Navigating the Algorithmic Divide: A Comparative Analysis of Modern Retirement Planning Software

Retirement planning has undergone a profound technological transformation. Once the exclusive domain of high-fee wealth managers armed with proprietary mainframe systems, the discipline of retirement projection has been thoroughly democratized. Today, highly sophisticated software engines are available directly to individual consumers. These online platforms help users solve two critical, lifelong financial puzzles: determining optimal savings rates during their wealth-accumulation years, and calculating sustainable distribution strategies to avoid outliving their capital during decumulation.

However, the proliferation of these digital tools has introduced a new challenge: algorithmic divergence. Because different software packages rely on distinct mathematical methodologies, tax assumptions, and economic models, they rarely yield identical results.

A landmark study examining five of the industry’s most popular retirement planning software packages revealed stark discrepancies in their projected outcomes for identical household profiles. The researchers concluded that relying on a single calculator introduces systemic planning risks. To mitigate this, they advised individuals to run their financial profiles through multiple planning engines before implementing any actionable retirement strategy.

This comprehensive guide analyzes the leading retirement planning platforms, evaluates their underlying methodologies, and explores the economic theories that drive their calculations.

1. Main Facts: The Algorithmic Divergence in Retirement Projections

The core issue facing self-directed investors is that retirement planning is not a static calculation; it is a complex web of interrelated, shifting variables. A robust projection engine must account for:

- Tax Optimization: Estimating federal, state, and local taxes over multiple decades, including the shifting brackets of ordinary income, capital gains, and Required Minimum Distributions (RMDs).

- Stochastic vs. Deterministic Modeling: Choosing between deterministic projections (assuming a constant, flat rate of return) and stochastic modeling (using Monte Carlo simulations to model thousands of randomized market pathways).

- Sequence-of-Returns Risk: Calculating how early-retirement market downturns affect the long-term viability of a portfolio.

- Regulatory Dynamics: Incorporating complex rules governing Social Security claiming strategies, Medicare premium surcharges (IRMAA), and Roth IRA conversion limits.

Because each software developer weighs these variables differently, the same financial data can produce a 95% probability of success on one platform and a warning of impending insolvency on another. Consequently, sophisticated planning requires a multi-tool approach to stress-test assumptions and find consensus among differing mathematical models.

2. Chronology: The Evolution of Retirement Planning Technology

To understand the current landscape of retirement software, it is helpful to trace how these analytical frameworks have evolved over the past three decades.

[Phase 1: The Static Era] ───► [Phase 2: The Stochastic Shift] ───► [Phase 3: The API & Tax Integration Era]

(1990s: Bengen's 4% Rule, (2000s: Monte Carlo Simulations, (2010s-Present: Real-Time Account Linking,

Simple Spreadsheets) Sequence-of-Returns Modeling) Roth Conversion Engines, Custom Sandbox Scenarios)Phase 1: The Static Era (1990s)

Retirement planning relied heavily on static, deterministic calculations. Following William Bengen’s seminal 1994 study on the "4% Rule," early web-based calculators asked users for their current age, retirement age, savings rate, and an assumed annual investment return (often a flat 7% or 8%). These tools failed to account for market volatility, inflation fluctuations, or changing tax brackets.

Phase 2: The Stochastic Shift (2000s)

As computing power grew, developers integrated Monte Carlo simulations into consumer-facing software. Rather than assuming a linear asset growth path, these systems simulated 500 to 10,000 market trials using historical volatility data. This shifted the industry standard from a binary "yes/no" projection to a nuanced probability of success.

Phase 3: The API and Tax Integration Era (2010s–Present)

The current generation of retirement software features secure API account aggregation (linking real-time portfolio balances), hyper-detailed tax optimization engines, and customizable "what-if" scenario sandboxes. Modern platforms can model complex strategies like multi-year Roth IRA conversion ladders, Medicare premium brackets, and dynamic spending rules.

