Navigating the Shifting Sands of 2026: Market Resilience, AI’s Economic Paradox, and Societal Transformation

New York, NY – July 15, 2026 – As mid-2026 unfolds, global markets and societal trends present a complex tapestry of resilience, rapid technological advancement, and profound behavioral shifts. A recent synthesis of insights, spearheaded by financial commentators Ben Carlson and Michael Batnick through their "Animal Spirits" podcast, illuminates key dynamics shaping the economic and social landscape. From surprising breadth in equity market rallies to the evolving narrative of AI’s impact on employment, and the seismic shifts brought by new healthcare innovations, the period is marked by both continuity and dramatic change.

This overview delves into the main facts, recent chronology of developments, supporting data, expert responses, and the far-reaching implications of these trends, offering a comprehensive look at the forces at play in July 2026.

Main Facts: A Mid-2026 Snapshot

The financial world in mid-2026 is characterized by several dominant narratives:

- Broad Market Strength: Despite persistent concerns about market concentration, the S&P 500’s performance is extending beyond its technology giants, with broad market indicators reaching new all-time highs.

- Equity Market Dominance: The U.S. stock market has solidified its position as an unprecedented component of household net worth, leading some to deem it "too big to fail" and a critical pillar of the national economy.

- AI’s Unforeseen Employment Impact: Contrary to widespread early fears, artificial intelligence is currently perceived by some industry leaders as a net job creator, prompting a re-evaluation of its economic integration.

- Shifting Wage Dynamics: A notable convergence in year-over-year wage growth between higher- and lower-income households suggests a rebalancing in the labor market.

- Healthcare Revolution: GLP-1 medications for weight loss have seen an explosive surge in adoption, indicating a significant, rapid transformation in public health and consumer behavior.

- Evolving Entertainment Consumption: Streaming platforms continue to grapple with audience retention challenges, highlighting the cutthroat nature of the content industry.

- China’s Semiconductor Ascent: China is aggressively building its domestic semiconductor industry, rapidly emerging as a global powerhouse in this critical technological sector.

Chronology: A Week of Market Insights and Tech Revelations

The past week, culminating on July 15, 2026, has seen a flurry of data and commentary underscore these prevailing themes:

Early July (July 6-7, 2026):

- Streaming Content Challenges Emerge: On July 6, Anish Moonka highlighted a stark contrast in audience retention for streaming services. While Netflix’s live-action adaptations like "Avatar" and "Beef" saw significant audience drop-offs (59% and 58% respectively, with "A Good Girl’s Guide to Murder" losing 80%), HBO’s "The Last of Us" returned after a two-year hiatus with an increased viewership. This data point immediately sparked discussions about content quality, subscriber loyalty, and the efficacy of different release strategies in the saturated streaming market.

- The Stock Market’s Indispensable Role: On July 7, Eric Balchunas, a prominent ETF analyst, published a widely discussed note positing that the U.S. stock market has become "arguably too big and too important to fail." He underscored its role as "America’s retirement fund" and even suggested its potential to shore up Social Security, which faces long-term solvency challenges. This commentary reflects a growing awareness of equities’ systemic importance beyond mere investment vehicles.

Mid-July (July 9-10, 2026):

- Meta Unleashes Advanced AI: On July 9, Mark Zuckerberg announced the release of Muse Spark 1.1, Meta’s latest "strong agentic and coding model." This advanced AI, available through Meta’s new Model API and Meta AI, signifies continued rapid progress in artificial intelligence, making sophisticated tools more accessible and potentially accelerating innovation across industries.

- The Stock Market as the Economy: Following Balchunas’s observations, Joe Weisenthal, a leading financial commentator, reiterated on July 10 the astounding fact that "US household exposure to equities is at a record high." He emphasized that the stock market now constitutes a "SIGNIFICANTLY greater component of total household net worth than real estate," leading him to declare, "The stock market is the economy." This perspective highlights a profound shift in wealth accumulation and economic perception.

