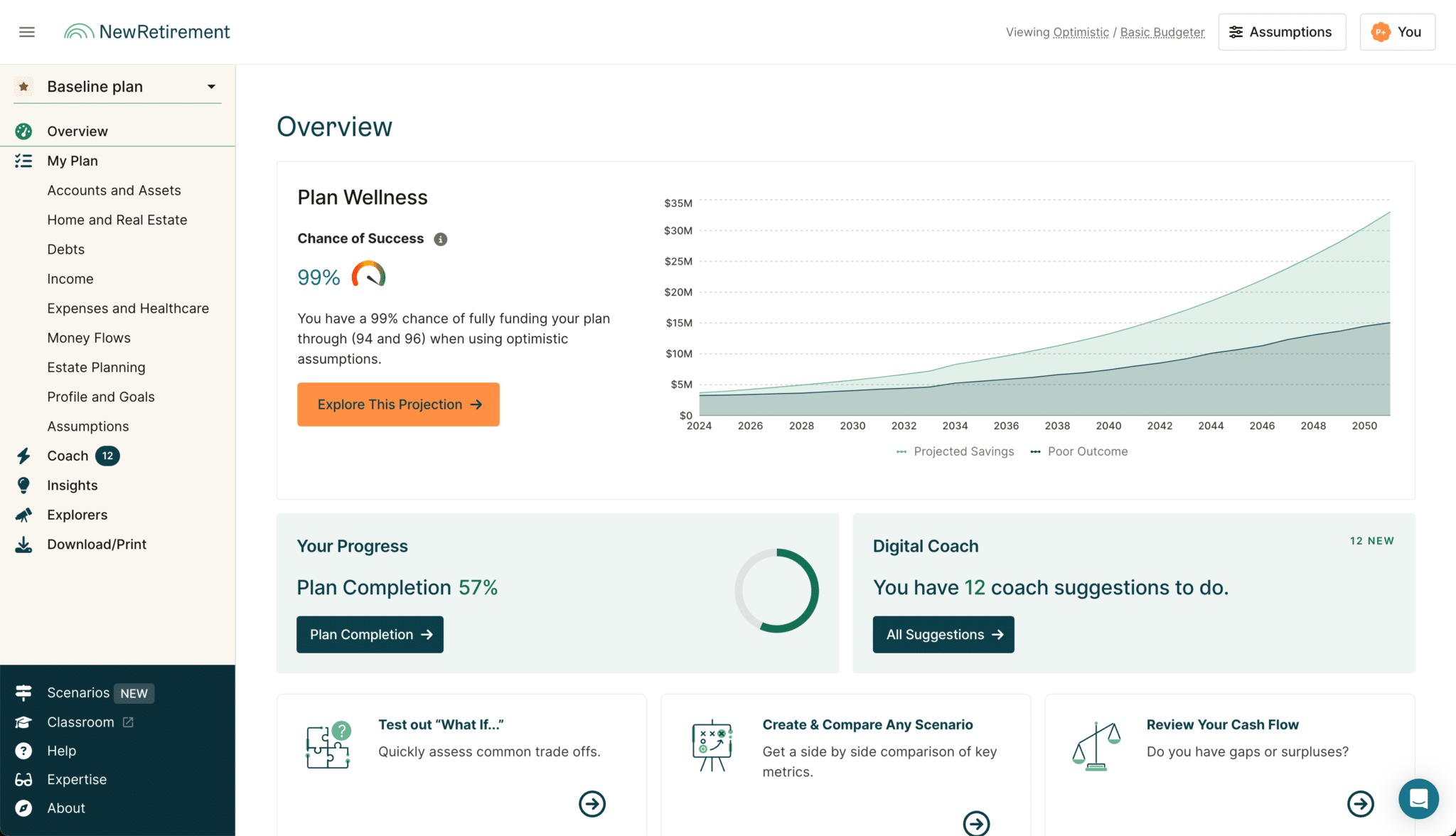

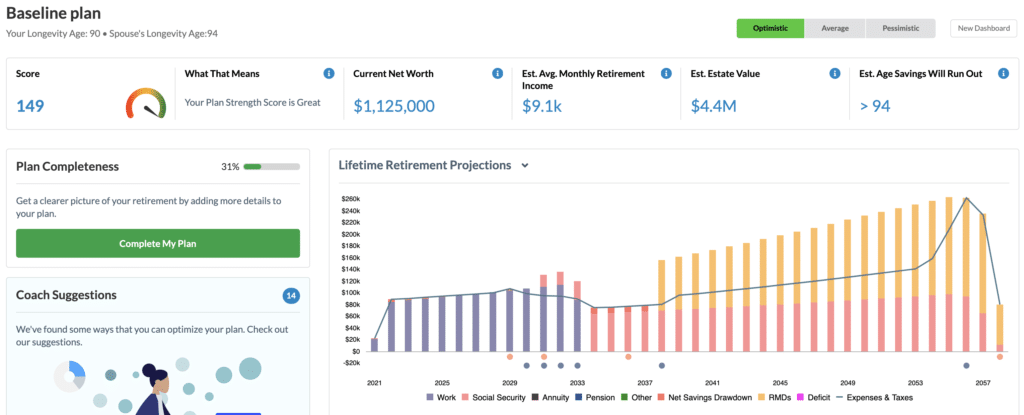

1. Boldin (Formerly New Retirement)

Boldin is widely regarded by financial planners as one of the most comprehensive consumer-facing retirement modeling tools available. It is engineered specifically to handle the granular details of the decumulation phase.

+-----------------------------------------------------------------+

| BOLDIN PLATFORM PROFILE |

+-----------------------------------------------------------------+

| Pros: |

| * Highly granular inputs (monthly, annual, or one-off basis) |

| * Excellent Roth IRA conversion optimization calculator |

| * Models Medicare, Social Security, and pensions with precision |

| |

| Cons: |

| * Lacks historical backtesting (relies on average-return models)|

| * Steep learning curve for novice users |

+-----------------------------------------------------------------+Key Capabilities and Usability

Boldin balances complexity with accessibility through a two-tiered onboarding process. Users can complete a quick-start guide in under five minutes to receive a baseline snapshot of their retirement readiness. From there, they can dive into highly detailed portals to model complex cash-flow events.

The platform allows users to map out future income and expenses with extreme specificity. For example, a user can program a temporary income stream (like part-time consulting work) that terminates at age 65, alongside a one-time capital expense (such as a home renovation) at age 70.

Standout Feature: Roth IRA Conversion Optimization

One of Boldin’s most powerful tools is its proprietary Roth IRA conversion calculator. This engine analyzes a user’s current tax bracket and projects future tax rates to determine the optimal timing and dollar amount for converting traditional tax-deferred assets into tax-free Roth assets. This feature alone can potentially save retirees tens of thousands of dollars in lifetime taxes and Medicare premium surcharges (IRMAA).