3. Supporting Data: Comparative Analysis of the Top Retirement Planning Platforms

To identify the most effective tools on the market, we evaluated the leading retirement software platforms based on feature density, calculation engines, user interfaces, and pricing models.

| Platform | Best For | Simulation Engine | Unique Feature | Cost Structure |

|---|---|---|---|---|

| Boldin | Advanced Cash-Flow & Tax Planning | Deterministic & Monte Carlo | Multi-year Roth IRA conversion modeling | Free tier; PlannerPlus: $144/year |

| ProjectionLab | "What-If" Scenario Sandboxes | Monte Carlo & Historical Backtesting | Custom withdrawal strategies (e.g., Guyton-Klinger) | Free tier; Premium: $129/year; Lifetime: $799 |

| Empower | Automated Portfolio Tracking | Monte Carlo (Stochastic) | Automatic API account aggregation | 100% Free |

| MaxiFi | Economic Consumption Smoothing | Proprietary Dynamic Programming | Maximizing lifetime discretionary spending | $109/year (Basic); $149/year (Premium) |

Detailed Platform Breakdowns

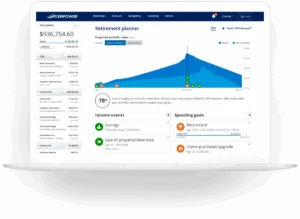

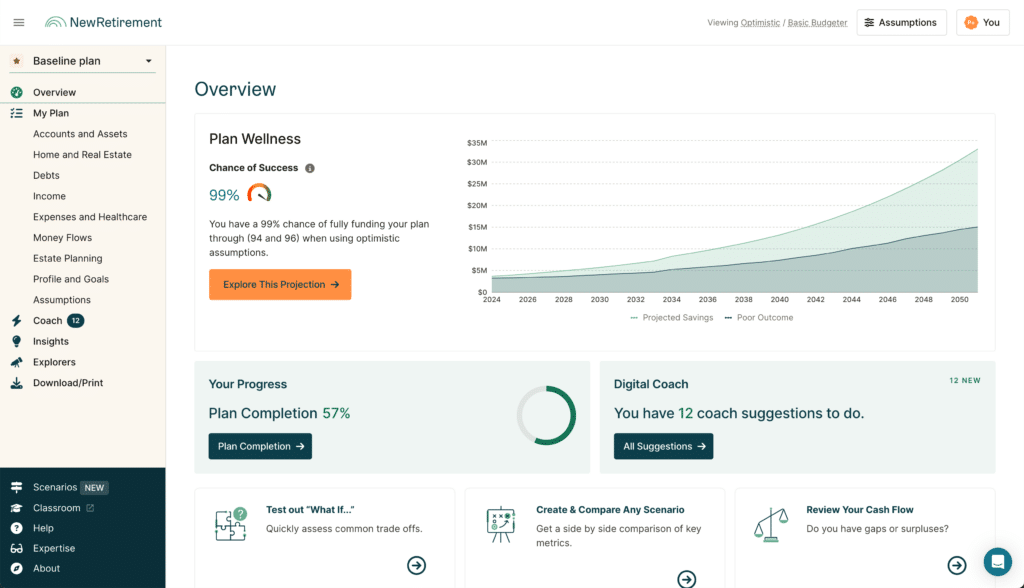

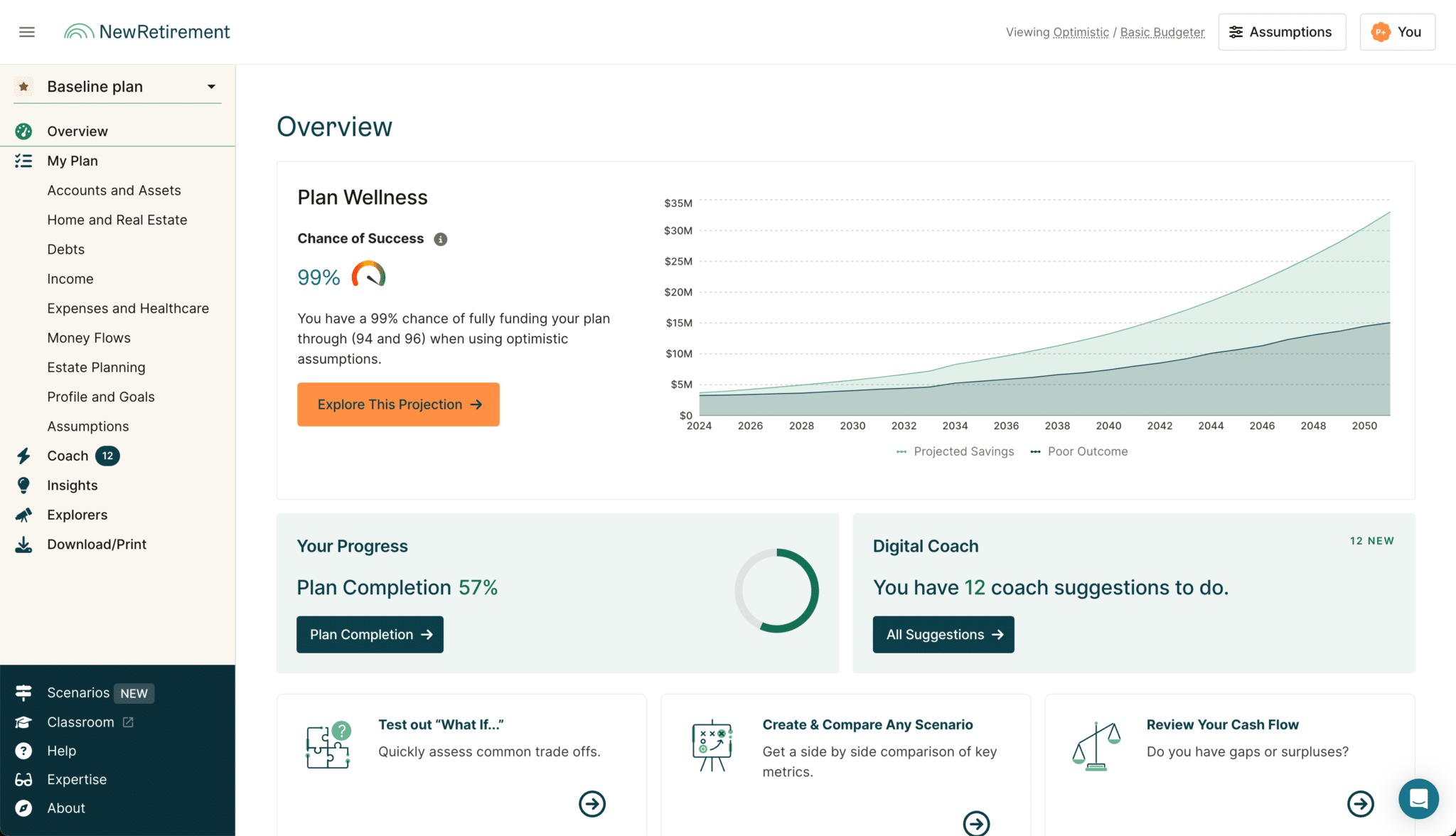

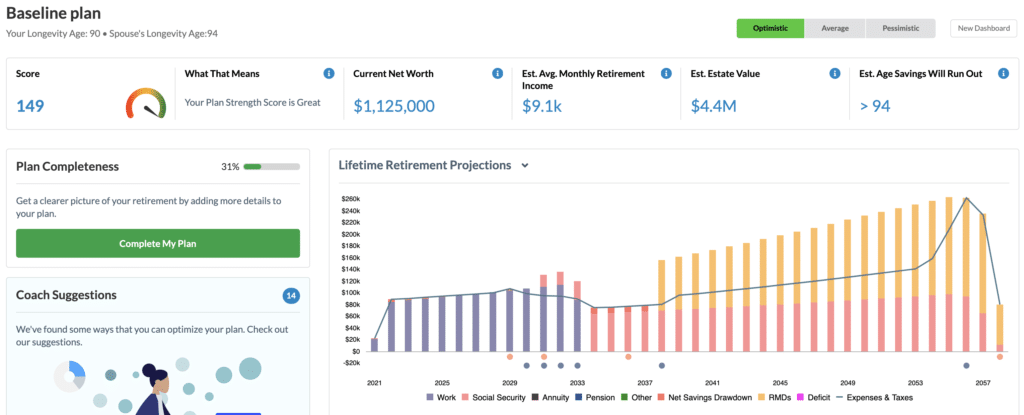

Boldin (formerly New Retirement)

For users who want to map out every detail of their decumulation years, Boldin is an exceptionally thorough tool. The software excels at cash-flow modeling, allowing users to schedule income, expenses, and asset sales on a monthly, annual, or one-off basis.

