The Desktop Era Yields to the Cloud: Analysing the Best Quicken Alternatives for Personal Wealth Management

For over four decades, Quicken was the undisputed titan of personal finance. Launched in the mid-1980s, the software revolutionized how households tracked their income, categorized expenses, and managed investments. However, the rise of cloud computing, open banking APIs, and artificial intelligence has fundamentally altered the personal financial management (PFM) landscape.

Today, legacy desktop software has been largely eclipsed by agile, cloud-native applications that offer real-time synchronization, advanced automation, and collaborative features. As consumers seek modern solutions to manage their net worth, a diverse ecosystem of platforms has emerged to challenge Quicken’s historical dominance. This analysis evaluates the primary shifts in the PFM market and details the leading alternatives available to consumers.

Main Facts: The Evolution of Personal Financial Management

The modern personal finance sector is defined by a shift away from manual ledger entry toward automated data aggregation. While Quicken—now rebranded as Quicken Classic—remains functional, its transition to a mandatory annual subscription model has alienated legacy users who prefer one-time purchase software. Simultaneously, the shuttering of popular free tools like Intuit Mint has triggered a massive migration of consumers seeking alternative platforms.

Today’s financial technology (fintech) consumers demand:

- Multi-Platform Access: Seamless transition between web browsers, tablets, and smartphone applications.

- Automated Syncing: Secure, instantaneous connections to banks, credit card issuers, brokerages, and loan servicers via aggregators like Plaid and Finicity.

- Collaborative Tools: Shared dashboards for couples and families to manage joint finances without sharing login credentials.

- Holistic Wealth Tracking: Unified dashboards that display cash flow, budgeting metrics, investment portfolios, and net worth calculations side-by-side.

Chronology: From Floppy Disks to Generative AI

To understand the current state of the market, it is essential to trace the historical trajectory of personal finance software:

[1983] Quicken Launches (DOS/Apple II) -> Manual entry, desktop-bound

│

[1990s-2000s] Desktop Domination -> Quicken and Microsoft Money rule the market

│

[2007] Mint.com Launches -> Introduction of free, ad-supported, web-based aggregation

│

[2009] Intuit Acquires Mint -> Consolidation of desktop and early web tools

│

[2010s] Mobile & Wealth Shift -> Personal Capital (now Empower) focuses on high-net-worth tracking

│

[2020s] SaaS and AI Revolution -> Mint shuts down; platforms pivot to subscription models and AI assistance- 1983–1999: The Desktop Era. Quicken was introduced by Intuit on DOS and Apple II platforms. Users manually entered transactions from paper bank statements. The software served as a digital checkbook register.

- 2000–2009: The Web 1.0 Transition. The launch of Mint.com in 2007 disrupted the market by offering free, automated bank account aggregation via early screen-scraping technologies. Intuit acquired Mint in 2009 to protect its market share.

- 2010–2019: The Mobile and Wealth Shift. Smartphones became the primary access point for financial services. Personal Capital (founded in 2009 and later acquired by Empower) introduced sophisticated investment-tracking tools to the mass market for free, leveraging a wealth-management advisory business model.

- 2020–2026: The AI and SaaS Consolidation. The PFM industry experienced massive consolidation. Intuit shuttered Mint, pushing millions of users to find new platforms. Subscription fatigue led to the rise of premium, ad-free platforms like Monarch Money, while AI-powered financial assistants like Origin began automating budget creation and tax preparation.

Supporting Data: Detailed Evaluations of the Top Alternatives

To assist consumers in navigating the crowded PFM landscape, financial analysts and software testers have identified eight standout alternatives to Quicken Classic. Each platform targets a specific user demographic, ranging from zero-based budgeting purists to high-net-worth investors.

1. Monarch Money: Best Overall for Budgeting and Collaboration

Monarch Money has emerged as one of the most highly rated modern budgeting tools on the market. Developed by a team of product designers and fintech veterans, it focuses heavily on user experience, data privacy, and household collaboration.

- App Store Rating: 4.9/5 (approx. 88,000 reviews)

- Android Rating: 4.8/5 (approx. 21,200 reviews)

- Pricing: $8.33 per month (billed annually at $99.99), with promotional discounts (e.g., 50% off the first year with code

ROB50) and a 7-day free trial. - Target Audience: Couples, modern budgeters, and former Mint users who prefer an ad-free, premium experience.

