Financial Crossroads: A Case Study on Modern Adulthood, Debt, and the Path to Stability

In the heart of Connecticut, Brian and Michael, both 34, find themselves standing at a pivotal junction of their lives. A couple since 2013, they have navigated a decade of personal growth, career pivots, and the challenges of the modern economy. Yet, as they approach their 10-year anniversary this November, the pair feels a mounting sense of urgency. Despite successful careers—Brian as a quality assurance manager for a state-run hospital and Michael as a project coordinator for a state behavioral health agency—they are grappling with a persistent cycle of consumer debt and a lack of property ownership.

This article explores their journey, the systemic and personal hurdles they face, and the professional guidance offered to help them transition from financial anxiety to a position of long-term security and wealth-building.

The Chronology of a Modern Struggle

Brian and Michael’s story is one shared by many in their generation—a narrative of high aspirations competing with the realities of a volatile economic landscape. For years, they enjoyed the relative simplicity of a 600-square-foot studio apartment, keeping costs low while they built their lives. However, the events of 2022 and 2023 forced a sudden acceleration of their life plan.

The couple was displaced from their long-term home and forced to navigate a difficult, high-cost rental market. This transition, combined with unexpected veterinary expenses for their two kittens, acted as a catalyst that disrupted their financial trajectory. While they had previously forecasted an entry into the housing market by late 2023, these unplanned costs forced them to hit the pause button.

Today, the couple resides in a refurbished mill, a space that offers them room to breathe and a dedicated home office. While they appreciate the industrial beauty of their new surroundings, the psychological weight of their financial situation remains a constant presence. For Michael, the struggle is marked by feelings of shame regarding his financial choices; for Brian, it is a sense of being "behind" his peers in terms of homeownership, academic achievements, and athletic goals.

Supporting Data: The Financial Snapshot

To understand the scope of their situation, one must look at the raw data. The couple maintains a combined annual gross income of $167,544, resulting in a net annual take-home pay of approximately $109,455.

The Debt Burden

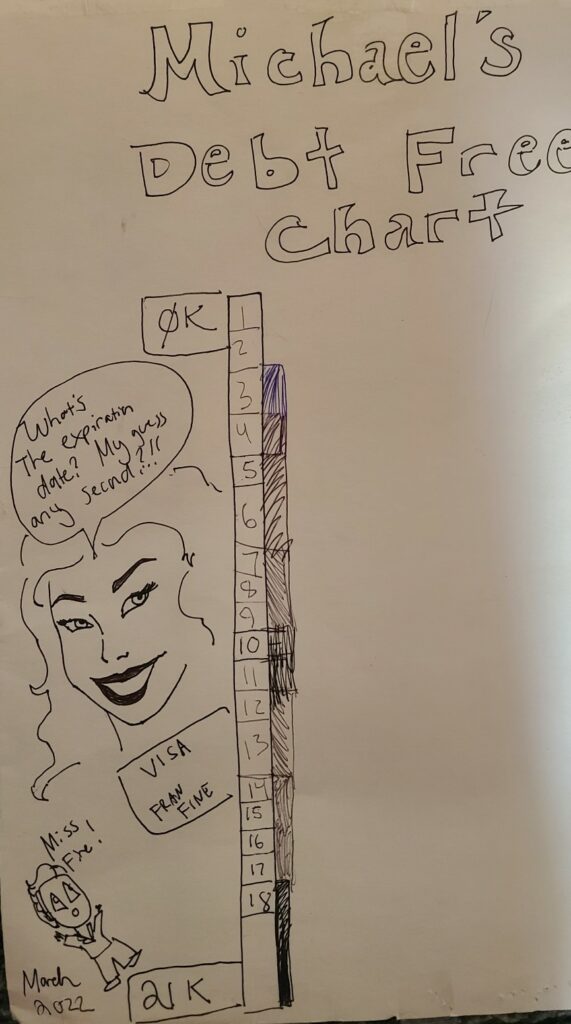

The couple currently carries $28,259 in consumer debt, primarily spread across credit cards. The structure of this debt is a significant concern:

- Brian’s Visa (SCU): $16,057 (0% interest until November 2023, escalating to 17.99% thereafter).