[User Input Data] ───► [Boldin Engine] ───► [Tax Bracket & Cash Flow Output]

│

└───► [Roth Conversion Optimizer]- Pros: Outstanding interface that balances deep technical capabilities with user accessibility; robust Roth IRA conversion tools; detailed Medicare and Social Security claiming modules.

- Cons: Does not support pure historical sequence-of-returns simulations (backtesting through specific historical eras).

- The Analytical Engine: Boldin utilizes a comprehensive cash-flow engine that calculates federal and state income taxes year by year, helping users identify "tax valleys"—years between retirement and the onset of RMDs when strategic Roth conversions can significantly reduce lifetime tax burdens.

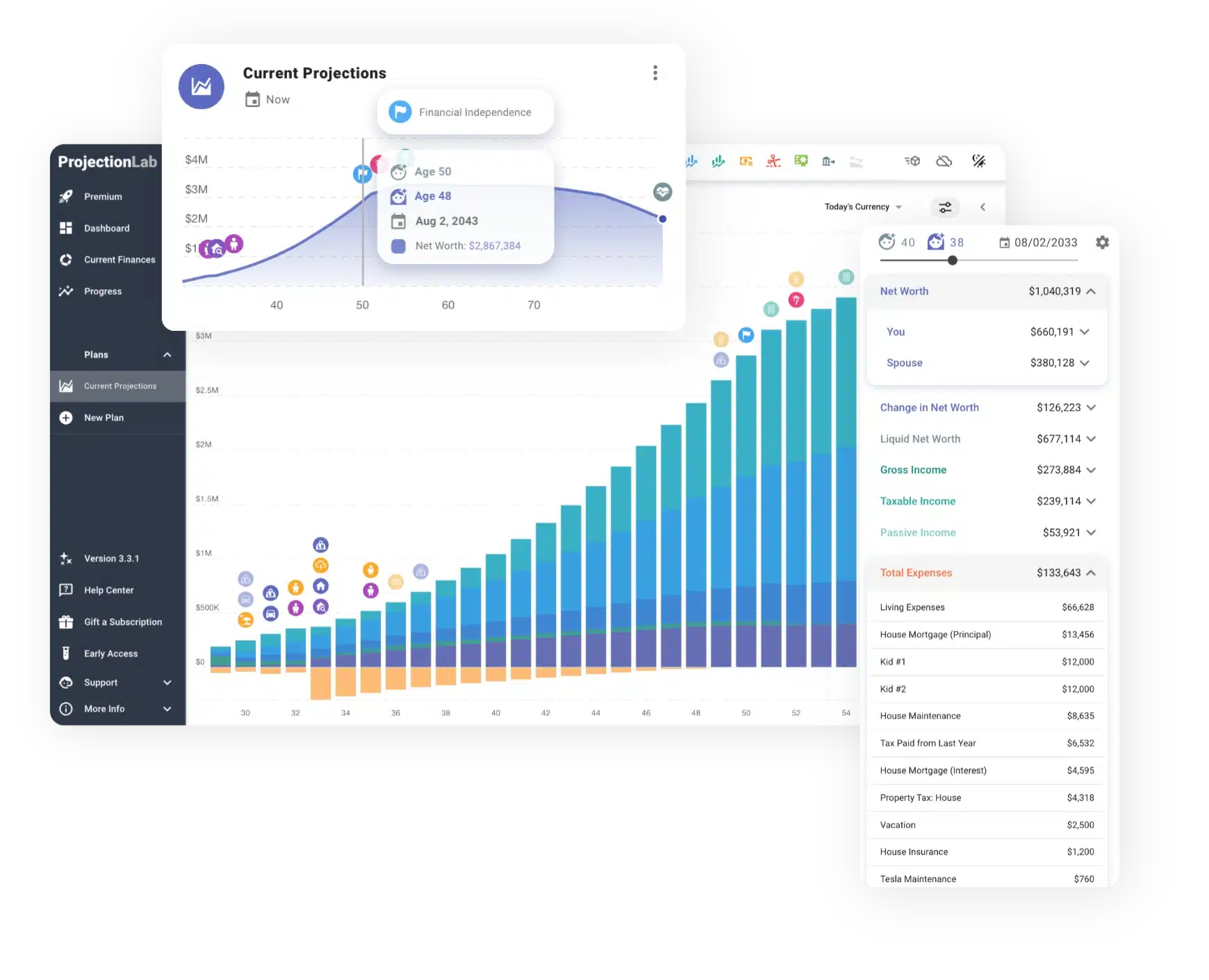

ProjectionLab

Created by developer Kyle Nolan, ProjectionLab has quickly become a favorite among the Financial Independence, Retire Early (FIRE) community. The platform stands out for its elegant user interface and its highly customizable simulation engine.