- Narrowing Wage Gap: Also on July 10, Mike Zaccardi, CFA, CMT, presented data showing a welcome trend in wage growth. In June, higher-income households saw their after-tax wage growth ease to 4.2% year-over-year, while the lower-income cohort’s growth improved to a similar level. This convergence suggests a potential easing of income inequality pressures or a more balanced labor market recovery.

Late Week (July 11-13, 2026):

- AI’s Unexpected Job Creation: On July 11, Sam Altman, a key figure in the AI revolution, shared a surprising observation: "so far at least, i’m pretty sure AI has been net job-creating." He admitted this was contrary to his earlier, albeit less pessimistic, expectations, suggesting that the current level of AI capability had yet to manifest significant job displacement.

- Demystifying Job Trends: Conor Sen, an economic analyst, provided a counter-narrative on July 11 regarding professional and business services jobs. He argued that the year-over-year growth in this sector "looks a lot more like ‘Pandemic overhiring bullwhip/normalization’ than anything related to AI," suggesting that recent job fluctuations are more about post-pandemic adjustments than immediate AI impacts.

- Broad Market Momentum Continues: On July 13, Alfonso De Pablos, CMT, provided reassuring signals of market breadth. He reported that the S&P 500 Ex-Technology Index had closed the week at new all-time highs, and, crucially, the Advance-Decline Lines for the S&P 500, S&P 400 (mid-cap), and S&P 600 (small-cap) all pushed to fresh all-time highs. This data refutes the narrative of a market solely driven by a few mega-cap tech stocks, indicating a healthier, more widespread participation.

- Momentum Factor Correction: Concurrently on July 13, Mike Zaccardi noted that the "momentum factor had one of the largest 3-week sell-offs on record." This suggests a rotation out of previously high-flying momentum stocks, potentially into the broader market names highlighted by De Pablos.

- GLP-1 Surge Continues: On July 12 (data released July 13), Kevin Gordon reported findings from the latest Gallup survey: 11% of U.S. adults now take GLP-1 medications for weight loss, a significant jump from 3% in 2024. Furthermore, 15% reported having used the medicine at some point, an increase of 9 percentage points. This underscores the accelerating adoption and profound societal impact of these new drugs.

