Raising Financially Literate Children: A Masterclass in Early Economic Education

In an era defined by ubiquitous digital transactions and a pervasive consumer culture, the task of teaching children the fundamental value of money has become increasingly complex. For many parents, the county fair—with its dizzying array of trinkets, sugar-laden treats, and carnival games—serves as a primary battleground for the conflict between impulse and fiscal responsibility. For one Vermont-based family, these outings are not merely recreational; they serve as a sophisticated, hands-on laboratory for instilling long-term money management skills in their five- and seven-year-old children.

By demystifying the flow of capital and creating a structured, tangible framework for their daughters, these parents are proving that financial literacy is not a subject to be reserved for the high school classroom, but a daily practice that begins with simple, clear-cut philosophies.

The Core Philosophy: Distinguishing Need from Want

At the heart of their approach is a straightforward "Family Money Philosophy." While the name suggests complex academic theory, the execution is remarkably elegant in its simplicity. The parents operate under a binary division of financial responsibility:

- Parental Obligation: The parents cover the "essentials," a category defined as shelter, clothing, basic nutrition, healthcare, educational materials, and general admission to cultural venues like museums or regional fairs.

- Child Discretionary Spending: The children are solely responsible for "extras." This includes specific indulgent snacks (such as restaurant desserts), non-essential souvenirs at gift shops, and supplemental media like Scholastic Book Fair orders.

By drawing this firm line, the parents avoid the common trap of funding every whim, instead forcing the children to evaluate the marginal utility of a purchase against the effort required to earn the funds.

Chronology of Financial Development

The evolution of these lessons follows a developmental trajectory, starting from the basic recognition of currency and moving toward complex concepts like debt and interest.

Phase 1: The Basics of Exchange

The initial stage of the program focuses on the mechanics of money. At age five, the focus is on identifying denominations, basic arithmetic, and the concept of "price." The parents go to great lengths to explain that money is a limited resource derived from labor. By narrating their own work lives—explaining that time spent at a computer in a meeting translates into the capital required to purchase groceries—they strip away the magic of the "infinite wallet."