Key Features & Analysis

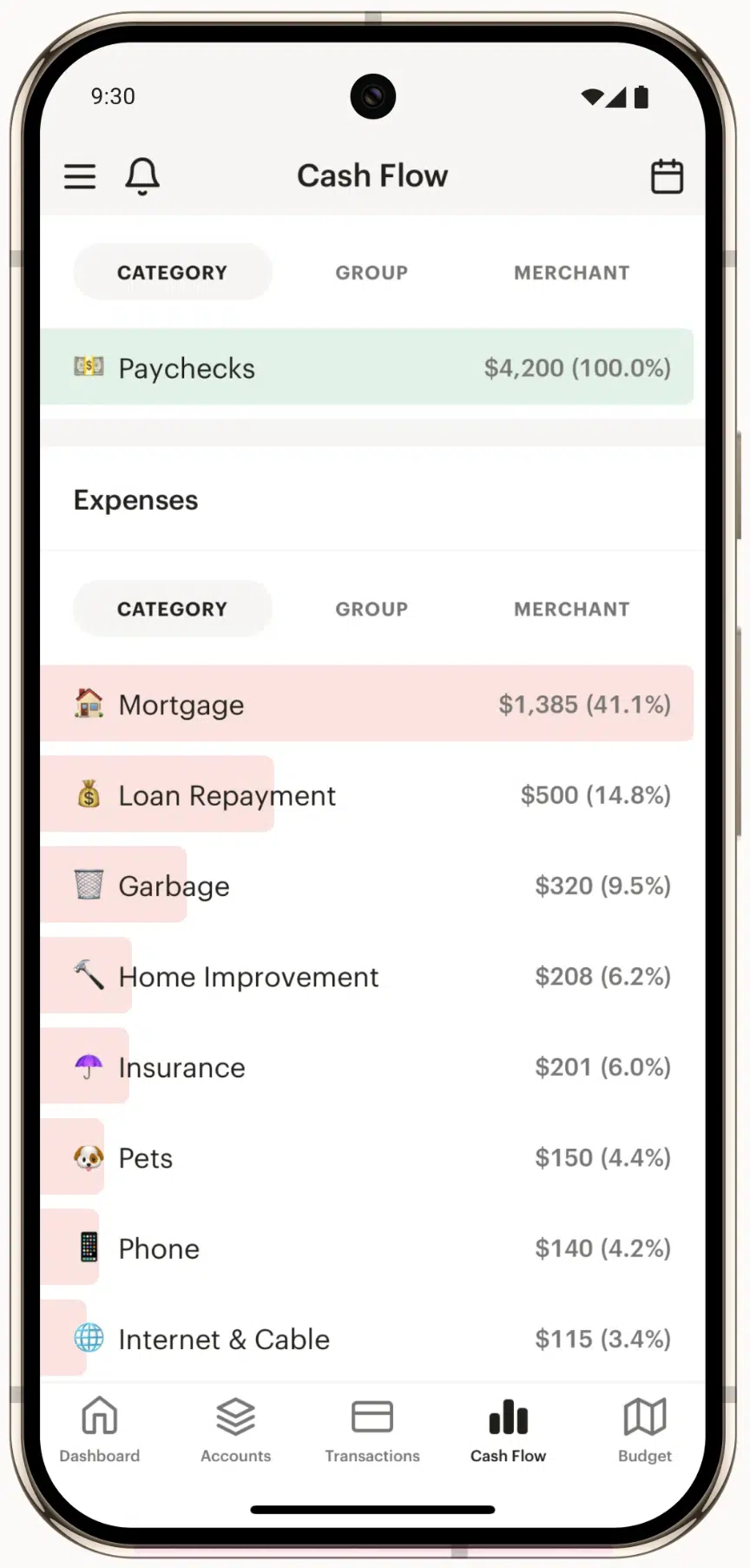

Monarch excels at account synchronization, utilizing multiple data networks to maintain stable connections with financial institutions. It features customizable transaction rules, tracking of recurring subscriptions, and a "Flex Budgeting" system designed to accommodate fluctuating monthly expenses.

For couples, Monarch offers joint accounts with separate login credentials, allowing both partners to view a unified financial picture without compromising individual account security.

2. Quicken Simplifi: Best for Balanced Budgeting and Bill Tracking

For users who want to transition away from Quicken Classic but prefer to stay within the Quicken brand ecosystem, Quicken Simplifi offers a streamlined, mobile-first web application.

- App Store Rating: 4.5/5 (approx. 9,500 reviews)

- Android Rating: 4.1/5 (approx. 4,220 reviews)

- Pricing: $6.99 per month (billed annually), with introductory pricing often available at $3.49 per month, backed by a 30-day money-back guarantee.

- Target Audience: Mobile-first users seeking an affordable, automated spending tracker.