- Michael’s Visa Platinum: $9,700 (10.99% interest).

- Brian’s Visa Platinum (Navy Federal): $2,503 (0.99% interest until November 2023, escalating to 17.74% thereafter).

Assets and Retirement

Despite their concerns, the couple has managed to amass a total of $91,250 in assets. This includes a robust mix of tax-advantaged accounts:

- Michael’s 401k: $36,992.

- Brian’s old 401k: $19,305.

- Brian’s Pension Fund: Projected payout of $4,150/month in 2054.

- Various other accounts: Including 457, 403b, IRAs, and HSAs.

The monthly expense profile is substantial, totaling roughly $8,035. This figure includes $2,000 in rent and significant monthly allocations toward debt repayment and high-cost living expenses in Connecticut.

Expert Analysis: A Path Toward Equilibrium

Financial experts, including those from the Frugalwoods platform, suggest that while the couple feels "behind," they are actually in a strong position. The primary issue is not a lack of income, but a lack of intentionality in directing that income toward their stated goals.

The Power of Expense Tracking

The first pillar of the recommended strategy is a rigorous transition to expense tracking. The couple currently has a net income that exceeds their spending by approximately $13,000 annually. If this surplus is not being captured, it is likely being lost to "lifestyle creep" or unmonitored discretionary spending. Experts advise that the couple must adopt an "expense tracking system"—whether via apps like Empower or simple spreadsheets—to ensure every dollar is accounted for.

The Debt Payoff Strategy

The consensus on their debt is clear: it is not a moral failing, but a "spreadsheet problem." The recommendation is to immediately enter a "spending detox." By categorizing expenses into Fixed, Reducible, and Discretionary, the couple can identify thousands of dollars in annual savings.

By eliminating discretionary spending—such as eating out, non-essential home goods, and entertainment—the couple could redirect those funds to pay off their $28,259 debt load in as little as 6.5 months. Once the debt is cleared, the psychological "shame" that currently hinders their progress will dissipate, replaced by the momentum of a clean slate.

Long-Term Implications and Strategic Priorities

For Brian and Michael, the goal of homeownership is achievable, but only if they follow a disciplined hierarchy of financial priorities.

1. The Hierarchy of Needs

Experts have outlined a clear sequence for the couple to follow:

- Debt Repayment: High-interest debt is the greatest barrier to wealth.

- Emergency Fund: Currently, they have about one month of expenses in cash. This must be increased to cover 3–6 months of living costs.

- Retirement Contributions: Before saving for a down payment, they must maximize their tax-advantaged retirement accounts, particularly their 401k and 457b plans.

- Home Ownership: Only after the above are stabilized should the couple look toward the housing market.

2. The Education Debate

Regarding Brian’s desire to pursue a graduate degree, the professional consensus is cautious. A master’s degree should only be pursued if there is a direct, iron-clad, and quantifiable link to a higher salary. If the degree is purely for personal interest, it should be categorized as a discretionary expense and deferred until the couple is entirely debt-free and retirement-secure.

3. The Pension and Social Security Wildcards

While Brian has access to a government pension—a rare and valuable asset in the modern workforce—he should not rely on it as his sole retirement vehicle. The same applies to Social Security. Diversification remains the gold standard; by maximizing their private 401k and IRA contributions, the couple builds a layer of protection that ensures their lifestyle remains independent of external political or economic shifts.

Conclusion: Reframing the Narrative

Brian and Michael’s situation is emblematic of the "mid-career squeeze." They have successfully navigated the challenges of employment and built a foundation of assets, yet they remain tethered to debt that prevents them from reaching the next level of financial independence.

The path forward for them does not require a higher income, but rather a higher degree of discipline. By treating their finances with the same analytical rigor they apply to their professional roles, they can transition from a state of "feast and famine" to a sustainable, secure lifestyle. In ten years, the difference between their current anxiety and their future success will be defined by the decisions they make in the next six months. As they prepare to celebrate their 10th anniversary, the most valuable gift they can give themselves is the realization that they possess all the tools necessary to build the legacy they desire.