Navigating the Path to Stability: A Financial Case Study of a Connecticut Couple

In the heart of Connecticut, a couple is working to redefine their future. Brian and Michael, both 34, share a life centered on professional service, advocacy, and a love for their two cats. Yet, beneath the surface of their seemingly stable life—marked by steady employment in the public and non-profit sectors—lies a growing anxiety regarding personal debt and the elusive milestone of homeownership. As they approach their 10-year anniversary, they find themselves at a crossroads: how to break the cycle of "feast and famine" spending and finally unlock the next level of adult independence.

This article examines their financial profile, the challenges they face, and expert recommendations on how to transition from recurring debt to long-term wealth accumulation.

Main Facts: A Portrait of Two Professionals

Brian and Michael are established in their respective fields. Brian serves as a quality assurance manager for a state-run hospital, while Michael works as a project coordinator for a behavioral health agency serving youth, supplemented by work as a disability leadership coordinator. Their combined annual gross income sits at approximately $167,544, with a net take-home pay of roughly $109,455.

Despite these strong earnings, the couple reports feeling "behind" their peers. Their primary points of friction include:

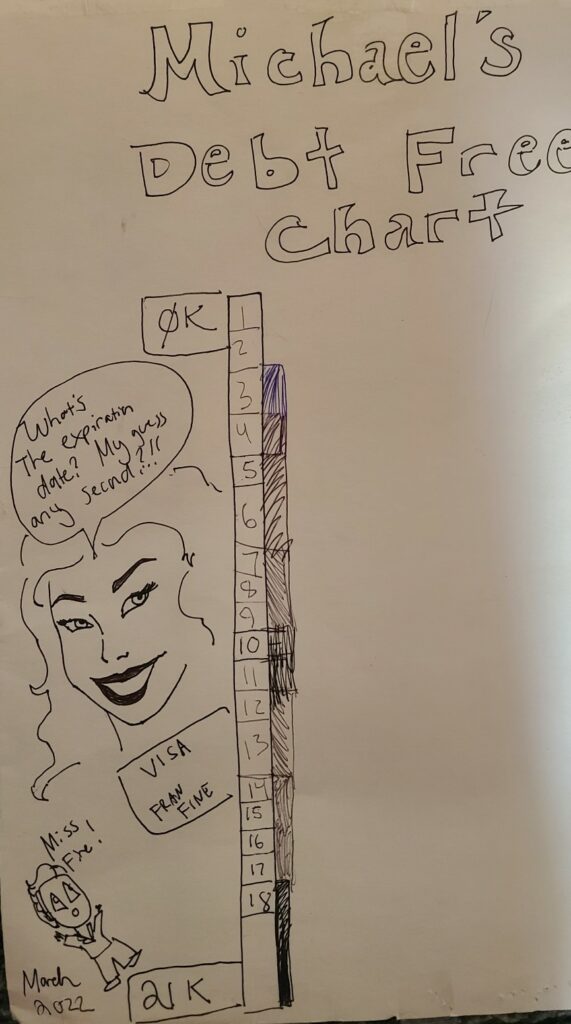

- Persistent Consumer Debt: The couple is managing $28,259 in outstanding credit card balances.

- The Rental Trap: Having been forced to relocate from a long-term, affordable studio to a more expensive, albeit beautiful, industrial-style apartment, they feel the pressure of the current housing market.

- The "Adulting" Gap: A perceived lack of progress toward homeownership and robust retirement savings has created a sense of shame and urgency.

Chronology: From Stability to Turbulence

The couple’s financial journey has been defined by a significant transition over the last 18 months.

August 2022: At this point, the couple was living in a $945/month studio, comfortably saving and planning for a future home purchase. They were debt-free (or nearly so) and were operating under a clear roadmap.

Late 2022 – Early 2023: A "perfect storm" of events upended their plans. The couple spent over three months navigating an aggressive rental market. The transition, combined with unexpected veterinary bills for their two new kittens, depleted their liquid savings and forced them to rely on credit cards.

Present Day: Having settled into a new, more expensive living space, the couple is now attempting to recalibrate. They have successfully identified their long-term goals—including marriage, starting a business, and achieving athletic success—but they feel their current debt load is acting as an anchor, preventing them from taking the next steps.

Supporting Data: The Financial Snapshot

A transparent look at their finances reveals the source of their stress.

Debt Breakdown

The couple is currently juggling three distinct credit card balances:

- Brian’s Visa (SCU): $16,057 (0% interest until Nov 2023).

- Michael’s Visa Platinum: $9,700 (10.99% interest).

- Brian’s Visa (Navy Federal): $2,503 (0.99% interest until Nov 2023).

Income and Expenses

While their annual net income is $109,455, their current annual expenditures—including debt payments—total $96,414. This leaves a surplus of roughly $13,000. However, the lack of a structured tracking system has led to "leakage" in their budget, where discretionary spending often encroaches on the funds meant for debt retirement.

Official Expert Analysis and Recommendations

Financial consultant Liz Frugalwoods, who reviewed the case, suggests that while the couple feels "behind," they are actually in a strong position. The core issue is not a lack of income, but a lack of intentional spending and a clear, unified strategy.

1. Rigorous Expense Tracking

The first mandate is the implementation of a rigorous tracking system. Using platforms like Empower (formerly Personal Capital) or traditional spreadsheets, the couple must categorize every dollar. The goal is to move from "reactive" spending to "proactive" allocation.

2. The "No-Spend" Detox

To address the debt before interest rates spike in November, the expert recommends a short-term, aggressive "spending detox." This involves:

- Eliminating Discretionary Spending: Cutting non-essential categories such as eating out, gifts, books, and hobbies temporarily.

- The "Fixed-Reduceable-Discretionary" Model: By reclassifying expenses, the expert proposed a "new" budget that could reduce their annual spending from $96,414 to approximately $79,980. This would free up an additional $4,400+ per month to be directed toward debt.

3. Prioritizing the "Safety Net"

The expert highlights that an emergency fund is not for "expected" expenses (like car repairs or pet care) but for true emergencies. Because their current cash savings of $9,000 only covers one month of expenses, they must prioritize building a 3-6 month cash buffer immediately after the debt is cleared.

4. Retirement Strategy: The "Triple Crown"

Brian’s government employment provides access to a 403b, a 457, and a pension. This is described as the "triple crown" of retirement benefits. The expert advises against prioritizing a master’s degree unless it has a guaranteed, iron-clad, and significant correlation to an increase in salary. Instead, the focus should be on maximizing contributions to these tax-advantaged accounts.

Implications for the Future

The path forward for Brian and Michael is not one of perpetual austerity, but one of calculated discipline. The expert argues that "earning more does not help if it just causes you to spend more."

The Path to Homeownership

Homeownership is a valid goal, but it is placed at the end of the priority list. Before they can responsibly enter the housing market, they must:

- Eliminate high-interest consumer debt.

- Fully fund their emergency savings.

- Establish a consistent, tax-advantaged retirement contribution habit.

Addressing the Psychological Toll

Perhaps most importantly, the analysis addresses the "shame" the couple feels. By reframing their financial situation as a "spreadsheet problem" rather than a moral failure, the couple is encouraged to stop comparing their behind-the-scenes reality to the "highlight reels" of others.

In conclusion, Brian and Michael possess the earning power to achieve their dreams. By adopting a rigid, goal-oriented budget and viewing their debt as a temporary obstacle rather than a permanent state of being, they can transition from a cycle of recurring debt to a future of security, potential, and long-term legacy. The "next level of adulting" is not about a single purchase or a specific milestone, but the disciplined, day-to-day management of their most precious resource: their income.