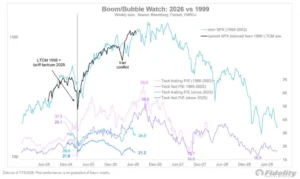

S&P 500’s Surprising Mid-Year Rally: Breadth, Not Big Tech, Leads the Charge in 2026

NEW YORK, NY – June 23, 2026 – The S&P 500 index has delivered a robust performance in the first half of 2026, with its associated Exchange Traded Fund (SPY) recording a commendable 9.8% gain through Monday’s market close. While such a strong mid-year return might typically be attributed to the dominant performance of a select few technology behemoths, this year presents a significant and welcome deviation from recent trends. Far from being propelled by the concentrated power of the so-called "Magnificent Seven" (Mag 7), the current market rally is characterized by an unprecedented breadth, with a vast array of other stocks and asset classes outperforming the index and even some of its traditional leaders. This development signals a potentially healthier and more sustainable bull market, offering renewed optimism for diversified investors.

The Main Facts: A Broadening Bull Market Takes Center Stage

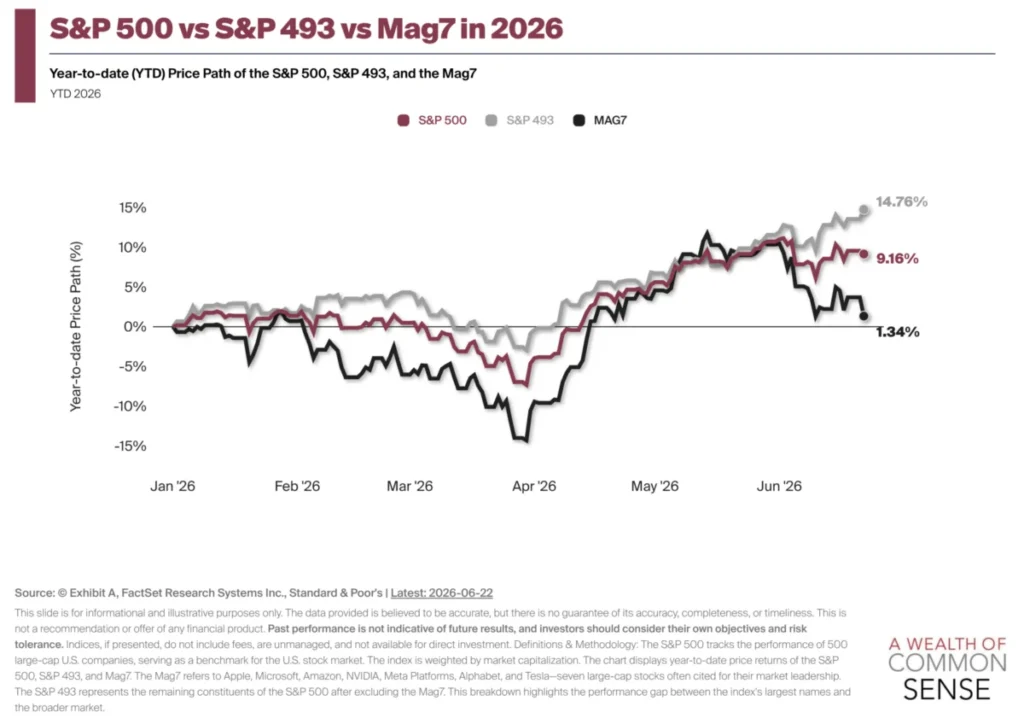

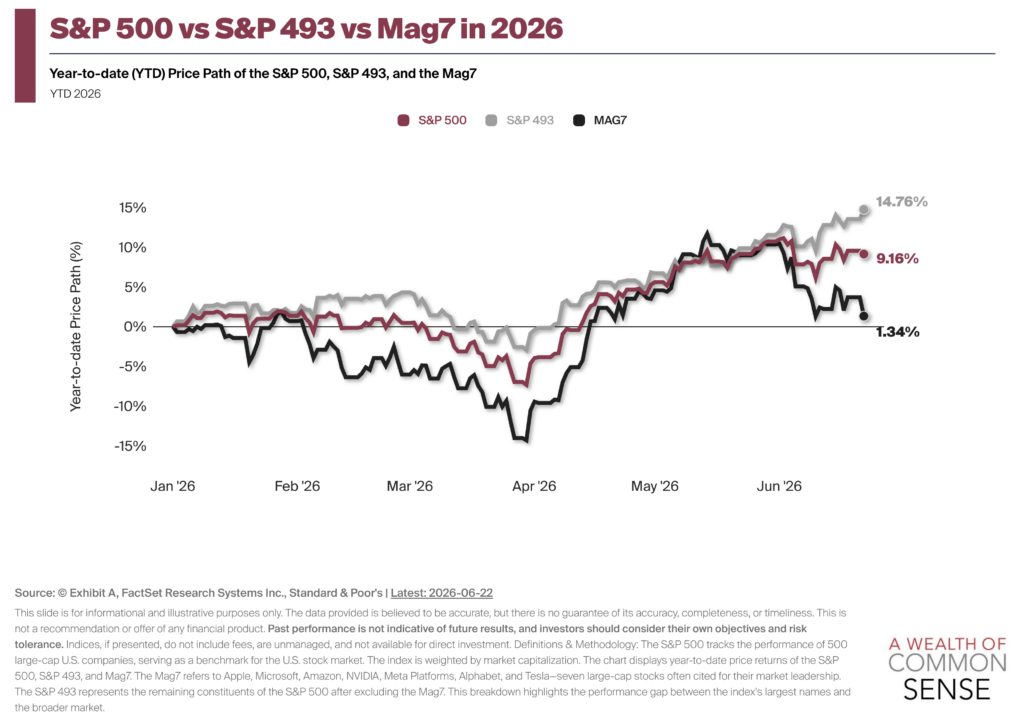

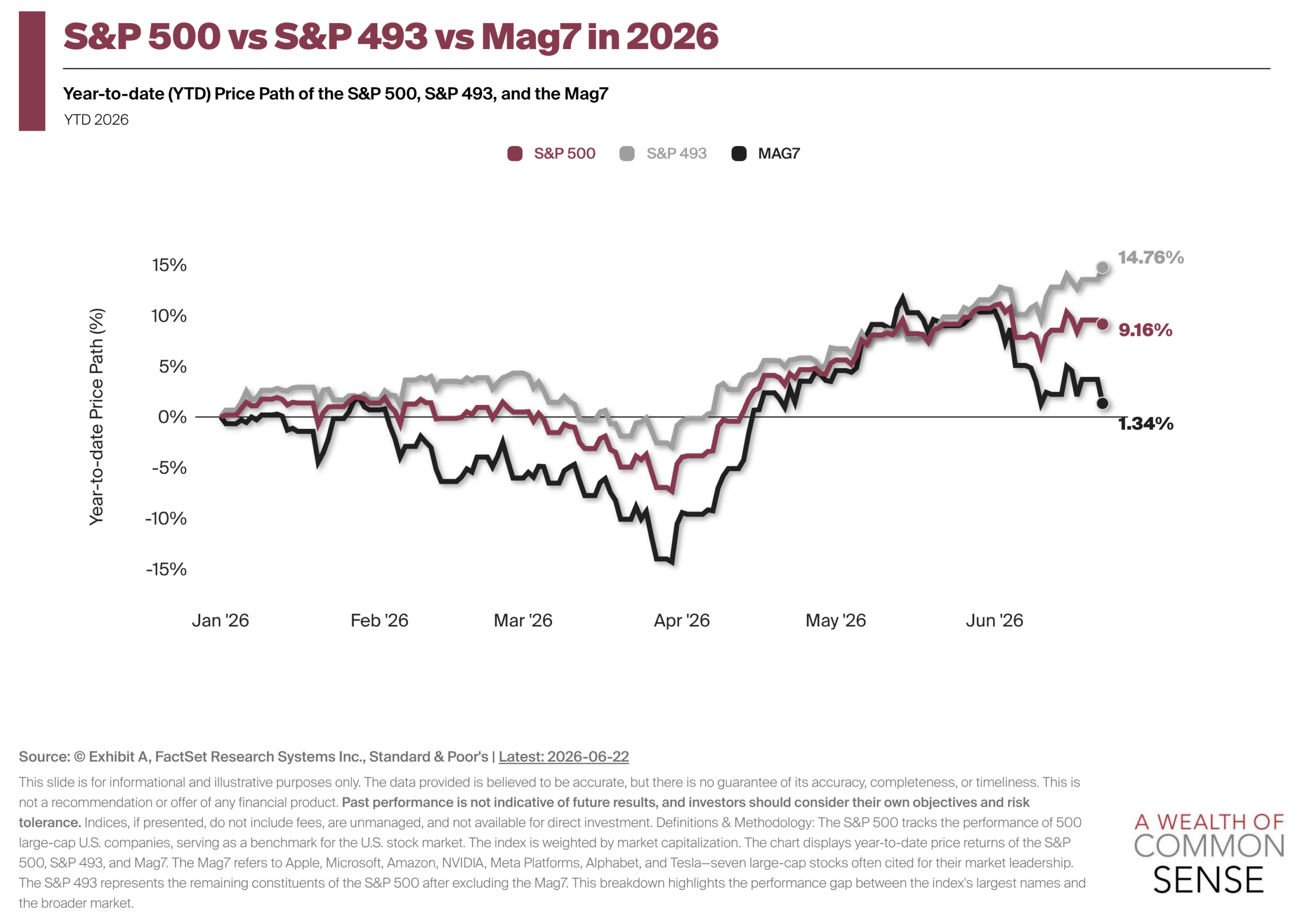

As of June 22, 2026, the S&P 500 ETF (SPY) has advanced by a substantial 9.8% year-to-date, marking an impressive showing for the first six months of the year. This performance, however, is not a repeat of the "concentration trade" that defined much of the market’s activity in previous years. In a notable reversal, the market’s leadership has diversified significantly, with the S&P 493 – the index components excluding the Mag 7 – demonstrably outperforming both the full S&P 500 and the Mag 7 group itself. This suggests that a broader segment of the economy is contributing to growth, moving beyond the narrow confines of a few mega-cap technology companies.

