The Great Migration: Evaluating the Top Personal Finance Platforms in the Wake of the Mint.com Shutdown

Main Facts: The End of an Era in Digital Budgeting

For nearly two decades, Mint.com stood as the undisputed pioneer of web-based personal finance management (PFM). Launched in 2007, the platform revolutionized how consumers interacted with their money by aggregating bank accounts, credit cards, investments, and bills into a single, automated, and free dashboard. At its peak, Mint boasted millions of active users who relied on its automated transaction categorization and budget tracking.

However, the digital budgeting landscape underwent a seismic shift when Intuit—which acquired Mint in 2009 for $170 million—officially shuttered the service. Current users were forced to migrate their historical financial data or find a replacement platform. While Intuit directed users toward its Credit Karma brand, many consumers found the replacement lacking in granular budgeting tools, prompting an industry-wide migration to alternative fintech platforms.

The market has since responded with a highly competitive suite of PFM tools. These platforms range from free, investment-centric trackers to premium, subscription-based budgeting ecosystems. For displaced Mint users, finding a replacement requires balancing data security, platform compatibility, feature sets, and cost.

Chronology of the PFM Market: The Rise and Fall of Mint

To understand the current state of personal finance software, it is essential to trace the timeline of the market’s evolution and the vacuum left by Mint’s departure:

- 2007: Mint.com launches at the TechCrunch 40 conference, immediately winning top honors for its innovative use of screen-scraping technology to aggregate financial accounts.

- 2009: Intuit acquires Mint.com for $170 million, integrating it into its suite of financial software alongside TurboTax and QuickBooks.

- 2010–2020: Mint dominates the free budgeting space. However, users increasingly complain of stagnant feature development, frequent account connection breakages, and an ad-heavy user interface designed to upsell credit cards and financial products.

- November 2023: Intuit formally announces the decision to shut down Mint.com, setting a final termination timeline for early 2024. The company details plans to transition core budgeting features into Credit Karma.

- Early 2024: Mint.com officially goes dark. Displaced users scramble to export their transaction history via CSV files, prompting rival fintech platforms to build custom "Mint Import" tools to capture the massive influx of migrating users.

