Beyond Quicken Classic: The Evolution of Personal Finance Management and the Best Alternatives for 2026

The landscape of personal finance management (PFM) is undergoing a profound transformation. For nearly four decades, Quicken was the undisputed titan of desktop budgeting, establishing a loyal user base that relied on its robust offline databases to track every penny. Today, however, legacy software faces an existential challenge. The modern consumer demands real-time synchronization, cloud accessibility, cross-platform utility, and artificial intelligence integration—features that many contemporary platforms now offer, frequently at highly competitive price points or even for free.

As subscription fatigue sets in and users seek more intuitive, automated solutions, a sophisticated cohort of financial technology platforms has emerged to fill the void left by legacy systems. This comprehensive analysis explores the shifting dynamics of the PFM market, traces the historical evolution of financial tracking software, evaluates the leading Quicken alternatives in 2026, and assesses the implications of AI and open banking on the future of wealth management.

1. Main Facts: The PFM Market Shift in 2026

The transition away from traditional desktop-bound financial software like Quicken Classic is driven by a fundamental change in how households interact with money. While Quicken Classic remains a powerful tool for niche power users who require complex, local-first bookkeeping, the broader market has pivoted toward cloud-native ecosystems.

Key Market Dynamics:

- The Rise of Specialized Ecosystems: Modern consumers are dividing into two primary camps: those seeking highly structured budgeting tools (such as zero-based budgeting) and those seeking holistic net-worth and investment-tracking dashboards.

- The Subscription Imperative: Quicken’s transition to a mandatory annual subscription model has leveled the financial playing field, prompting users to compare its recurring costs directly against modern, agile competitors.

- The Sunset of Mint: The financial technology sector experienced a massive migration event following Intuit’s decision to shut down Mint.com. This vacuum accelerated the growth of platforms like Monarch Money and Quicken Simplifi, both of which engineered seamless migration pathways for displaced users.

- The AI Frontier: Financial planning is shifting from reactive reporting (showing where money was spent) to proactive guidance (predicting cash flow bottlenecks, optimizing tax strategies, and automating debt payoff plans).

2. Chronology: The Evolution of Personal Finance Software

To understand the current state of the PFM market, it is essential to trace its evolution over the past forty years. The industry has progressed through four distinct eras, defined by technological capabilities and consumer expectations.

[1980s-1990s: Desktop Era] ──> [2000s: Web 2.0 & Mint] ──> [2010s: Specialization] ──> [2020s-2026: AI & Open Banking]

- Local database files - Cloud-based aggregators - High-net-worth dashboards - Real-time APIs (Plaid)

- Manual data entry - Ad-supported free models - Zero-based budgeting apps - Predictive cash flow/AIThe Desktop Era (1980s–1990s)

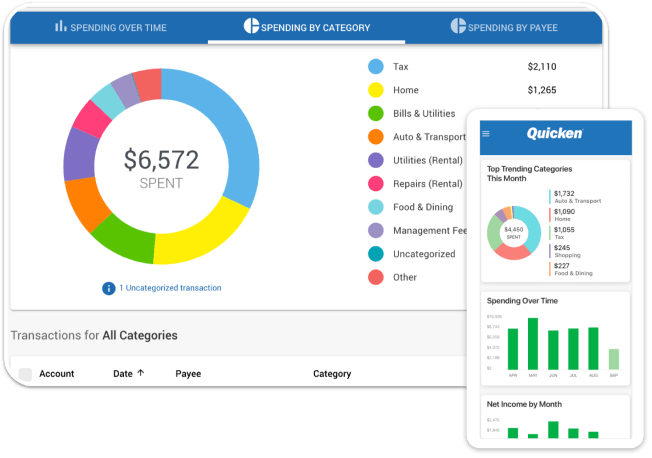

In the mid-1980s, Quicken revolutionized household finances by bringing double-entry bookkeeping concepts to the personal computer. Running on DOS and later early iterations of Windows and Macintosh operating systems, Quicken relied on local database files. Users manually entered transactions from bank statements or reconciled accounts using floppy disks. Security was high because data remained offline, but the barrier to entry was steep, requiring discipline and manual effort.

