The Paradoxical Landscape: Trillion-Dollar Funds, Retail Frenzy, and a Shifting American Wealth Divide

FOR IMMEDIATE RELEASE

New York, NY – June 12, 2026 – The financial world is currently navigating a fascinating and often contradictory landscape, marked by monumental shifts in investment strategies, investor demographics, and national wealth distribution. A recent milestone, the Vanguard S&P 500 ETF (VOO) surpassing an unprecedented $1 trillion in assets, encapsulates the powerful surge of passive investing. Yet, this era of methodical, low-cost index fund accumulation coexists with a dramatic increase in speculative retail trading and a complex redefinition of America’s middle class – a narrative where progress and widening inequality unfold simultaneously.

Authored by Ben Carlson and initially highlighted by Bloomberg, the VOO’s achievement signals a pivotal moment for the exchange-traded fund industry. This record-breaking figure is not an isolated incident but rather a symptom of deeper, intertwined trends that are reshaping capital markets and challenging conventional economic wisdom.

The Rise of the Trillion-Dollar Titans: A Passive Revolution

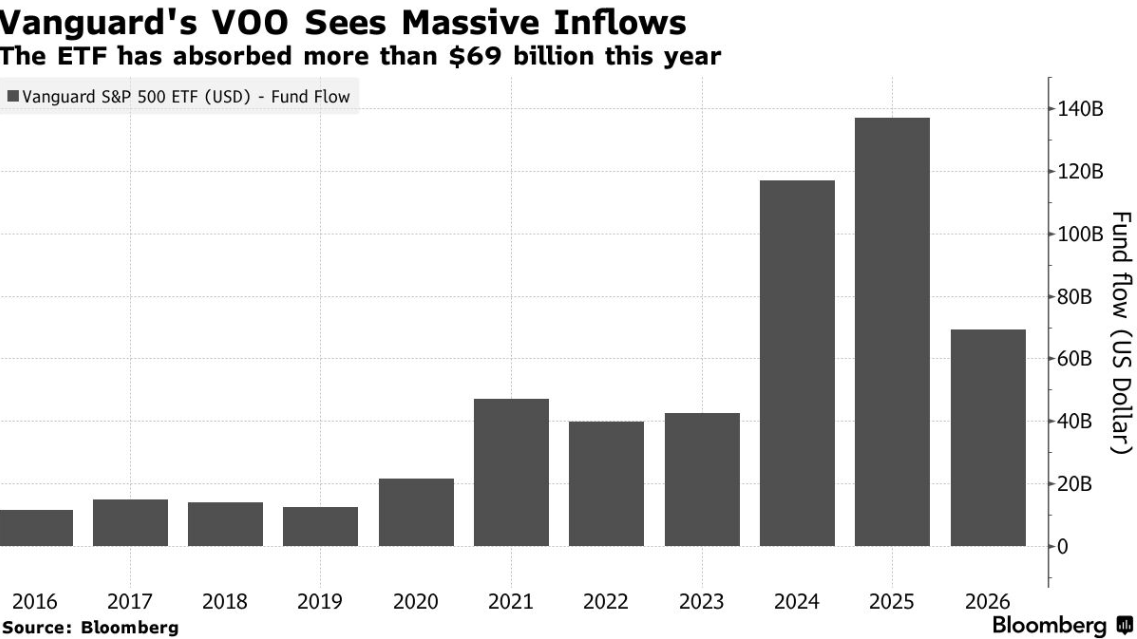

The financial community was abuzz last week with the news, initially reported by Bloomberg, that the Vanguard S&P 500 ETF (VOO) has become the first ETF in history to amass $1 trillion in assets under management. This remarkable achievement underscores the relentless and accelerating march of passive investing, a strategy that prioritizes tracking market indices over attempting to outperform them. The fund’s asset flows have been nothing short of monumental, demonstrating a sustained investor appetite that shows no signs of abating.

VOO’s ascent is not unique in its scale, though its trillion-dollar valuation sets a new benchmark. Its counterparts, such as the SPDR S&P 500 ETF Trust (SPY) and the iShares Core S&P 500 ETF (IVV), are also titans in their own right, each commanding over $800 billion. Even broader market index funds, like the Vanguard Total Stock Market ETF (VTI), which mirrors the entire U.S. stock market rather than just the S&P 500, has swelled to over $660 billion. These figures collectively illustrate an undeniable truth: an enormous and ever-increasing amount of capital is being channeled into index-tracking ETFs.

