The Great Migration: Why Capital is Abandoning Mutual Funds for the ETF Revolution

The wealth management landscape is undergoing a structural transformation that is no longer a matter of debate—it is a matter of record. As of the week ending July 1, 2026, the latest asset flow data from the Investment Company Institute (ICI) confirms a profound migration of capital away from traditional mutual funds and into the more agile, tax-efficient structure of Exchange-Traded Funds (ETFs).

This is not a simple case of investors fleeing the market; rather, it is a calculated "rotation" of capital. Investors are not leaving the markets; they are upgrading their vehicles. With ETFs capturing $32.3 billion in net new issuance while long-term mutual funds suffered a $28.87 billion exodus, the industry is witnessing a clear divergence that suggests the "mutual fund era" is rapidly giving way to the "ETF era."

The Core Data: A Tale of Two Structures

The ICI data for the first week of July 2026 provides a stark snapshot of this shifting preference. While the aggregate long-term fund industry managed a net inflow of $3.43 billion, this number masks a violent tug-of-war beneath the surface.

Equity Market Divergence

The most significant battlefield remains the equity market. Equity ETFs saw a massive influx of $19.70 billion, with domestic equity allocations leading the charge at $16.27 billion, supplemented by $3.42 billion in world equity exposure.

In total contrast, traditional equity mutual funds faced a combined outflow of $29.91 billion. Domestic equity funds bore the brunt of this shift, shedding $22.10 billion, while international and world equity funds saw investors pull $7.81 billion. Even in the hybrid fund category—which often serves as a "middle-ground" for conservative investors—ETFs managed to attract $316 million, while mutual funds saw a contraction of $2.69 billion.

The Fixed Income Exception

Fixed income remains the only sector where mutual funds have maintained a foothold, though they are still being outpaced by their ETF counterparts. Bond ETFs secured a robust $14.94 billion in net issuance, split between $13.15 billion in taxable products and $1.79 billion in municipal options. Bond mutual funds did manage to attract $3.73 billion in net inflows, but this pales in comparison to the structural preference shown for bond ETFs.

Chronology of a Shift: How We Got Here

The ascent of the ETF is not a sudden phenomenon but the culmination of a decade-long evolution in investor behavior and advisory practices.

- 2021–2023: The Adoption Phase. As retail investors became more tech-savvy, the convenience of intraday liquidity began to outweigh the "set it and forget it" convenience of mutual fund end-of-day pricing.

- 2024: The Rise of the Model Portfolio. The industry began a pivot toward model portfolios, providing advisors with pre-packaged, diversified strategies that prioritize efficiency.

- 2025: The Fee Compression War. As advisors faced pressure to lower costs for clients, the 0.25% fee gap between ETFs and mutual funds became impossible to ignore, accelerating the migration.

- 2026: The "Fever Pitch." Current data reflects a mature market where the infrastructure (custodians, trading platforms, and model marketplaces) is fully optimized for ETFs, leaving mutual funds as a legacy product for an aging demographic.

The "Model Moment": Efficiency as a Catalyst

A central theme at the ETF Exchange 2026 conference was the concept of the "Model Moment." As market dispersion increases, the ability to build and adjust portfolios with precision has become a critical skill for wealth managers.

Modern model portfolios act as navigational guides. By utilizing ETFs, advisors can construct a portfolio that aligns with a specific risk profile and set of goals, all within an automated, transparent system. This shift has profound implications for the advisor-client relationship. When an advisor spends less time on manual trade execution and fund selection, they spend more time on high-value activities: tax planning, estate coordination, and emotional coaching.

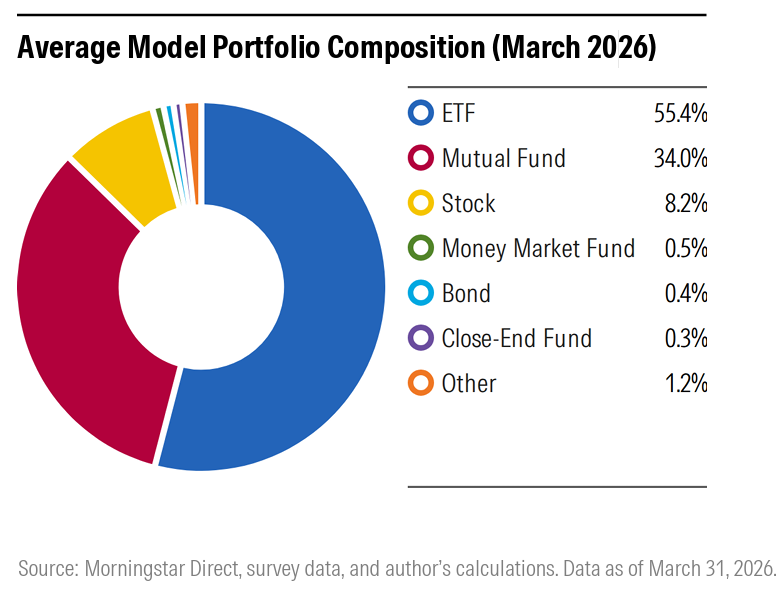

According to Morningstar data from March 2026, ETFs now occupy an average of 55% of all model portfolio allocations. To put this in perspective, that figure stood at just 43% five years ago. Furthermore, the assets within custom model portfolios have exploded to $258 billion—a staggering 40% year-over-year increase. This growth is driven by the desire for tactical allocation, where advisors can pivot sectors or asset classes in real-time to respond to volatility.