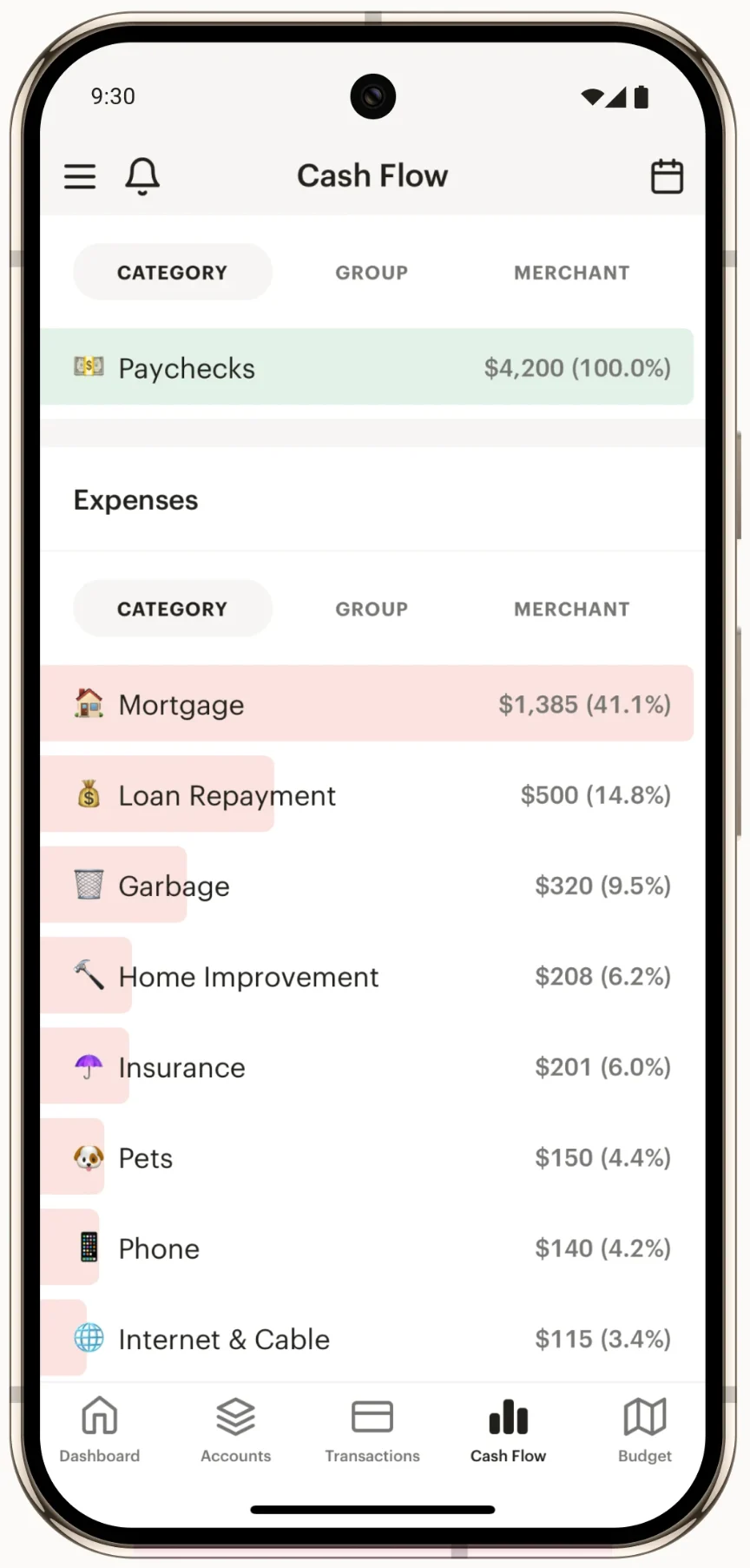

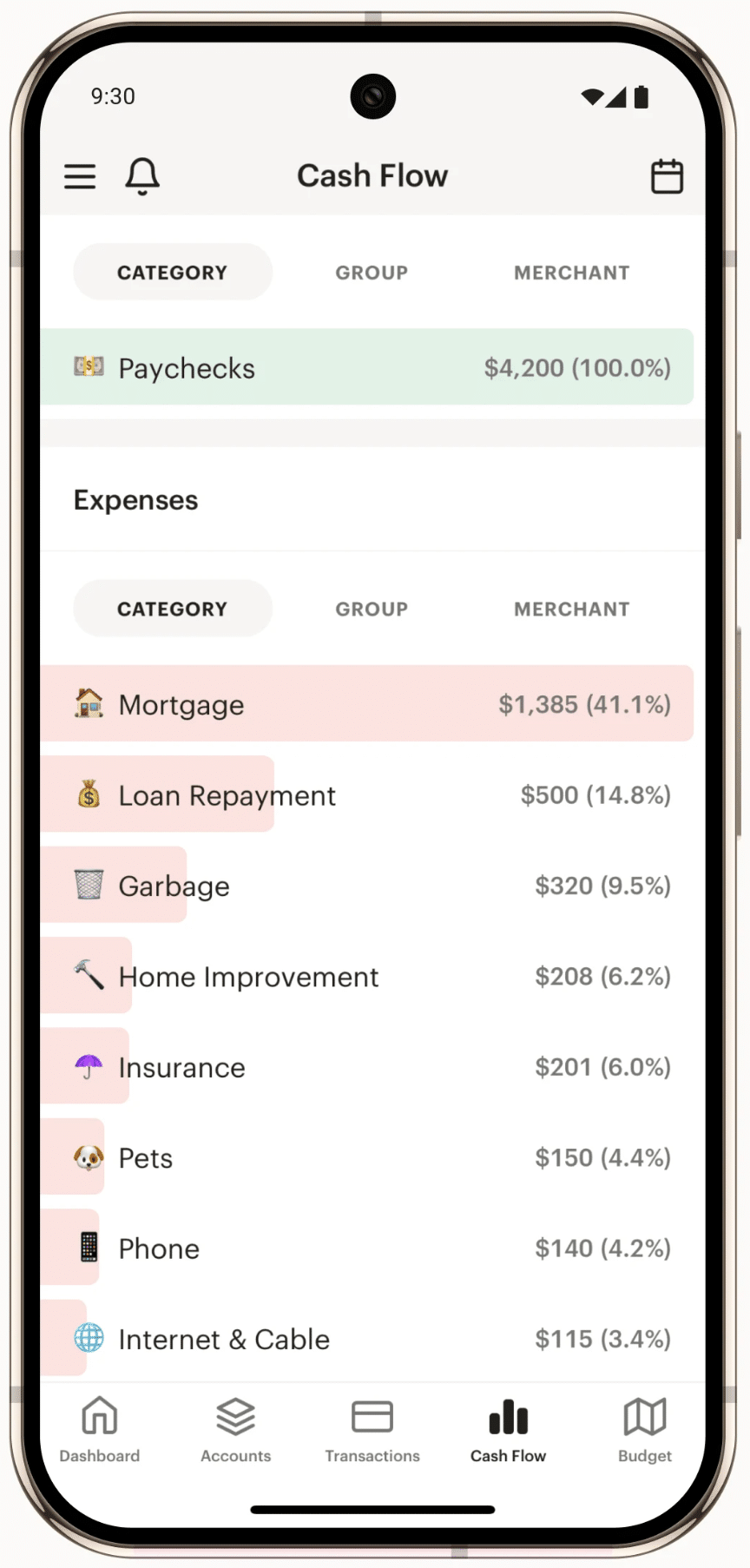

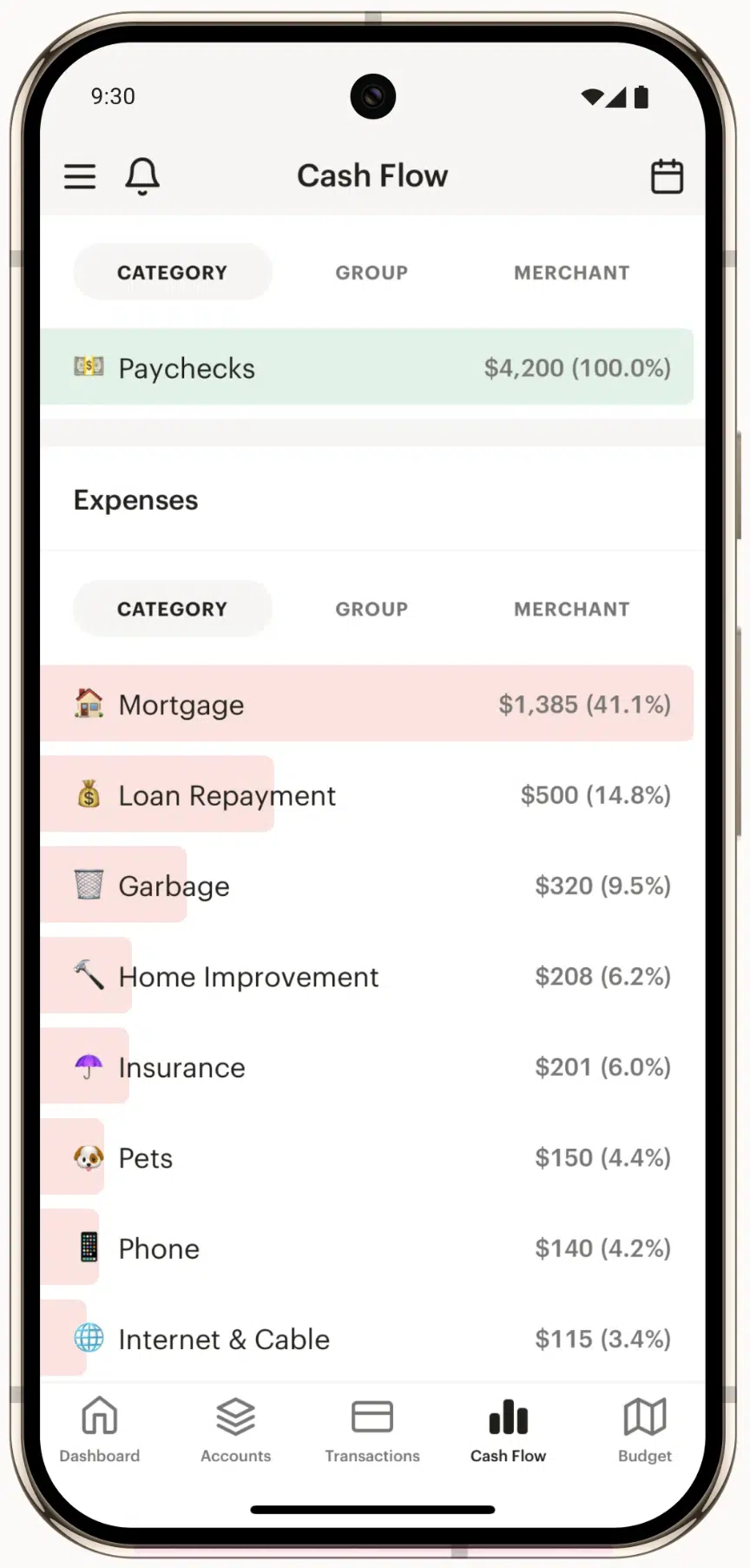

Supporting Data: Comprehensive Evaluation of the Top 8 Mint Alternatives

To assist consumers in navigating this transition, we have compiled extensive operational data, pricing structures, and performance ratings for the eight leading platforms currently positioning themselves as the premier alternatives to Mint.

+------------------+------------------------------+-------------------------+--------------------+