The Inexorable Shift from Active to Passive Management

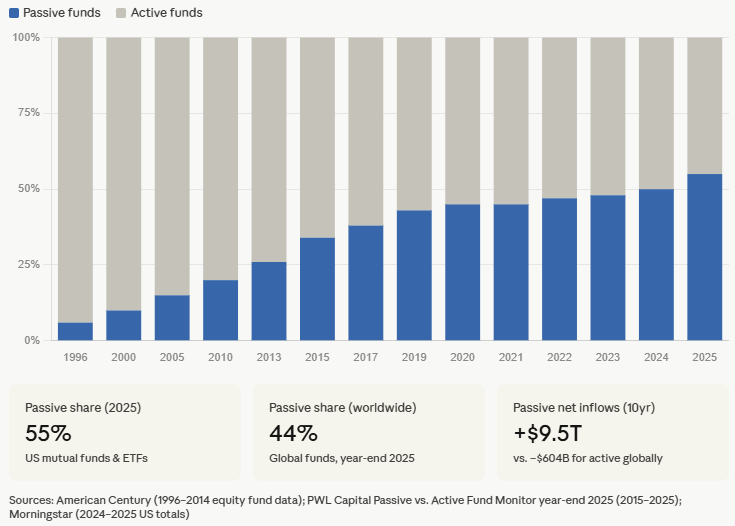

This phenomenon represents a seismic shift within the fund industry, where passive management is steadily eclipsing its active counterpart. Data vividly illustrates this trend, showing passive funds consistently "swallowing active share." While the exact tipping point remains a subject of debate, industry observers widely anticipate that passive funds could eventually account for 70% to 80% of assets within the fund industry. This transition is driven by several compelling factors: the consistent underperformance of a majority of active managers against their benchmarks, the significantly lower fees associated with passive funds, and the inherent simplicity and transparency of index investing. Investors, both institutional and individual, have increasingly recognized the long-term benefits of broad market exposure at minimal cost.

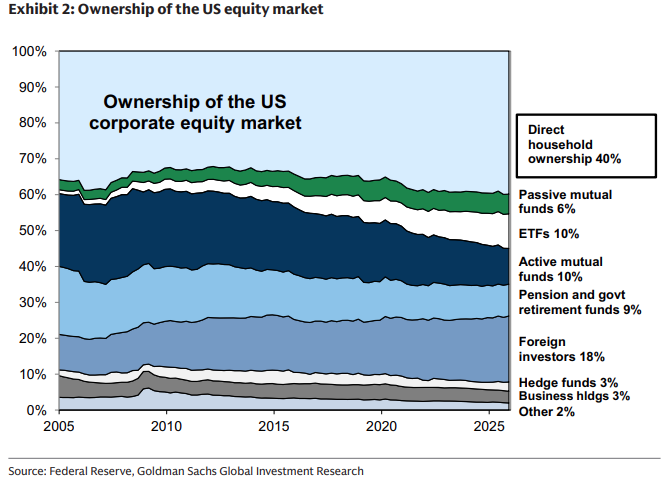

However, it is crucial to contextualize these figures. While passive funds dominate within the fund industry, their aggregate ownership of the overall stock market remains relatively smaller. This distinction is vital for understanding market dynamics, as it suggests that a substantial portion of individual stock ownership and direct market participation still resides outside of these large index vehicles. This nuance prevents an oversimplified view of passive investing’s total market influence.