Structural Advantages: Why the Migration is Permanent

The migration from mutual funds to ETFs is not merely about brand preference; it is rooted in three fundamental structural advantages that directly benefit the end investor.

1. Lower Fee Hurdles

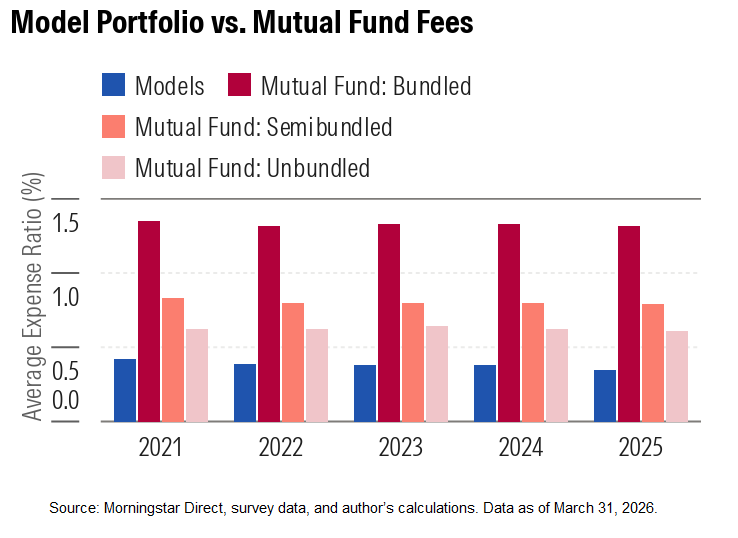

The cost of ownership is the most tangible benefit. Morningstar’s 2025 year-end data highlights that model portfolios featuring ETFs carried an average asset-weighted fee of 0.35%, compared to 0.61% for unbundled mutual funds. For an investor with a significant retirement nest egg, this 26-basis-point difference can result in thousands of dollars in additional wealth over a decade of compounding.

2. Intraday Liquidity

Mutual funds are governed by the "closing bell" rule—they price and trade only once per day. In a volatile market, this can be a disadvantage. ETFs, by contrast, offer intraday liquidity. This allows advisors to execute trades, rebalance accounts, or exit positions during the trading day, providing a level of control that mutual funds simply cannot match.

3. Tax Efficiency

Perhaps the most "invisible" but impactful advantage is the tax shield provided by the ETF creation/redemption mechanism. In a mutual fund, when other investors sell their shares, the fund manager may be forced to sell underlying assets to raise cash, which triggers capital gains taxes for all remaining shareholders. ETFs use an "in-kind" process where shares are exchanged for the underlying securities, effectively bypassing the tax event for the average investor.

Implications for the Future of Finance

What does this mean for the future of the asset management industry? The implications are three-fold:

The Death of the "Stock-Picker" Mutual Fund:

As passive and semi-passive ETFs continue to dominate, actively managed mutual funds are under extreme pressure to prove their alpha. If they cannot outperform their benchmark after fees, they will continue to lose assets to low-cost ETF alternatives.

The Rise of Customization:

The growth of the "custom model" segment suggests that the future of wealth management is hyper-personalized. Advisors are increasingly using ETFs as "building blocks" to create bespoke portfolios that consider a client’s specific tax bracket, charitable goals, and ESG preferences.

Consolidation of Distribution:

Asset managers who do not have a robust ETF shelf are finding themselves on the outside looking in. We expect to see a wave of traditional mutual fund firms either launching ETF suites or acquiring existing ETF providers to stay relevant in an increasingly automated distribution landscape.

Conclusion

The ICI data from the first week of July 2026 serves as a definitive signal: the financial markets are voting with their feet. The transition from mutual funds to ETFs is not a cyclical fluctuation; it is a structural evolution. As the industry moves toward a future defined by lower costs, greater liquidity, and superior tax efficiency, the ETF has emerged as the definitive instrument of choice for the modern investor.

For the financial advisor, the message is clear: the tools of yesterday are no longer sufficient to meet the challenges of tomorrow. By embracing the ETF-centric model portfolio, they are not only optimizing their own practices but providing a superior, more transparent, and more efficient experience for their clients. As this trend continues to gain momentum, the gap between the two fund structures will likely widen, cementing the ETF’s position at the heart of the global wealth management ecosystem.