| Budgeting App | Primary Focus | Pricing Structure | Free Trial Length |

+------------------+------------------------------+-------------------------+--------------------+

| Monarch Money | Holistic Household Budgeting | $99/year (or promo) | 7 Days |

| Empower | Investment & Net Worth | Free | N/A |

| Rocket Money | Subscription Management | Free / $7–$14/month | Custom |

| Quicken Simplifi | Mobile-First Spending Plans | $3.49/month (billed annually) | N/A |

| Origin | Total Wealth & Tax Planning | $12.99/month or $99/year| 7 Days |

| Tiller Money | Spreadsheet Automation | $79/year | 30 Days |

| Quicken Classic | Advanced Desktop Ledger | Varies by Tier | N/A |

| YNAB | Zero-Based/Envelope Budgeting| $14.99/month or $109/year| 34 Days |

+------------------+------------------------------+-------------------------+--------------------+1. Monarch Money — Best Overall Budgeting App

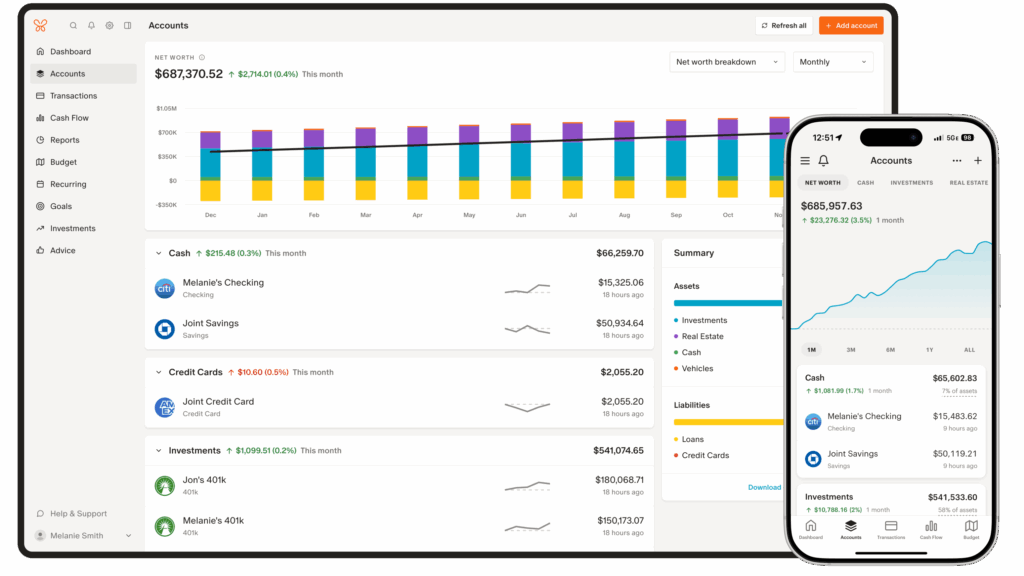

Developed in part by Val Agostino—the original product manager of Mint.com—Monarch Money was built specifically to address the structural flaws of older PFM tools. It has emerged as the premier paid alternative for households and couples.