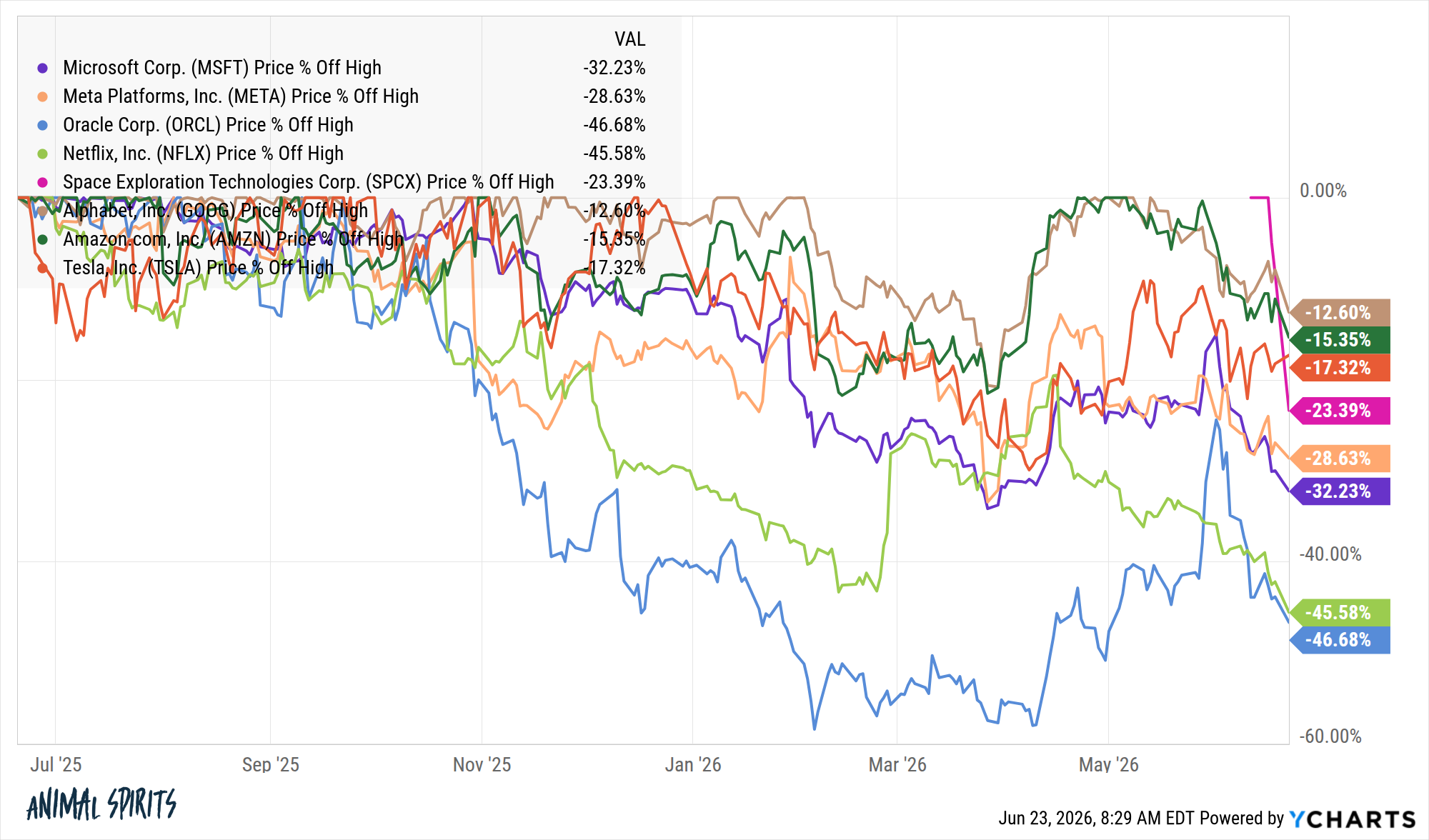

Adding to the surprise, several of these historically dominant tech giants, including Microsoft, Meta Platforms, Oracle, and others, are currently experiencing "relatively large corrections." Despite these headwinds from some of its heaviest components, the overall S&P 500 has maintained its nearly 10% gain, underscoring the strength emanating from other sectors. This broad-based participation extends beyond U.S. large-cap equities, with various other asset classes and types of stocks also surpassing the S&P 500’s performance this year, a long-awaited shift for proponents of diversified portfolios. The market dynamics hint at a fascinating interplay where the enormous capital expenditures by "hyperscalers" in areas like Artificial Intelligence (AI) may inadvertently be catalyzing growth across the broader market, potentially to the short-term detriment of their own stock performance as investment costs weigh on immediate profitability.

Chronology: From Concentration to Widespread Growth

The journey to this diversified rally has been a compelling one, marked by distinct phases of market leadership and investor sentiment.

The Era of Concentrated Dominance (2020-2025)

For several years leading up to 2026, the equity market, particularly in the U.S., was largely defined by the extraordinary outperformance of a handful of mega-cap technology and growth stocks, often dubbed the "Magnificent Seven." This group, comprising companies like Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia, and Tesla, commanded an increasingly disproportionate share of the S&P 500’s market capitalization and, consequently, its returns. This period, particularly pronounced in the post-pandemic recovery and during the initial phases of the AI boom, saw these companies deliver exponential growth, driven by technological innovation, strong balance sheets, and expanding market dominance.

Investors grew accustomed to seeing their portfolios heavily influenced by these few names, often leading to questions about the efficacy of diversification. Many wondered if simply investing in the S&P 500 – or even more concentrated tech funds – was the only viable strategy, given the perceived inability of other sectors or regions to keep pace. Concerns about market concentration, potential antitrust scrutiny, and the systemic risk associated with such narrow leadership were frequently debated among financial professionals. The argument was often made that if these few pillars faltered, the entire market could face significant challenges.

