The Elusive Quest for Alpha: Navigating the Persistent Challenges of Active Management and Diversification

Main Facts

For decades, the financial industry has been driven by an insatiable quest: to outperform the market. This objective is particularly acute within the realm of institutional investing, where endowments, foundations, and pension plans manage vast sums of capital with a primary mandate to generate returns that not only preserve but also grow their assets beyond broad market benchmarks. To achieve this, these formidable entities often employ active managers – professionals tasked with making specific investment decisions aimed at beating a passive index. The monitoring of these managers is a rigorous, often quarterly, exercise, employing a traffic-light system: green for outperformers, yellow for those in the middle, and red for underperforming managers. While seemingly logical, this performance-based approach, which often favors managers with recent strong returns, inadvertently exposes a fundamental paradox of investing: outperformance is, by its very nature, fleeting. This reality, coupled with an ever-expanding universe of diversification options, presents a complex challenge for both institutional and individual investors, forcing a re-evaluation of how portfolios are constructed and, more importantly, how they are maintained through inevitable periods of underperformance.

The Institutional Imperative: Chasing Market-Beating Returns

The mandate for institutional investors extends beyond mere capital preservation; it often involves meeting specific spending policies, funding future liabilities, or sustaining charitable missions. This inherent need for growth places immense pressure on investment committees and boards to seek out managers who can deliver "alpha" – returns in excess of what the market provides. The traditional approach involves a painstaking selection process, often followed by a robust monitoring framework. Managers overseeing allocations to stocks, bonds, hedge funds, and private assets are subjected to intense scrutiny, their performance meticulously compared against predefined benchmarks.

The traffic-light system, a common tool in this oversight, appears straightforward: reward success, identify mediocrity, and eliminate failure. Outperforming managers are given a "green light," signifying continued confidence and, often, additional capital. Those delivering benchmark-like returns receive a "yellow light," signaling caution and a need for improved performance. The "red light" is reserved for consistent underperformers, typically leading to their dismissal. On paper, this system aims to keep portfolios aligned with top talent and efficient strategies. However, the reality of market dynamics frequently undermines this seemingly rational approach, leading to a cycle of hiring based on past success and subsequent disappointment.

The Cycle of Hope and Disappointment: The Fleeting Nature of Outperformance

The belief that past performance is indicative of future results is a powerful, yet often misleading, heuristic in investing. The institutional world, despite its sophistication, is not immune to this behavioral trap.

The Siren Song of Past Performance

The journey often begins with the allure of a newly discovered "star" manager. These managers, having recently delivered exceptional returns, capture the attention of investment committees. Their track record looks impeccable, their pitch compelling, and the prospect of replicating their past success irresistible. The decision to allocate capital to such a manager is often made with optimism, fueled by the expectation that the impressive performance streak will continue. This strategy, sometimes termed a "momentum game," assumes that winners will keep winning and losers will keep losing, thereby allowing investors to continually prune their portfolios for optimal performance.

Monitoring and The Momentum Trap

Once hired, these managers enter the regular monitoring cycle. For a time, some may continue their strong performance, reinforcing the committee’s decision. But as quarters turn into years, the inherent difficulty of consistently beating the market begins to manifest. The momentum strategy, which thrives on the persistence of trends, finds itself increasingly challenged. Markets are dynamic, and the factors that drive outperformance in one period rarely remain constant. Economic cycles shift, competitive landscapes evolve, and even the most skilled investors face periods where their particular strategy is out of favor. This leads to the inevitable truth that even the world’s best investors experience periods of underperformance.

The Underperformance Paradox

This leads to a common, almost predictable, scenario: a manager is hired precisely because their recent returns look "amazing," only to underperform after being brought into the portfolio. This phenomenon is not an isolated incident but a recurring pattern, driven by the non-persistence of alpha. The very act of chasing past returns often means buying into a strategy at its peak, just before its inevitable reversion to the mean or a period of struggle. The original article highlights this perfectly with a hypothetical illustration: a manager’s performance chart showing a sharp rise pre-hire, followed by a noticeable decline post-hire. While not every investor falls into this trap, it occurs with a frequency that belies its counter-intuitive nature. The emotional and psychological desire to align with success often overrides the cold, hard statistical evidence of its impermanence.

