Dispelling the "Relentless Beg": Why Aging Boomers Won’t Crash the Stock Market

[DATELINE] New York, NY – June 18, 2026 – For over a decade, financial markets have largely benefited from a phenomenon dubbed the "Relentless Bid." This continuous influx of capital into equities, primarily driven by tax-deferred retirement accounts like 401(k)s and the consistent investment habits of the Baby Boomer generation, has been credited with supporting stock prices and dampening volatility. However, as the demographic tide turns and Baby Boomers increasingly enter retirement, a new concern is emerging among investors: the potential for a "Relentless Beg," or "Relentless Ask," where a mass sell-off by aging retirees could significantly depress stock valuations.

This anxiety, frequently voiced by readers and market observers alike, posits that as target-date funds automatically shift assets from stocks to bonds for older investors, and as Required Minimum Distributions (RMDs) mandate withdrawals from retirement accounts, a cascade of selling could overwhelm buying demand. Yet, leading financial strategists and economists largely dismiss the notion of an impending market collapse solely due to aging demographics, citing several structural and generational counter-currents that are expected to mitigate, if not entirely offset, this theoretical selling pressure.

The Genesis of the "Relentless Bid"

The concept of the "Relentless Bid" gained prominence around 2014, articulated by financial experts like Josh Brown. It described a powerful, underlying force in the stock market: the steady, almost automatic buying of equities. This wasn’t merely speculative trading but a systemic characteristic of modern investing, fueled by several key developments:

Automatic Investing Revolution

The widespread adoption of 401(k)s and similar tax-advantaged retirement plans transformed how Americans save. These plans, often coupled with employer matching contributions and default enrollment features, created a continuous, algorithm-like stream of capital into investment vehicles. This "automatic investing revolution" meant that, irrespective of daily market news or economic sentiment, a significant portion of the workforce was consistently allocating funds to diversified portfolios, a substantial part of which was directed towards equities.

Technological Advancements and Lower Costs

Improvements in financial technology drastically reduced transaction costs and made investing more accessible. The proliferation of low-cost index funds and exchange-traded funds (ETFs) allowed investors to gain broad market exposure efficiently, further channeling funds into stocks without requiring active, discretionary decisions from individual investors or their advisors.

Longevity and Investment Horizons

Advisors, armed with actuarial tables demonstrating increased life expectancies, began to allocate a gently but consistently higher proportion of client assets towards equities. The understanding was that clients, living longer than ever, required sustained portfolio growth to outpace inflation and ensure financial security throughout extended retirement periods. This long-term perspective naturally favored growth assets like stocks.

At the forefront of this trend were the Baby Boomers, born between 1946 and 1964. Having participated in this automatic investing revolution for decades, often during periods of robust economic growth and market appreciation, they accumulated unprecedented levels of wealth.

The Accumulation of Generational Wealth: Boomers at the Zenith

The Baby Boomer generation stands as the wealthiest generation in history, a testament to their long tenure in the workforce and their extensive participation in the capital markets. Their financial dominance is staggering, with profound implications for the economy and investment landscape.