The Retail Investor Resurgence: A Speculative Countercurrent

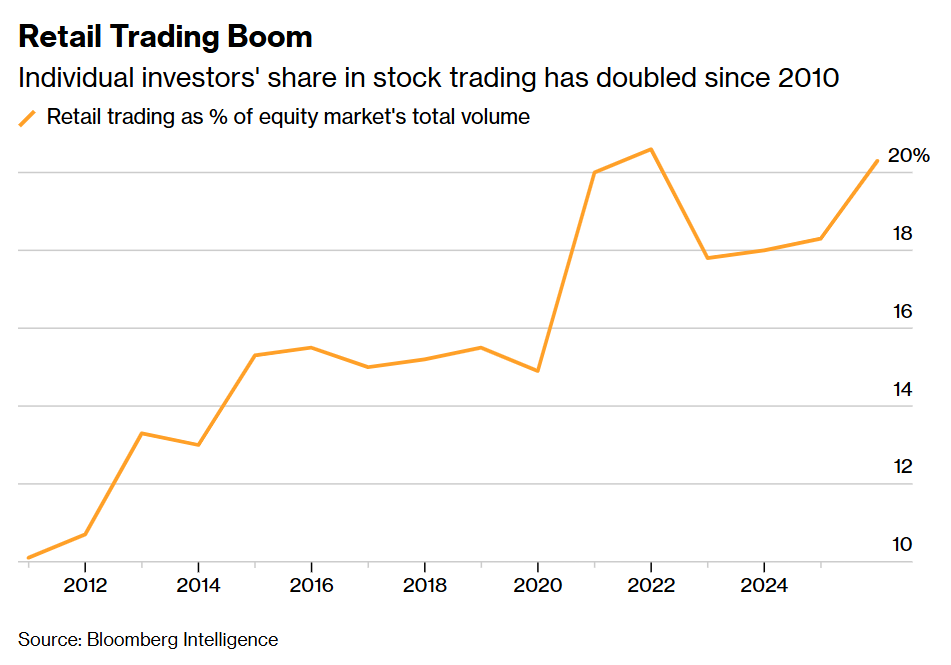

Paradoxically, the same decade that witnessed the monumental growth of passive, long-term investing also saw an explosion in retail trading activity, often characterized by short-term speculation. Starting around 2020, propelled by factors such as government stimulus checks, widespread remote work, zero-commission trading platforms, and the rise of social media-driven investment communities, retail investors dramatically increased their share of market trading.

Bloomberg data confirms this significant leap, particularly noting the surge coincident with the onset of the pandemic. Platforms like Robinhood became synonymous with this new wave of market entrants, many of whom were drawn to opportunities in high-growth technology stocks, meme stocks, and cryptocurrencies. This surge in retail participation marked a stark departure from the 2010s, where institutional investors largely dominated daily trading volumes.

A Tale of Two Investor Philosophies

This juxtaposition presents a fascinating dichotomy in contemporary investing. On one hand, trillions of dollars are being poured into "boring" index funds, representing a disciplined, long-term approach to wealth accumulation. These investors are often seeking broad market returns and eschewing the complexities and costs of active stock picking. On the other hand, a growing cohort of retail traders is actively engaging in more speculative ventures, often driven by different motivations, including the pursuit of rapid gains, a sense of market democratization, or simply the thrill of participation.

The coexistence of these two seemingly opposing trends—the steady, broad-based accumulation in passive funds and the volatile, targeted speculation by retail traders—underscores the multifaceted nature of today’s financial markets. It reflects a diverse investor base with varying objectives, risk tolerances, and access to information, creating a "narrative for everyone."

Unpacking American Wealth: Progress Amidst Persistent Disparity

Beyond the investment landscape, a similar tapestry of seemingly contradictory truths emerges when examining the distribution of wealth in the United States. Recent reports offer a nuanced perspective on the American middle class, challenging simplistic interpretations of its trajectory.

