Navigating Digital Wealth: A Comprehensive Analysis of the Market’s Leading Retirement Planning Software

As the responsibility for retirement security has shifted from institutional employers offering defined-benefit pensions to individual savers managing defined-contribution plans, the demand for robust financial planning technology has surged. Today, retirement calculators and comprehensive planning software serve as the primary navigational instruments for millions of pre-retirees and retirees. When users are decades away from retirement, these digital tools help determine necessary savings rates; as retirement approaches, they assist in calculating sustainable annual spending to prevent premature portfolio depletion.

However, not all retirement planning tools yield the same results. Because different platforms employ distinct methodologies, proprietary algorithms, and baseline assumptions regarding inflation, market returns, and tax structures, their final projections can vary dramatically. A prominent academic study evaluating five popular retirement planning software packages revealed stark differences in estimated retirement readiness and sustainable withdrawal rates. Consequently, financial experts recommend that individuals utilize multiple programs to stress-test their assumptions before executing a long-term financial strategy.

This report provides an in-depth analysis of the leading retirement planning platforms on the market today, examining their technical capabilities, methodologies, financial structures, and implications for personal wealth management.

Chronology: The Evolution of Personal Financial Planning Technology

To understand the current state of digital retirement planning, it is necessary to examine how these tools have evolved over the past three decades.

+----------------------------------------------------------------------------+

| 1990s - Early 2000s: Static Calculators |

| - Simple web forms with deterministic calculations. |

| - Assumed constant, linear rates of return (e.g., 7% annually). |

| - Ignored sequence-of-returns risk and complex tax regulations. |

+----------------------------------------------------------------------------+

|

v

+----------------------------------------------------------------------------+

| Late 2000s - 2010s: Automated Aggregation & Monte Carlo |

| - Introduction of account linking (APIs and screen scraping). |

| - Launch of Personal Capital (now Empower), offering free net-worth tools. |

| - Adoption of Monte Carlo simulations to model market volatility. |

+----------------------------------------------------------------------------+

|

v

+----------------------------------------------------------------------------+

| 2020s: Granular Customization & Rebranding |

| - Shift toward highly customizable cash-flow and tax planning. |

| - Rebranding of major platforms (e.g., New Retirement to Boldin). |

| - Emergence of indie developer tools like ProjectionLab. |

| - Integration of advanced strategies: Roth conversions and dynamic rules. |

+----------------------------------------------------------------------------+The Era of Static Calculators (1990s–Early 2000s)

Early internet retirement calculators were basic, single-page web forms. Users entered a few static variables: current age, target retirement age, current savings, and expected annual return. The software applied linear mathematical formulas, assuming a constant rate of return (e.g., 7% every year) and a fixed inflation rate. These deterministic models failed to account for market volatility, sequence-of-returns risk, or complex tax implications, often providing users with a false sense of security or unnecessary alarm.

The Rise of Aggregation and Monte Carlo Analysis (Late 2000s–2010s)

With the advent of secure account aggregation protocols, platforms began linking directly to users’ bank, brokerage, and retirement accounts. This period saw the rise of Personal Capital (founded in 2009, later rebranded as Empower), which democratized access to institutional-grade portfolio tracking and basic retirement forecasting. During this era, Monte Carlo simulations—which run thousands of randomized market trials to determine the probability of portfolio survival—became the industry standard for consumer-facing software.

The Era of Granular Customization and Rebranding (2020–Present)

Today’s retirement planning landscape is characterized by highly sophisticated, consumer-accessible engines that rival the proprietary software used by professional wealth managers. Platforms have shifted from simple "calculators" to comprehensive "planning suites" capable of modeling complex tax strategies, healthcare costs, and localized cash flows.

Reflecting this evolution, several prominent tools have undergone significant rebranding and restructuring. For example, the widely used platform New Retirement rebranded as Boldin to signal a broader focus on active wealth building and life planning, while Personal Capital fully integrated into Empower following its acquisition, solidifying its position as a leading free financial management portal.

Supporting Data: In-Depth Evaluation of Leading Software Platforms

To assist investors in selecting the appropriate software for their needs, we evaluated the four leading platforms currently dominating the market: Boldin, ProjectionLab, Empower, and MaxiFi.