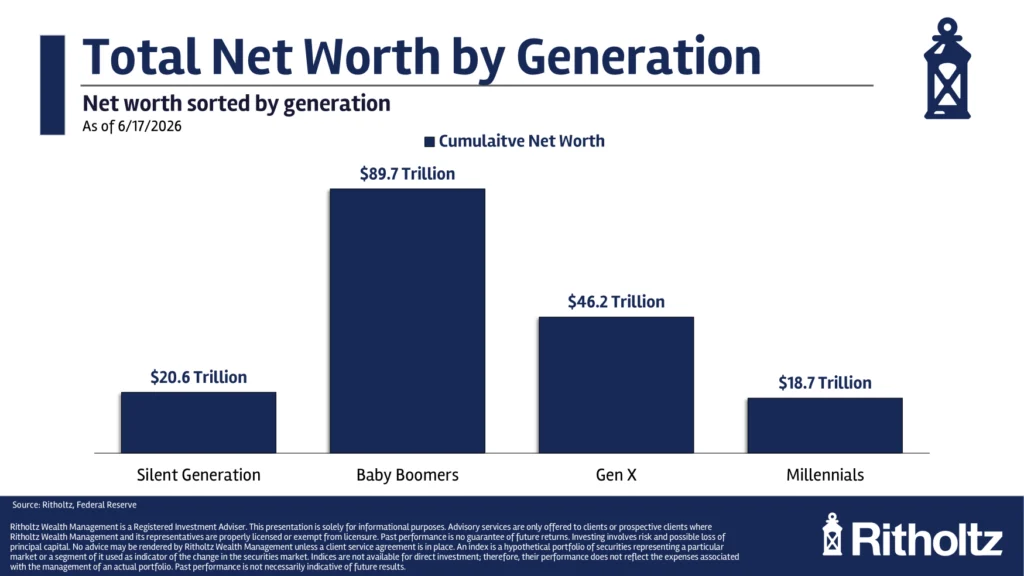

Unprecedented Net Worth

As of mid-2026, Baby Boomers control an estimated $90 trillion in total net worth. This figure is likely an underestimate, as substantial wealth is continually being transferred from the even older Silent Generation (those aged 81 and above), who currently hold around $20 trillion in assets. Much of this intergenerational transfer flows directly to Baby Boomers, pushing their effective wealth closer to $100 trillion.

Dominance in Key Asset Classes

This colossal wealth is not merely theoretical; it translates into tangible control over significant segments of the economy. Baby Boomers and older generations collectively own nearly 70% of all stocks. Furthermore, they control approximately half of all housing market wealth. This concentration of assets means that their investment and spending patterns have disproportionately influenced market dynamics for many years. Their sustained buying power has been a critical component of the "Relentless Bid," contributing to both asset price appreciation and reduced market volatility.

The Looming Specter of the "Relentless Beg"

The concerns about a "Relentless Beg" are not without a logical foundation. The sheer scale of Baby Boomer wealth, combined with the immutable laws of demographics, suggests that a significant portion of this capital will eventually need to be liquidated.

Demographic Reality

The oldest Baby Boomers are now in their early 80s, while the youngest are entering their 60s. Many have already retired, with an estimated 40 to 50 million Baby Boomers currently out of the workforce. As individuals age, their financial planning often dictates a shift towards more conservative asset allocations, typically moving from stocks to bonds, particularly within target-date funds designed to de-risk portfolios closer to retirement.

Required Minimum Distributions (RMDs)

Furthermore, federal regulations mandate Required Minimum Distributions (RMDs) from traditional tax-deferred retirement accounts once individuals reach a certain age (currently 73, though it has shifted over time and is subject to future changes). These RMDs necessitate the withdrawal of a specified percentage of account balances annually, regardless of market conditions or personal spending needs. For many, these withdrawals require selling underlying assets, including stocks.

The fear, therefore, is that the combined effect of target-date fund rebalancing, individual de-risking strategies, and mandatory RMDs could trigger a sustained wave of selling pressure that current market demand might struggle to absorb, potentially leading to a significant downturn.

Expert Analysis: Debunking the Cataclysmic Forecast

Despite the logical appeal of the "Relentless Beg" hypothesis, a closer examination by financial strategists reveals several powerful counterarguments that suggest the fears of a market crash driven by aging demographics are largely overblown.