The Web 2.0 and Aggregation Era (2000s)

The launch of Mint.com in 2006 marked a paradigm shift. Utilizing screen-scraping technology, Mint allowed users to aggregate data from multiple financial institutions automatically into a single web browser interface. Intuit, recognizing the threat to Quicken, acquired Mint in 2009 for $170 million. This era established the expectation of automated transaction downloads and transaction categorization, though it relied heavily on ad-supported models and cross-selling financial products.

The Specialization and Subscription Era (2010s)

As consumers grew wary of ad-heavy interfaces and data privacy concerns, paid subscription models gained traction. You Need A Budget (YNAB) transitioned from a desktop spreadsheet-style application to a robust cloud service, championing the envelope budgeting methodology. Concurrently, Personal Capital (now Empower) emerged, targeting high-net-worth individuals by offering a free, world-class investment tracking dashboard designed to funnel qualified users toward its premium wealth management services. Quicken itself was spun off from Intuit in 2016 to H.I.G. Capital, eventually shifting its software to a subscription-based framework to secure stable recurring revenue.

The AI-Driven Open Banking Era (2020s–2026)

Following the eventual retirement of Mint, the PFM market experienced rapid fragmentation and innovation. The widespread adoption of secure open banking APIs (via aggregators like Plaid, Finicity, and MX) replaced unreliable screen scraping. Today, in 2026, the market is characterized by collaborative household tools, advanced investment tracking, and artificial intelligence capable of building personalized financial roadmaps.

3. Supporting Data: Comparative Analysis of the Top Quicken Alternatives

When evaluating a replacement for Quicken, consumers must balance cost, platform compatibility, and feature depth. The following analysis details the top eight financial platforms leading the market in 2026.

Comparative Overview of Leading PFM Platforms

| Platform | Target Audience | Primary Focus | Cost Structure | Platform Availability | Key Feature |

|---|---|---|---|---|---|

| Monarch Money | Couples & Modern Budgeters | Collaborative Budgeting & Wealth Tracking | $8.33/mo (billed annually) | iOS, Android, Web | Flex Budgets & Multi-User Collaboration |

| Quicken Simplifi | Mobile-First Spenders | Active Cash Flow & Bill Tracking | $6.99/mo (billed annually) | iOS, Android, Web | Visual Spending Plans & Bill Calendars |

| Empower | Investors & High Net Worth | Portfolio Analysis & Net Worth | Free | iOS, Android, Web | Retirement Planner & Fee Analyzer |

| Origin | Holistic Financial Planners | Unified Wealth & AI Advice | $12.99/mo or $99/yr | iOS, Android, Web | AI Financial Assistant & Built-in Tax Prep |

| Rocket Money | Subscription Managers | Expense Reduction & Bill Neg. | Free tier; Premium $7–$14/mo | iOS, Android, Web | Active Subscription Cancellation Services |

| YNAB | Disciplined Budgeters | Zero-Based Envelope Budgeting | $14.99/mo or $109/yr | iOS, Android, Web | "Give Every Dollar a Job" Methodology |

| PocketSmith | Forward-Looking Planners | Cash Flow Forecasting | Free tier; Premium from $7.50/mo | iOS, Android, Web | Calendar-Based Financial Forecasting |

| CountAbout | Legacy Migrators | Seamless Data Importation | $9.99/yr (Basic) to $39.99/yr | iOS, Android, Web | Quicken/Mint QIF & CSV Data Importing |

In-Depth Platform Evaluations

1. Monarch Money: Best Overall for Collaborative Budgeting

Monarch Money has established itself as a premier alternative to Quicken, particularly for households and couples who manage finances jointly. Developed by personal finance veterans, the platform features an intuitive, ad-free dashboard designed to eliminate the friction of modern wealth tracking.

- App Store Rating: 4.9 (approx. 88,000 reviews)

- Android Rating: 4.8 (approx. 21,200 reviews)

- Pricing & Offers: $8.33 per month when billed annually. A 7-day free trial is standard, and users can leverage promotional codes (such as ROB50) to secure a 50% discount on the first year of the Core Plan.

- Key Strengths: Monarch’s standout innovation is its "Flex Budgeting" system, which accommodates fluctuating, non-monthly expenses without breaking the user’s broader financial plan. Its dual-login capability allows couples to connect separate and joint accounts under a unified dashboard, fostering shared financial accountability.

