Beyond the Giants: S&P 500’s Broadening Rally Signals New Market Dynamics

New York, NY – June 23, 2026 – The S&P 500 Index, a bellwether for the U.S. stock market, has posted a robust 9.8% gain year-to-date through the close of markets on Monday, June 23, 2026. While this performance alone is impressive for the first six months of the year, the underlying drivers of this rally represent a significant and welcomed shift in market dynamics. For the first time in several years, the surge is not being carried by the concentrated power of a few dominant technology giants, but rather by a broad-based advance across a diverse range of companies and asset classes. This broadening of the bull market has profound implications for investors, validating long-held principles of diversification and hinting at a healthier, more sustainable growth trajectory.

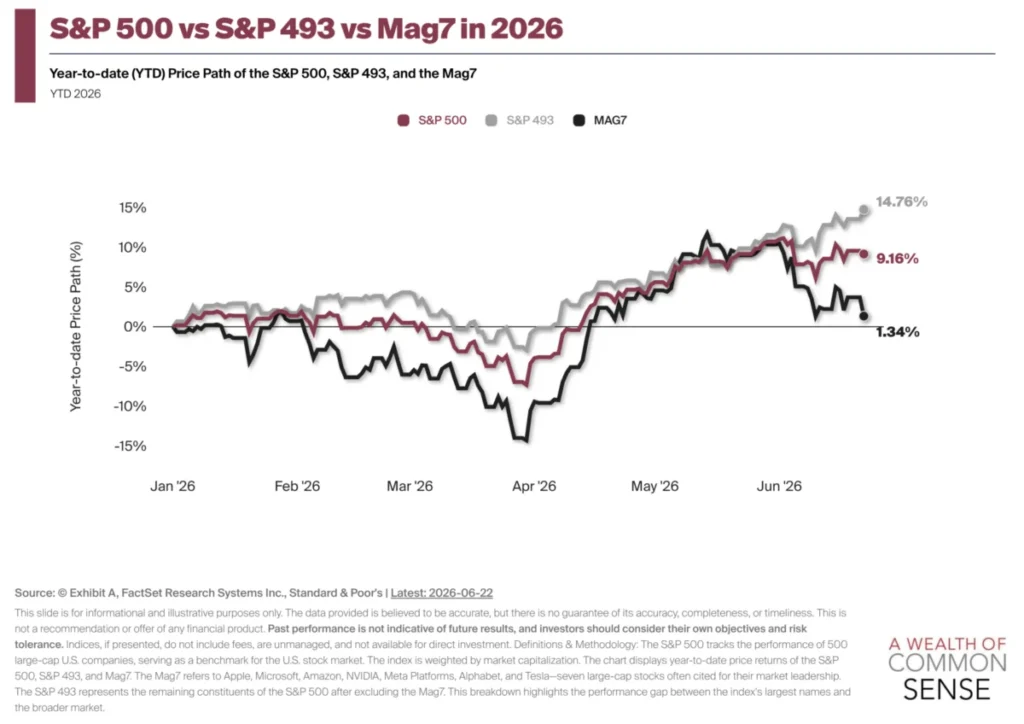

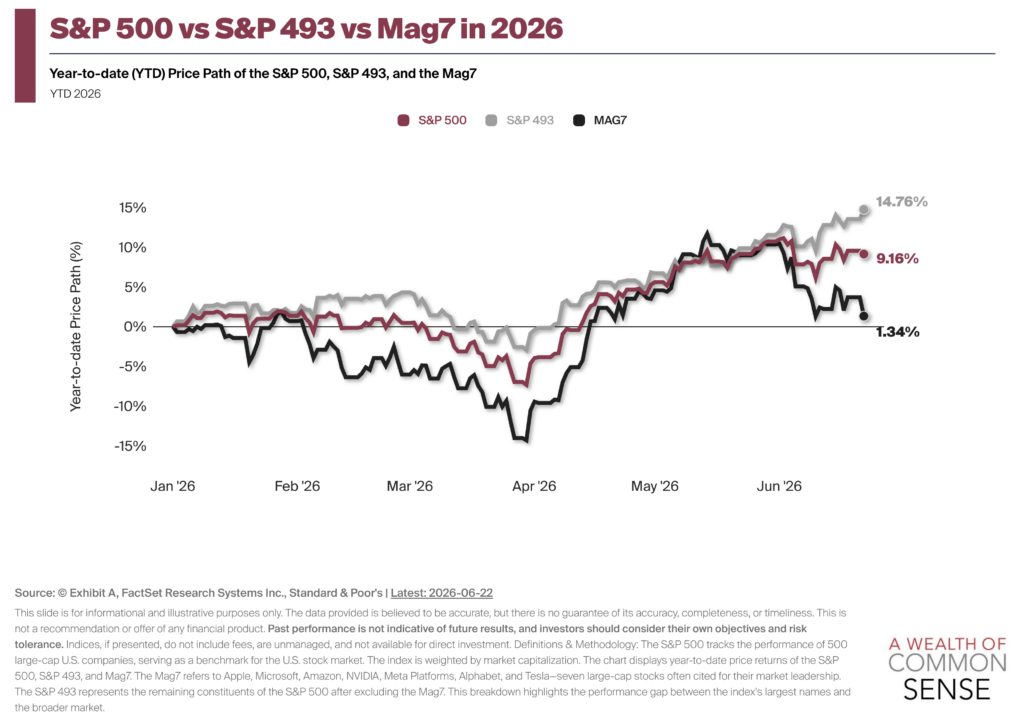

For a considerable period, market performance was largely dictated by the "Magnificent Seven" (Mag 7) – a handful of mega-cap technology and growth stocks that exerted an outsized influence on the S&P 500’s returns. However, recent data paints a dramatically different picture: the "S&P 493," comprising the remaining companies in the index, is now significantly outperforming both the full S&P 500 and the Mag 7. This reversal suggests a fundamental re-evaluation of market leadership and a potential rotation of capital into previously overlooked segments.

