A New Chapter for Steel City Finance: Sagehaven Bancorp Seeks to End Pittsburgh’s Two-Decade De Novo Drought

By [Your Name/Journalistic Staff]

For nearly twenty years, the financial landscape of Pittsburgh—a city synonymous with industrial might and the institutional heft of banking giants like PNC and BNY—has remained largely static in terms of new entrants. That era of stagnation may soon be coming to a close. A veteran-led group has officially signaled its intent to shake up the local market, filing applications for federal approval to establish Sagehaven Bancorp, a proposed community bank designed to cater specifically to the region’s small-to-mid-market enterprises and high-net-worth individuals.

If successful, Sagehaven would mark the first de novo bank to launch in the city in roughly two decades, representing a significant test of the current regulatory appetite for new financial institutions and a bold bet on the enduring vitality of the Pittsburgh business ecosystem.

The Visionaries Behind the Charter

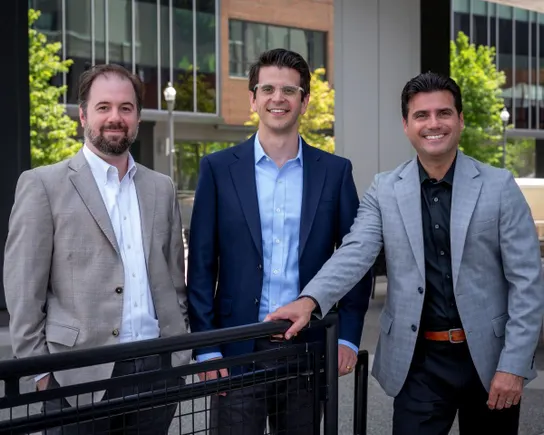

The project is spearheaded by Brian Tabb, a former senior vice president of corporate treasury at BNY. Tabb, who departed the global financial institution in March, has stepped into the role of proposed CEO for Sagehaven. His transition from the rigid, high-tech corridors of a global systemic bank to the entrepreneurial frontier of a community start-up is driven by a desire for localized impact.

Tabb is joined by a seasoned executive team with deep roots in the region’s financial machinery. Angelo Innamorato, a former BNY and Huntington executive, is slated to serve as the bank’s chief operating officer. Rounding out the leadership trio is Jared Leland, a former partner at the law firm Houston Harbaugh, who will act as the bank’s chief counsel. Together, the team represents a calculated blend of treasury management, operational expertise, and legal acumen, aimed at navigating the arduous process of obtaining a national charter.

For Tabb, the choice of Pittsburgh as the launchpad for his banking career is not merely strategic; it is deeply personal. "I really, truly want to immerse myself in this community and make an impact across this community, particularly given that my daughters are going to be raised here," Tabb shared in an interview. He views the bank as a vehicle for community engagement, emphasizing that the primary appeal of the banking sector lies in the tangible influence a local lender can have on the prosperity of its clients and neighbors.

Chronology and Strategic Milestones

The journey to launch Sagehaven is currently in its infancy but moving at a deliberate, methodical pace. The team officially submitted its applications to the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC) on Tuesday.

- March 2024: Brian Tabb departs BNY to focus full-time on the formation of Sagehaven.

- Late 2024: The leadership team finalizes the strategic roadmap, opting for a national charter to maximize geographic reach.

- November 2024: Formal submission of charter and deposit insurance applications to the OCC and FDIC.

- April 2027 (Target): The proposed opening date for Sagehaven’s inaugural branch in Pittsburgh’s central business district.

The selection of a national charter over a state charter reflects a forward-looking strategy. Tabb noted that while the bank will be firmly planted in the Steel City, its prospective clients often conduct business across state lines—specifically in Ohio, West Virginia, and upstate New York. By securing a national charter, Tabb intends to ensure that the bank can follow its clients wherever their growth takes them. "I don’t want to close the door on anyone," he explained.