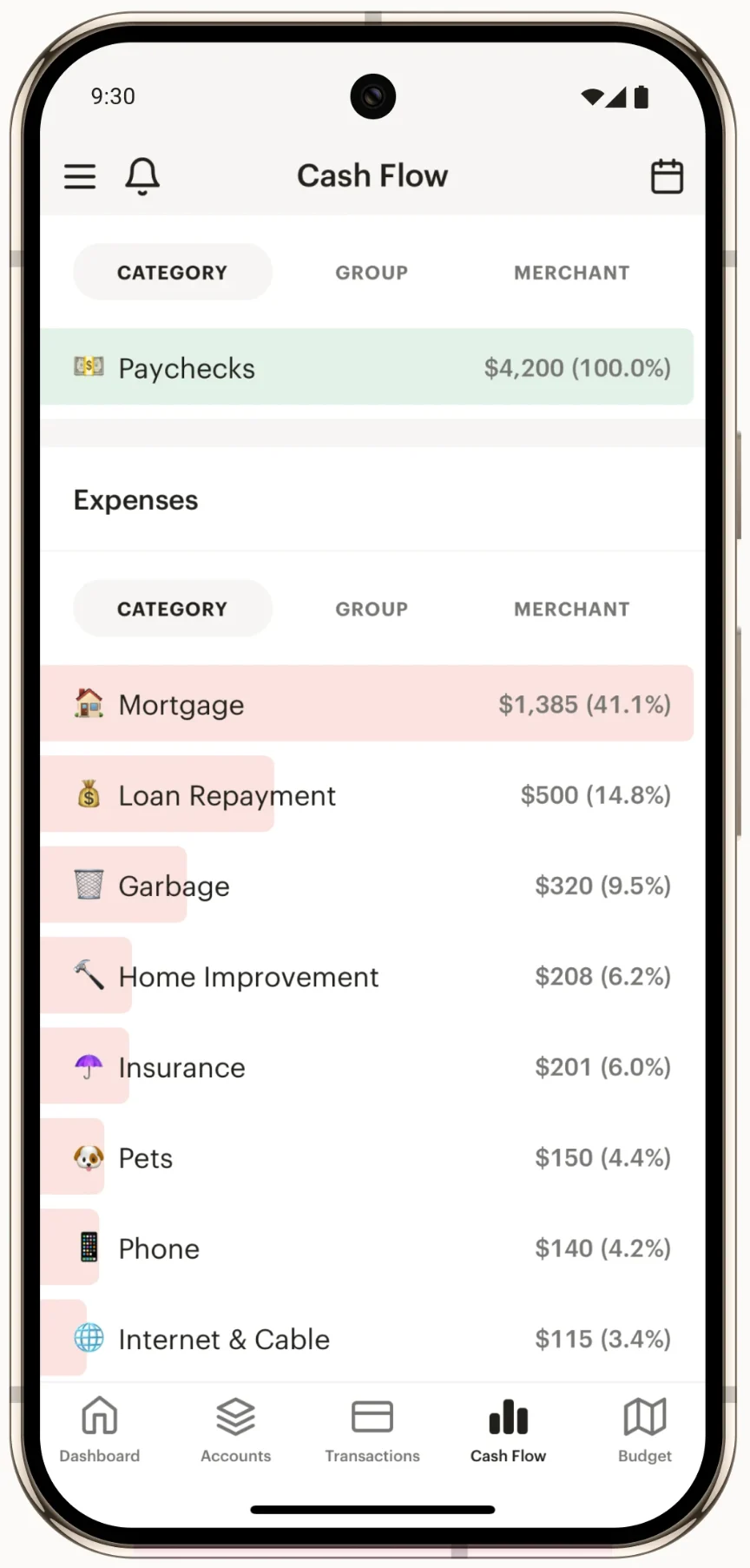

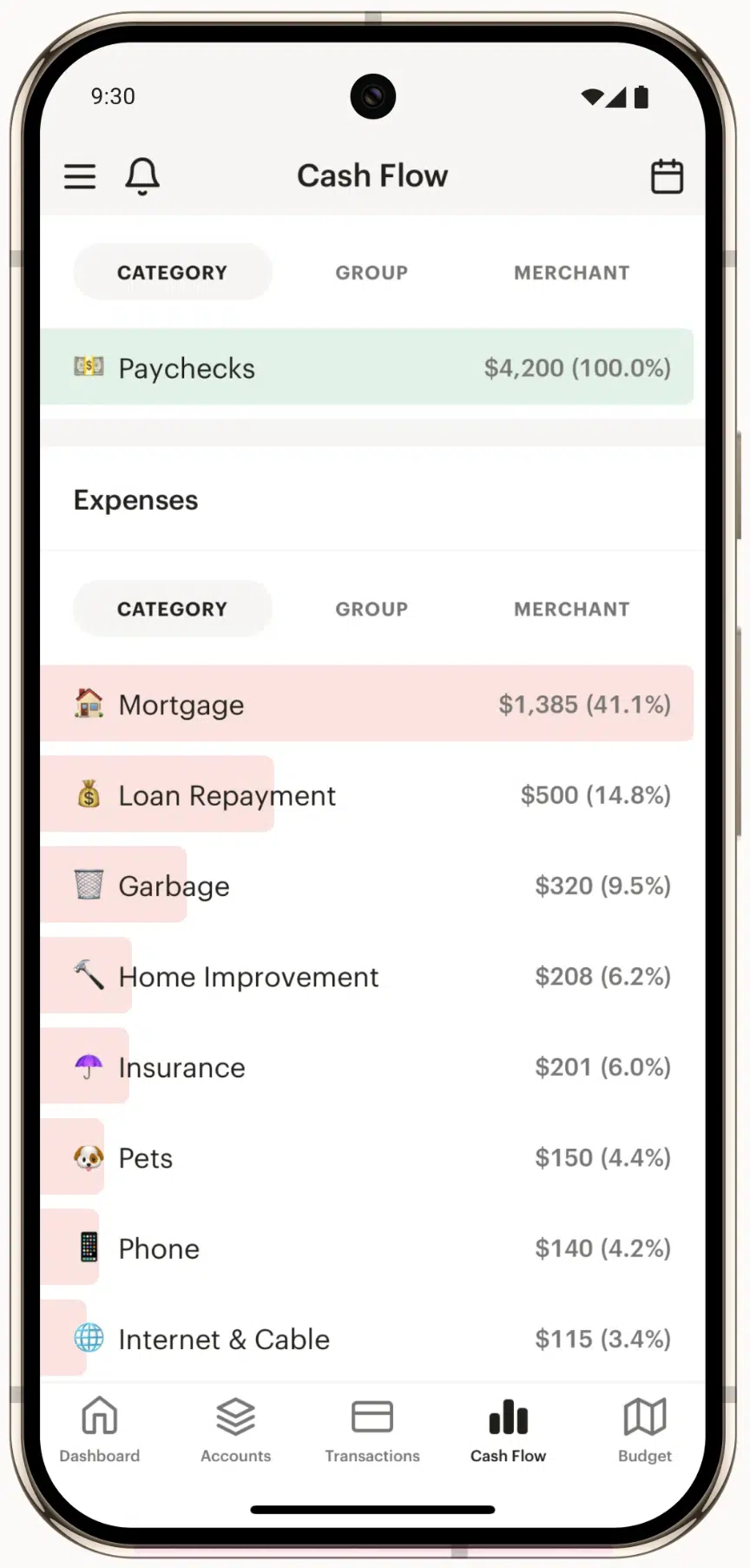

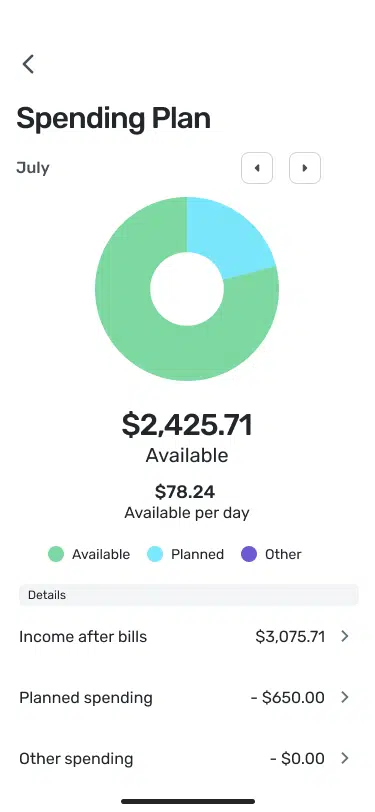

2. Quicken Simplifi: Best for Streamlined Spending Plans

As Quicken’s cloud-native, mobile-first offering, Simplifi was designed from the ground up to counter the clunkiness of legacy desktop software. It represents a strategic pivot by Quicken to retain users who prefer lightweight, proactive tracking over deep ledger management.