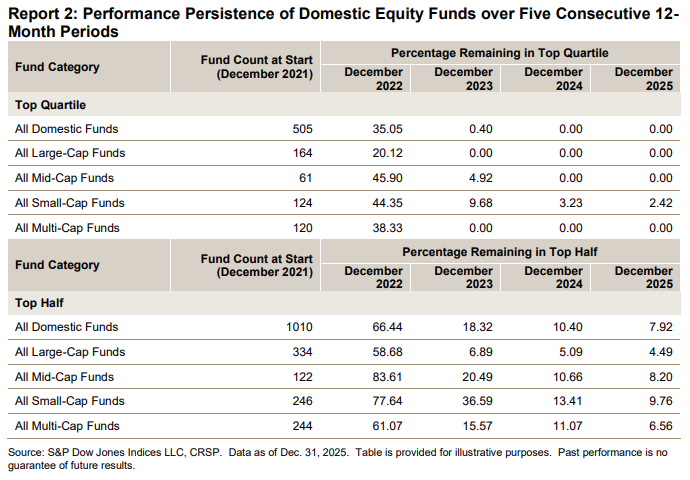

Data-Driven Reality: The S&P Dow Jones SPIVA Persistence Scorecard

The anecdotal observations of fleeting outperformance are robustly supported by empirical data. S&P Dow Jones Indices (S&P DJI) regularly publishes its SPIVA (S&P Dow Jones Indices Versus Active) reports, which provide a comprehensive and unbiased look at how active funds perform against their respective benchmarks globally. Crucially, SPIVA also offers a "Persistence Scorecard," directly addressing the question of whether past outperformance predicts future success.

Unpacking SPIVA: Methodology and Insights

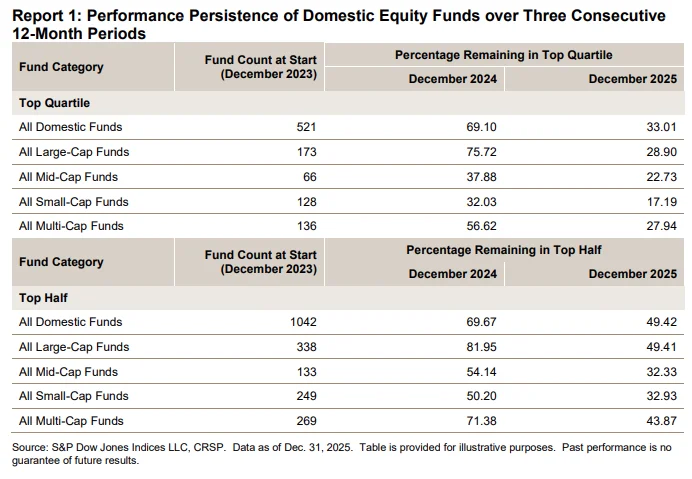

The SPIVA Persistence Scorecard analyzes the consistency of fund performance over various consecutive periods. It tracks funds that manage to stay in the top quartile (the top 25% of performers) or even the top half (top 50%) over sequential periods. The methodology is straightforward: identify funds in a given quartile in one period, then track how many of those same funds remain in that quartile in subsequent periods. This offers a clear, quantitative measure of performance persistence. The results consistently challenge the efficacy of a strategy based on chasing past returns.

The Three-Year Persistence Conundrum

Consider the numbers for U.S. stock market funds over consecutive three-year periods, as highlighted in the original article. For instance, if we look at funds in the top quartile of returns for 2023, a significant 69% managed to remain in that top quartile in 2024. This might initially seem encouraging, suggesting some degree of skill. However, the picture changes dramatically when extending the horizon. Only 33% of those initial 2023 top-quartile performers could sustain that level of excellence into 2025. This sharp drop-off from 69% to 33% within just two additional years underscores the rapid erosion of outperformance. It illustrates that while short-term streaks can occur, sustaining them becomes progressively harder.

The Five-Year Vanishing Act

The trend becomes even more stark and conclusive when examining persistence over five-year periods. The data reveals a near-complete vanishing act for sustained top-tier performance. For funds starting in 2021, the probability of remaining in the top quartile for three, four, or even five consecutive years becomes infinitesimally small. The original article notes that "less than 10% of funds could stay in the top half of performers for five consecutive years." This statistic is profoundly impactful. It implies that for every ten funds that started in the top half, fewer than one could maintain that relative position for half a decade. This data serves as a sobering reminder that consistent, market-beating performance is an anomaly, not a norm, and that relying on historical track records for manager selection is a strategy fraught with risk.

Broader SPIVA Context: A Consistent Narrative

Beyond persistence, the overall SPIVA reports consistently demonstrate that a majority of active managers across various asset classes and geographic regions underperform their respective passive benchmarks over extended periods (e.g., 5, 10, 15 years). This broader context further solidifies the argument against the ease of active management. The combined evidence from SPIVA – both on outright outperformance and the persistence of that outperformance – paints a clear picture: "Stock-picking is hard, but it might be even harder to pick the managers that will outperform the market." The very structure of efficient markets, where information is rapidly disseminated and priced in, makes it incredibly difficult for any single manager to consistently find mispricings and capitalize on them.