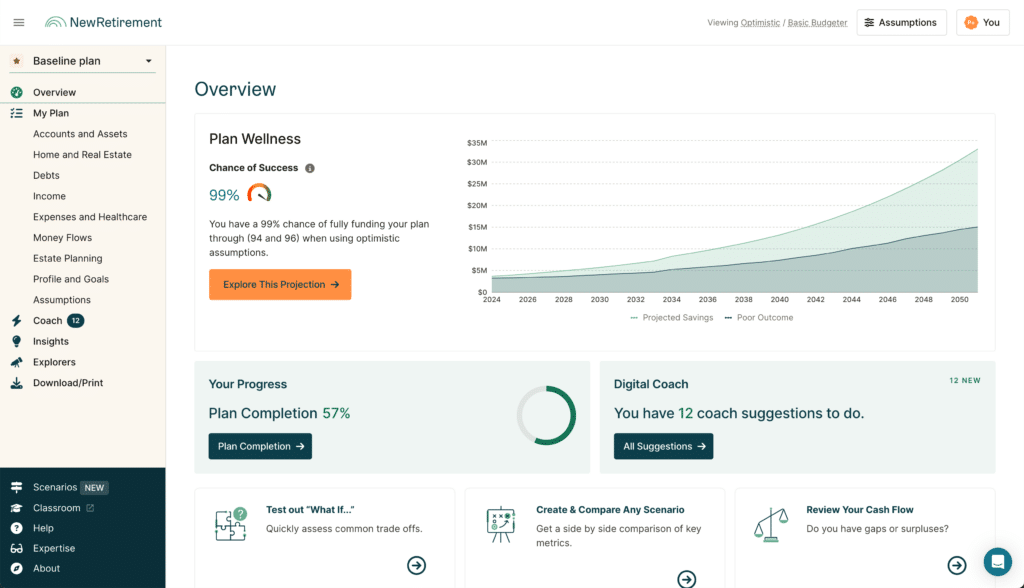

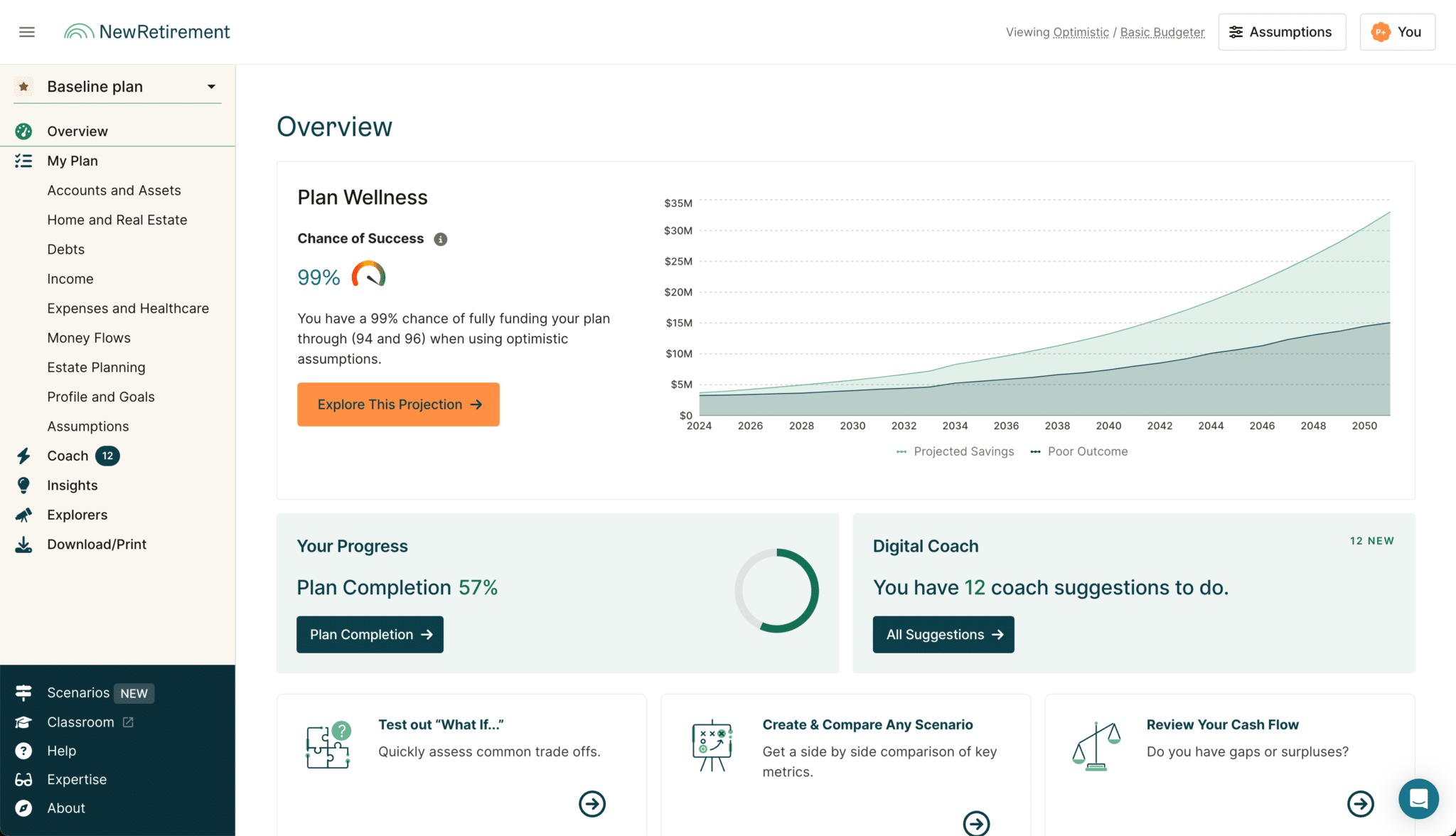

1. Boldin (Formerly New Retirement)

Boldin is designed for users who require a highly detailed, cash-flow-based retirement plan. It allows for granular modeling of almost every financial variable a retiree might face.

+-------------------------------------------------------------------------+

| BOLDIN METRICS |

+--------------------------+----------------------------------------------+

| Platform Availability | Web |

+--------------------------+----------------------------------------------+

| Pricing Model | Free basic tier |

| | PlannerPlus: $12/month ($144 billed annually)|

+--------------------------+----------------------------------------------+

| Key Strengths | Detailed Roth conversion modeling |

| | Medicare and Social Security integration |

+--------------------------+----------------------------------------------+

| Key Weaknesses | Lacks historical backtesting simulations |

+--------------------------+----------------------------------------------+Core Methodology & Features

Boldin models future income, expenses, and net worth on a monthly, annual, or one-off basis. The platform’s strength lies in its ability to handle complex, real-world variables:

- Tax Optimization: It features a dedicated Roth IRA conversion calculator, allowing users to estimate the tax impact of converting traditional pre-tax assets into tax-free Roth accounts over customized time horizons.

- Government Benefit Integration: Users can model various Social Security claiming strategies, Medicare premiums (including IRMAA surcharges), and pension options.

- Account Linking: Supports both manual entry and automated account linking to maintain real-time balances.