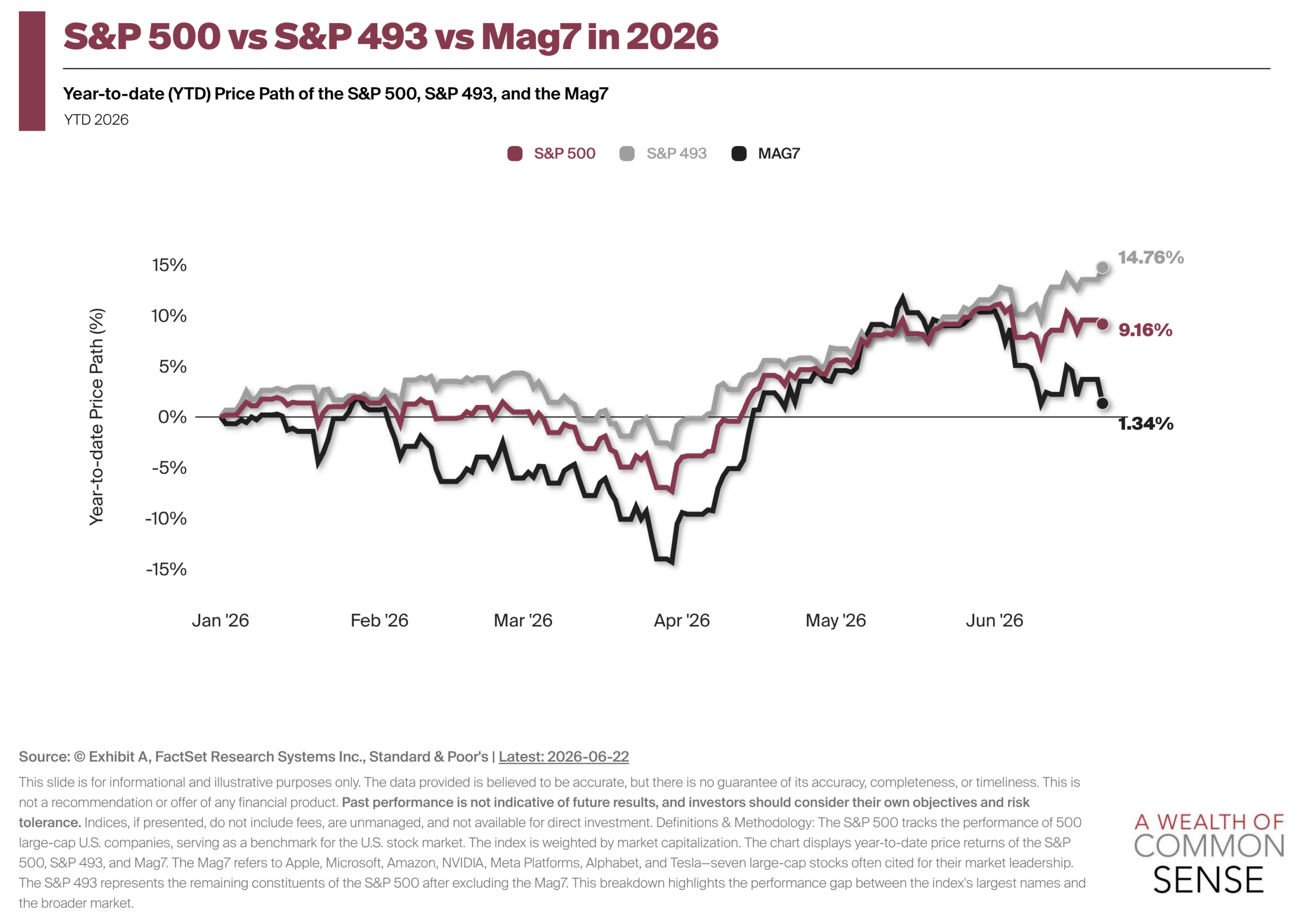

Adding to this intriguing narrative, several prominent tech stocks, including titans like Microsoft, Meta, Oracle, Netflix, Google, Amazon, and Tesla, are currently navigating what analysts describe as "relatively large corrections." Despite these headwinds from some of the market’s most influential players, the S&P 500 has managed to maintain its impressive near-10% ascent. This resilience underscores the strength and breadth of the underlying market rally, demonstrating that growth is now emanating from a much wider base.

Beyond the domestic large-cap sphere, a diverse array of other asset classes and types of stocks are also outperforming the S&P 500 this year. This includes emerging markets, small-cap value, and small-cap growth stocks, among others, marking a significant departure from previous periods of highly concentrated returns. This widespread participation is particularly good news for diversified investors, who have long grappled with the challenges posed by market concentration.

A Shifting Tide: The S&P 500’s Broadened Advance

The current market environment represents a pivotal moment, signaling a departure from the "winner-take-all" mentality that characterized recent years. The robust 9.8% year-to-date return of the S&P 500 ETF (SPY) is, by any measure, an excellent performance for a half-year period. However, the real story lies beneath the surface of this headline number.

Decoding the Mid-Year Surge

The S&P 500’s performance through mid-2026 is noteworthy not just for its magnitude but for its composition. Historically, such strong gains in major indices have often been attributable to a select few high-flying companies, creating a narrow market leadership that raised concerns about sustainability. This year, however, the narrative has shifted, suggesting a more robust and equitable distribution of gains across sectors and company sizes. This broad participation generally indicates a healthier market, less susceptible to the idiosyncratic risks associated with a few dominant players. Investors are increasingly looking beyond the familiar names, seeking value and growth opportunities in a wider array of companies that may have been overshadowed in the past.

