Navigating the Path to Financial Independence: A Case Study on Debt, Homeownership, and Long-Term Stability

For many, the transition into their mid-30s brings a heightened awareness of financial trajectory. For Brian and Michael, a couple based in central Connecticut, this period of life has prompted a critical examination of their fiscal habits and future aspirations. Despite stable careers and a decade-long partnership, the duo finds themselves at a crossroads: burdened by lingering consumer debt and the elusive goal of homeownership, they have reached out to the financial community for guidance on how to transition from "surviving" to "thriving."

Main Facts: The Profile of a Modern Couple

Brian and Michael, both 34, represent a demographic often caught in the middle of the modern economic squeeze. Brian serves as a quality assurance manager for a state-run hospital, while Michael works as a project coordinator for a behavioral health agency, supplemented by advocacy work. Together, they bring home a combined annual net income of approximately $109,455.

Living in a spacious, industrial-style apartment in a refurbished mill, the couple enjoys a comfortable lifestyle. However, they are currently grappling with $28,259 in consumer debt—a reality that, while not insurmountable, feels like a significant anchor on their dreams of purchasing a home, formalizing their marriage, and building a sustainable legacy.

Chronology: A Year of Transition

The past 12 months have been defined by volatility. In August 2022, the couple’s financial plan was on track, with hopes to re-enter the housing market by late 2023. However, life intervened. A forced move from their long-term, low-cost studio apartment into a more expensive unit, combined with unexpected veterinary expenses for their two kittens, derailed their timeline.

This period of instability, while managed, forced the couple to rely on credit cards to bridge the gap. Today, they are settled into a new, larger home, but the psychological and financial weight of the recent transition has left them feeling behind their peers. They now view their lack of real estate ownership as a vulnerability in a fluctuating market and are seeking a definitive plan to secure their future.

Supporting Data: The Financial Snapshot

An analysis of their current financial health reveals a mix of strengths and areas for immediate improvement.

Debt Overview

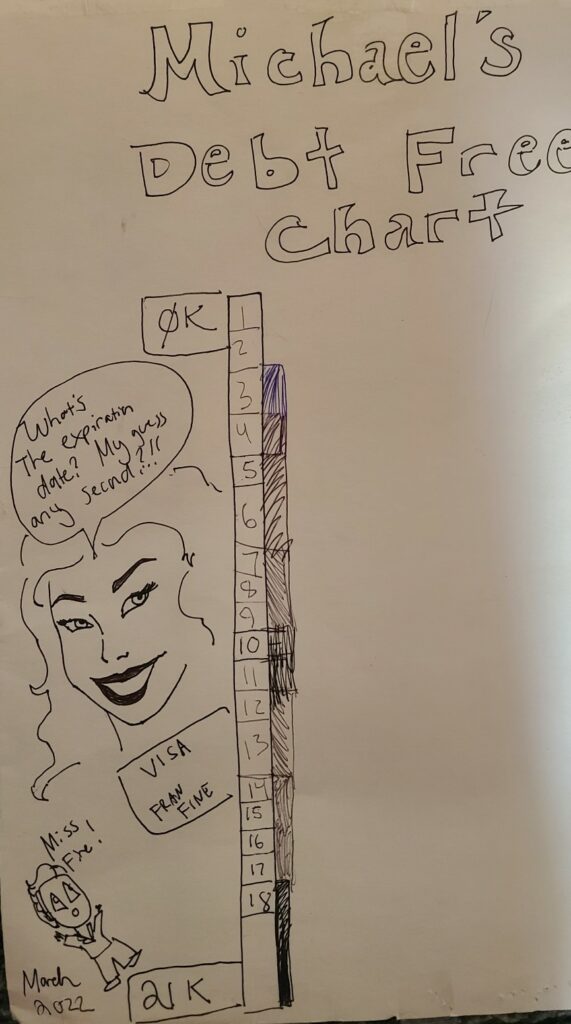

- Brian’s Visa (SCU): $16,057 (0% interest until Nov 2023)