- App Store Rating: 4.5 (approx. 9,500 reviews)

- Android Rating: 4.1 (approx. 4,220 reviews)

- Pricing & Offers: Regularly $6.99 per month, Simplifi frequently runs promotional campaigns offering a 50% discount for the first year (reducing the cost to $3.49 per month), backed by a 30-day money-back guarantee.

- Key Strengths: Simplifi utilizes a "Spending Plan" methodology rather than rigid traditional budgets. It calculates available discretionary income in real-time after accounting for bills, savings goals, and pending transactions. Recent updates have integrated robust investment tracking, making it a highly balanced option for middle-market consumers.

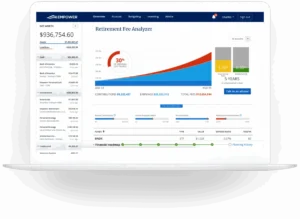

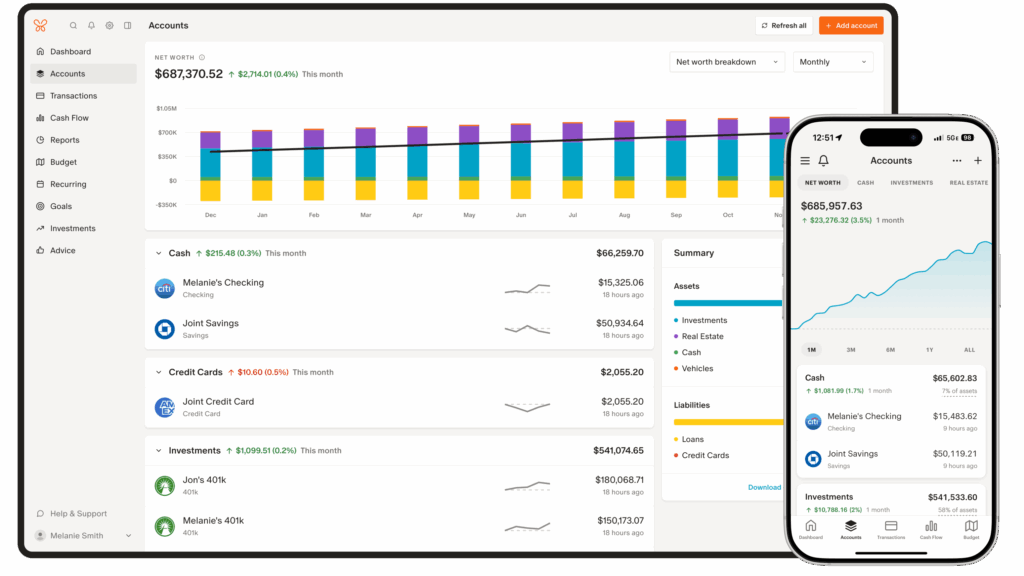

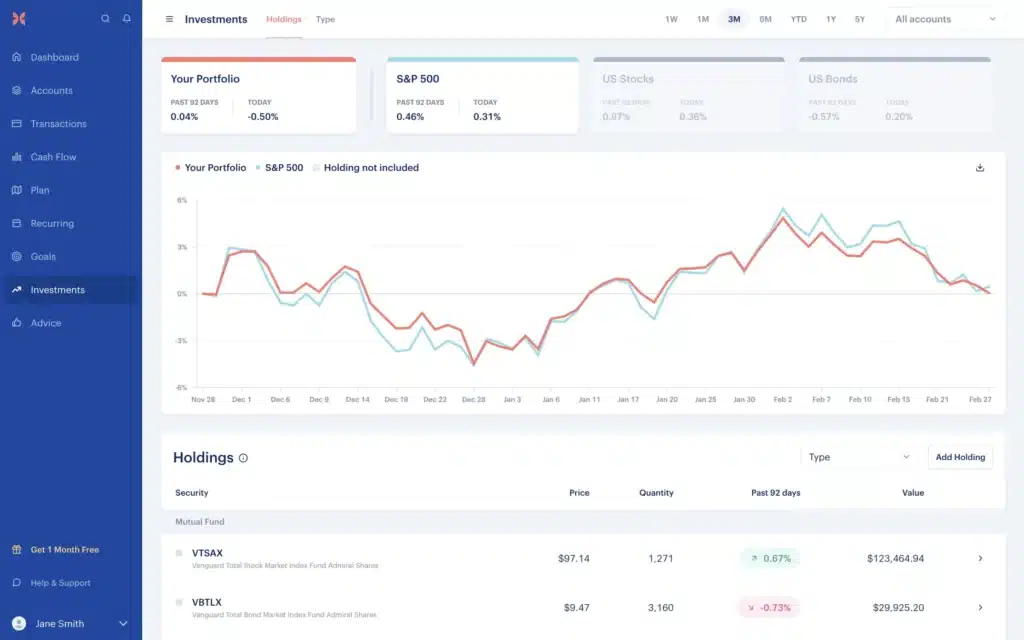

3. Empower: Best Free Alternative for Investment and Net Worth Tracking

Formerly known as Personal Capital, the Empower Personal Dashboard remains the gold standard for tracking investments, retirement trajectories, and overall net worth without monthly software fees.

- App Store Rating: 4.8 (approx. 378,000 reviews)

- Pricing: Free.

- Key Strengths: Empower excels in portfolio diagnostics. Its Investment Checkup tool evaluates asset allocation, while the Fee Analyzer exposes hidden costs in mutual funds and 401(k) plans. The Retirement Planner runs Monte Carlo simulations to project the probability of retirement success. Because it is free, it serves as an excellent companion tool alongside dedicated budgeting apps.

Empower Dashboard Core Capabilities:

├── Net Worth Tracking (Real-time asset & liability syncing)

├── Portfolio Diagnostic Engine (Fee Analyzer & Asset Allocation check)

└── Retirement Planning Simulator (Monte Carlo predictive modeling)4. Origin: Best AI-Powered Financial Suite

Origin is designed as a comprehensive, modern financial ecosystem. Unlike apps that focus solely on transaction categorization, Origin integrates budgeting, equity tracking, tax filing, estate planning, and wealth management into a single subscription.