- App Store Rating: 4.9 (88k reviews) | Android Rating: 4.8 (21.2k reviews)

- Platforms: iOS, Android, Web

- Cost: 7-day free trial, then $99/year. (Promotional discounts, such as code

ROB50, frequently offer up to 50% off the first year). - Key Features: Multi-user collaboration without account sharing; "Flex Budgeting" for fluctuating monthly expenses; custom transaction rules; recurring subscription trackers; VantageScore 3.0 credit score monitoring.

- Analysis: Monarch’s dashboard is widely regarded as the cleanest and most intuitive in the industry. Its synchronization engine utilizes multiple data aggregators (Plaid, Finicity, MX) to ensure stable bank connections, a major pain point of the old Mint platform.

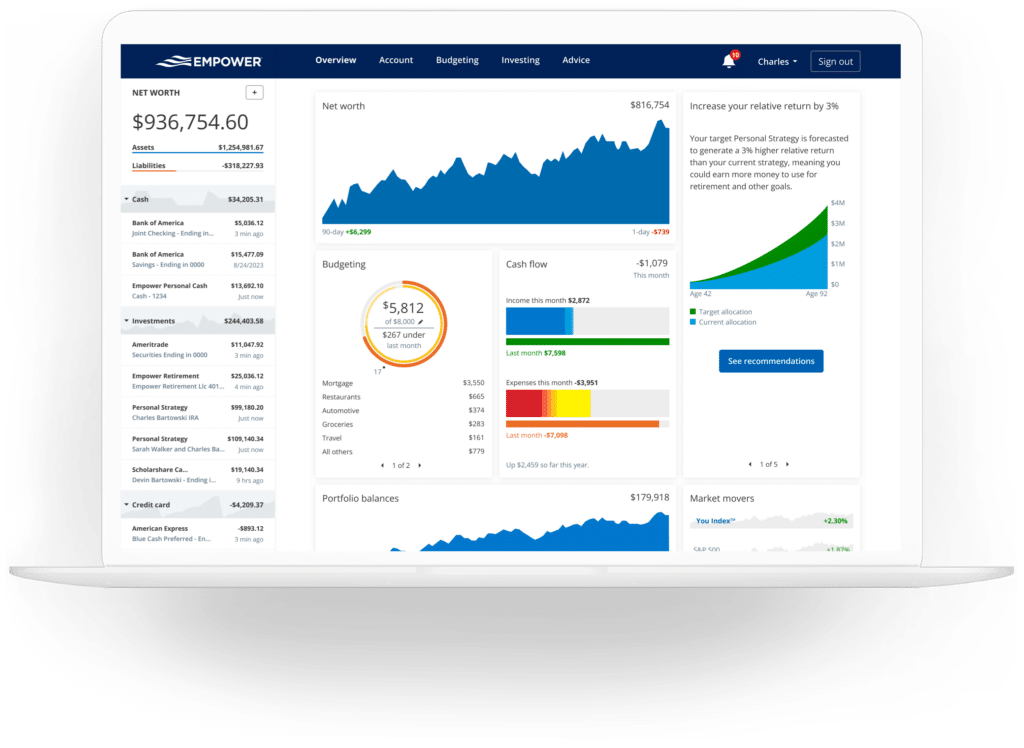

2. Empower — Best for Tracking Investments and Net Worth

Formerly known as Personal Capital, Empower is a wealth management platform that offers its robust financial aggregation software completely free of charge.

- Platforms: iOS, Android, Web

- Cost: Free

- Key Features: Real-time net worth tracking; investment portfolio fee analyzer; retirement planning calculator; asset allocation visualizers.

- Analysis: For users who utilized Mint primarily to track their net worth and investment portfolios rather than construct strict monthly spending limits, Empower is the superior choice. The software monetizes by offering optional, human-led wealth management services to high-net-worth individuals, keeping the software itself free of intrusive third-party banner ads.

3. Rocket Money — Best for Subscription and Bill Management

Originally launched as TrueBill, Rocket Money has evolved into a highly visual, consumer-centric budgeting application with a strong emphasis on reducing fixed overhead expenses.

- Platforms: iOS, Android, Web

- Cost: Free tier available; Premium features operate on a sliding scale of $7 to $14 per month (billed annually).