The Shrinking Middle Class: A Story of Upward Mobility

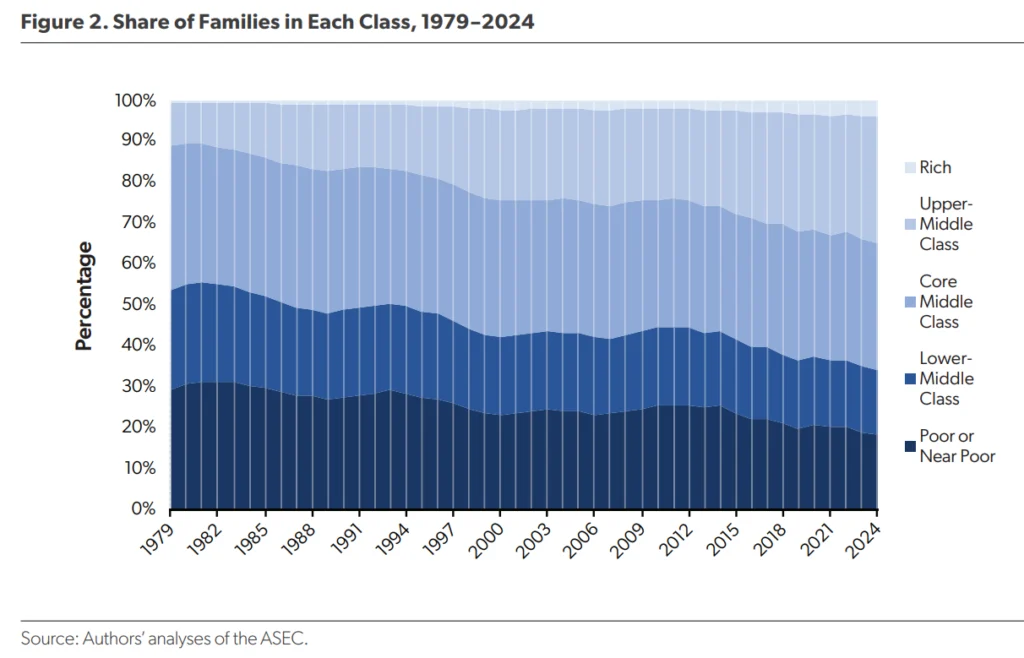

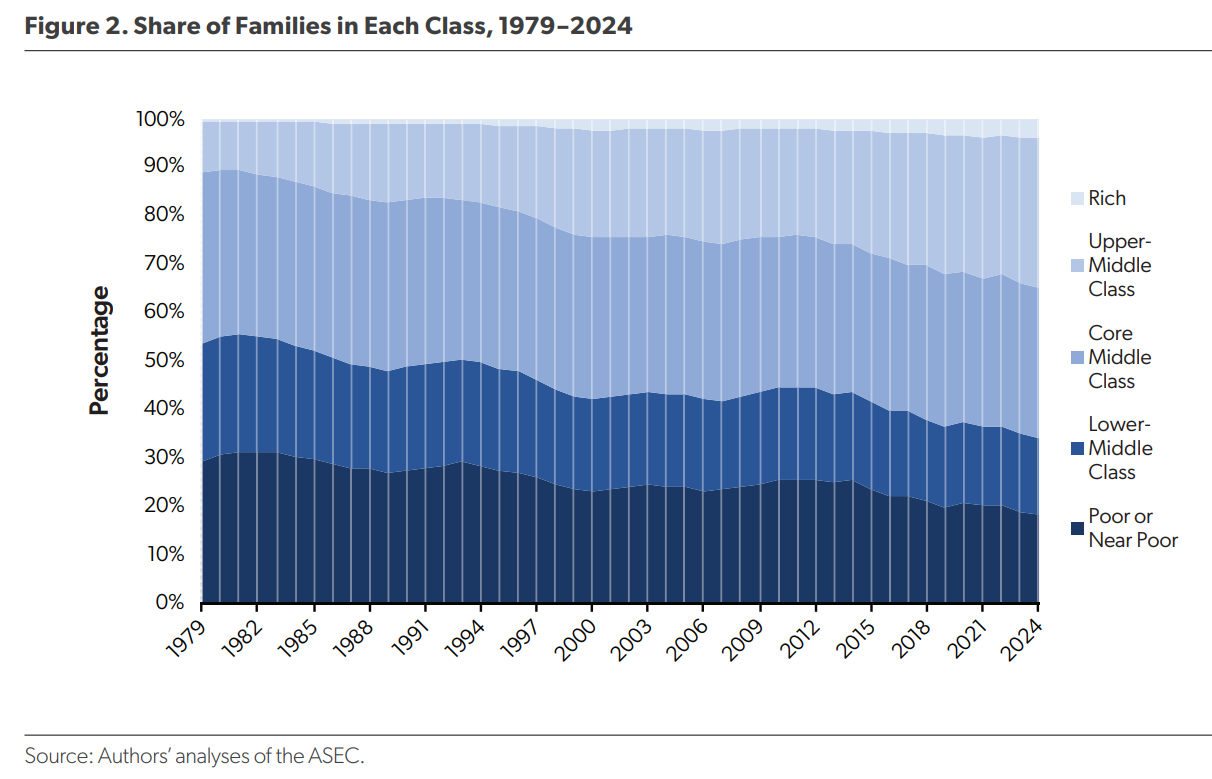

A comprehensive report released this year by the American Enterprise Institute (AEI) presents a compelling argument that the shrinking of the middle class is not necessarily a negative indicator but rather a sign of economic progress. According to the AEI’s findings, the primary reason for the middle class’s contraction is that a significant portion of households are moving up into the upper-middle class.