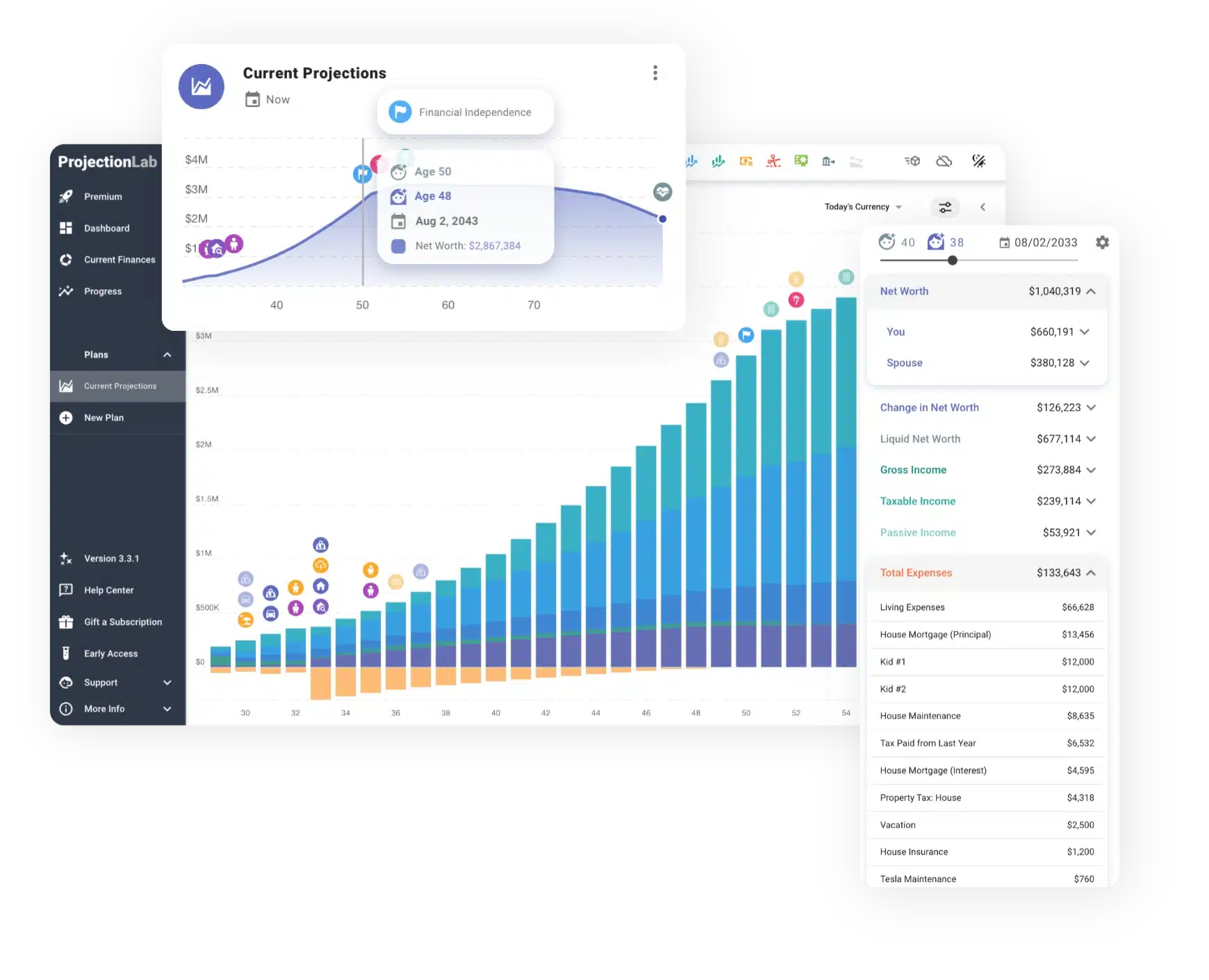

2. ProjectionLab

Created by developer Kyle Nolan, ProjectionLab has quickly become a favorite among the Financial Independence, Retire Early (FIRE) community and tech-savvy investors. The platform is praised for its modern user interface, highly interactive charts, and transparent calculations.

+-----------------------------------------------------------------+

| PROJECTIONLAB PLATFORM PROFILE |

+-----------------------------------------------------------------+

| Pros: |

| * Best-in-class user interface and interactive data visuals |

| * Highly flexible "What-If" scenario builder |

| * Supports Monte Carlo and historical backtesting |

| |

| Cons: |

| * Lacks automated, dedicated Roth conversion engines |

| * Social Security simulation tools are less detailed than peers|

+-----------------------------------------------------------------+Key Capabilities and Usability

ProjectionLab excels at visual representation and fluid scenario planning. It allows users to create a "Base Plan" and then layer on multiple alternative scenarios to see how changes in retirement age, investment yields, or real estate transactions impact their long-term wealth trajectory.

The software supports a wide range of account types, including traditional and Roth 401(k)s, 403(b)s, traditional and Roth IRAs, Health Savings Accounts (HSAs), and standard taxable brokerage accounts.

Standout Feature: Advanced Withdrawal Strategy Modeling

Unlike basic tools that assume a static drawdown rate, ProjectionLab allows users to model and compare complex, dynamic withdrawal strategies. Users can test how their portfolio would fare under:

- The 4% Rule: A constant inflation-adjusted spending model.