- Pricing & Offers: Offers a 7-day free trial, with entry-level promotional tiers starting as low as $1 for the first year, before transitioning to $12.99 per month or $99 annually.

- Key Strengths: Origin utilizes artificial intelligence to build personalized debt-paydown schedules and cash reserves. It features built-in tax preparation software and basic estate planning (wills) at no additional charge. Furthermore, Origin provides a competitive cash management account, yielding 4.52% APY (as of late 2025/2026), alongside automated robo-advisory services.

5. Rocket Money: Best for Subscription Management and Bill Negotiation

Rocket Money (formerly Truebill) focuses on identifying and eliminating financial waste, making it highly effective for users seeking immediate cash flow optimization.

- Pricing: A robust free tier is available. Premium features utilize a sliding scale payment model ranging from $7 to $14 per month.

- Key Strengths: The platform excels at identifying recurring subscription fees, offering an in-app service to cancel unwanted subscriptions on the user’s behalf. Additionally, Rocket Money employs professional negotiation agents who actively contact telecom and utility providers to lower users’ monthly bills.

6. You Need A Budget (YNAB): Best for Zero-Based Budgeting

YNAB is built around a strict, zero-based envelope budgeting philosophy. It requires users to allocate every dollar of income to a specific category, ensuring that all spending is intentional.

- Pricing: $14.99 per month or $109 per year, following a 34-day free trial.

- Key Strengths: YNAB’s "Four Rules" help users break the paycheck-to-paycheck cycle and build a financial buffer. It is highly effective for debt reduction and savings discipline. However, it lacks robust investment analysis tools, making it less suitable for wealth managers seeking a direct replacement for Quicken Premier.