Key Features & Analysis

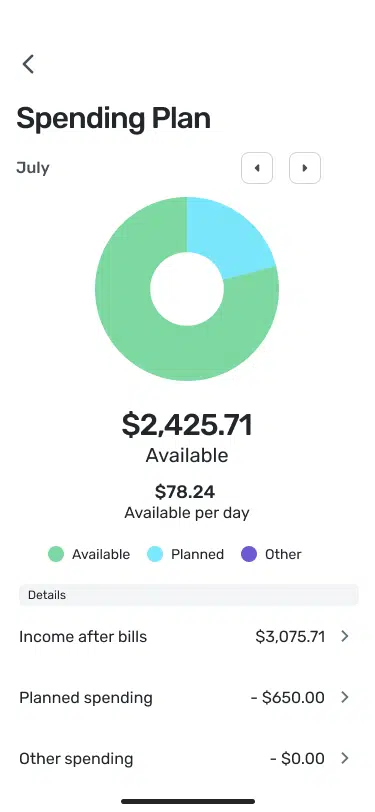

Rather than traditional spreadsheet-style budgeting, Simplifi utilizes a "Spending Plan" model. This approach calculates how much discretionary income remains after accounting for bills, savings goals, and already-committed spending.

Simplifi has recently expanded its investment tracking capabilities, making it a closer feature-match to Quicken Classic, though migrating data requires exporting to a CSV file and manually formatting it to match Simplifi’s schema.

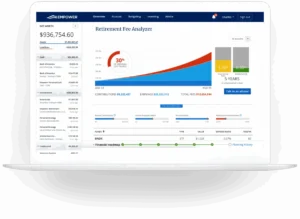

3. Empower Personal Dashboard: Best Free Alternative for Investors

Formerly known as Personal Capital, the Empower Personal Dashboard is a robust financial tracking tool that focuses heavily on asset allocation, investment fees, and retirement planning.

- App Store Rating: 4.8/5 (approx. 378,000 reviews)

- Pricing: Free.

- Target Audience: High-net-worth individuals, active investors, and those planning for retirement.