Beyond Active Management: The Universal Truth of Investment Volatility

The challenge of consistent outperformance is not solely confined to active management. It is a universal truth of investing that applies to every strategy and asset class: "Nothing works all the time." This fundamental principle dictates that even the most robust and well-researched investment approaches will experience periods of underperformance or struggle.

"Nothing Works All The Time": A Foundational Principle

This concept is crucial for investors to internalize. Whether one invests in growth stocks, value stocks, small-caps, large-caps, emerging markets, or developed markets, there will be cycles where that particular segment lags. The same applies to different asset classes: bonds may outperform stocks for a period, only to reverse course; real estate can boom and bust; commodities can swing wildly. Even seemingly diversified, rules-based strategies or passive index funds will have periods where they underperform specific niche strategies or even cash, depending on market conditions. Understanding this impermanence is the first step towards building a resilient portfolio and developing the psychological fortitude required for long-term investing success.

The Evolving Diversification Landscape

In recent years, the investment landscape has exploded with new opportunities for diversification. The author, reflecting on a recent book tour, noted a flurry of questions from investors grappling with this expanded universe:

- "Is the 60/40 portfolio dead?" – a classic allocation now questioned after a decade of low bond yields and recent inflation.

- "Don’t we need to update this with the times?" – a natural inquiry given market shifts.

- "What do you think about adding gold to a portfolio? Or Bitcoin?" – exploring traditional and nascent alternative assets.

- "How about trend-following or managed futures?" – delving into systematic strategies.

- "How should investors think about diversifying their fixed income exposure given the bond bear market this decade?" – a critical question after a challenging period for bonds.

- "How about buffer ETFs? Or option income funds?" – considering more complex structured products.

- "What about private investments?" – accessing illiquid, higher-return potential assets.

This proliferation of options presents both a tremendous opportunity and a significant challenge.

The Diversification Dilemma: Opportunity or "Diworsification"?

The good news for today’s individual investor is the unprecedented breadth of investment opportunities available for diversification. Technological advancements, lower barriers to entry, and the growth of various financial products mean that a highly diversified portfolio, once the exclusive domain of large institutions, is now accessible to almost anyone.

Navigating Modern Portfolio Theory

Modern Portfolio Theory (MPT), pioneered by Harry Markowitz, posits that investors can construct portfolios to maximize expected return for a given level of market risk, or conversely, minimize risk for a given level of expected return, through diversification. The goal is to combine assets that do not move in perfect lockstep, thereby smoothing out overall portfolio volatility. Historically, this often meant a mix of stocks and bonds. Today, MPT’s principles are applied across a much wider array of assets, including real estate, commodities, alternative strategies, and even cryptocurrencies. The sheer number of accessible options allows for highly customized risk-return profiles.

The Spectrum of Portfolio Complexity

However, this abundance comes with a caveat: the temptation to "diworsify." This term, coined by Peter Lynch, refers to the act of diversifying a portfolio with too many funds or strategies, often leading to a dilution of returns, increased complexity, and higher costs, without necessarily providing true diversification benefits. The spectrum of portfolio complexity is vast, and there is no single "perfect portfolio" universally applicable to every investor. Some individuals thrive on simplicity, preferring a minimalist 3-fund portfolio (e.g., total U.S. stock, total international stock, total U.S. bond) or even a single target-date fund. For them, anything more complex leads to overwhelm and poor decision-making.

The Trap of Over-Diversification

On the other hand, some sophisticated investors prefer to cover more bases, holding a wider array of different funds and strategies to achieve more granular diversification. These investors often possess the knowledge, time, and discipline to manage such complexity. The critical distinction lies in understanding one’s own behavioral tendencies and capacity for managing complexity. The risk of diworsification arises when investors, in an attempt to optimize or hedge against every conceivable market scenario, add layers of complexity they don’t fully understand or can’t commit to long-term. This can lead to paralysis, impulsive trading, and ultimately, suboptimal returns. The abundance of choice, therefore, demands an increased level of self-awareness and discipline from investors.

The Ultimate Litmus Test: The Diversification Test

Given the inherent difficulty of consistently outperforming, the fleeting nature of alpha, and the myriad options for diversification, how can an investor confidently build and maintain a portfolio that is truly right for them? The author proposes a powerful, yet simple, rule: the diversification test.