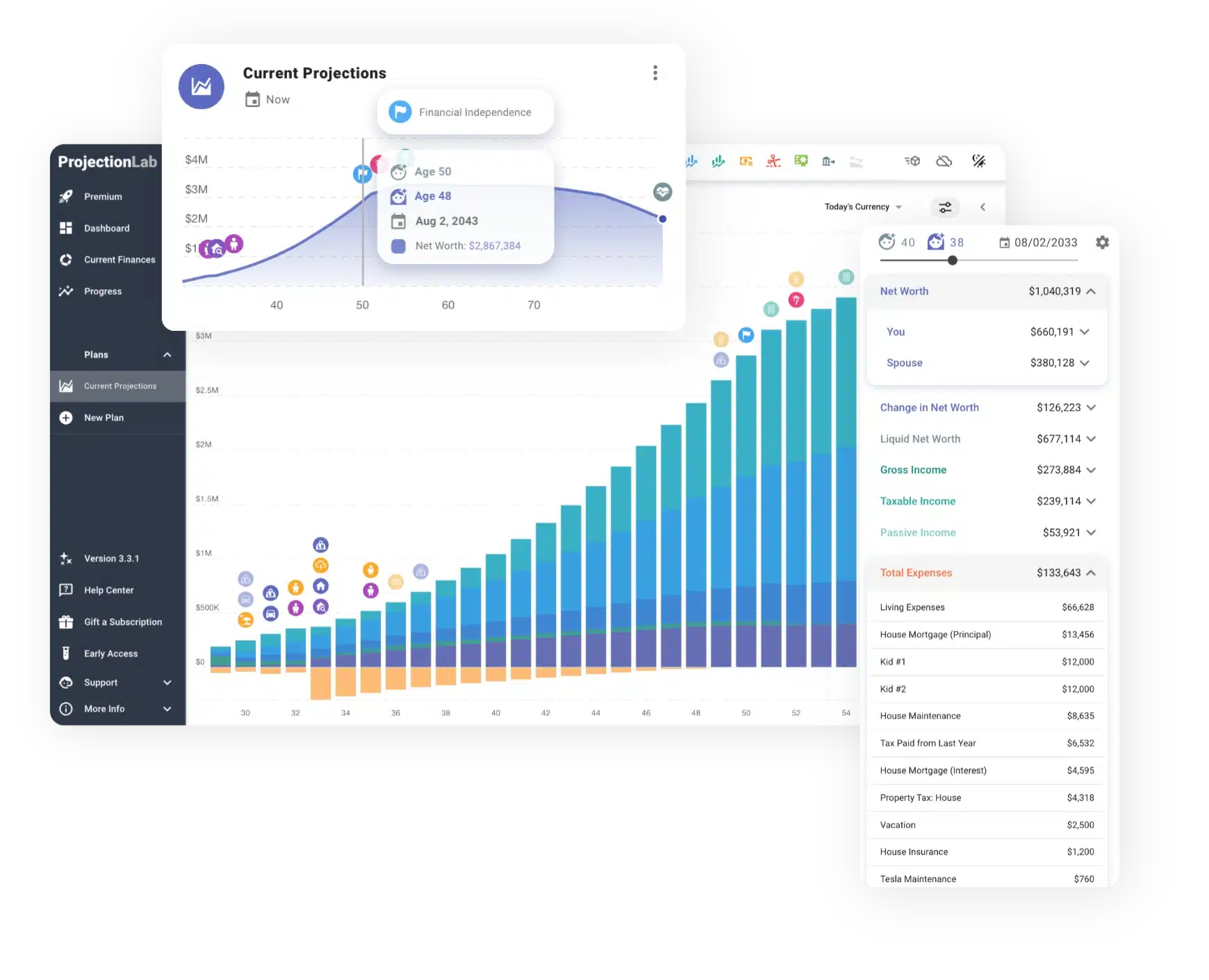

2. ProjectionLab

Created by independent developer Kyle Nolan, ProjectionLab has emerged as a favorite among tech-savvy financial planners and adherents of the FIRE (Financial Independence, Retire Early) movement. It is highly regarded for its fluid user interface, visual clarity, and analytical depth.

+-------------------------------------------------------------------------+

| PROJECTIONLAB METRICS |

+--------------------------+----------------------------------------------+

| Platform Availability | Web |

+--------------------------+----------------------------------------------+

| Pricing Model | Free basic tier |

| | Premium: $129/year |

| | Lifetime Subscription: $799 |

+--------------------------+----------------------------------------------+

| Key Strengths | Advanced "what-if" scenario comparisons |

| | Dynamic withdrawal strategy modeling |

+--------------------------+----------------------------------------------+

| Key Weaknesses | Less automated guidance; steeper curve |

+--------------------------+----------------------------------------------+Core Methodology & Features

ProjectionLab allows users to build highly customized financial plans and run simulations based on both Monte Carlo analysis and historical market backtesting.

- Dynamic Withdrawal Strategies: Unlike platforms limited to fixed spending rates, ProjectionLab can model complex withdrawal methodologies, including the traditional 4% Rule, Guyton-Klinger guardrails, and Variable Percentage Withdrawal (VPW) models.

- Comprehensive Scenario Planning: The platform’s "what-if" engine allows users to compare different life paths side-by-side, such as changing careers, purchasing real estate, or relocating to a state with different tax rates.

- Account Diversity: Models a wide array of account types, including traditional and Roth 401(k)/403(b) accounts, IRAs, Health Savings Accounts (HSAs), and taxable brokerage accounts.

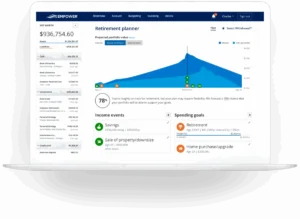

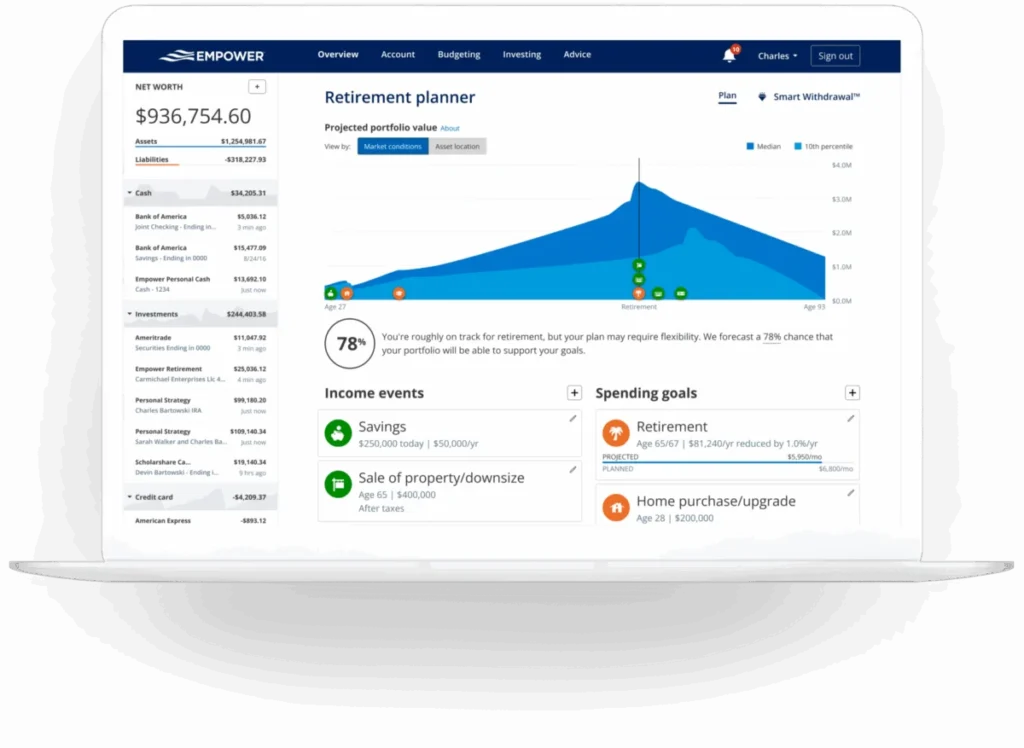

3. Empower

Empower remains the gold standard for free, consumer-facing financial tracking and basic retirement forecasting. It operates on a freemium model, providing high-quality software at no cost to attract users to its paid wealth management advisory services.

+-------------------------------------------------------------------------+

| EMPOWER METRICS |

+--------------------------+----------------------------------------------+

| Platform Availability | Web, iOS, Android |

+--------------------------+----------------------------------------------+

| Pricing Model | 100% Free |

+--------------------------+----------------------------------------------+

| Key Strengths | Automatic account aggregation and tracking |

| | Excellent investment allocation analytics |

+--------------------------+----------------------------------------------+

| Key Weaknesses | Limited customization for complex strategies |

+--------------------------+----------------------------------------------+Core Methodology & Features

Empower’s Retirement Planner is built around automated account aggregation. Once a user links their various external bank and investment accounts, the software automatically aggregates the data to build a baseline projection.

- Monte Carlo Engine: Runs 5,000 randomized market simulations to generate a "probability of success" percentage.

- Scenario Comparison: Users can easily compare a handful of macro-scenarios, such as adjusting retirement ages, changing target spending levels, or altering the timing of a major real estate sale.

- Investment Analytics: Beyond retirement planning, the tool provides robust analysis of investment fees, asset allocation, and portfolio sector drift.

4. MaxiFi

MaxiFi approaches retirement planning through the lens of academic financial economics. Developed by Boston University economics professor Laurence Kotlikoff, the software eschews traditional target-spending methodologies in favor of "consumption smoothing."