┌───► Monte Carlo Simulation (Probabilistic)

[ProjectionLab] ────┼───► Historical Backtesting (Staging real historical cycles)

└───► Deterministic Projection (Linear asset growth)- Pros: Highly flexible; allows users to compare different complex withdrawal strategies (e.g., Variable Percentage Withdrawal, Guyton-Klinger guardrails); private and security-focused data options.

- Cons: Lacks automated step-by-step guidance for complex maneuvers like Roth conversions, requiring users to set up these parameters manually.

- The Analytical Engine: Unlike platforms limited to Monte Carlo simulations, ProjectionLab allows users to backtest their portfolios against actual historical cycles, such as the Great Depression or the 1970s stagflation era, to see how their plan would have held up.

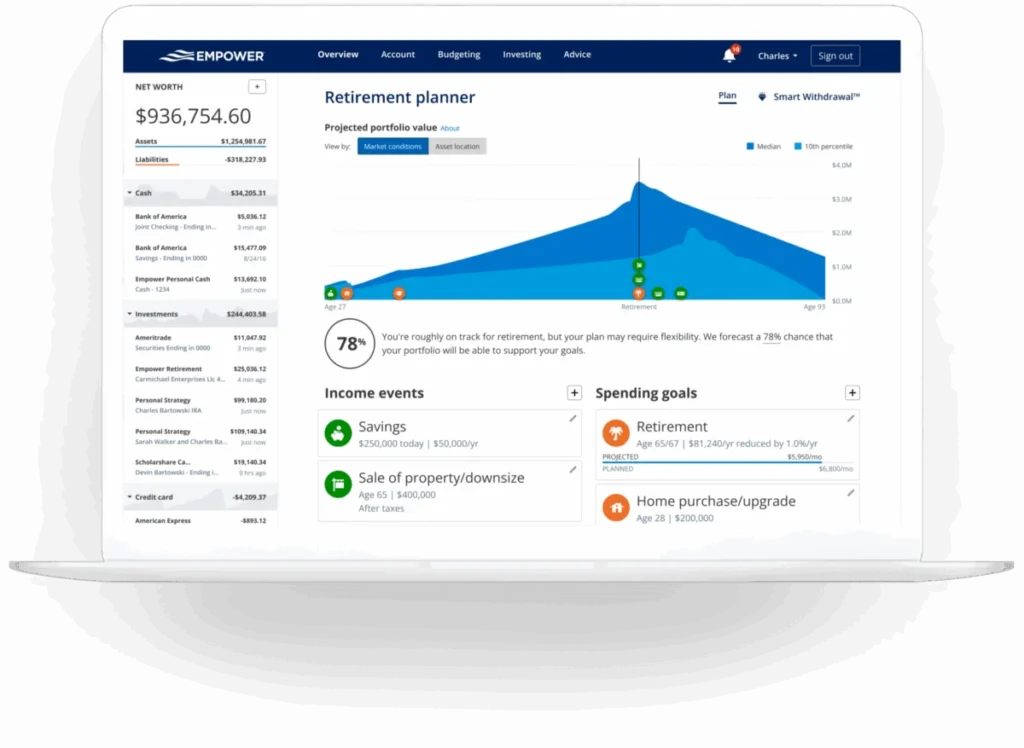

Empower

Empower (formerly Personal Capital) remains the gold standard for free, automated investment tracking. By linking bank, brokerage, and retirement accounts via secure APIs, Empower provides a real-time, consolidated view of net worth, asset allocation, and investment fees.

[Linked Brokerage Accounts] ───► [Empower Aggregator] ───► [Monte Carlo Engine] ───► [% Probability of Success]- Pros: Fully automated data entry; clean, intuitive dashboards; excellent tools for analyzing investment fees and asset allocation.