- Key Features: Automated subscription detection and cancellation services; bill negotiation concierge; automated savings transfers; real-time spending push notifications.

- Analysis: Rocket Money excels at helping users plug "spending leaks." Its dashboard clearly highlights recurring charges, making it incredibly simple to identify forgotten SaaS subscriptions or gym memberships.

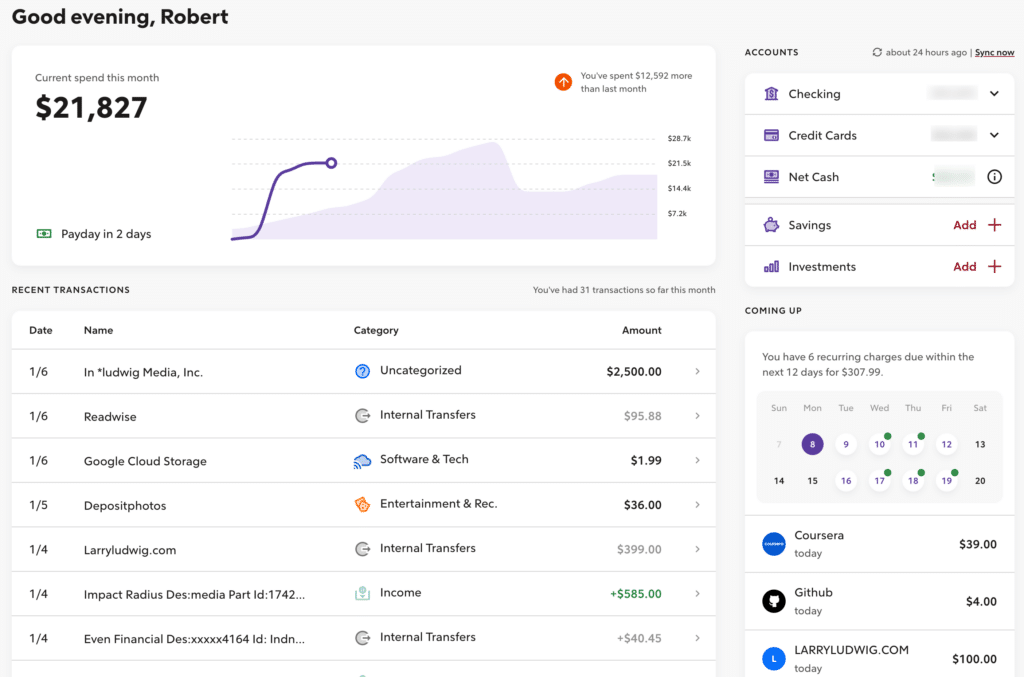

4. Quicken Simplifi — Best Mobile-First Budgeting Experience

Simplifi is Quicken’s modern, cloud-native response to the mobile budgeting era. It is built entirely separate from Quicken’s legacy desktop software.

- Platforms: iOS, Android, Web

- Cost: $3.49 per month (billed annually at 50% off the standard $6.99/month rate).

- Key Features: Automated "Spending Plans" based on historical income and fixed expenses; calendar-based bill tracking; watchlists for specific spending categories; customizable dashboard widgets.

- Analysis: Simplifi offers a highly automated approach to budgeting. Instead of forcing users to manually categorize every dollar, it calculates a real-time "available to spend" balance after accounting for savings goals, bills, and pending transactions.

