Financial Crossroads: A Case Study on Debt, Aspirations, and the Path to Stability for a Connecticut Couple

In the heart of Connecticut, 34-year-old partners Michael and Brian find themselves at a pivotal juncture. Having been together since 2013, the couple is preparing to celebrate their 10-year anniversary this November. On the surface, their lives appear stable and fulfilling: both hold steady jobs in the public and non-profit sectors, they share a beautiful, renovated mill apartment, and they are surrounded by the warmth of their two kittens. Yet, beneath this veneer of contentment, a gnawing sense of financial unease persists.

Despite a combined annual income of over $167,000, the couple feels "stuck." They are currently grappling with consumer debt, a lack of home ownership, and a lingering sense of falling behind their peers. In a candid submission to the Frugalwoods Reader Case Study series, the couple is seeking a roadmap to navigate their financial future, aiming to transition from a cycle of debt and uncertainty toward permanent financial independence and the dream of owning property.

The Chronology of a Financial Squeeze

The past year has been one of significant turbulence for Michael and Brian. In August 2022, the couple’s life was defined by the stability of a 600-square-foot studio apartment, where they lived comfortably on a modest rent of $945 per month. Their long-term strategy was clear: maintain low expenses to save for a down payment on a home, with a target of re-entering the housing market by late 2023.

However, life intervened. A combination of unforeseen veterinary expenses for their new kittens and the reality of a volatile 2022/2023 rental market forced the couple to uproot their lives. They spent three and a half months in a frantic search for a new residence, eventually settling into a luxurious, industrial-style two-bedroom apartment. While this new space offers them a home office, a library, and a sense of "adult" living, the transition came at a cost. The higher rent and the ripple effects of moving-related expenses derailed their savings timeline, leaving them feeling vulnerable and financially exposed.

Analyzing the Debt Landscape

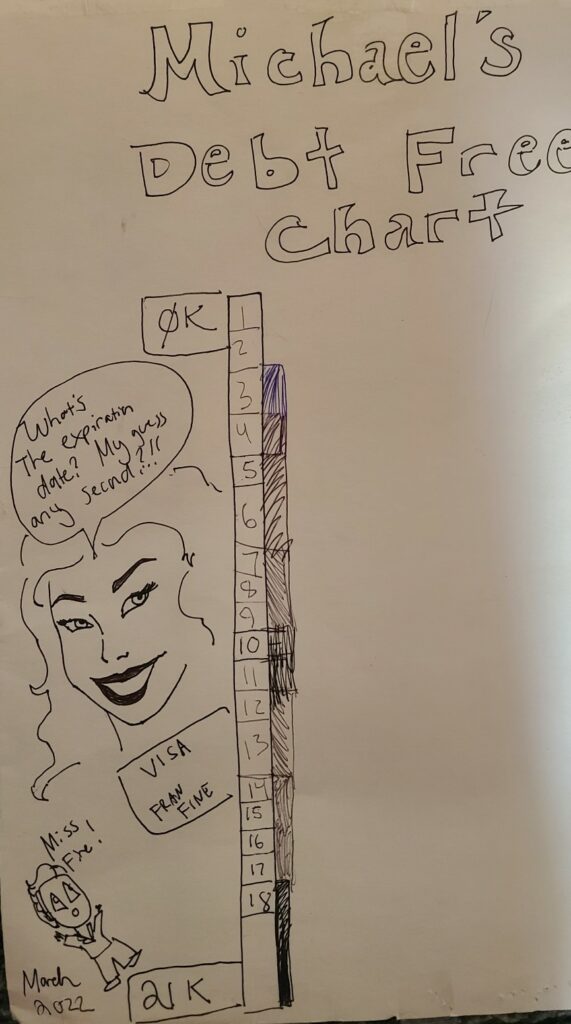

The financial picture for the couple is a study in contrasts. On one hand, Brian has achieved a significant milestone by paying off $58,000 in student loans and securing a position at a state-run hospital that offers robust benefits, including a pension and comprehensive healthcare. On the other hand, the couple currently carries approximately $28,259 in consumer credit card debt.