Supporting Data: Charts and Figures Driving the Narrative

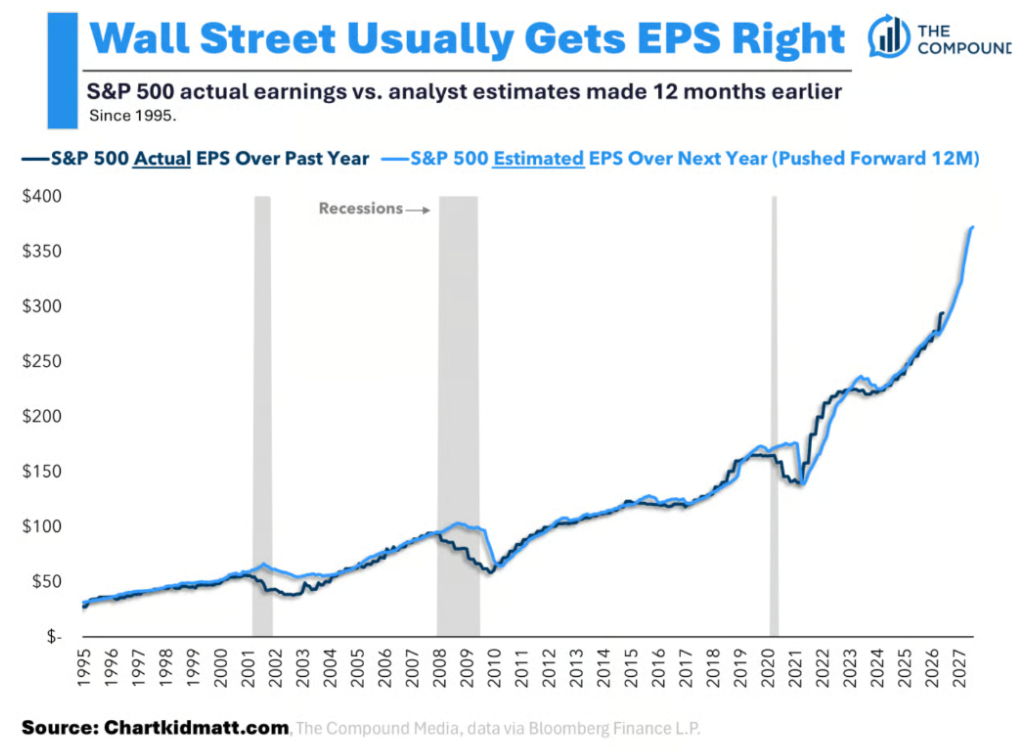

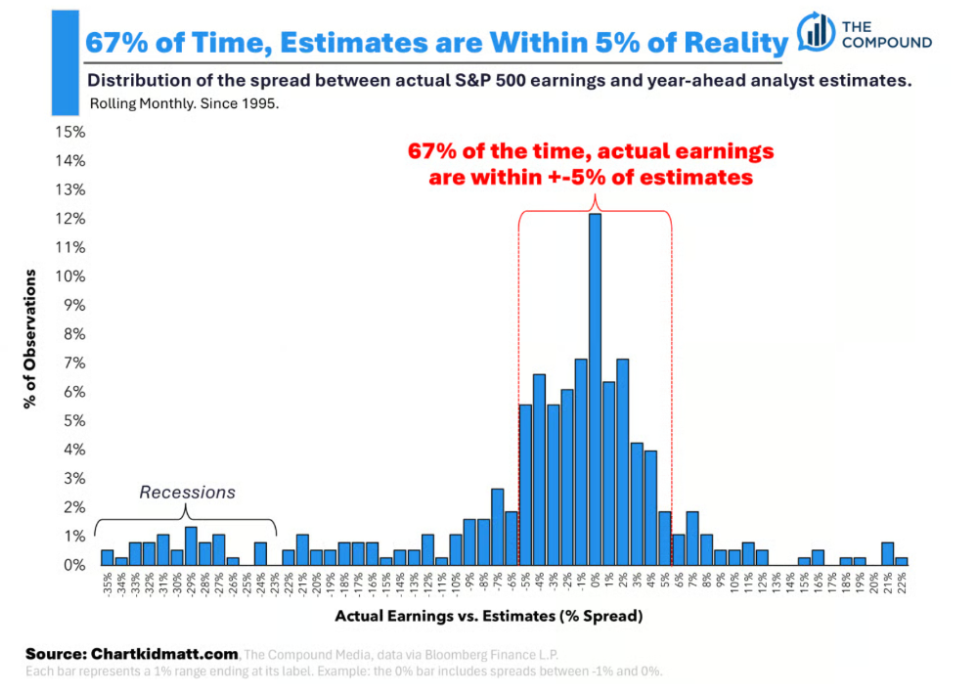

While specific chart details are not provided in the original content, the associated images and commentary clearly point to robust data supporting these trends:

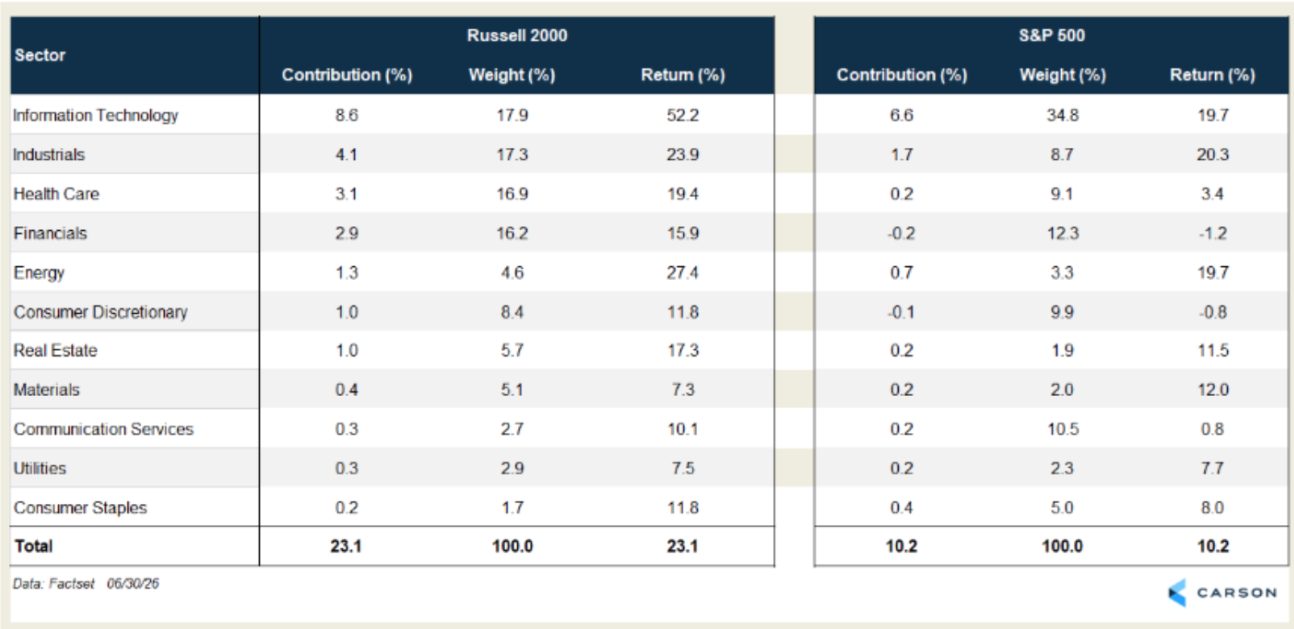

- Equity Market Breadth: Charts showing the S&P 500 Ex-Technology Index reaching new highs and the S&P 500, S&P 400, and S&P 600 Advance-Decline Lines all pushing to record levels are crucial. These visuals would demonstrate that market strength is not confined to a handful of dominant technology companies but is broadly distributed across various market capitalizations.

- Household Net Worth Composition: Visualizations illustrating the increasing proportion of U.S. household net worth allocated to equities, surpassing real estate, would dramatically support the "stock market is the economy" thesis. This data would highlight a fundamental shift in wealth accumulation strategies and the public’s direct stake in corporate performance.

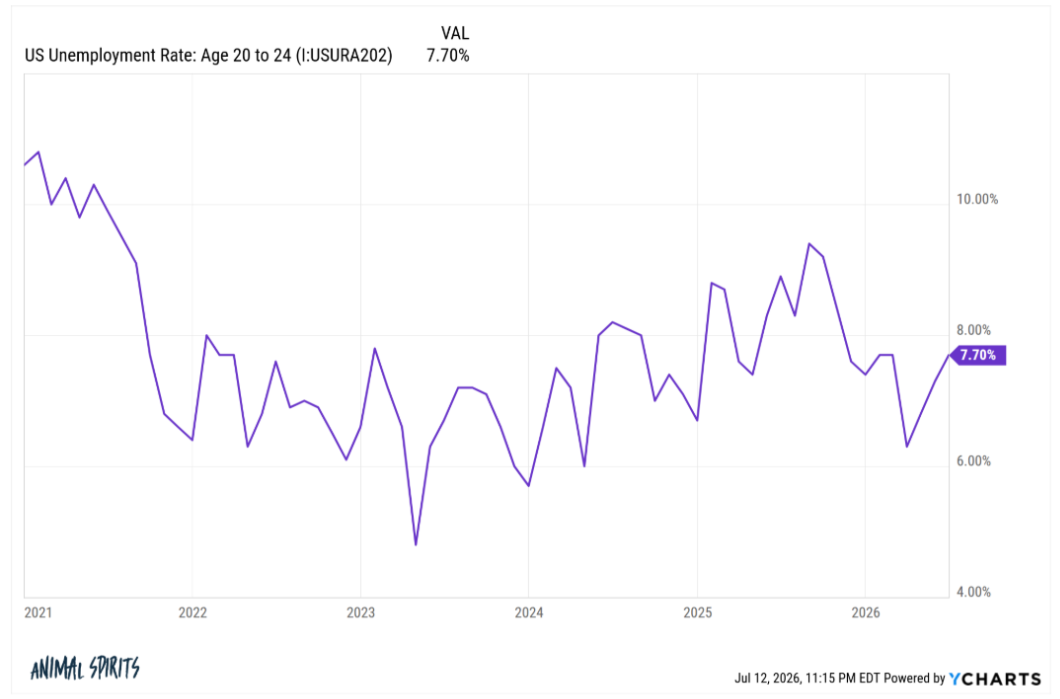

- Wage Growth Trends: Graphs depicting the year-over-year after-tax wage growth for different income cohorts, showing the convergence of higher- and lower-income groups, would provide empirical evidence for the observed rebalancing in labor market compensation.

- GLP-1 Adoption Curve: A chart illustrating the sharp upward trajectory of GLP-1 medication usage in the U.S., from 3% in 2024 to 11% in 2026, would visually emphasize the unprecedented speed of adoption for these pharmaceutical innovations.

- Professional Services Employment: Data on the year-over-year growth in professional and business services jobs, likely showing a "bullwhip" effect of overhiring followed by normalization, would offer a clearer picture of employment dynamics, differentiating them from direct AI-driven impacts.

- Momentum Factor Performance: A chart detailing the "largest 3-week sell-offs on record" for the momentum factor would visually capture the significant rotation occurring within market sectors.

Official Responses and Expert Commentary

While "official responses" from government bodies or central banks are not explicitly detailed, the commentary from leading financial experts and industry figures serves as a critical interpretive lens:

- Financial Analysts on Market Structure: Experts like Joe Weisenthal and Eric Balchunas, with their observations on the stock market’s expanding role in household wealth and its systemic importance, are effectively articulating the market’s "response" to its own growth and integration into the broader economy. Their analysis prompts a re-evaluation of how policymakers and the public perceive market stability.

- Tech Leaders on AI’s Impact: Mark Zuckerberg’s announcement of Muse Spark 1.1 represents a direct "official response" from a major tech player to the demand for advanced AI capabilities. Sam Altman’s commentary on AI being "net job-creating" serves as a significant, albeit preliminary, "official response" from the AI development community regarding its economic impact, directly challenging popular anxieties.

- Investment Community’s Reaction: The observation of a significant momentum factor sell-off by Mike Zaccardi, alongside the broad market strength noted by Alfonso De Pablos, reflects the market’s dynamic "response" to changing conditions, suggesting active portfolio rebalancing and a search for value beyond traditional growth leaders.

- Healthcare Industry Adaptation: The rapid increase in GLP-1 usage, as reported by Gallup, is not an "official response" but rather a massive consumer adoption that will undoubtedly elicit "official responses" from pharmaceutical companies (increased production, R&D), healthcare providers (new treatment protocols, insurance coverage adjustments), and even food and beverage industries (product reformulation, marketing shifts).

- China Semiconductor Strategy: The "sponsored" content from VanEck, highlighting China’s rapid semiconductor growth and the availability of the VanEck China Semiconductor ETF (SMHC), can be seen as a market-driven response to a major geopolitical and industrial trend. It signifies that the financial sector is actively providing tools for investors to gain exposure to China’s strategic push for technological autonomy. VanEck positions SMHC as a means to access 25 of the largest and most liquid Chinese semiconductor companies, underscoring the industry’s significant scale and investor interest.

Implications: Reshaping Economies and Societies

The trends highlighted by the "Animal Spirits" podcast and supporting data carry profound implications for investors, policymakers, businesses, and individuals alike.

Investment Landscape:

- Diversification and Breadth: The sustained strength in the S&P 500 Ex-Technology and the broad Advance-Decline Lines suggest that a more diversified investment approach might be prudent. The rotation out of momentum factors indicates that relying solely on past winners could be risky, emphasizing the importance of seeking opportunities across various sectors and market capitalizations.