Defining the Test: Conviction in Adversity

The test is straightforward: "If your investment is down in value, will you lean into the pain and buy more?" This question cuts to the heart of investment conviction and discipline. It challenges the investor to look beyond superficial returns and assess their fundamental belief in an asset or strategy. It’s easy to invest in something when it’s trending upwards, fueled by FOMO (fear of missing out) and the thrill of gains. The true test of any investment strategy or asset allocation, however, is how an investor handles it when it’s falling behind, when the headlines are negative, and when doubt begins to creep in.

The Institutional Failure Point

Many of the institutional investors the author worked with failed this test repeatedly. Every time a manager underperformed, the immediate reaction was often to hit the "eject button" and fire them. This reactive behavior, driven by short-term performance metrics and accountability pressures, perpetuates the cycle of chasing past returns and divesting from underperforming assets, often at the worst possible time. This constant churn rarely leads to superior long-term results and often locks in losses while missing subsequent recoveries. One of the reasons for this reactive stance is that many institutional managers employ discretionary and often complicated strategies. When such a strategy underperforms, it’s challenging for committees to discern if the manager is merely going through a temporary rough patch adhering to a sound but out-of-favor process, or if the underlying strategy is fundamentally broken and no longer effective.

The Clarity of Rules-Based Strategies

This difficulty in understanding discretionary strategies is precisely why the author advocates for rules-based strategies and index funds. With an index fund, the process is entirely transparent: it simply tracks a defined market segment according to a set of clear, immutable rules. When an index fund underperforms, the reason is typically clear – the underlying market segment it tracks is out of favor. There’s no ambiguity about the manager’s "skill" or the integrity of the process. This transparency fosters greater confidence and discipline during downturns. An investor who understands what they own and why they own it – based on a clear, rules-based methodology – is far more likely to "lean into the pain and buy more" during a market dip, thereby capitalizing on the long-term tendency of markets to recover and grow.

Discretionary vs. Rules-Based: A Matter of Trust

The contrast between discretionary and rules-based approaches is significant for investor psychology. With a discretionary manager, an investor must trust the manager’s judgment, even when that judgment leads to losses. This trust can be difficult to maintain when performance lags, as the investor lacks direct insight into the decision-making process. Is the manager sticking to their principles, or are they making ad-hoc changes? Is their strategy temporarily out of sync with the market, or is it fundamentally flawed? These questions can erode confidence and lead to impulsive decisions. Conversely, with a rules-based strategy, the process itself is the trusted entity. The investor is not relying on an individual’s constantly evolving judgment but on a predetermined, transparent methodology. This allows for more reasonable expectations and greater confidence in the overall investment process, reducing the temptation to constantly jump in and out of different investments.

Building a Resilient Portfolio: Beyond Returns

Ultimately, the diversification test is about building a resilient portfolio – one that an investor can stick with through thick and thin. It acknowledges that markets are cyclical, and every asset class and strategy will have its moment in the sun and its time in the shade. The true measure of a portfolio’s suitability isn’t just its potential for high returns, but its ability to withstand adverse conditions without prompting panic-driven decisions. By selecting asset classes, strategies, and holdings that pass this test, investors cultivate a deeper understanding and conviction in their choices. This conviction is the bedrock of long-term success, enabling them to endure volatility, avoid costly behavioral errors, and remain invested during the very periods that set the stage for future growth.

The Psychological Edge

This psychological advantage is invaluable. Knowing that you have a plan you believe in, and that you are prepared to act counter-intuitively by adding to positions when they are down, empowers you to navigate market turbulence with a steady hand. It transforms volatility from a source of fear into an opportunity, aligning behavior with long-term financial goals rather than succumbing to short-term emotional swings. The "diversification test" is not merely an investment principle; it is a profound exercise in self-awareness and discipline, essential for any investor aiming for sustained success in the unpredictable world of finance.

Conclusion: Embracing the Impermanence of Outperformance for Long-Term Success

The pursuit of consistent outperformance in active management is, for the vast majority, a Sisyphean task, as evidenced by the compelling data from SPIVA’s Persistence Scorecard. Outperformance is fleeting, and the strategy of chasing past winners often leads to disappointment. In an increasingly complex financial world brimming with diversification options, investors face the dual challenge of harnessing opportunity without succumbing to "diworsification." The solution lies not in finding the "perfect" portfolio, but in constructing one that aligns with an investor’s deep-seated convictions and psychological fortitude. The "diversification test" provides a crucial litmus test: the willingness to "lean into the pain and buy more" when an investment is down. This discipline, often fostered by the transparency of rules-based strategies, is the cornerstone of long-term investing success, allowing investors to navigate market cycles with confidence and consistency, rather than succumbing to the temptation of short-term performance chasing.

Further Reading: