Global Markets Teeter on a Trillion-Dollar Borrowing Binge: A Deep Dive into Rising Leverage and Systemic Risks

Posted: June 30, 2026

In the annals of financial wisdom, legendary investor Charlie Munger once distilled the pathways to ruin for even the brightest minds into three potent vices: liquor, ladies, and leverage. As global stock markets surge, particularly in the technology sector, it appears a significant cohort of investors worldwide is enthusiastically putting the "leverage" theory to a rigorous, and potentially perilous, test. The exuberance surrounding unprecedented market rallies, fueled by a potent mix of innovation and speculative fervor, has seen a dramatic escalation in margin debt and other forms of borrowed capital, raising questions about the sustainability of current valuations and the potential for magnified downturns.

From the vibrant trading floors of Seoul to the tech-centric exchanges of Taipei and the expansive markets of New York, a common thread of aggressive borrowing now weaves through the global investment landscape. This phenomenon, while often a concurrent indicator of bull markets, is reaching levels that warrant closer scrutiny, prompting financial analysts and regulators to weigh the immediate gratification of amplified gains against the specter of outsized losses.

The Main Facts: A Global Symphony of Debt and Daring

The current market environment is characterized by astonishing growth rates in key equity indices, particularly those influenced by the artificial intelligence (AI) boom. This growth, however, is increasingly underpinned by borrowed money, a trend observed across multiple continents.

- South Korea’s Market Ascent: The South Korean stock market has been a standout performer, skyrocketing by nearly 200% over the past 12 months. This meteoric rise has naturally drawn significant investor attention, leading to a substantial increase in margin lending.

- Taiwan’s AI Fever: Similarly, Taiwan’s market, heavily influenced by its semiconductor industry and its pivotal role in the AI supply chain, has doubled in value over the last year. Here too, individual investors are borrowing heavily to chase returns.

- America’s Record Margin Debt: Not to be outdone, the United States has also witnessed a historic surge in margin debt. This figure, representing funds borrowed from brokerages to purchase securities, has reached unprecedented levels, supplemented by other high-leverage instruments.

This confluence of rapid market appreciation and aggressive borrowing presents a complex scenario, where the potential for continued gains is balanced by the amplified risks inherent in leveraged positions.

Chronology of Exuberance: A Year of Unprecedented Growth and Borrowing

The past year, culminating in mid-2026, marks a period of extraordinary market performance and a corresponding escalation in investor leverage.

Mid-2025 Onwards: The Genesis of the AI Boom and Market Rallies

The seeds of the current market exuberance were sown in the preceding months, as advancements in artificial intelligence began to translate into tangible corporate earnings and groundbreaking product announcements. This period saw a gradual, then accelerating, rally in technology and AI-related stocks globally. As these initial gains materialized, investor confidence soared, paving the way for more aggressive investment strategies.

Early 2026: South Korea Leads the Charge in Leverage

By the beginning of 2026, the South Korean stock market was already demonstrating remarkable momentum. Investors, keen to capitalize on the sustained upward trajectory, began to significantly ramp up their use of margin loans. Data from the Korea Financial Investment Association reveals a dramatic increase in this period. As of early May 2026, the outstanding balance of margin loans had reached an staggering 36.3967 trillion won. This represented an increase of 8.976 trillion won, or approximately 33%, from the 27.4207 trillion won recorded at the start of the year.

The phenomenon extended beyond conventional margin loans. Loans secured by deposited securities, a method employed by investors who had already exhausted their initial credit limits, also witnessed a substantial rise. This category swelled by nearly 2 trillion won within the year, reaching 25.9297 trillion won. This aggressive pursuit of additional purchases, often through strategies like dollar-cost averaging despite the increased burden of collateral requirements, underscored a pervasive belief in sustained market growth and a willingness to take on considerable risk.