The Vanishing Dominance of the ‘Magnificent Seven’

For years, the "Magnificent Seven" – a group of mega-cap tech companies known for their innovative power and market capitalization – were the primary engines driving the S&P 500. Their outperformance was so significant that many analysts questioned the efficacy of traditional diversification, leading some investors to ponder whether simply concentrating their portfolios in these behemoths was the optimal strategy. This year, that paradigm has been inverted.

The S&P 493, which represents the S&P 500 excluding the Mag 7, is now leading the charge, outperforming both the full index and the Mag 7 by a notable margin. This phenomenon presents a compelling irony: the very hyperscalers pouring colossal sums into artificial intelligence (AI) infrastructure and development might be inadvertently catalyzing growth across the broader market, even as their own stock prices undergo corrections. Their massive investments in AI capabilities, data centers, and advanced computing power create a ripple effect, stimulating demand for components, services, and talent from a vast ecosystem of smaller and mid-sized companies. This capital expenditure, while potentially weighing on the immediate profitability or valuation multiples of the tech giants, acts as an economic stimulus for countless other enterprises, leading to a more distributed market rally.

Tech Corrections Amidst Overall Gains

Further highlighting the market’s broadened base, several prominent technology stocks, including bellwethers like Microsoft, Meta Platforms, Oracle, Netflix, Alphabet (Google), Amazon, and Tesla, are experiencing significant corrections. These are not minor dips but "relatively large corrections," indicating a substantial pullback from their recent peaks. In previous market cycles, such a widespread downturn among major tech players would likely drag the entire S&P 500 into negative territory or severely temper its gains. Yet, the S&P 500 has managed to climb nearly 10% this year. This resilience is a testament to the strength and vitality of the other 493 companies within the index, as well as the broader market segments that are picking up the slack. It suggests that investor capital is rotating out of these momentarily struggling tech giants and into other sectors that are demonstrating stronger performance or more attractive valuations.

Chronology of a Market Metamorphosis

The shift witnessed in 2026 did not occur in a vacuum but is the culmination of evolving market dynamics and investor sentiment. Understanding the timeline helps contextualize the current landscape.

The Era of Concentration (Pre-2026)

The period leading up to 2026 was largely defined by an unprecedented level of market concentration. The "Magnificent Seven" (or similar groups like FAANG stocks) consistently delivered outsized returns, making them the primary drivers of the S&P 500’s growth. This era led to considerable anxiety among financial professionals and individual investors alike. Concerns about the market’s narrow leadership, the potential for a "tech bubble," and the impact of a few companies dominating overall returns were frequent topics of discussion. Many diversified investors found themselves questioning their strategies, as their broader portfolios often lagged behind benchmarks heavily weighted towards these high-performing tech giants. Countless conversations revolved around the perceived futility of diversification when a handful of stocks seemed to be the only game in town.

The Turning Point in 2026

The early months of 2026 appear to have marked a significant turning point. While the precise catalyst for this shift is multifaceted, it likely involves a combination of factors: a re-evaluation of valuation multiples for high-growth tech stocks, a growing recognition of undervalued opportunities in other sectors, and perhaps a rotation driven by changing macroeconomic expectations. As the year progressed, the momentum began to visibly shift away from the concentrated leadership, with a broader array of companies demonstrating stronger earnings, growth prospects, or more attractive valuations. This gradual but decisive rotation has culminated in the current scenario, where the market’s strength is derived from a much wider base.

The AI Investment Ripple Effect

The "AI trade" has been a dominant theme in recent years, with the largest technology companies investing billions, if not trillions, into developing and deploying artificial intelligence capabilities. While these investments are crucial for their long-term competitiveness, they also entail significant short-term capital expenditures and operational costs. This massive spending creates a powerful ripple effect throughout the economy. Smaller companies that supply components, provide specialized software, offer data center infrastructure, or contribute to the AI supply chain are direct beneficiaries. For example, a hyperscaler building a new AI data center requires advanced cooling systems, specialized networking equipment, construction services, and a host of other goods and services, often procured from a wide range of suppliers. This distributed demand stimulates growth across various industries, from manufacturing and infrastructure to specialized software and consulting. The irony, as noted, is that these very investments, while potentially weighing on the immediate stock performance of the tech giants themselves due to high capex or shifting profit expectations, are simultaneously fueling the broader market rally by creating economic activity and growth opportunities for hundreds of other companies.