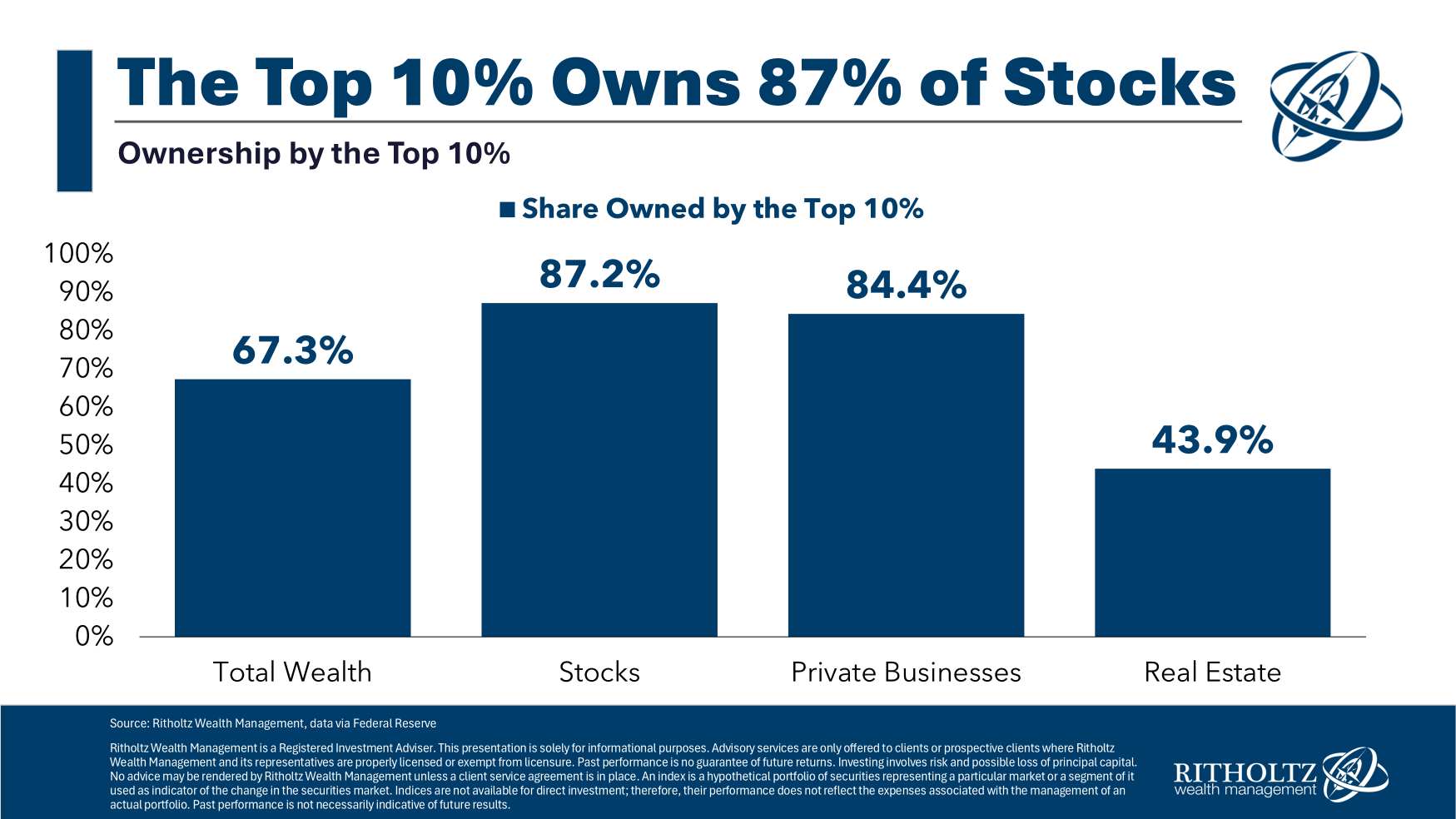

1. Concentration of Wealth and Intergenerational Transfer

One of the most critical factors often overlooked is the extreme concentration of wealth within the top echelons of society. Data consistently shows that the wealthiest 10% of households control a disproportionate share of assets: approximately 87% of all stocks, nearly 85% of private businesses, and close to 70% of total wealth.

This concentration fundamentally alters the narrative of mass liquidation. The ultra-wealthy, who hold the vast majority of financial assets, are typically not liquidating their portfolios en masse to fund retirement lifestyles. Instead, a significant portion of this wealth is managed with an eye toward intergenerational transfer. It is passed down to heirs, often through trusts, foundations, or direct inheritance, rather than being spent down entirely. While some selling will occur to fund opulent lifestyles or philanthropic endeavors, the sheer volume of assets intended for legacy planning far outweighs the portion earmarked for consumption.

Moreover, the spending that does occur through RMDs or retirement withdrawals is not "lost" to the economy. It is recycled. Baby Boomers’ consumption habits continue to fuel corporate revenues and economic activity. This spending, rather than being a drain, contributes to the very corporate earnings that underpin stock valuations. The process of spending down assets is also a "glidepath," occurring gradually over decades, rather than a sudden, synchronized sell-off.