Current Debt Obligations

- Brian’s Visa (SCU): $16,057 (0% interest until November 2023, then 17.99%)

- Michael’s Visa Platinum: $9,700 (10.99% interest)

- Brian’s Visa Platinum (Navy Federal): $2,503 (0.99% until November 2023, then 17.74%)

The urgency of their situation is dictated by the expiration of these promotional interest rates. As November approaches, the couple faces the prospect of high-interest debt that could quickly snowball if not addressed with a disciplined, aggressive repayment strategy.

Professional Insights: A Reality Check

In response to their situation, financial expert Liz Frugalwoods offers a perspective grounded in objective reality. She argues that while the couple feels "behind," their situation is far from catastrophic. "Brian assumes that everyone else his age has it together," she notes. "I can assure him that they do not."

According to the analysis, the couple’s core issue is not a lack of income, but a lack of structured tracking. With a net annual income of $109,455 and expenses totaling $96,414, the couple technically has a surplus of over $13,000 annually. The problem lies in the "leakage"—money flowing toward unexamined expenses that prevent them from reaching their larger life goals.

The Strategy for Debt Elimination

The recommended approach is a rigorous "spending detox." By categorizing expenses into Fixed, Reduceable, and Discretionary categories, the couple can identify significant areas for immediate cuts.

- Discretionary Spending: The recommendation is to eliminate non-essential spending—such as dining out, gifts, and luxury subscriptions—entirely for a short-term period.

- Debt Snowball: By redirecting the $2,000 currently being "frittered away" into a focused, aggressive debt-repayment fund, the couple could potentially clear their entire $28k debt burden in less than seven months.

Prioritizing the Future: Retirement and Home Ownership

A central question for the couple is how to balance competing financial desires. Liz Frugalwoods outlines a clear hierarchy of needs to ensure the couple does not sacrifice their long-term security for short-term desires.

1. The Hierarchy of Priorities

- Debt Elimination: This is the absolute priority. High-interest debt is a wealth killer that must be eradicated before any other major financial maneuvers are considered.

- Emergency Fund: Once debt is cleared, the couple must build a robust cash buffer. Currently, they have $9,000 in savings, which covers only about one month of expenses. A target of three to six months is essential to prevent future "emergencies" (like vet bills or car repairs) from becoming new debt cycles.

- Retirement Investing: With access to a 403b, a 457b, and a pension, Brian has the "triple crown" of retirement vehicles. The recommendation is to maximize these contributions before ever considering the luxury of a home down payment.

- Home Ownership: This is relegated to the final stage. While the desire to have a garden and land is valid, buying a home while carrying consumer debt and under-funded retirement accounts is a recipe for financial stress.

Addressing the "Master’s Degree" Dilemma

Brian has expressed a desire to pursue a graduate degree. However, the expert analysis offers a stark warning: "Don’t do it unless there is a precise, printed, iron-clad correlation to making more money." In the current economic climate, education is a significant investment of both time and capital. If the degree does not result in a guaranteed, significant salary increase, it should be viewed as a hobby rather than a career strategy. Given their goal of becoming debt-free and owning property, the recommendation is to defer academic pursuits until the financial foundation is rock-solid.

Implications for Long-Term Wellness

The psychological toll of financial instability is evident in the couple’s narrative. Both Michael and Brian admit to feeling "shame" regarding their financial state, leading to a cycle of isolation. The proposed solution is not just about numbers; it is about changing their relationship with money.

By tracking every dollar, the couple will shift from a "feast or famine" cycle to a state of intentional spending. The ultimate goal is not to reach a life of austerity, but to find a "comfortable middle" where they can rest, secure in the knowledge that they are living within their means.

Key Takeaways for the Couple:

- Track Everything: Utilize tools like Empower or a simple spreadsheet to gain visibility into cash flow.

- Aggressive Debt Payoff: Use the current surplus to clear all credit card debt before interest rates spike in November.

- Maximize Tax-Advantaged Accounts: Prioritize the 457b and 401k to leverage long-term compound growth.

- Redefine "Emergency": Recognize that car repairs and vet bills are predictable life events, not emergencies. Budget for them annually.

- Patience is a Virtue: Achieving home ownership is a 5-to-10-year goal, not a 12-month one.

In conclusion, Michael and Brian are in a strong position, provided they take decisive action now. By aligning their daily spending with their long-term vision, they can transform their current anxiety into the confidence of a household that is truly in control of its own destiny. The "next level of adulting" they seek is not found in a bank account balance, but in the discipline and clarity that will allow them to build a lasting legacy on their own terms.