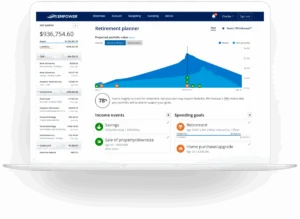

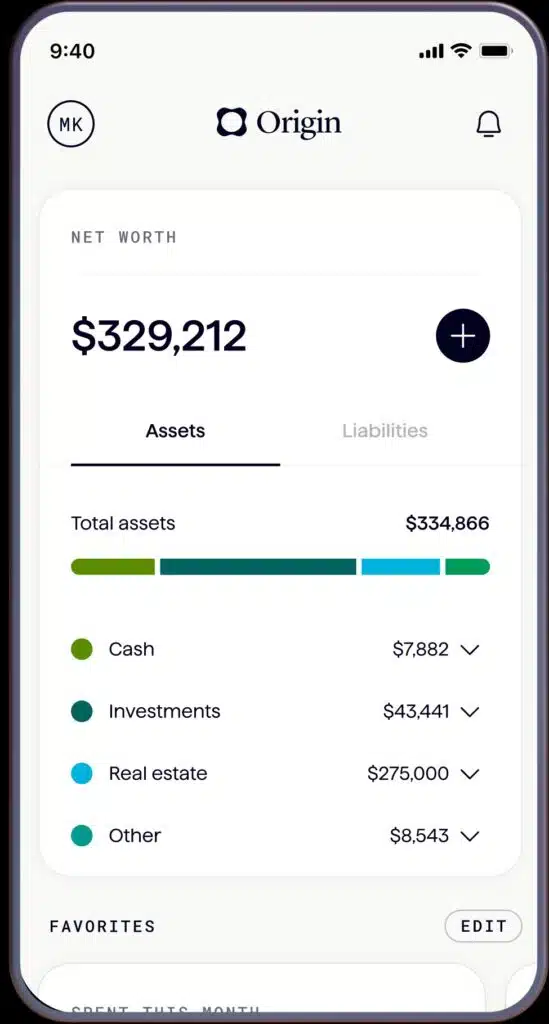

5. Origin — Most Comprehensive Financial Management Platform

Origin represents a new class of "all-in-one" financial wellness platforms, combining budgeting, tax filing, and equity management into a single subscription.

- Platforms: iOS, Android, Web

- Cost: 7-day free trial, then $12.99/month or $99/year. (Limited-time promotional rates occasionally offer the first year for $1).

- Key Features: Integrated federal and state tax filing (included in subscription); estate planning (trust and will creation); equity and stock option tracking; AI-powered financial advisory assistant.

- Analysis: Origin is highly distinct in its integration of generative AI. Users can converse with an AI assistant to analyze spending trends, draft emergency fund plans, or optimize tax withholding strategies. It is ideal for high-earning professionals with complex compensation packages.

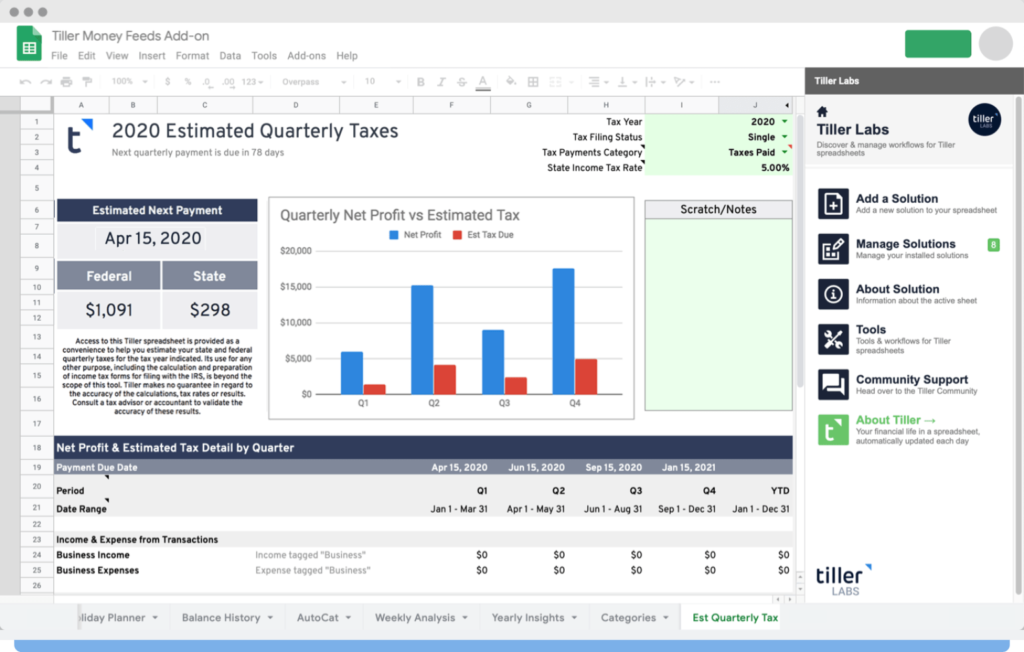

6. Tiller Money — Best for Spreadsheet Enthusiasts

Tiller is the only platform on the market that bridges the gap between automated bank aggregation and the total customization of personal spreadsheets.