2. Longevity and the Enduring Need for Risk

Another powerful counter-argument stems from the dramatic increase in life expectancy. For a 65-year-old couple in 2026, there is a statistically significant 64% chance that at least one spouse will live into their 90s. This extended lifespan fundamentally reshapes retirement planning.

Retiring in one’s early to mid-60s now means potentially needing a portfolio to last for 20, 30, or even 40 years. Such a long investment horizon necessitates continued exposure to growth assets to combat the corrosive effects of inflation and ensure the portfolio can sustain a desired standard of living. Purely conservative allocations, heavily weighted towards bonds, often struggle to generate the real returns needed over such extended periods.

Consequently, many retirees, even those well into their retirement years, continue to hold a significant portion of their assets in equities. They recognize the need to take calculated risks to hedge against the "inflationary beast" and ensure their wealth outlives them. Stocks, despite their volatility, remain a crucial component of diversified retirement plans designed for longevity.

3. The Millennial Counterbalance: A New Wave of Buyers

Perhaps the most compelling demographic counter-force to the "Relentless Beg" is the rise of the Millennial generation. While Baby Boomers (around 70 million strong today) are projected to decline by roughly 16 million by 2035 and another 24 million by 2045, the Millennial generation presents a formidable offset.

Comprising approximately 73 million individuals, Millennials are now entering their prime earning years. The largest population group this year is aged 33 to 37, representing a demographic bulge that is rapidly accumulating wealth and increasing its participation in financial markets. This generation is demonstrating a strong propensity for investing, often at earlier ages and in greater numbers than Baby Boomers did at comparable stages of their lives, thanks to widespread access to investment platforms, financial education, and a culture of automated saving.

As Baby Boomers eventually begin to spend down or transfer their assets, Millennials are poised to step up as significant buyers. Whether it’s stocks, real estate, or other financial assets, there will be a robust pool of younger, accumulating investors eager to acquire these holdings. The intergenerational transfer of wealth, whether through inheritance or market transactions, is a natural economic cycle, not necessarily a destructive one.

Market Efficiency and Foresight

Finally, it is crucial to remember that financial markets are generally forward-looking and remarkably efficient. Demographic shifts, such as the aging of the Baby Boomer generation, are not sudden surprises. They are well-documented, predictable trends that have been extensively studied and discussed for decades. It is highly probable that the market has already, to a significant extent, priced in these known demographic changes. The long-term implications of these trends are constantly being factored into asset valuations, mitigating the risk of a sudden, unforeseen collapse.

Broader Implications and the Evolving Financial Landscape

The discussion surrounding the "Relentless Bid" and the potential "Relentless Beg" underscores the dynamic nature of financial markets and the profound impact of demographic shifts. While the immediate threat of a catastrophic market crash driven by aging Boomers appears overstated, the ongoing evolution of generational wealth transfer will undoubtedly shape investment strategies and economic policy for decades to come.

The continued consumption patterns of affluent retirees will influence corporate earnings and economic growth. The mechanisms of intergenerational wealth transfer—whether through direct inheritance, philanthropic endeavors, or market-based asset sales—will become increasingly scrutinized. Financial advisors will need to adapt their strategies to cater to longer retirement horizons and the unique needs of both wealth-accumulating Millennials and wealth-preserving Boomers.

These complex questions are a regular subject of discussion among financial professionals. For instance, recent episodes of "Ask the Compound" have delved into these very issues, with experts like Bill Sweet joining the conversation to address topics ranging from time management and student loan forgiveness programs to property taxes, entrepreneurial ventures, and even more bearish market predictions from figures like Ray Dalio. Such ongoing dialogues highlight the constant need for nuanced analysis in a world shaped by evolving demographics and economic forces.

In conclusion, while the transition from a "Relentless Bid" to a theoretical "Relentless Beg" might seem daunting on paper, the intricate interplay of wealth concentration, extended longevity, and the emergence of a new generation of avid investors suggests that the market is more resilient and adaptable than alarmist predictions might imply. The financial landscape is indeed changing, but it is likely to be an evolution rather than a revolution, driven by the steady hand of generational succession.