Phase 2: Labor and Market Value

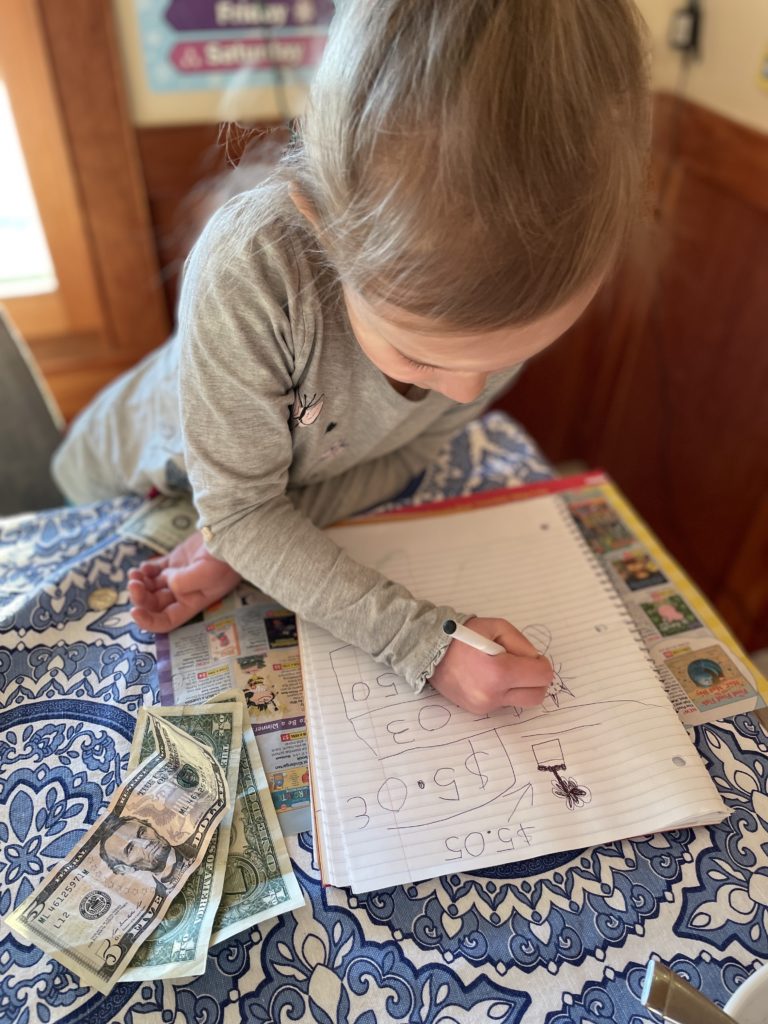

To earn the funds for their discretionary spending, the children are tasked with chores that go beyond basic self-care. The parents utilize a "fair market value" system. Children are encouraged to negotiate the price of a job. For instance, a recent successful negotiation saw a seven-year-old earn a $10 lump sum for organizing the household’s kitchen cabinets. This early exposure to negotiation provides children with an understanding of labor value and the reality that income is a direct result of productivity.

Phase 3: The Hard Lessons of Debt

Perhaps the most significant milestone in this educational journey occurred during a previous county fair, where a child desired a $13 inflatable unicorn while possessing only $9. The parents allowed the purchase, but issued a $4 loan. The subsequent requirement to "work off" that debt through non-negotiable chores provided a visceral, real-world lesson: debt is a form of future-taxation on one’s time. The child’s realization—that performing labor to pay for an object already acquired is "not fun"—serves as a powerful deterrent against future impulsive borrowing.

Supporting Data: The Utility of Real-Life Scenarios

The efficacy of this model is supported by the children’s shifting behavior. Following the "unicorn debt" incident, the children became significantly more cautious. They now engage in proactive planning for outings, often carrying their own wallets and calculating the costs of items beforehand.

This shift was evidenced during a series of weekly "pizza nights" at a local farm. Initially, the older child funded the dessert entirely, only to realize that her sister was benefiting from a product she had paid for with her own labor. This led to a sophisticated, child-led negotiation regarding cost-sharing and the division of $7—an odd number that forced them to grapple with fractioning and coin denominations. The parents noted that the children now handle the transaction at the counter independently, building confidence alongside fiscal competence.

Official Perspective: The "Parental Unit" View

The parents view their role as "financial architects." They emphasize that the goal is not to force children into a life of austerity, but to provide them with a toolkit for navigating an adult world where money is merely a medium for achieving specific life goals.

"Money is not status, self-worth, emotional wellness, happiness, or contentment," the mother noted. By framing money as a tool—no different than exercise, sleep, or nutrition—the parents remove the anxiety and social stigma often associated with household finances. They deliberately keep their children away from high-level topics like investment portfolios or retirement strategy, recognizing that such concepts are too abstract for the developmental stage of a kindergartener. Instead, they focus on the "scaffold" approach: ensuring the foundation is secure before adding higher-level financial concepts.

Implications for Future Financial Health

The success of this program carries significant implications for the future of the children’s financial habits. By age seven, the elder child is already demonstrating a high level of accountability, including the ability to recover misplaced property—a lesson learned during a high-stakes search for a lost wallet at a museum.

The Next Frontier: The "Bank of Parental Units"

As the children have mastered earning, saving, and the consequences of debt, the parents are now preparing to introduce the concept of interest. The proposed "Bank of Parental Units" will act as a personal savings account where the children can deposit their earnings to see them grow. This will introduce the concept of delayed gratification and the time value of money, shifting the children from "spenders" to "investors."

Addressing Parental Anxiety

Many parents hesitate to involve children in financial conversations for fear of causing stress or insecurity. However, this case study suggests that transparency, when properly curated, acts as a stress-reliever. By explaining that a car full of groceries represents a finite number of hours worked, the children gain a sense of security through understanding. They are no longer living in a world where items appear by magic; they are participants in a system they can control.

Long-Term Outcomes

The ultimate goal of this pedagogical approach is to raise children who understand the "cost of living" before they move out of the house. Whether or not these specific habits persist into adulthood, the children have already internalized the most critical lesson of all: that every dollar spent represents a trade-off. By allowing their children to make mistakes—losing a wallet, going into debt, or miscalculating a shared purchase—the parents are providing a safe environment for failure. In this household, the price of a lesson learned early is far cheaper than the cost of a financial mistake made in adulthood.

As they move toward their next educational phase, the parents continue to solicit advice from their community, signaling that even in the business of raising financially literate children, the most effective strategy remains one of constant adaptation and open communication.