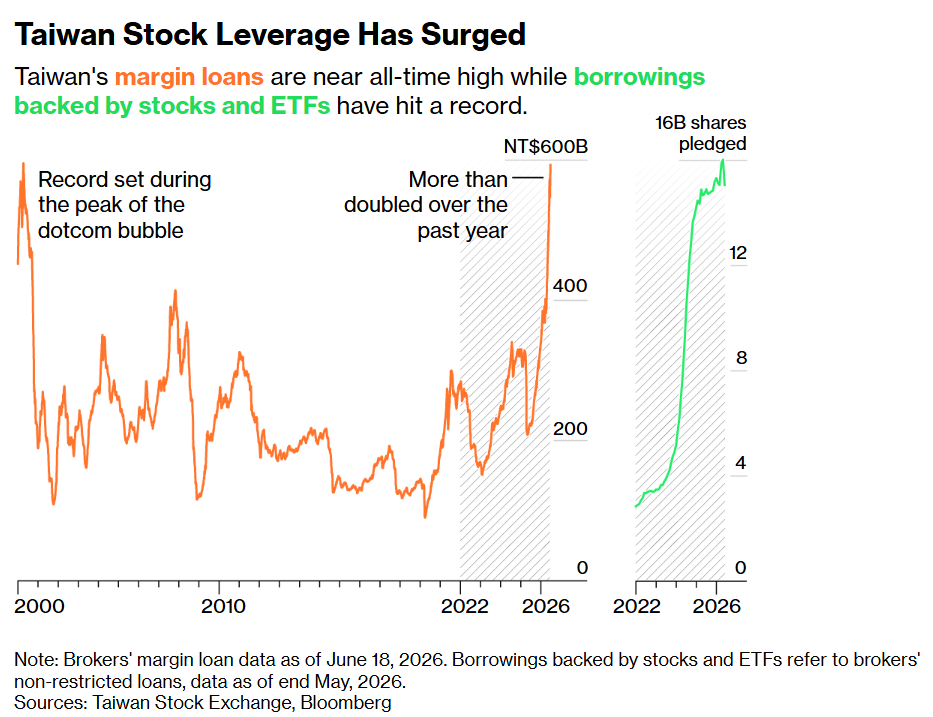

Spring 2026: Taiwan Catches AI Fever and Borrows Aggressively

Following South Korea’s lead, or perhaps concurrently, Taiwan’s market experienced its own AI-fueled surge. The island nation, home to critical components of the global technology supply chain, saw its market double within the past year. The sentiment among Taiwanese investors became markedly bullish, characterized by a widespread belief that "Buy any stock and you will make money." This anecdotal evidence, exemplified by individuals like 26-year-old Andy Cheng, an unemployed investor leveraging borrowed funds to own $60,000 worth of Taiwanese tech stocks, highlighted a speculative environment where risk assessment was potentially overshadowed by the allure of quick gains. The concentration of this enthusiasm around companies like Taiwan Semiconductor Manufacturing Company (TSMC), a linchpin in AI chip production, further amplified the market’s upward trajectory and the associated borrowing.