- Cons: Limited customization for complex tax planning or non-standard income and expense events.

- The Analytical Engine: Empower runs a linked portfolio through a Monte Carlo simulation based on the user’s current asset allocation. It provides a straightforward probability score, making it an excellent high-level dashboard, though it lacks the granular tax-planning depth of Boldin or ProjectionLab.

MaxiFi

MaxiFi takes a fundamentally different mathematical approach to retirement planning. Developed by Boston University economics professor Laurence Kotlikoff, the software is built entirely around the economic theory of "consumption smoothing."

[Assets & Income Sources] ───► [MaxiFi Algorithms] ───► [Stable Annual Discretionary Spending Target]- Pros: Highly sophisticated mathematical calculations; prevents users from over- or under-saving by calculating a sustainable lifetime standard of living.

- Cons: Steeper learning curve; rigid interface; runs counter to how many retirees naturally prefer to spend money.

- The Analytical Engine: Rather than asking users to guess their future retirement spending, MaxiFi analyzes their current assets, liabilities, and future income streams to calculate exactly how much they can spend each year to maintain a consistent standard of living throughout their life.

4. Expert Perspectives and Theoretical Foundations

The stark differences in how these platforms calculate retirement readiness stem from a fundamental debate within financial economics: Goal-Based Planning versus Consumption Smoothing.

The Academic View: Consumption Smoothing

Proponents of consumption smoothing, such as MaxiFi creator Laurence Kotlikoff, argue that traditional financial planning is backward. Standard software asks users to input a target retirement spending goal (e.g., 80% of pre-retirement income).

According to economic theory, this approach is deeply flawed because human beings naturally seek to maintain a stable standard of living. If an individual saves too much, they unnecessarily lower their current standard of living; if they save too little, they face a sharp drop in their quality of life later. Consumption smoothing algorithms solve this by treating annual spending as the dependent variable, dynamically adjusting it based on the user’s total financial picture.

The Pragmatic View: Goal-Based Cash-Flow Modeling

Conversely, many practical financial planners argue that consumption smoothing is too rigid for real-world behavior. Empirical data shows that retirement spending is rarely flat. Instead, it typically follows a "U-shaped" curve:

Spending Level

▲

│ /▀▀▀▀▀▀▀▀ /▀▀▀▀▀▀▀▀

│ / / (Late-Stage Healthcare Costs)

│ / /

│/ _______/

│ "Go-Go" Years "Slow-Go" "No-Go"

└────────────────────────────────────────► AgeDuring the early active retirement years ("Go-Go" phase), spending on travel and leisure spikes. It then declines during the mid-retirement years ("Slow-Go" phase), before rising again in late retirement ("No-Go" phase) due to healthcare and long-term care costs. Platforms like Boldin and ProjectionLab allow users to model these distinct spending phases, which many retirees find more aligned with their actual plans.

5. Implications: Best Practices for Self-Directed Retirement Planning

The divergence in software outputs highlights a clear lesson: relying on a single algorithmic tool can create a false sense of security or cause unnecessary financial anxiety. To build a resilient retirement plan, self-directed investors should adopt a structured, multi-step process:

- Use Empower for Real-Time Tracking: Leverage Empower’s free API integration to aggregate accounts, analyze portfolio fees, and monitor overall asset allocation.

- Use Boldin for Decumulation and Tax Mapping: Import asset values into Boldin to identify tax-saving opportunities, model Roth IRA conversions, and plan for Medicare and Social Security claiming strategies.

- Use ProjectionLab to Stress-Test Scenarios: Run the plan through ProjectionLab’s historical backtesting and custom withdrawal engines to see how it performs under different market conditions and spending rules.

- Adopt a Conservative Margin of Safety: Given the inherent limits of long-term economic forecasting, target a Monte Carlo success rate of 85% to 95%. Any higher may indicate over-saving, while any lower suggests a need for greater flexibility in retirement spending.

Ultimately, retirement planning software should not be viewed as a generator of absolute truths, but rather as a tool for mapping out possibilities. By understanding the methodologies behind these platforms and comparing their results, investors can make highly informed, confident decisions about their financial future.