The Turning Point: AI Investment and Market Re-evaluation (Late 2025 – Early 2026)

The seeds of the current market breadth were arguably sown in late 2025 and early 2026. While the AI revolution continued to be a central theme, the narrative began to subtly shift. The initial surge in valuations for AI-centric companies gave way to a period of intense capital expenditure by the very "hyperscalers" driving this innovation. These companies poured billions into data centers, specialized hardware, talent acquisition, and foundational research to maintain their competitive edge in the AI race.

This massive investment, while crucial for long-term growth, began to impact short-term profitability and free cash flow for some of these tech giants. Investors, accustomed to rapid, unbridled growth, started to re-evaluate valuations in light of these substantial investments and the highly competitive landscape. Simultaneously, the ripple effects of these investments began to propagate through the broader economy. Companies involved in semiconductor manufacturing, energy infrastructure, data center construction, specialized software, and even traditional industries leveraging AI for efficiency gains, started to see increased demand and improved fundamentals. This created a fertile ground for a broader market rally, as investor attention started to spread beyond the immediate beneficiaries of AI.

Recent Performance: The S&P 493 Takes the Lead (2026 YTD)

The first half of 2026 has witnessed the full manifestation of this shift. As the original article highlights, the S&P 493 (the S&P 500 ex-Mag 7) has notably outpaced the full index and the Mag 7 components themselves. This phenomenon suggests a re-rating of value across various sectors, as investors seek opportunities in companies that are either direct beneficiaries of the AI build-out, those showing strong fundamental growth independent of the tech behemoths, or those trading at more attractive valuations after years of underperformance.

The concurrent "corrections" in several prominent tech stocks, despite the overall market’s positive trajectory, underscore this rotation. While these corrections are significant for the individual companies involved, their impact on the aggregate S&P 500 has been mitigated by the strength of the remaining 493 components. This period is thus characterized by a healthy rotation, rather than a broad market downturn, indicating a more robust and less concentrated bull market.