7. PocketSmith: Best for Long-Term Cash Flow Forecasting

PocketSmith stands out for its visual, calendar-centric approach to cash flow projection, allowing users to map out their financial health up to 30 years into the future.

- Pricing: Free manual plan; Premium plans with automatic bank feeds start at $7.50 per month when billed annually.

- Key Strengths: PocketSmith translates budgets into a calendar interface, showing how today’s spending decisions affect bank balances months or years down the line. It is highly favored by visual planners and freelancers with irregular income streams.

8. CountAbout: Best for Importing Legacy Quicken Files

CountAbout is a minimalist, web-based budgeting tool focused on security, simplicity, and seamless transition pathways for legacy desktop users.

- Pricing: Basic plan costs $9.99 per year; Premium plan with automated banking downloads costs $39.99 per year.

- Key Strengths: For users with decades of financial history stored in Quicken or Mint, CountAbout offers one of the most reliable importing engines. It preserves historical category structures and tags, ensuring a smooth transition without data loss.

4. Official Responses: Strategic Corporate Positions

The competitive dynamics of the 2026 PFM market are reflected in how these platforms position themselves to consumers.

The Quicken Defense: Preserving Power Features While Innovating

In response to market fragmentation, Quicken’s corporate strategy is bifurcated:

- Quicken Classic (available via subscription for Windows and macOS) remains positioned as the ultimate tool for power users, small business owners, and real estate investors who require offline data storage, advanced tax reporting (Schedule C/E), and manual control.

- Quicken Simplifi is marketed to a younger, mobile-first demographic. Quicken positions Simplifi as an intuitive spending companion that reduces the anxiety of budgeting by focusing on what is safe to spend, rather than historical post-mortems.

Monarch Money’s Privacy-First Position

Monarch Money has built its brand on user trust, positioning itself as a consumer-aligned alternative to ad-supported models. Co-founded by Val Agostino, an early product leader at Mint, Monarch positions its subscription fee as a guarantee of data privacy. The company frequently highlights that it does not sell user data or cross-sell financial products, aligning its financial incentives directly with its users.

Empower’s Loss-Leader Strategy

Empower continues to utilize its personal financial dashboard as a highly effective customer acquisition tool. By providing a free, enterprise-grade investment tracking suite, Empower establishes trust with users. This allows them to selectively pitch their paid, fiduciary wealth management services to individuals with investable assets exceeding $100,000.

5. Implications: The Future of Personal Finance Management

The ongoing evolution of the PFM market carries significant implications for consumers, financial institutions, and the broader fintech ecosystem.

Future Trends in PFM Technology:

├── Open Banking Standards (Enhanced security & reliable API syncing)

├── AI-Driven Proactive Planning (Predictive cash flow & automated wealth advice)

└── Consolidation of Wealth Tech (All-in-one financial dashboards)The Regulatory Impact of Open Banking

In the United States, the Consumer Financial Protection Bureau (CFPB) has pushed to finalize rules under Section 1033 of the Dodd-Frank Act. These regulations mandate that financial institutions provide consumers with secure, permissioned access to their financial data via standardized APIs, effectively ending the era of unstable credential-based screen scraping. This shift ensures that syncing issues—long a primary complaint of PFM users—will decline, allowing fintech platforms to offer faster, more secure connections.

From Reactive Budgeting to Autonomous Finance

The integration of generative AI is shifting PFM software from a passive record of historical transactions to an active, autonomous financial assistant. Platforms are moving toward "self-driving money" systems. In these environments, AI algorithms can automatically route excess cash to high-yield savings accounts, allocate funds to optimize investment portfolios, or dynamically adjust debt-paydown strategies based on daily spending patterns.

The True Cost of "Free" Financial Tools

The decline of ad-supported platforms like Mint underscores a growing consumer realization: when a service is free, the user’s data is often the product. As a result, the market is stabilizing around premium, subscription-based models. Consumers are increasingly willing to pay $40 to $120 annually for ad-free financial tools that protect their privacy and offer reliable performance.

Ultimately, the decline of Quicken’s monopoly has fostered a highly competitive, innovative ecosystem. Whether prioritizing granular investment analysis, collaborative household budgeting, or automated expense management, consumers in 2026 have access to a sophisticated suite of financial platforms tailored to their unique wealth-building journeys.