- Platforms: Google Sheets, Microsoft Excel (accessible on Desktop/Tablet)

- Cost: 30-day free trial, then $79/year.

- Key Features: Automated daily bank feed updates directly into spreadsheets; customizable templates (e.g., Foundation Template); zero-ad privacy-focused model; open-source developer community.

- Analysis: Tiller is designed for users who want total control over their data without the tedious chore of manual entry. While highly powerful, it lacks a dedicated mobile app, making smartphone navigation and quick on-the-go logging difficult.

7. Quicken Classic — Best Traditional Desktop Software

For power users who require decades of historical data storage, advanced tax reporting, and local file storage, Quicken Classic remains the industry standard.

- Platforms: Windows, macOS (companion app available for iOS/Android)

- Cost: Subscription-based, tiered pricing depending on feature requirements.

- Key Features: Local offline data storage; advanced investment tracking (cost basis, capital gains); direct bill pay capabilities; custom report generation.

- Analysis: Quicken Classic represents the traditional ledger-based approach to personal finance. While its interface can feel dated compared to cloud-native platforms, its analytical depth is unmatched for complex household portfolios.

8. You Need a Budget (YNAB) — Best for Zero-Based Budgeting

YNAB is built on a strict, proactive budgeting philosophy: "Give every dollar a job." It remains a cult favorite for individuals actively trying to break the paycheck-to-paycheck cycle.

- Platforms: iOS, Android, Web, Apple Watch

- Cost: 34-day free trial, then $14.99/month or $109/year.

- Key Features: Zero-based (envelope) budgeting structure; loan planner tool; goal tracking progress bars; extensive educational workshops.

- Analysis: YNAB does not track investments or net worth dynamically. Instead, it focuses exclusively on immediate cash flow. It carries a steep learning curve and a premium price tag, but its methodology has proven highly effective for debt reduction.

Official Responses and Market Realignment

The shutdown of Mint triggered sharp reactions across the financial technology sector.

In official statements, Intuit defended the transition, arguing that Credit Karma would provide a more holistic financial home for users by focusing on credit building, net worth monitoring, and recommendations for financial products. "We are excited to bring the best of Mint’s features into Credit Karma, creating a more unified experience to help users find the right financial products," an Intuit spokesperson stated during the transition rollout.

However, competitors viewed the move as an abandonment of pure budgeting enthusiasts. Fintech executives immediately seized the opportunity. Monarch Money’s CEO, Val Agostino, publicly welcomed displaced Mint users, emphasizing that Monarch’s subscription model aligned its incentives directly with consumers rather than advertisers. Similarly, Quicken Simplifi and YNAB launched dedicated marketing campaigns highlighting the ease of migrating historical Mint data via CSV imports, effectively absorbing hundreds of thousands of active accounts within a matter of weeks.

Implications for Consumers and the Fintech Industry

The dissolution of Mint.com carries several long-term implications for both everyday consumers and the broader fintech ecosystem:

1. The Decline of "Free" and the Rise of Subscription Privacy

Mint proved that the "free, ad-supported" model of personal financial management is difficult to sustain. When users do not pay for a product, they are the product—monetized through credit card offers, personal loan ads, and data sharing. The market’s shift toward subscription models (Monarch, YNAB, Tiller) indicates that consumers are increasingly willing to pay a premium annual fee in exchange for data privacy, stable bank connections, and an ad-free user interface.

2. The Open Banking Revolution

The transition to modern alternatives has accelerated the adoption of secure API connections. Legacy screen-scraping methods—which required users to share their bank passwords with third parties—are being phased out in favor of open banking protocols mediated by services like Plaid and Finicity. This transition ensures safer, more stable, and more reliable data pipelines.

3. AI-Driven Financial Planning

As demonstrated by platforms like Origin, the future of budgeting lies in predictive analytics. Instead of merely reflecting historical spending, next-generation platforms will leverage artificial intelligence to proactively advise users on tax optimization, debt payoff schedules, and investment allocations, turning static budget tools into dynamic, automated financial advisors.