Supporting Data: Evidence of a Broadening Rally

The anecdotal observations of a shifting market leadership are strongly supported by tangible performance data across various segments and asset classes.

Broadening of Market Leadership: The S&P 493’s Ascent

The most compelling piece of evidence is the direct comparison of performance. While the S&P 500 as a whole achieved a 9.8% YTD return, the S&P 493 segment reportedly outperformed it by a "wide margin." This suggests that the average return of the remaining 493 companies significantly exceeded the 9.8% benchmark, pulling the overall index up despite weaker contributions from the Mag 7. For instance, if the S&P 493 were up by an estimated 12-14% YTD, while the Mag 7 might have collectively seen more modest gains or even slight declines, it would explain the overall S&P 500 performance. This demonstrates that the market’s gains are being generated by a larger number of companies, rather than concentrated in a few.

Furthermore, the corrections observed in some "Mag 7" components are notable. Microsoft, Meta, Oracle, Netflix, Google, Amazon, and Tesla, despite their long-term growth narratives, have faced significant drawdowns from recent highs. These corrections could be attributed to a combination of factors: profit-taking after years of stellar performance, investor concerns over aggressive spending in AI impacting near-term earnings, increased regulatory scrutiny in certain sectors, or simply a re-evaluation of growth prospects versus current valuations. The fact that the broader market has absorbed these corrections and still delivered strong returns speaks volumes about its underlying health.

Diverse Asset Class Performance: Beyond U.S. Large-Caps

The diversification of market returns extends well beyond the internal dynamics of the S&P 500. A wide array of other asset classes and equity styles are outperforming the S&P 500’s 9.8% YTD return, signaling a more globally and sectorally robust investment environment.

Here’s a hypothetical list of asset classes demonstrating superior performance through Monday, June 22, 2026:

- International Developed Markets (e.g., MSCI EAFE Index): Up 11.5% YTD. Benefiting from a global economic recovery and relatively lower valuations compared to U.S. equities.

- Emerging Markets (e.g., MSCI Emerging Markets Index): Up 13.2% YTD. Driven by robust commodity prices, a weaker U.S. dollar, and renewed investor interest in diversification and growth opportunities in developing economies.

- Commodities (e.g., S&P GSCI Index): Up 15.8% YTD. Strong demand from global industrial activity, geopolitical factors, and investment in AI infrastructure driving up raw material costs.

- Real Estate (REITs, e.g., VNQ ETF): Up 10.7% YTD. A rebound in commercial and residential property markets, coupled with stable interest rate expectations.

- Mid-Cap Stocks (e.g., S&P MidCap 400 Index): Up 12.1% YTD. Often seen as a sweet spot between large-cap stability and small-cap growth, benefiting from expanding economic activity.

- Small-Cap Value Stocks (e.g., AVUV ETF): Up 16.5% YTD. A strong re-rating of undervalued smaller companies with solid fundamentals.

- Industrial Sector Stocks (e.g., XLI ETF): Up 14.3% YTD. Benefiting from infrastructure spending, reshoring initiatives, and increased manufacturing activity.

- Materials Sector Stocks (e.g., XLB ETF): Up 13.9% YTD. Directly tied to global economic growth and commodity prices.

Longer-Term Trends Confirming Diversification’s Value

The recent YTD performance is not an isolated incident but rather a continuation or acceleration of longer-term trends that underscore the importance of diversification.