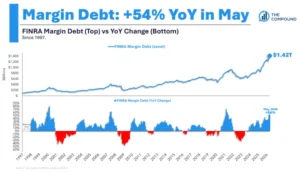

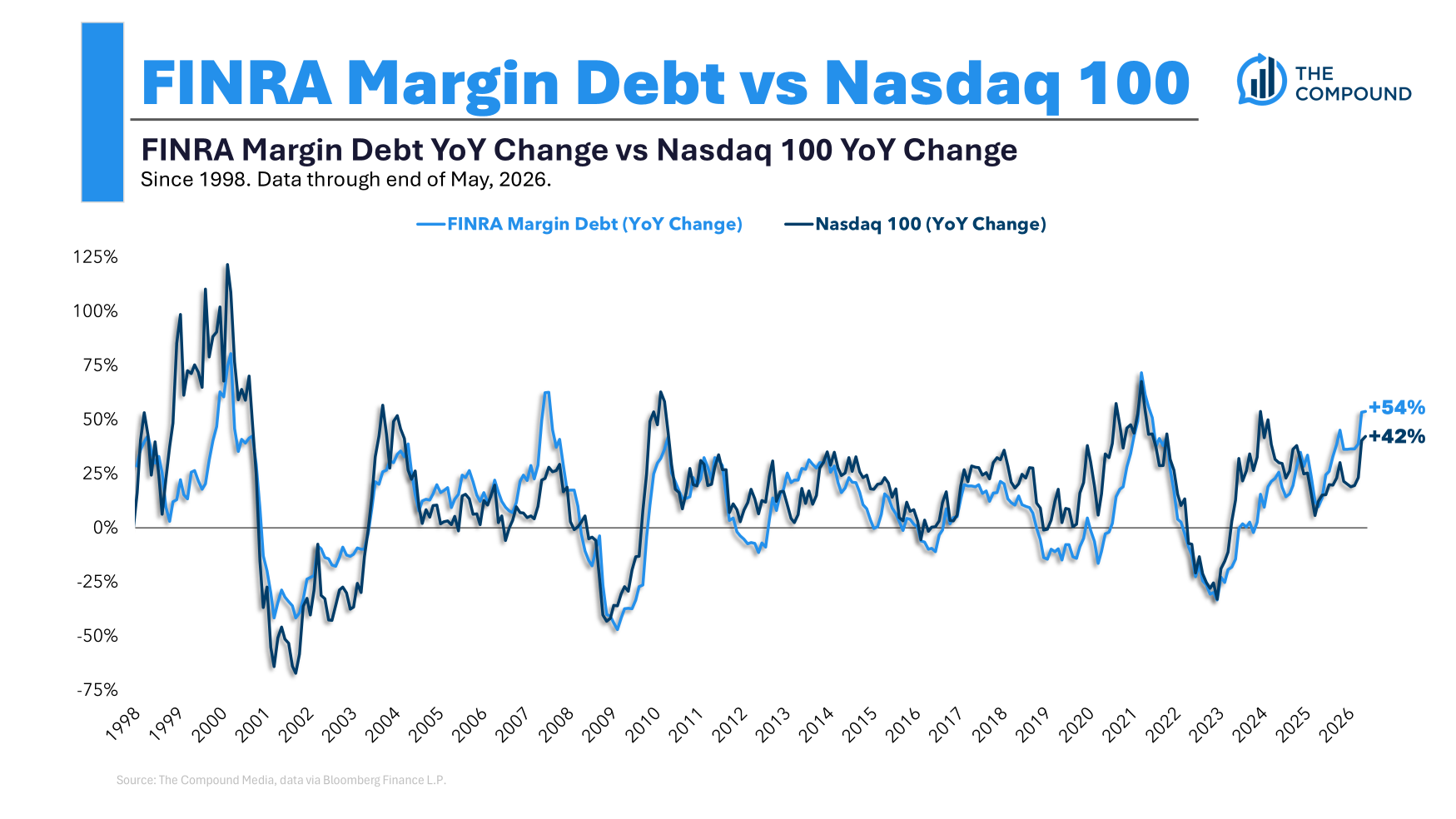

Mid-2026: The U.S. Joins the Trillion-Dollar Margin Club

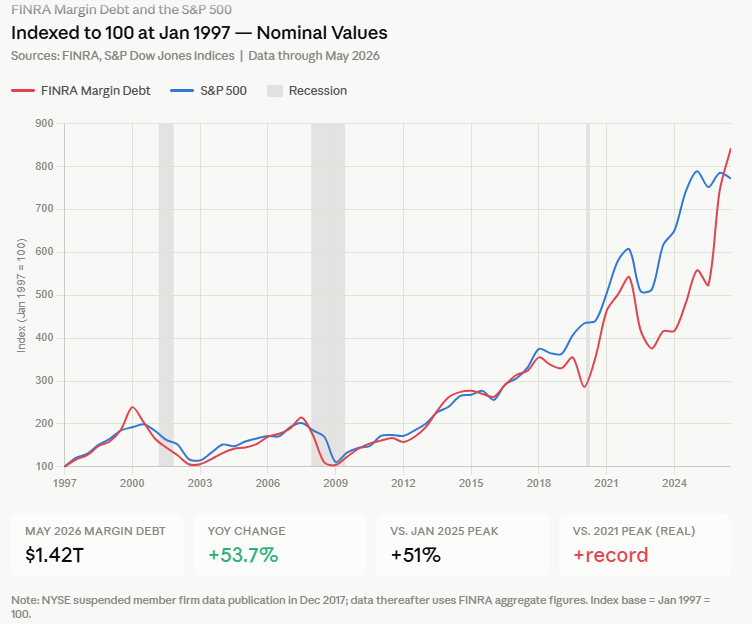

As the global tech rally persisted, American investors demonstrated their own appetite for leveraged positions. By May 2026, U.S. margin debt, as reported by the Financial Industry Regulatory Authority (FINRA), had surged to a record $1.4 trillion. This figure represented a substantial 54% increase from just a year prior.

Crucially, this staggering sum only encompasses a portion of the actual leverage deployed in the U.S. market. The Wall Street Journal highlighted that this record does not account for the growing popularity of high-risk leveraged exchange-traded funds (ETFs), which are designed to produce double or triple the daily returns of their underlying assets. Furthermore, the burgeoning trade in options tied to these leveraged ETFs, along with other sophisticated instruments like box spread loans and the embedded leverage in futures and options contracts, suggests the true scale of market borrowing is considerably higher than publicly reported margin debt statistics alone. This comprehensive borrowing binge, spanning retail and institutional investors alike, paints a picture of a market heavily reliant on continued upward momentum to sustain its elevated levels.

Supporting Data: Quantifying the Leverage Phenomenon

The data presented paints a clear picture of escalating leverage in direct correlation with market performance.

- South Korean Margin Debt: The outstanding balance of margin loans reached 36.3967 trillion won as of May 2026, a 33% jump from the start of the year. Loans secured by deposited securities also hit 25.9297 trillion won. These figures underscore the aggressive stance of Korean investors.

- U.S. Margin Debt: FINRA data indicates U.S. margin debt rose 54% to a record $1.4 trillion in May 2026 from a year earlier. This substantial increase highlights the growing reliance on borrowed funds across the American market.

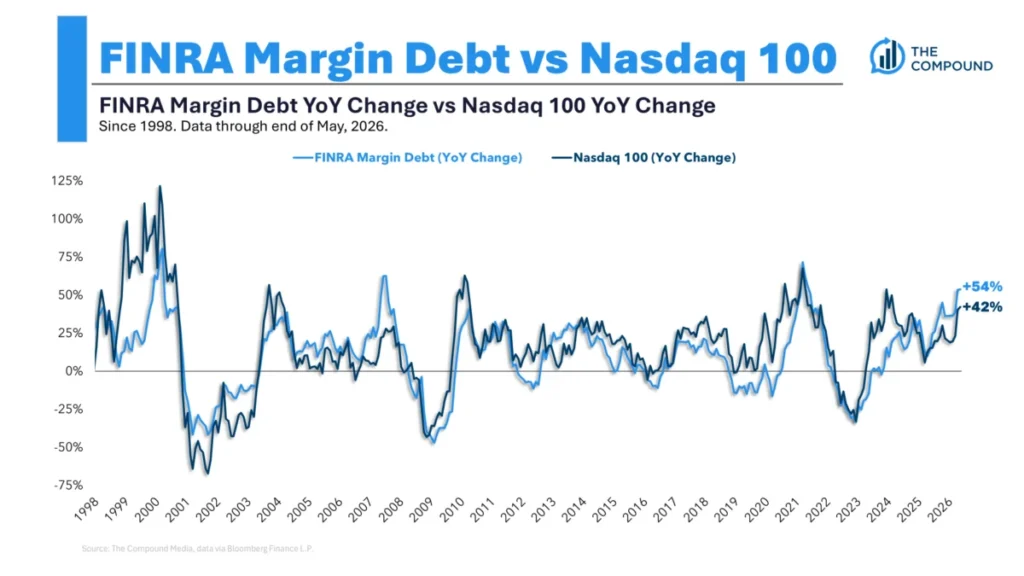

- Margin Debt as a Concurrent Indicator: As noted by financial analysts, margin debt typically moves in tandem with the overall stock market. When the market reaches all-time highs, it is expected that margin debt will also be at elevated levels. Visual representations often show a strong positive correlation between the S&P 500 and total margin debt, illustrating that growth in margin debt generally follows growth in the stock market. This relationship signifies that rising leverage is more of a reflection of market confidence and momentum rather than a standalone predictive indicator of an imminent downturn.

- Margin Debt as a Percentage of Market Cap: While absolute margin debt figures can seem alarming, examining margin debt as a percentage of the S&P 500 market capitalization offers a more nuanced perspective. This ratio tends to fluctuate, often peaking during periods of intense speculation and declining during market corrections. However, it’s not a reliable tool for calling market tops. Its movements are more a reflection of prevailing market conditions than a harbinger of future reversals.

The interplay of these data points suggests a market propelled by strong performance, but also increasingly vulnerable to shifts in sentiment or liquidity due to the sheer volume of leveraged positions.

Official Responses: Monitoring the Mounting Debt

While explicit "official responses" in the form of direct interventions or stern warnings have been somewhat muted, financial regulators and associations are actively monitoring the situation. Their primary role often involves data collection, risk assessment, and the issuance of guidance.

- Korea Financial Investment Association: The very act of collecting and publishing detailed statistics on margin loans and secured loans in South Korea by the Korea Financial Investment Association signifies an awareness and monitoring of these trends. Such transparency is crucial for market participants and regulators to gauge systemic risk. While not a direct intervention, the provision of such data allows for informed decision-making and serves as an implicit signal of vigilance.

- FINRA and SEC in the U.S.: In the United States, FINRA’s regular reporting of margin debt levels is a key mechanism for tracking investor leverage. The Securities and Exchange Commission (SEC), while not directly commenting on specific debt levels, maintains an overarching mandate to protect investors and ensure market integrity. This includes monitoring for excessive speculation or practices that could destabilize the market. Should leverage reach levels deemed systemically dangerous, regulatory bodies possess the authority to implement stricter margin requirements or issue investor advisories, though such actions are typically reserved for extreme circumstances.

- Central Banks and Financial Stability: Globally, central banks and financial stability boards are increasingly incorporating metrics like margin debt into their broader assessments of financial system health. While not directly regulating brokerage lending, they understand that a sudden unwinding of leveraged positions could have wider implications for economic stability. Their concerns are generally focused on macroprudential risks, aiming to prevent a localized market event from cascading into a broader financial crisis.

The current approach appears to be one of careful observation rather than immediate intervention. Regulators are likely weighing the benefits of robust market activity against the potential pitfalls of over-leverage, ready to act if signs of systemic distress become more pronounced.

Implications: Micro Vulnerabilities and Macro Resilience (for now)

The proliferation of leverage, while not inherently negative, carries significant implications for individual investors, specific market segments, and potentially the broader financial system.

Micro-Level Vulnerabilities: The Risk to Individuals and High-Flyers

The most immediate and discernible impact of rising leverage is on the individual investor and the performance of specific, high-flying stocks. Charlie Munger’s warning resonates most strongly at this micro level.