Leveraging Technology: The "Mile 20" Advantage

One of the most significant hurdles for legacy banks is the "tech debt" accumulated over decades of siloed systems and antiquated infrastructure. Tabb sees Sagehaven’s start-up status as a distinct competitive advantage.

"Starting a new bank enables us to employ modern, rather than legacy, technology," Tabb noted, describing the process as "entering at mile 20 of a marathon instead of mile two." By avoiding the burden of retrofitting aging core systems, Sagehaven intends to deploy agile, AI-driven platforms from the start.

Tabb’s tenure at BNY was, by his own admission, instrumental in shaping this technological philosophy. Working under the leadership of BNY CEO Robin Vince—a vocal proponent of artificial intelligence—Tabb witnessed firsthand how AI could streamline operations and enhance client service. "It was ingrained in our everyday life at BNY," Tabb said. "Now, that informs how we are thinking about our strategy for a much, much smaller scale."

The bank’s initial strategy will focus on efficiency and seamlessness, utilizing the latest in financial technology to bridge the gap between the high-touch service expected by private wealth clients and the automated speed required by small-business owners.

The Regulatory Climate and Market Context

The timing of Sagehaven’s application arrives during a notable shift in federal regulatory activity. Under Comptroller Jonathan Gould, the OCC has signaled a more welcoming stance toward de novo applications. Last year alone, the agency processed 18 applications—a figure matching the total volume of the previous four years combined. So far this year, the OCC has received more than two dozen applications, with several already granted.

While Tabb acknowledges that this shift in the regulatory wind is "helpful," he maintains that it was not the primary driver for his application. "We’re starting a community bank. We’re not necessarily going into any of these niche products, like digital assets," Tabb clarified. Instead, he views the regulators’ commitment to a 120-day window for preliminary decisions as a positive sign that the process has become more predictable and transparent.

For the industry, this uptick in charter applications suggests a renewed interest in the community banking model. In an era dominated by digital-only neo-banks and monolithic global institutions, there remains a persistent demand for banks that can provide personalized service rooted in local expertise.

Official Responses and Next Steps

The regulatory review process is now underway. An FDIC spokesperson has confirmed the receipt of Sagehaven’s application for deposit insurance, a critical step in the path toward becoming a licensed entity. While the application had not yet appeared on the OCC’s public portal as of Thursday, the filing marks the commencement of what is expected to be a rigorous, months-long vetting process.

The OCC, which maintains a high bar for capital adequacy, management quality, and risk management systems, will now scrutinize Sagehaven’s business plan to ensure it meets federal standards. For the leadership team, the next two years will be spent securing capital, building out the technological infrastructure, and preparing for the grand opening in 2027.

Implications for the Pittsburgh Market

The arrival of Sagehaven could serve as a bellwether for the Pittsburgh economy. If a new, independent bank can successfully navigate the complexities of federal regulation and establish a foothold in a market dominated by multi-billion-dollar institutions, it could signal a resurgence in local business confidence.

Furthermore, Sagehaven’s focus on the central business district suggests a continued belief in the vitality of downtown Pittsburgh, even as remote and hybrid work models have forced other urban centers to recalibrate their commercial real estate needs.

For the clients Sagehaven targets—the mid-market companies that often struggle to get the attention of the "too-big-to-fail" banks—the arrival of a new, nimble, and technology-forward player could introduce a much-needed layer of competition. By focusing on the "human" element of banking while utilizing the "machine" efficiency of modern software, Tabb and his team are banking on the idea that Pittsburgh is ready for a financial institution that is as modern as it is local.

As the industry watches the progress of the Sagehaven application, the broader message is clear: the de novo era is not dead. In the right hands, with the right technology and a deep commitment to the local community, the prospect of starting a bank from the ground up remains one of the most compelling, albeit challenging, ventures in American finance. Whether Sagehaven succeeds in its marathon run will ultimately depend on its ability to turn these lofty, high-tech plans into the day-to-day reality of community banking excellence.