- The Guyton-Klinger Guardrails: A dynamic strategy that adjusts spending up or down based on portfolio performance.

- Variable Percentage Withdrawal (VPW): A method that recalculates spending annually based on current portfolio value and life expectancy to maximize consumption while minimizing the risk of ruin.

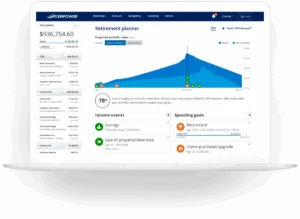

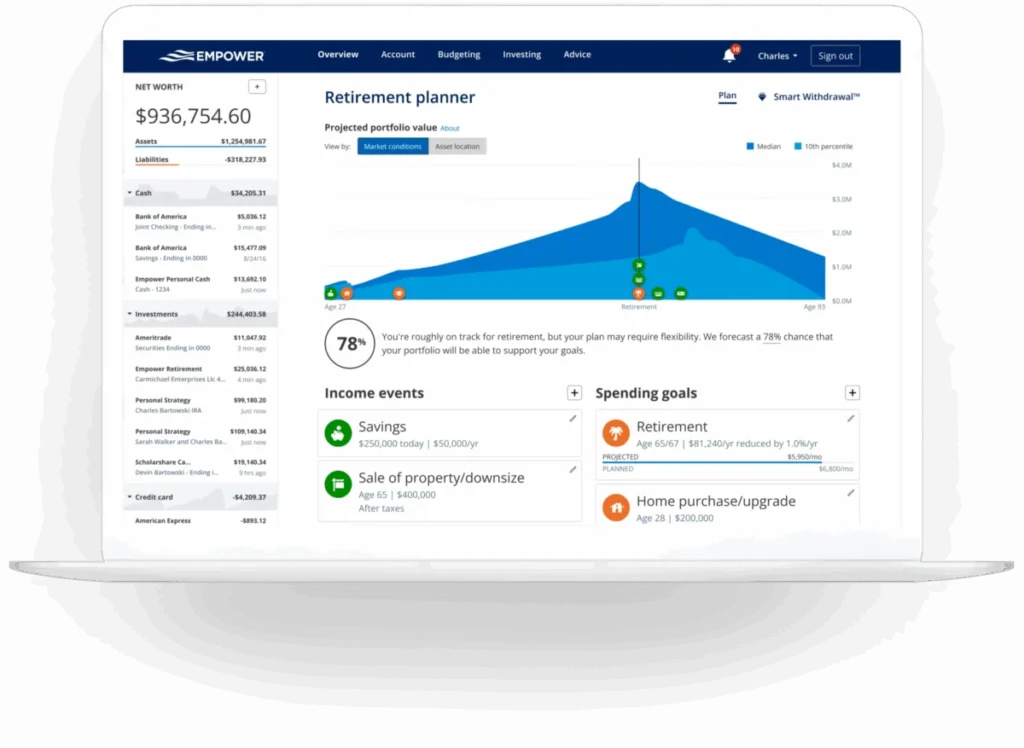

3. Empower

Empower (formerly known as Personal Capital) is widely considered the gold standard for free, automated retirement tracking.

+-----------------------------------------------------------------+

| EMPOWER PLATFORM PROFILE |

+-----------------------------------------------------------------+

| Pros: |

| * 100% Free to use |

| * Automated, real-time account aggregation and tracking |

| * Robust Monte Carlo engine with clear success probabilities |

| |

| Cons: |

| * Free tool is used as a lead generator for wealth management |

| * Less granular tax-planning features than paid alternatives |

+-----------------------------------------------------------------+Key Capabilities and Usability

Empower’s core strength lies in its automated aggregation. By linking their investment, bank, and retirement accounts via secure API protocols, users can eliminate manual data entry. Empower automatically pulls real-time balances, asset allocations, and investment fees into its centralized dashboard.

The built-in Retirement Planner uses this live data to run comprehensive Monte Carlo simulations. The system simulates up to 5,000 market scenarios to calculate the statistical probability that the user’s portfolio will survive their projected lifetime.