- Amplified Gains and Losses: Leverage acts as a double-edged sword. While it can magnify gains during a bull run, it equally amplifies losses during market corrections. For individual investors who are "maxed out" on credit or using securities as collateral, even a modest downturn in their holdings can trigger margin calls, forcing them to liquidate positions at unfavorable prices or inject additional capital. This forced selling can lead to rapid and devastating losses, potentially wiping out years of accumulated wealth in a short period.

- "Air Pockets" in Momentum Stocks: The article specifically points to highly volatile, rapidly appreciating stocks such as SK Hynix, Samsung, Taiwan Semi, Micron, and SanDisk, which have seen gains ranging from 150% to 700% in the past year alone. These "momentum names" are particularly susceptible to sharp reversals. When a significant number of investors hold these stocks on margin, any downward pressure – be it a negative news item, a slight earnings miss, or general market jitters – can trigger a cascade of margin calls. This can lead to rapid, concentrated selling pressure, creating "air pockets" where prices plummet dramatically in a very short timeframe. The 1987 Black Monday crash, while impacting the entire market, saw its severity exacerbated by the prevalence of portfolio insurance and program trading, which created a feedback loop of selling that is conceptually similar to the risks posed by widespread leveraged positions in today’s momentum stocks. While the author clarifies this isn’t a prediction for the entire market, the analogy holds for specific sectors.

- Behavioral Biases: High leverage often goes hand-in-hand with overconfidence and speculative behavior. Investors borrowing heavily in a surging market might become complacent, believing the upward trend is immutable. This can lead to poor risk management decisions, further exacerbating their vulnerability when market conditions inevitably shift. The "buy any stock and you will make money" mentality observed in Taiwan is a classic example of this speculative fervor.

Macro-Level Resilience (for now): Systemic Considerations

While the immediate risks are often localized to individuals and specific stocks, the broader implications for the overall market and economy are also a critical concern.

- Systemic Risk Mitigation: Unlike past eras (e.g., 1929), today’s financial system has more robust regulatory frameworks designed to prevent individual brokerage failures from cascading into a full-blown systemic crisis. Capital requirements for financial institutions, stress testing, and enhanced risk management protocols are intended to create a buffer against widespread defaults. This is partly why the author believes leverage is unlikely to "bring down the entire stock market" in isolation.

- Market Volatility Amplification: Even if a systemic collapse is averted, widespread leverage can significantly increase overall market volatility. A sudden, sharp correction in highly leveraged sectors could trigger a broader sell-off as nervous investors deleverage, even in less-leveraged parts of the market. This could lead to larger and more frequent market swings, making investing more challenging and potentially undermining broader economic confidence.

- Liquidity Squeeze: In an extreme scenario, if a significant number of margin calls are issued simultaneously, it could create a liquidity squeeze. Brokerages might struggle to find buyers for the vast quantities of forced-sale securities, driving prices down further and exacerbating the crisis. This feedback loop, while less likely to be systemic than in past decades, remains a risk in a highly interconnected global market.

- Impact on Economic Sentiment: Beyond direct financial impacts, a significant market correction, particularly one exacerbated by leverage, can have a chilling effect on consumer and business confidence. A sudden destruction of wealth could lead to reduced spending, investment, and hiring, potentially slowing economic growth.

In conclusion, the current environment of surging stock markets and record-breaking leverage presents a delicate balance. While the market’s upward trajectory has rewarded many, the mounting reliance on borrowed capital introduces a significant layer of risk. For individual investors, the danger of overextension is palpable, with the potential for substantial losses in the event of a market correction, particularly in the most volatile, high-momentum stocks. For the broader market, while current regulatory structures offer some protection against a full systemic meltdown, the increased leverage undoubtedly amplifies volatility and the potential for sharp, painful adjustments. As Munger wisely cautioned, understanding and respecting the power of leverage is paramount, lest its allure lead to unforeseen and severe consequences. Prudence, risk management, and a healthy dose of skepticism remain essential virtues in these exuberant times.

Further Reading:

Two Things I’m Not Worried About (Ben Carlson, 2024)