- Systemic Risk of Equities: With the stock market constituting a larger portion of household net worth, the financial system’s stability becomes increasingly intertwined with equity market performance. This could lead to greater regulatory scrutiny and a potential "put option" from policymakers to prevent severe market downturns, given its role as "America’s retirement fund."

- Alternative Investments: The sponsorship by Nuveen, promoting "alternative investments" (nuveen.com/alternatives), signals a growing interest in asset classes beyond traditional stocks and bonds, perhaps driven by investors seeking diversification or enhanced returns in a complex market environment.

- China’s Tech Sovereignty: The rise of China’s semiconductor industry, as highlighted by VanEck, presents both opportunities and challenges. Investors looking for exposure to this rapidly growing segment can utilize specialized ETFs like SMHC, but must also weigh the geopolitical risks and regulatory environment surrounding Chinese equities. This strategic push by China has long-term implications for global supply chains and technological competition.

Economic Outlook:

- Balanced Labor Market: The convergence of wage growth between income cohorts could signify a healthier, more balanced labor market, potentially reducing inflationary pressures from wage-price spirals while supporting consumer spending across the economic spectrum.

- AI’s Evolving Role in Employment: Sam Altman’s optimistic view on AI’s job-creating potential, even if preliminary, suggests that fears of mass technological unemployment might be overstated in the short to medium term. Instead, AI could be fostering new roles, enhancing productivity, and creating entirely new industries. However, the caveat from Conor Sen about "pandemic overhiring" reminds us that not all job market shifts are AI-driven, requiring nuanced analysis.

- Productivity Gains: Advanced AI models like Meta’s Muse Spark 1.1, with their agentic and coding capabilities, are poised to unlock significant productivity gains across various sectors, from software development to research and automation, potentially driving long-term economic growth.

Societal and Consumer Behavior:

- GLP-1 Revolution: The exponential rise in GLP-1 medication usage will have profound, multi-faceted societal impacts. Beyond individual health benefits, it could reshape the food industry (demand for healthier options, reduced portion sizes), apparel (changing sizing standards), and public health infrastructure (managing side effects, long-term care, and accessibility). It represents a significant shift in how society approaches obesity and related health conditions, potentially leading to a healthier population but also raising questions about access, cost, and ethical considerations.

- Future of Entertainment: The contrasting fortunes of Netflix and HBO in audience retention underscore the ongoing challenges in the streaming wars. Content quality, brand loyalty, and effective long-term storytelling strategies are proving more critical than sheer volume. This will force streaming services to rethink their production models, distribution strategies, and how they cultivate lasting viewer engagement.

- Wealth Distribution and Policy: The increasing dominance of the stock market in household net worth raises important policy questions about retirement security, wealth inequality, and the stability of the financial system. Governments may need to consider new approaches to ensure broad-based prosperity and mitigate risks associated with highly concentrated wealth in equities.

Conclusion

The mid-2026 landscape, as illuminated by the insights curated for the "Animal Spirits" podcast, is one of dynamic evolution. The U.S. equity market demonstrates surprising breadth and systemic importance, while the AI revolution continues its nuanced dance with employment, challenging conventional wisdom. Simultaneously, breakthroughs in healthcare, particularly GLP-1 medications, are triggering a rapid transformation in public health, and the global technological race, epitomized by China’s semiconductor ambitions, intensifies. These interconnected trends demand careful observation, strategic adaptation, and a willingness to embrace a future where established norms are continually reshaped by innovation and changing economic realities.

Important Disclaimers:

Nothing in this blog constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Any opinions expressed herein do not constitute or imply endorsement, sponsorship, or recommendation by Ritholtz Wealth Management or its employees.

The Compound, Inc., an affiliate of Ritholtz Wealth Management, received compensation from the sponsor of this advertisement. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship, or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investing in speculative securities involves the risk of loss. Nothing on this website should be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product.