Supporting Data: Beyond Large-Cap Tech

The quantitative evidence unequivocally supports the narrative of a broadening market. The specific data points highlight the extent of this diversification of market leadership.

The S&P 493 Takes the Lead

The starkest evidence of this shift is the superior performance of the S&P 493. This segment of the index, which excludes the Magnificent Seven, has outperformed both the full S&P 500 and the Mag 7 by a substantial margin year-to-date. This suggests a powerful reallocation of capital, where investors are actively seeking opportunities beyond the mega-cap tech stocks that previously dominated headlines and portfolios. This broader participation reduces systemic risk and indicates a more balanced assessment of value and growth across the market.

A Diverse Array of Outperformers

The trend extends beyond the S&P 500’s internal dynamics. A variety of other asset classes and market segments are currently outpacing the overall S&P 500 in 2026. This welcomed change for diversified investors indicates that strategic asset allocation is once again proving its worth. The list of outperformers includes:

- Emerging Markets (EM): These markets, often characterized by higher growth potential and lower valuations than developed markets, have shown significant strength.

- Small Cap Value Stocks: Companies with smaller market capitalizations and lower valuation multiples have experienced a resurgence, benefiting from a rotation towards value.

- Small Cap Stocks (Broad): The entire small-cap segment, often seen as more sensitive to domestic economic conditions, has been on a strong upward trajectory.

- International Developed Markets: Stock markets in regions like Europe and Japan are also showing signs of independent strength, benefiting from global economic recovery and potentially more attractive valuations.

- Commodities: Certain commodities, including energy and industrial metals, have seen strong performance, driven by supply-demand dynamics and global economic activity.

- Specific Value-Oriented Sectors: Within the U.S. market, sectors traditionally considered "value" plays, such as financials, industrials, and utilities, have seen renewed investor interest and strong performance.