Key Features & Analysis

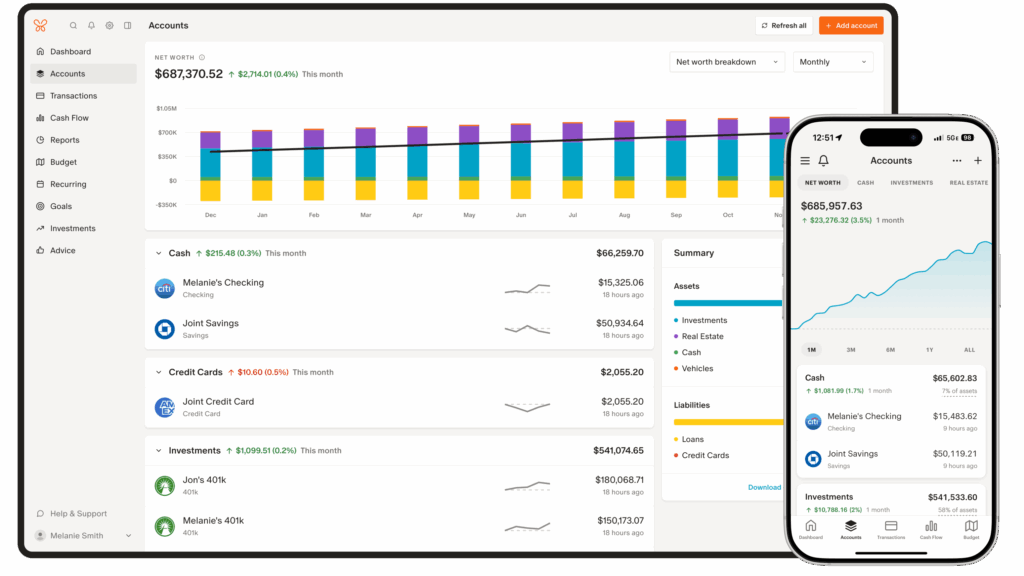

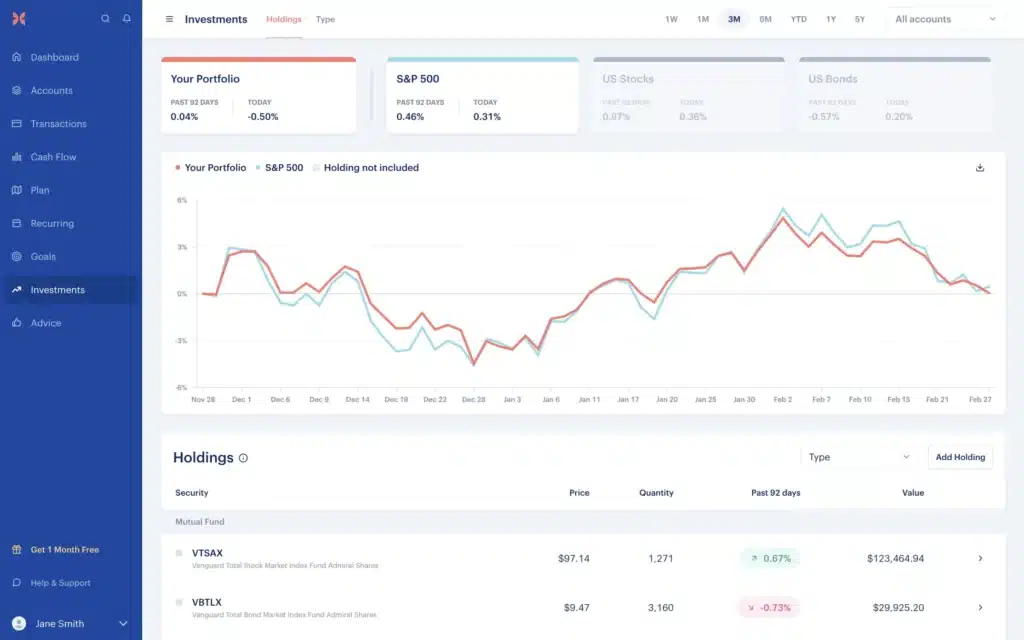

Empower tracks cash flow and basic expenses, but its budgeting capabilities are secondary to its investment features. The dashboard provides a comprehensive view of net worth by linking brokerage accounts, retirement accounts, mortgages, and real estate valuations (via integration with Zillow).

Its standout features include the Retirement Planner, which runs Monte Carlo simulations to project portfolio longevity, and the Fee Analyzer, which exposes hidden mutual fund and 401(k) fees. Empower remains free because it serves as a lead-generation tool for the company’s paid wealth management services.

4. Origin: Best for AI-Powered Financial Planning

Origin represents the cutting edge of AI-driven financial technology, aiming to serve as a comprehensive platform for budgeting, investing, tax filing, and estate planning.

- Pricing: $12.99 per month or $99 per year (with introductory promotions as low as $1 for the first year).

- Target Audience: Tech-forward users seeking automated, all-in-one financial guidance.

Key Features & Analysis

Origin integrates artificial intelligence directly into the user experience. The platform can automatically draft budgets based on historical transaction data and construct personalized debt-paydown or emergency-savings plans.

Uniquely, Origin includes tax preparation and filing services at no additional cost, alongside basic estate planning tools (including simple wills). It also features a built-in robo-advisor and a high-yield savings account (paying competitive rates, such as 4.52% APY in late 2025).

5. Rocket Money: Best for Subscription Management and Bill Negotiation

Rocket Money (formerly Truebill) is designed to optimize cash flow by identifying and eliminating unnecessary expenses.

- App Store Rating: 4.8/5 (approx. 350,000 reviews)

- Pricing: Free basic tier; premium services operate on a pay-what-you-want scale from $7 to $14 per month.

- Target Audience: Individuals looking to cut waste from their monthly expenses.

Key Features & Analysis

Rocket Money excels at parsing transaction history to identify recurring subscriptions, offering a dashboard that allows users to cancel unwanted services with a few clicks.

Additionally, the platform offers a bill negotiation service (where Rocket Money takes a percentage of the annual savings achieved on utilities or telecom bills) and provides real-time credit score monitoring.

6. You Need a Budget (YNAB): Best for Disciplined Zero-Based Budgeting

YNAB is a cult-favorite platform built on the philosophy of zero-based budgeting, where every single dollar of income is assigned a specific job.

- Pricing: $14.99 per month or $109 per year, with a 34-day free trial.

- Target Audience: Users seeking to break the paycheck-to-paycheck cycle and actively control their spending behavior.

Key Features & Analysis

YNAB does not encourage passive tracking; instead, it demands active participation. Users allocate their actual, available cash into customizable categories.

While YNAB supports automatic bank syncing, it lacks robust investment tracking and net-worth analysis tools. It remains one of the more expensive options on the market, but its adherents argue that the behavioral shift it inspires easily covers the subscription cost.

7. PocketSmith: Best for Calendar-Based Cash Flow Forecasting

PocketSmith is a highly customizable tool that approaches personal finance from a chronological perspective, mapping future income and expenses onto a calendar interface.

- Pricing: Free manual tier; paid tiers range from $7.50 to $26.66 per month (billed annually).