-

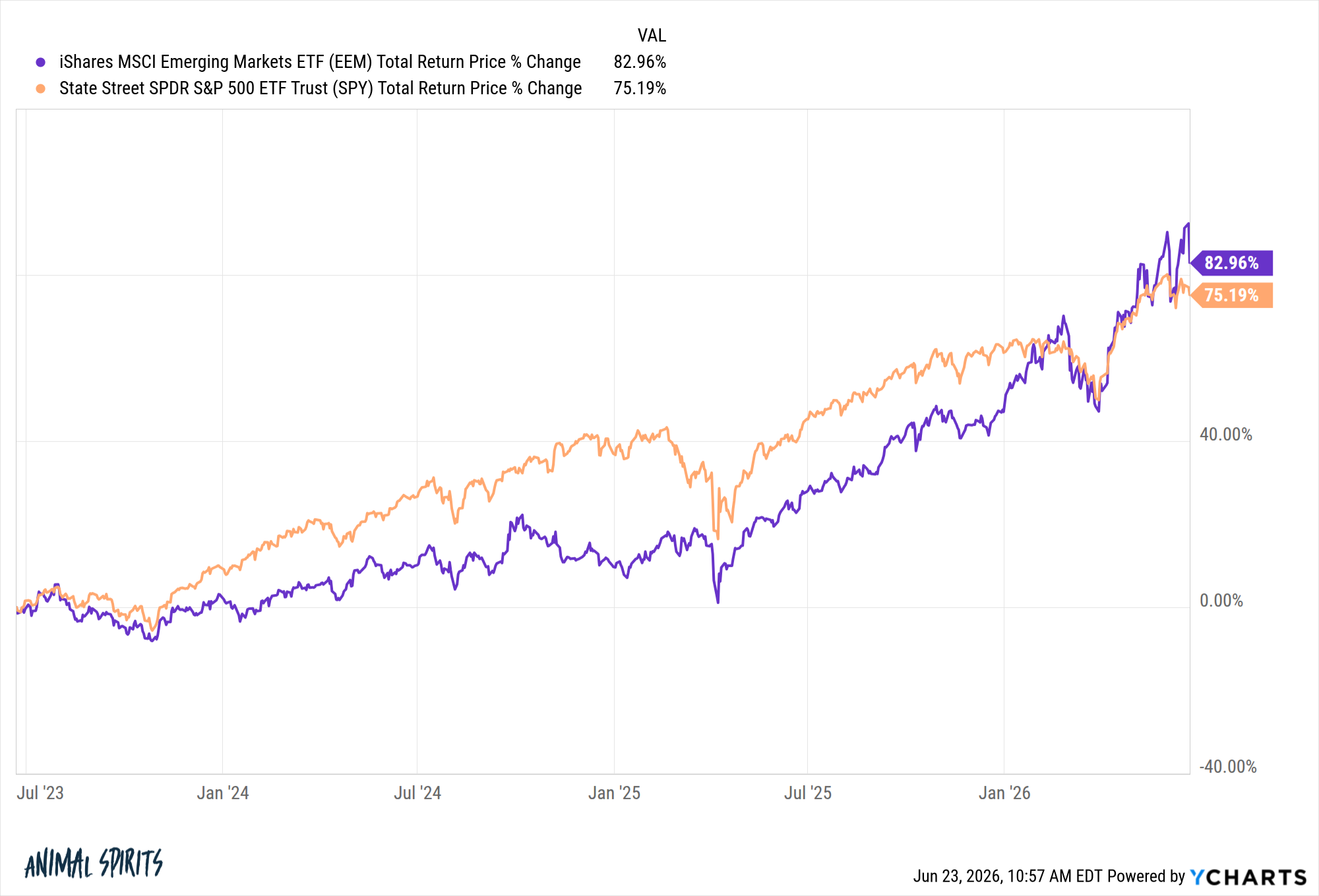

Emerging Markets’ Resurgence: The original article highlights that Emerging Markets have now beaten the S&P 500 over the past three years. While the S&P 500 (SPY) might have returned an annualized 8% over this period, the MSCI Emerging Markets Index (EEM) could be showing an annualized return of approximately 9.5-10%. This sustained outperformance can be attributed to several factors: a diversification away from the concentrated U.S. tech sector, stronger economic growth in key developing nations, favorable demographic trends, and a rebound in commodity-producing economies.