The data provides a clear chronological illustration of this positive trend. In 1979, for instance, 24% of American households were categorized as lower-middle class, while a substantial 30% were classified as poor or near-poor. By the latest reading, these numbers had significantly dropped to 16% and 19%, respectively. Concurrently, the upper-middle class experienced a dramatic expansion, surging from a mere 10% of households in 1979 to an impressive 31%. This growth means the upper-middle class now rivals the core middle class in size and is nearly as large as the combined lower-middle class and poor segments of the population. This upward mobility for a substantial segment of the population represents tangible economic progress.

The Expanding Rich: A Widening Gap at the Top

However, this positive narrative of upward mobility is tempered by another, equally significant trend: the disproportionate accumulation of wealth by the wealthiest households. A New York Times op-ed, referencing the same study authors, delved into the overall share of wealth held by different socioeconomic groups, revealing a stark contrast.

While the "pie" of national wealth has undoubtedly grown larger over time, allowing many to become richer in absolute terms, the distribution of the "slices" has become increasingly skewed. For example, the share of wealth held by the traditional middle class drastically fell from 24% in 1989 to a mere 8% in 2022. Even the upper-middle class saw its share decrease, from 50% to 39% during the same period.

In stark contrast, the wealthiest families—a mere 3% of all households in 2022—experienced an exponential increase in their wealth share, which more than doubled from 26% in 1989 to a staggering 53%. This indicates that while more people are moving into the upper-middle class, the very top echelon of wealth holders has gained an outsized portion of the nation’s growing prosperity. The rich have indeed gotten much, much richer, exacerbating wealth inequality at the apex of the economic pyramid.

Industry Perspectives and Broader Implications

These concurrent, often conflicting, trends provoke significant discussion among financial professionals, economists, and policymakers.

Implications for Financial Markets and Regulation:

The immense growth of passive funds, particularly the concentration of assets in a few mega-ETFs, raises questions about market efficiency and corporate governance. Some argue that the sheer scale of passive investing might distort price discovery mechanisms or reduce active oversight of corporate management. Regulators continually monitor these trends for potential systemic risks, ensuring that the infrastructure supporting these massive funds remains robust. The implications for active fund managers are clear: the pressure to justify fees and deliver alpha in an increasingly passive market intensifies, leading to further consolidation or specialization within the active management space.

The surge in retail trading, especially in speculative assets, has also drawn regulatory scrutiny. Concerns include investor protection, the potential for market manipulation (as seen with "meme stocks"), and the impact of gamified trading platforms. Discussions around payment for order flow, the transparency of trading execution, and educational initiatives for new investors are ongoing as policymakers grapple with the implications of a more democratized yet potentially riskier market environment.

Implications for Economic Policy and Social Cohesion:

The nuanced narrative of wealth distribution has profound implications for economic policy. While the upward mobility of many into the upper-middle class is a positive indicator of overall economic growth and opportunity, the widening chasm between the top 3% and everyone else points to structural challenges. Policymakers face the delicate task of fostering broad-based prosperity while addressing the concerns of extreme wealth concentration. This often involves debates around progressive taxation, social safety nets, educational access, and policies aimed at ensuring equitable access to capital and opportunities. Different economic schools of thought offer varied approaches, from supply-side economics emphasizing growth to more interventionist policies focused on redistribution and wealth taxes.

The Challenge of Nuance in a Polarized World:

Ultimately, these parallel developments underscore a critical contemporary challenge: the difficulty of embracing nuance in an increasingly polarized world. It is tempting to adopt singular, definitive narratives—either "the middle class is dying" or "everyone is getting richer." However, the data clearly shows that both progress and inequality can, and often do, coexist. More money is being invested responsibly for the long term, while simultaneously, more individuals are engaging in high-risk speculation. Households are achieving greater prosperity, yet the concentration of wealth at the very top continues to accelerate.

Recognizing that things are rarely black and white, but rather various shades of gray, is essential for a complete and accurate understanding of our complex financial and economic realities. The ability to hold seemingly contradictory truths simultaneously, to analyze data without immediately resorting to outrage or oversimplification, is indeed a lost art, but one that is more crucial than ever for navigating the intricate dynamics of the 21st century.

Contact: [Insert Contact Information if applicable]

Further Reading:

- Bloomberg: "Vanguard’s VOO Hits $1 Trillion of Assets in ETF Industry First" (June 3, 2026)

- AEI Report: "The Middle Class Is Shrinking Because of a Booming Upper Middle Class" (2026)

- New York Times Op-ed: "Middle Class Liberals Economics" (June 8, 2026)