- Target Audience: Visual planners and individuals with complex, irregular income streams.

Key Features & Analysis

PocketSmith’s core differentiator is its projection engine, which can forecast a user’s bank balances up to 30 years into the future based on recurring transaction patterns. It features automatic categorization and net worth tracking, making it highly effective for scenario planning (e.g., simulating the financial impact of buying a home or changing careers).

8. CountAbout: Best for Importing Legacy Quicken and Mint Data

CountAbout is a minimalist, web-first budgeting tool designed specifically for users who refuse to lose decades of financial history when migrating away from legacy platforms.

- Pricing: $9.99 per year (basic manual entry) or $39.99 per year (with automatic bank downloads).

- Target Audience: Former Quicken and Mint power users who prioritize data preservation and simple, reliable budgeting.

Key Features & Analysis

CountAbout is one of the few platforms that offers direct, seamless data imports from Quicken and Mint. The interface is clean, ad-free, and highly responsive. It supports invoice creation for small business owners and allows users to attach digital receipt images directly to individual transactions.

Comprehensive Platform Comparison

| Platform | Core Strength | Price | Free Trial / Guarantee | Data Migration Ease |

|---|---|---|---|---|

| Monarch Money | Budgeting & Collaboration | $8.33/mo (billed annually) | 7-day free trial | High (Mint/Quicken import tools) |

| Quicken Simplifi | Spending Plans & Bills | $6.99/mo (annual billing available) | 30-day money-back | Moderate (Requires CSV formatting) |

| Empower | Investment & Net Worth | Free | N/A (Always free) | Low (Focuses on live syncing) |

| Origin | AI Financial Planning & Taxes | $12.99/mo or $99/yr | 7-day free trial | Moderate |

| Rocket Money | Expense Control & Bills | Free to $14/mo | 7-day trial (Premium) | Low |

| YNAB | Zero-Based Budgeting | $14.99/mo or $109/yr | 34-day free trial | Low |

| PocketSmith | Calendar Projections | $7.50 to $26.66/mo | Free tier available | Moderate |

| CountAbout | Legacy Data Preservation | $9.99 to $39.99/yr | 45-day free trial | Very High (Direct Mint/Quicken import) |

Official Responses and Market Positioning

The shift away from desktop software has forced Quicken to pivot its corporate strategy. Recognizing that desktop-only platforms are unsustainable in a mobile-first world, Quicken launched Simplifi to capture younger demographics.

However, Quicken’s decision to transition its legacy product, Quicken Classic, to a subscription-only model was met with consumer backlash, creating a market vacuum that independent developers were eager to fill.

[Legacy Market]

│ (Mandatory Subscription Shift)

▼

┌───────────────────────┐

│ Quicken Classic │

└───────────┬───────────┘

│ (User Exodus)

▼

┌─────────────────────────────────┐

│ Emergent Competitors │

└───────┬─────────────────┬───────┘

│ │

▼ ▼

[Ad-Free Premium] [Free Asset-Led]

(Monarch, YNAB) (Empower Dashboard)In contrast, modern subscription platforms like Monarch Money and YNAB have positioned themselves as premium, privacy-focused services. By charging a subscription fee, they explicitly pledge never to sell user financial data to third-party advertisers—a common practice among older, free tools like Mint.

Meanwhile, enterprise-backed platforms like Empower use their free dashboards as a funnel to convert high-net-worth users into paying advisory clients, highlighting the diverse monetization strategies active in the 2026 PFM market.

Implications: The Future of Personal Wealth Tech

The transition from desktop-bound programs to dynamic financial applications has profound implications for consumers:

- The Rise of Autonomous Finance: With platforms like Origin integrating sophisticated artificial intelligence, the industry is moving toward "self-driving money." AI models can now analyze spending patterns, automatically transfer excess cash into high-yield savings accounts, reallocate investment portfolios, and predict cash flow shortages before they occur.

- Open Banking and Security Standards: The reliance on credential-sharing (screen scraping) is rapidly being replaced by secure open banking frameworks (OAuth). This transition, supported by federal regulatory pushes, ensures that applications can access transaction data without requiring users to share their banking passwords.

- Subscription Consolidation: As single-purpose apps proliferate, consumers face subscription fatigue. The most successful platforms in the coming years will likely be those that consolidate multiple financial services—such as budgeting, tax filing, estate planning, and credit monitoring—into a single subscription price.

Ultimately, the decline of Quicken’s hegemony has fostered a highly competitive, innovative market. Whether users prioritize strict budgeting, passive investment tracking, or automated wealth optimization, the modern fintech ecosystem offers highly specialized tools designed to help consumers achieve financial autonomy.