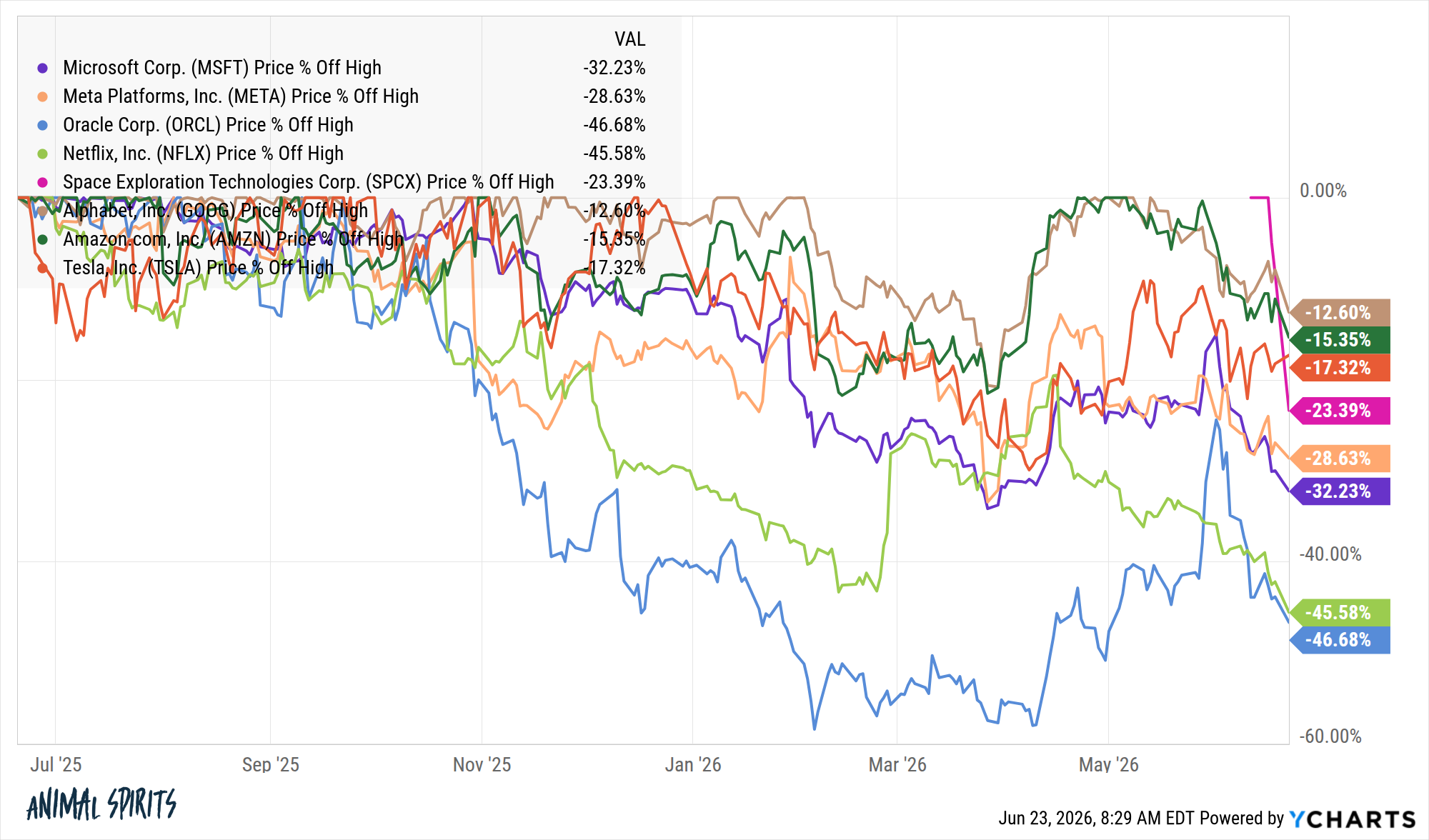

Emerging Markets’ Enduring Strength

Emerging markets, represented by ETFs like EEM, have now surpassed the S&P 500 over the past three years. This long-term outperformance is a significant development, as emerging markets have often lagged developed counterparts during periods of concentrated U.S. tech dominance. This sustained strength can be attributed to factors such as improved economic fundamentals in various emerging economies, favorable demographic trends, a rebound in commodity prices (benefiting commodity-exporting nations), and relatively lower valuations compared to overstretched developed market equities. This trend underscores the importance of a global perspective in portfolio construction.