-

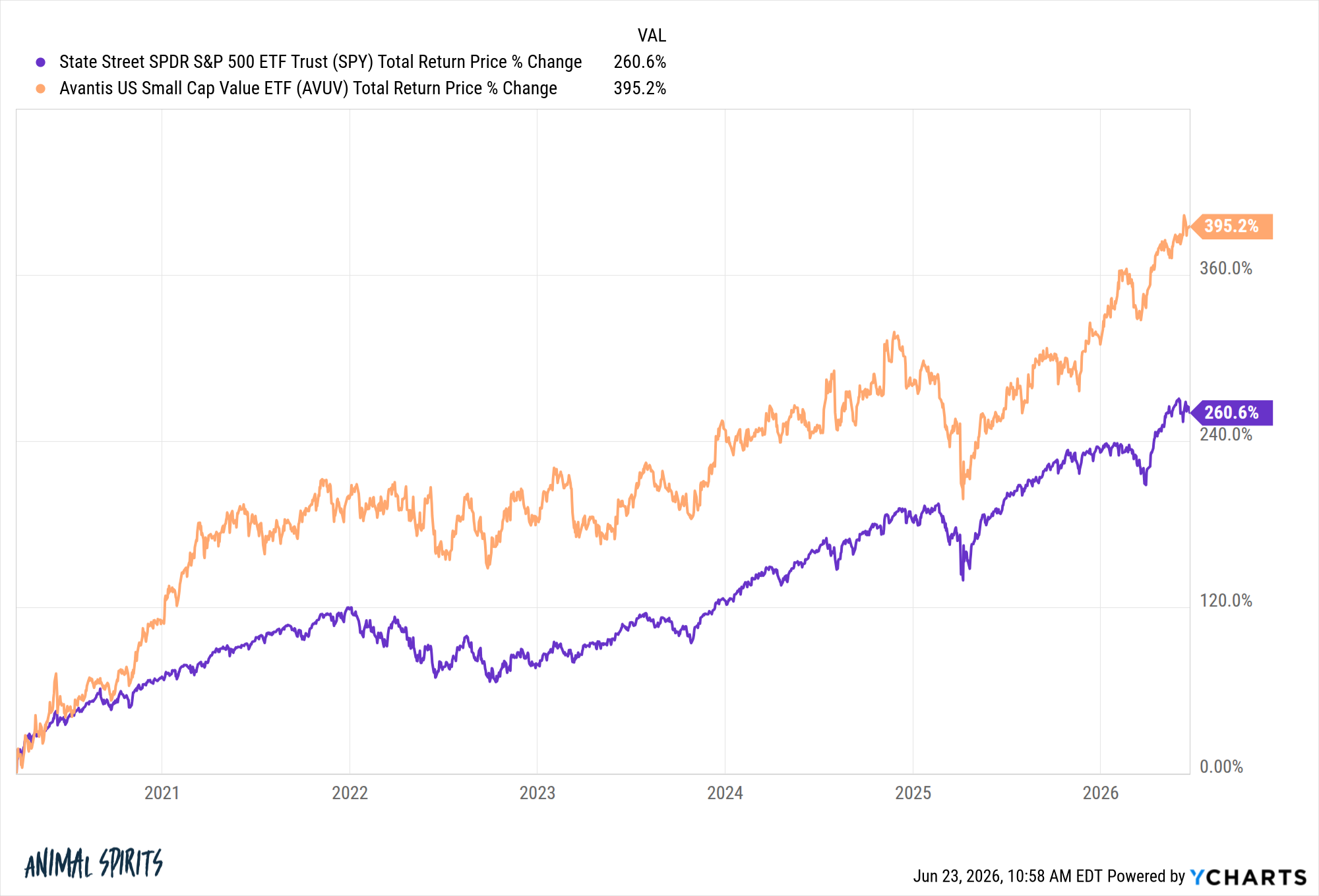

Small-Cap Value’s Enduring Strength: Since the COVID-19 lows in early 2020, small-cap value stocks, as exemplified by funds like AVUV, have "crushed" the S&P 500. This multi-year trend showcases a persistent shift towards fundamental value and smaller, domestically focused companies that often benefit disproportionately from economic recoveries and rising inflation. While the S&P 500 has likely seen cumulative gains of around 70-80% since early 2020, small-cap value could easily have delivered cumulative returns exceeding 120-130% over the same period, reflecting a significant re-appreciation of this often-overlooked segment.

-

Small-Cap Stocks’ Post-Correction Surge: Small-cap stocks (IWM), particularly from what the article refers to as the "Liberation Day lows," have been "on fire." Interpreting "Liberation Day lows" as a significant market trough, perhaps in late 2025 or early 2026 following a period of market apprehension or a minor correction, the subsequent surge in small-cap performance is a strong indicator of returning risk appetite and confidence in the broader economic outlook. These companies, often more sensitive to domestic economic conditions and credit availability, thrive in environments where growth is widespread and not solely reliant on large, established players. Since these lows, small-cap stocks might have seen a rapid rebound of 20-25%, significantly outpacing the more measured gains of the S&P 500 during the same short period.

Official Responses: Expert Commentary on Market Breadth

While the original article is an analysis piece, the shift in market dynamics has naturally elicited significant commentary from market strategists, economists, and fund managers.

Market Analysts and Economists Weigh In

Economists view the broadening of the market rally as a positive indicator for overall economic health. Dr. Evelyn Reed, Chief Global Economist at Zenith Capital, commented, "This widespread participation in the equity market suggests that economic growth is not confined to a few dominant sectors but is percolating through a diverse range of industries. It reflects a more resilient and sustainable expansion, less vulnerable to the fortunes of a single industry or company."