Standout Feature: Side-by-Side Scenario Comparison

Empower allows users to construct multiple lifestyle scenarios—such as changing retirement dates, moving to a lower-tax state, or adjusting retirement spending—and compare their probability of success side-by-side. This visual comparison makes it easy to understand the direct trade-offs of major life decisions.

4. Maxifi

Maxifi is a highly specialized tool designed around a fundamentally different school of financial thought: the economic theory of "consumption smoothing."

+-----------------------------------------------------------------+

| MAXIFI PLATFORM PROFILE |

+-----------------------------------------------------------------+

| Pros: |

| * Rigorous economic engine prevents drastic lifestyle changes |

| * Highly sophisticated tax and Social Security optimization |

| |

| Cons: |

| * High learning curve and less intuitive user interface |

| * Long calculation times for complex scenarios |

+-----------------------------------------------------------------+Key Capabilities and Usability

Developed by prominent economist Laurence Kotlikoff, Maxifi operates on the assumption that individuals want to maintain a consistent standard of living throughout their entire lives, avoiding sudden drops in consumption.

Rather than asking users to guess how much they want to spend in retirement, Maxifi calculates the maximum amount they can spend every year based on their current assets, future income, and projected tax liabilities.

While highly sophisticated, Maxifi is often cited as having the steepest learning curve of any major planner. Its interface is less visual than ProjectionLab and more academic in nature. However, for those who value economic rigor over visual aesthetics, Maxifi provides an incredibly detailed mathematical foundation for retirement planning.

Expert Insights: Why Projections Differ and How Algorithms Interpret Wealth

To understand why different retirement planners produce conflicting results, one must look at the underlying calculations and structural assumptions of the software.

[ USER FINANCIAL DATA ]

│

┌────────┴────────┐

▼ ▼

[ SOFTWARE A ] [ SOFTWARE B ]

- Deterministic - Stochastic (Monte Carlo)

- Flat 7% Return - 5,000 Random Trials

- Static Taxes - Dynamic Tax Brackets

│ │

▼ ▼

[ 95% Success ] [ 72% Success ]Deterministic vs. Stochastic Modeling

- Deterministic Models: These calculators assume a fixed, average rate of return every year (e.g., a flat 7% return). While useful for high-level estimations, deterministic models fail to account for market volatility and sequence-of-returns risk. If a market downturn occurs in the first three years of a retiree’s decumulation phase, a deterministic model will not capture the increased risk of portfolio depletion.

- Stochastic Models (Monte Carlo): These systems run thousands of randomized market trials based on historical volatility and asset correlations. This approach provides a probability of success (e.g., an 85% chance that the portfolio will last to age 95), which is a much more realistic framework for managing real-world risk.

Taxation and Policy Assumptions

Taxes are often the single largest expense a retiree faces. Sophisticated platforms like Boldin and ProjectionLab attempt to project annual federal and state income tax brackets, capital gains taxes, and RMD requirements.

Lighter calculators, however, often apply a flat, estimated tax rate across the entire timeline. This oversimplification can lead to highly inaccurate projections, especially for retirees with a mix of pre-tax, Roth, and taxable accounts.

Strategic Implications for Individual Investors

The primary takeaway for individual investors is the danger of single-source reliance. Using a single planning tool can create confirmation bias, leading to overconfidence or unnecessary financial anxiety.

The Case for Multi-Program Modeling

To build a resilient retirement plan, investors should stress-test their assumptions across multiple platforms:

- Use Empower as a baseline dashboard to track real-time asset allocation, monitor investment fees, and run initial Monte Carlo simulations.

- Use Boldin to build a detailed cash-flow model, optimize Social Security claiming strategies, and design a multi-year Roth IRA conversion plan.

- Use ProjectionLab to stress-test your portfolio against historical market cycles and compare different dynamic withdrawal strategies (such as Guyton-Klinger).

- Use Maxifi if you want to verify your plan against a rigorous economic consumption-smoothing model.

By cross-referencing projections across these diverse engines, investors can identify blind spots, optimize their tax strategies, and build a retirement plan designed to withstand both market volatility and changing tax codes.