- Michael’s Visa Platinum: $9,700 (10.99% interest)

- Brian’s Visa Platinum (Navy Federal): $2,503 (0.99% interest until Nov 2023)

- Total Debt: $28,259

Assets and Retirement

The couple has managed to build a modest asset base of $91,250, primarily through retirement vehicles. Brian has access to a state pension, a 403b, and a 457 plan—a "triple crown" of retirement security. Michael maintains a 401k with a 4% company match. Despite these tools, the couple feels their retirement accounts are underfunded and lack the diversification necessary to hedge against the potential long-term instability of Social Security.

The Budgetary Discrepancy

With an annual net income of $109,455 and annual expenses totaling $96,414, the couple technically operates with an annual surplus of roughly $13,000. However, this surplus has been absorbed by their debt service and recent life shocks, highlighting a need for more rigorous expense tracking and discretionary spending management.

Expert Analysis and Official Recommendations

Financial consultant Liz Frugalwoods, who reviewed the case, argues that the couple is in a far better position than they perceive. She characterizes their stress as "spreadsheet problems" rather than existential failures.

1. The Power of Expense Tracking

The first recommendation is the implementation of a rigorous, consistent expense-tracking system. Whether via platforms like Empower or simple spreadsheets, the goal is to identify exactly where the $13,000 annual surplus is vanishing. By categorizing expenses into "Fixed," "Reducible," and "Discretionary," the couple can identify immediate areas for adjustment.

2. The Debt-Payoff Sprint

The recommendation is a "no-spend" period to prioritize debt liquidation. By cutting discretionary spending—including dining out, gifts, and non-essential subscriptions—the couple could potentially free up an additional $1,370 per month. Combined with their existing debt payments, this would allow them to allocate roughly $4,450 toward their balances, clearing their total debt in approximately six to seven months.

3. Redefining Retirement and Homeownership

The expert advice suggests that retirement planning must take precedence over a home down payment. With access to tax-advantaged accounts that allow for up to $80,500 in combined annual contributions, the couple should focus on maximizing these vehicles before diverting cash toward real estate. A home is a life goal, but it is not a retirement strategy; building the tax-advantaged nest egg provides a safety net that real estate—an illiquid asset—cannot.

Implications: Building a Sustainable Future

The journey for Brian and Michael is as much about psychology as it is about arithmetic. They suffer from a "feast or famine" cycle: they overspend, feel shame, and then attempt to cut everything to the bone, leading to eventual burnout.

The Need for a "Middle Way"

The long-term implication for the couple is to find a sustainable equilibrium. The goal is not to live in perpetual austerity, but to align their spending with their core values. By intentionally deciding which discretionary items to reintroduce after their "spending detox," they can ensure their lifestyle remains within their means without the feeling of deprivation.

Addressing the Education Question

Regarding Brian’s desire to pursue a graduate degree, the advice is stern: unless there is an iron-clad, contractually guaranteed path to a significant salary increase, the investment is not recommended. In the current economic climate, the opportunity cost of time and tuition is too high given the couple’s pressing goals of debt freedom and homeownership.

Strategic Priorities

The final suggested roadmap for the next 12–24 months is as follows:

- Execute an immediate debt-payoff plan to neutralize high-interest exposure.

- Build a robust emergency fund that covers 3–6 months of essential expenses to prevent future reliance on credit cards.

- Maximize employer-sponsored retirement contributions to capture tax advantages and employer matches.

- Explore investment optimization, including rolling over Brian’s old 401k into an IRA for better fee management.

- Evaluate homeownership only after the above steps are firmly established and the emergency fund is fully capitalized.

By shifting their perspective from one of shame to one of strategy, Brian and Michael are well-positioned to achieve their goals. The "next level of adulting" they seek is not a destination, but a process of disciplined, values-based decision-making. Through these steps, they can transform their current financial anxiety into a solid foundation for the decade to come.