Small Caps Reasserting Their Value

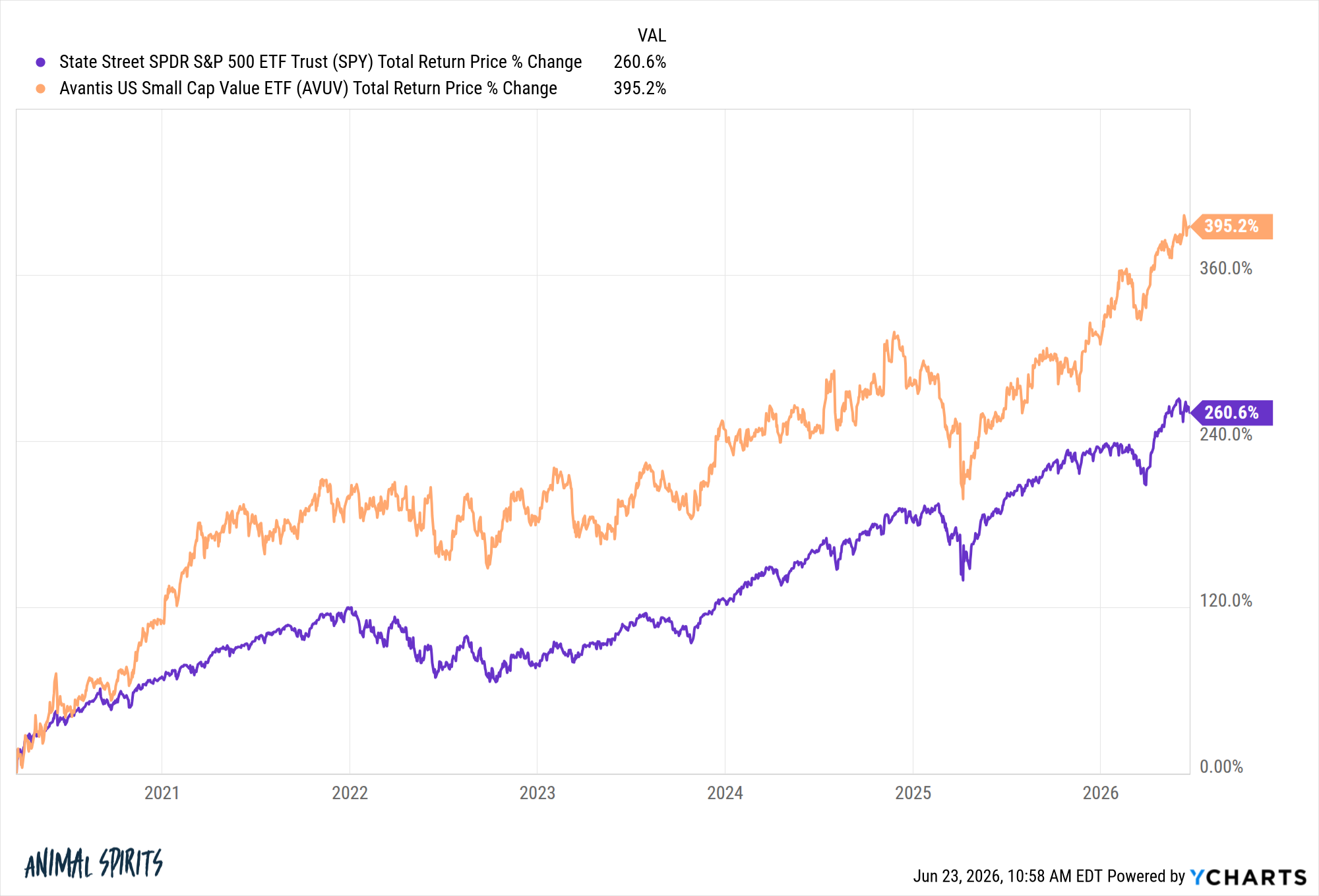

The performance of small-cap stocks, particularly small-cap value, has been exceptionally strong in recent periods. Small-cap value stocks, exemplified by ETFs like AVUV, have "crushed" the S&P 500 since the Covid lows, indicating a robust recovery and a preference for companies with strong underlying fundamentals but smaller market footprints. Similarly, broader small-cap stocks (e.g., IWM) have been "on fire" since the "Liberation Day lows," a specific market inflection point perhaps referring to a period of significant economic reopening or policy shift. This resurgence of small-cap companies often signals a healthy economic environment where growth is not solely confined to large, established players but is also thriving among smaller, agile businesses. Their performance is often seen as a leading indicator of economic vitality, suggesting confidence in broader economic expansion.

Expert Perspectives and Market Commentary

The dramatic shift in market leadership has naturally drawn significant attention from financial analysts, strategists, and economists, who are now reassessing their outlooks and portfolio recommendations.

Analysts Weigh In on Diversification

"This broadening of the bull market is precisely what diversified investors have been hoping for," states Dr. Eleanor Vance, Chief Market Strategist at Global Asset Management. "For too long, the narrative was about whether diversification was dead. This year’s performance unequivocally proves its enduring value. It’s a sign of a healthier market when gains are distributed across a wider range of companies and sectors, rather than being concentrated in a few."