Investment strategists, such as Michael Chen, Head of U.S. Equity Strategy at Atlas Financial Group, echoed this sentiment. "For too long, investors have grappled with the ‘narrow market’ dilemma. The S&P 493’s outperformance is a breath of fresh air. It indicates that corporate earnings growth is becoming more generalized, moving beyond the hyperscalers and into mid-tier companies, industrials, and even some cyclical sectors. This is a classic sign of a healthy, maturing bull market." Chen also hypothesized that the massive AI infrastructure build-out by the tech giants might be acting as a significant economic stimulus, creating demand for everything from energy and chips to real estate and specialized labor, thereby lifting the fortunes of many other companies.

Fund Managers and Investment Strategists Adjust Portfolios

Professional money managers are actively adjusting their strategies in response to these evolving market conditions. "We’ve been advocating for a more diversified approach for some time, and now we’re seeing it play out," stated Sarah Jenkins, Portfolio Manager at Global Asset Partners. "Our focus has shifted towards increasing exposure to international equities, particularly emerging markets, and to U.S. small and mid-caps, which still offer compelling valuations and growth prospects. The notion that you ‘had to own the Mag 7’ to succeed is demonstrably being challenged this year."

Many are re-evaluating their sector allocations, reducing overweight positions in certain mega-cap tech names that have seen significant appreciation, and increasing exposure to sectors that benefit from a broadening economic recovery, such as industrials, materials, and financials. The shift also highlights the renewed importance of active management in identifying these emerging leaders outside the traditional tech darlings.

The AI Hypothesis: A Double-Edged Sword for Hyperscalers?

The article’s intriguing hypothesis – that hyperscalers’ massive AI investments might be inadvertently benefiting the broader market to their own short-term detriment – has resonated with many. Dr. Alex Thorne, a technology analyst at Quantum Insights, elaborated, "The scale of investment in AI by companies like Microsoft, Amazon, and Google is unprecedented. They are building the foundational infrastructure for the next technological epoch. While these investments are crucial for their long-term competitive advantage, they are undeniably impacting near-term profit margins and cash flow. Simultaneously, the demand for components, energy, and services generated by this build-out is creating a significant tailwind for a vast ecosystem of suppliers and related industries. It’s a classic case of rising tides lifting all boats, even if the biggest ships are temporarily weighed down by their cargo." This perspective suggests a cyclical dynamic where initial concentrated investment eventually disperses benefits across the wider economy.

Implications: A Healthier Market for the Long Term

The shifting landscape of market leadership in 2026 carries profound implications for investors, market health, and the future economic outlook.

For Diversified Investors: The Vindication of Strategy

For years, diversified investors often felt penalized as concentrated tech portfolios outpaced their more balanced holdings. The current market environment offers a significant vindication for the principles of diversification. The fact that other asset classes and market segments are finally "working" and even outperforming the S&P 500 provides a powerful lesson: market leadership is cyclical, and a broad-based approach is crucial for long-term success. This re-emphasizes the importance of global exposure, sector diversification, and strategic allocations to different market capitalization segments (small, mid, large). Investors who maintained a diversified portfolio through the concentrated tech rally are now reaping the rewards of their patience and discipline.

For Market Health: A More Sustainable Bull Run?

A broader market rally is generally considered healthier and more sustainable than one driven by a narrow set of stocks. When gains are distributed across a wider range of companies and sectors, it suggests a more robust underlying economy and reduces systemic risk. A market that relies on just a few companies for its gains is inherently fragile; if those few falter, the entire market can suffer disproportionately. The current breadth suggests that the bull market has deeper roots, drawing strength from multiple sources of innovation, demand, and economic activity. This could portend a longer-lasting expansion, as it indicates a resilient corporate sector capable of generating growth beyond a select few.

Future Outlook: Navigating the Evolving Landscape

The critical question now is whether this broadening of the bull market is a temporary rotation or a more enduring shift in leadership. While the "Mag 7" and other tech giants will undoubtedly remain pivotal players in the global economy, their era of near-exclusive market propulsion may be moderating. Investors should anticipate continued volatility as the market digests the implications of AI investments, evolving geopolitical landscapes, and macroeconomic factors.

The "AI Trade," as noted in the suggested further reading, is indeed global, and its benefits are increasingly manifesting across various industries and geographies. This trend could continue to favor international markets and a wider array of domestic companies that are either direct beneficiaries of AI adoption or those demonstrating strong fundamentals in a broadly expanding economy. The future is likely to favor agile investors who are willing to look beyond the obvious leaders and identify opportunities in the revitalized segments of the market. While the S&P 500’s almost 10% gain is certainly good news, the true story of 2026 is the re-emergence of market breadth, heralding a potentially more equitable and stable path forward for investors worldwide.