+-------------------------------------------------------------------------+

| MAXIFI METRICS |

+--------------------------+----------------------------------------------+

| Platform Availability | Web |

+--------------------------+----------------------------------------------+

| Pricing Model | Annual subscription (No free trial) |

+--------------------------+----------------------------------------------+

| Key Strengths | Rigorous, economically sound calculations |

| | Maximizes living standard over lifetime |

+--------------------------+----------------------------------------------+

| Key Weaknesses | Steep learning curve; less intuitive UI |

+--------------------------+----------------------------------------------+Core Methodology & Features

The core philosophy of MaxiFi is that individuals instinctively want to maintain a consistent standard of living (consumption) throughout their lives, adjusting for inflation, family size, and housing changes.

- Consumption Smoothing: Instead of asking the user how much they want to spend in retirement, MaxiFi calculates how much the user can spend each year, starting today, to ensure they never face a sudden drop in their standard of living.

- Behind-the-Scenes Optimization: The software performs thousands of complex, simultaneous calculations to identify optimal tax planning strategies, optimal Social Security claiming ages, and ideal withdrawal sequences.

- Rigorous Framework: Because it is designed around strict economic principles, it is highly structured and can be more difficult for casual users to navigate compared to more visual, cash-flow-based tools.

Methodological Comparison: How the Engines Calculate the Future

To understand why different tools produce different outcomes, we must look at how they process information. Below is a comparative overview of how these four tools approach key planning variables:

| Feature/Methodology | Boldin | ProjectionLab | Empower | MaxiFi |

|---|---|---|---|---|

| Primary Calculation Engine | Deterministic cash flow / Monte Carlo | Monte Carlo / Historical backtesting | Monte Carlo | Consumption smoothing algorithms |

| Tax Analysis | Highly detailed (State & Federal, Roth conversions) | High (State & Federal tax brackets) | Moderate (Estimated average tax rates) | Extremely high (Proprietary economic tax optimization) |

| Social Security Modeling | Detailed claiming age comparisons | Basic claiming inputs | Basic claiming inputs | Advanced optimization algorithms |

| Account Aggregation | Yes (via Plaid/Yodlee) | Manual or Plaid integration | Yes (Robust multi-account syncing) | Manual entry primary |

| User Interface Style | Form-driven, modular wizards | Interactive dashboards and charts | Clean, high-level consumer dashboard | Text-heavy, input-form tables |

Official Responses and Industry Perspectives

Financial planning professionals generally welcome the rise of sophisticated consumer software, but they express caution regarding how these tools are used.

Many Certified Financial Planners (CFPs) point out that while these tools are excellent for quantitative modeling, they cannot address the qualitative aspects of retirement planning. A software program can calculate the optimal mathematical age to claim Social Security or convert a Roth IRA, but it cannot assess a user’s emotional tolerance for market volatility or personal health realities.

Furthermore, industry analysts warn of the "black box" problem inherent in proprietary software. Because users rarely understand the underlying code or assumptions of a given calculator—such as how the software projects future inflation or handles asset allocation changes over time—they can easily fall victim to the "garbage in, garbage out" trap. A minor error in a user’s inputted inflation rate or tax bracket can lead to a projection that is off by hundreds of thousands of dollars over a thirty-year retirement horizon.

Implications for Future Retirees

The democratization of sophisticated financial planning software has profound implications for the wealth management industry and individual investors alike.

The Rise of the "Validator" Client

Historically, investors hired financial advisors to build retirement plans from scratch. Today, consumers are increasingly using tools like Boldin or ProjectionLab to build their own baseline plans, and then hiring flat-fee or hourly CFPs simply to validate their work. This shift is putting downward pressure on traditional assets-under-management (AUM) advisory fees.

The Value of Multi-Tool Stress Testing

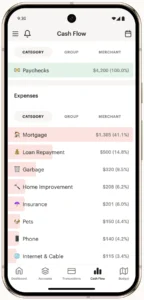

Because no single tool is perfect, the safest path for self-directed investors is to use a multi-tool approach:

- Use Empower for real-time portfolio tracking, fee analysis, and high-level asset allocation checks.

- Use Boldin to map out granular, year-by-year cash flows, plan for healthcare expenses, and evaluate Roth IRA conversions.

- Use ProjectionLab to stress-test the plan against historical market crises and model advanced withdrawal guardrails.

- Use MaxiFi to determine an economically sound baseline standard of living and optimize Social Security claiming strategies.

Ultimately, these platforms are not crystal balls; they are dynamic modeling engines. Their true value lies not in predicting the exact day an investor can retire, but in helping users understand how different variables—spending, savings, taxes, inflation, and market returns—interact to shape their financial future.