Mr. David Chen, Head of Emerging Markets Research at Zenith Capital, echoes this sentiment regarding global opportunities. "The sustained outperformance of emerging markets over the past three years, now definitively beating the S&P 500, highlights a rotation towards areas offering more compelling long-term growth prospects and more attractive valuations. Investors who maintained exposure to these markets are now reaping the benefits, and we expect this trend to continue as global economic growth normalizes and capital seeks out undervalued assets."

Ms. Isabella Rossi, Senior Economist at Pantheon Research, connects the market’s shift to broader economic currents. "The market’s ability to absorb corrections in major tech stocks while still posting strong overall gains suggests a robust underlying economy. It indicates that growth is not solely reliant on innovation from a handful of tech giants but is being driven by a more diverse set of industries. This decentralization of market power often correlates with a more stable and sustainable economic expansion."

Reassessing Portfolio Strategies

Financial advisors are actively engaging with clients to discuss these new market dynamics. The prevailing advice is to review and potentially rebalance portfolios, ensuring adequate exposure to the segments that are currently outperforming or show strong potential. This might involve increasing allocations to international equities, small-cap funds, or value-oriented sectors that have lagged in recent years. The current environment reinforces the importance of strategic asset allocation and periodic rebalancing to capture opportunities across various market cycles. It’s a reminder that past performance is not indicative of future results, and market leadership can, and often does, change.

Implications for Investors and the Economy

The current market environment carries significant implications for both individual investors and the broader economy, signaling a potentially more stable and opportunity-rich period.

The Vindication of Diversification

Perhaps the most significant implication for investors is the powerful vindication of diversification. For years, as the "Magnificent Seven" soared, many investors questioned the utility of holding a broad portfolio. This period unequivocally demonstrates that diversification is not merely a theoretical concept but a practical necessity for long-term investment success. It protects against the risks associated with concentration and positions portfolios to capture gains from wherever they emerge in the market. Those who maintained diversified portfolios through the periods of concentration are now experiencing the rewards as market leadership broadens.

A Healthier Bull Market

A bull market driven by broad participation is generally considered healthier and more sustainable than one reliant on a few select companies. When gains are distributed across a wide range of sectors and company sizes, it suggests a more robust economic environment and reduces the systemic risk associated with a potential downturn in any single industry or company. This diversified growth implies that the underlying economic fundamentals are strengthening across various segments, providing a more stable foundation for continued market appreciation.

Economic Undercurrents and Sector Rotation

The rotation of capital away from mega-cap tech and into other sectors and asset classes also reflects evolving economic undercurrents. It could indicate that the market is anticipating a broader economic recovery, higher inflation, or a shift in the interest rate environment that favors value stocks, smaller companies, or international markets. For instance, a stronger global economy might boost demand for commodities and benefit export-oriented emerging markets. Similarly, rising interest rates might make financials more attractive, while increased industrial activity could benefit manufacturing and infrastructure sectors.

Navigating Future Volatility

While the broadening market is a positive development, investors must remain vigilant. Market dynamics can shift rapidly, and what performs well today may not tomorrow. The current environment calls for continued monitoring of economic indicators, corporate earnings, and global geopolitical developments. Strategic adjustments to portfolios, rather than reactive decisions, will be crucial for navigating potential future volatility and capitalizing on emerging opportunities.

The Long-Term Outlook

Looking ahead, if this trend of broadening market participation continues, it suggests a more dynamic and potentially less volatile long-term investment landscape. It offers investors more avenues for growth and better opportunities to achieve their financial goals through a well-constructed, diversified portfolio. The era of concentrated gains may be giving way to a period of more equitable growth, fostering greater confidence in the overall health and resilience of the global financial markets.

In conclusion, the S&P 500’s strong performance in the first half of 2026, driven by a broad-based rally rather than a concentrated few, marks a significant and positive shift. This diversification of market leadership, coupled with the outperformance of various other asset classes, offers renewed hope and opportunities for diversified investors. It validates the foundational principles of investing and points towards a potentially healthier and more sustainable bull market ahead.