Navigating the Unpredictable: The Enduring Wisdom of Process Over Outcomes in Financial Planning

By [Your Name/Journalist’s Name], Senior Financial Correspondent

Posted: June 14, 2026

In the complex and often bewildering world of financial markets, the quest for certainty is a fool’s errand. Yet, the disciplined act of planning remains an indispensable anchor. Renowned financial commentator and author Ben Carlson recently shared his annual investment planning ritual, a candid look into how even seasoned professionals grapple with the inherent unpredictability of wealth accumulation. His insights, penned on June 14, 2026, serve as a timely reminder that true financial resilience stems not from accurate predictions, but from a steadfast commitment to process, regardless of market gyrations.

Carlson’s "back-of-the-envelope" approach is more than just a numerical exercise; it’s a foundational introspection designed to establish vital "goalposts" on his financial journey. By taking stock of current net worth, savings rates, and making informed assumptions about future income and return expectations, he models potential scenarios across 5, 10, 15, and 20-year horizons. This meticulous, albeit inherently flawed, projection began when he was 25 and continues to provide crucial "road markers" for strategic planning. The core objective, Carlson emphasizes, is not to achieve predictive certainty – an impossibility in dynamic markets – but to gauge progress against a reasonable range of anticipated outcomes.

The Unforgiving Chronology of Market Extremes

Carlson’s personal financial timeline offers a compelling illustration of market non-linearity, characterized by periods of both profound despair and unexpected exuberance. His journey underscores a universal truth: market assumptions are almost always wrong because financial landscapes, much like life itself, are "lumpy," not linear.

The Crucible of the Great Financial Crisis (2005-2010)

Carlson’s initial years of serious investing coincided with one of the most tumultuous periods in modern financial history: the Great Financial Crisis (GFC). Beginning his retirement contributions around 2005, he faced an immediate and brutal baptism by fire. The subsequent collapse of the housing market, the subprime mortgage crisis, and the cascading failures of major financial institutions like Lehman Brothers plunged global economies into a deep recession.

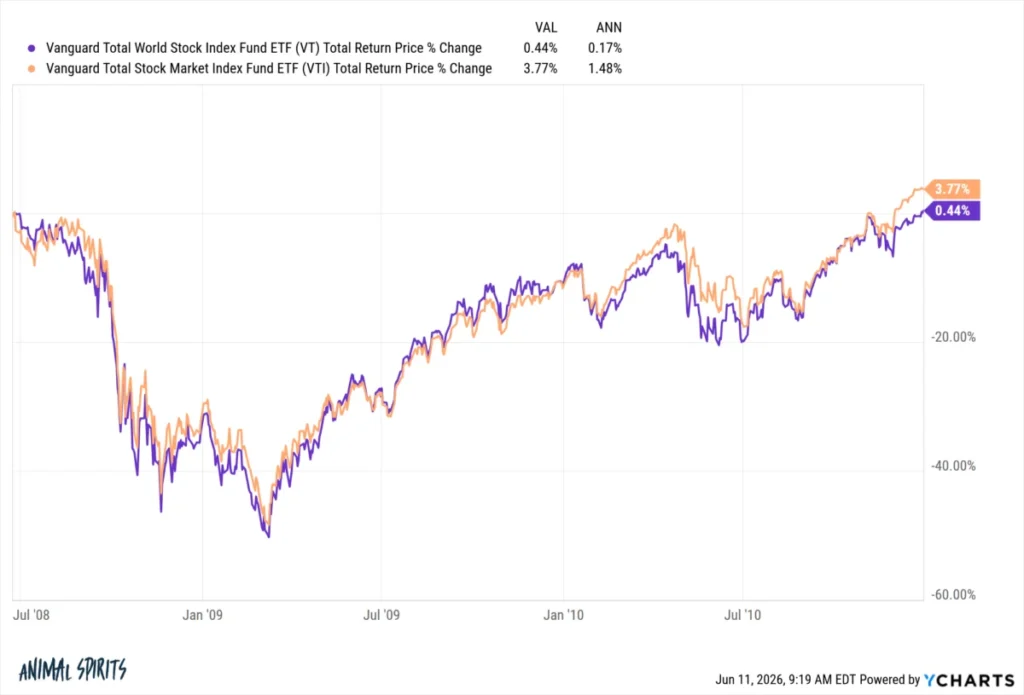

During this period, from late 2007 through early 2009, the S&P 500 index plummeted by approximately 57% from its peak. Carlson’s early financial projections, however conservative, fell "far short" of reality. As he recounts, "From 2005 to 2010, when I first started investing in my retirement accounts, stocks essentially went nowhere." The accompanying chart (likely depicting the performance of broad market ETFs like VT or VTI) would have vividly illustrated this stagnation, portraying a ferocious bear market that devoured capital and tested the resolve of even the most disciplined investors.

This environment, where consistent contributions yielded little to no visible progress in market value, could easily induce feelings of inadequacy or "dumbness" in an investor. Yet, Carlson’s unwavering commitment to his plan – continuing to buy periodically even as prices fell – exemplifies the counterintuitive wisdom required during downturns. While emotionally taxing, these years offered the strategic advantage of accumulating assets at significantly lower valuations, a silver lining often obscured by widespread panic. This period highlights the critical importance of emotional fortitude and adherence to a long-term investment strategy, particularly when immediate returns are abysmal.

The Unforeseen Ascent: A Bull Market Beyond All Expectations (2009-2026)

Following the depths of the GFC, the global financial landscape underwent a dramatic transformation. Fueled by unprecedented monetary stimulus from central banks, technological innovation, and a prolonged period of low interest rates, equity markets embarked on an extraordinary bull run. From the market bottom in early 2009, the S&P 500 has surged, generating annual returns exceeding 15% per year, while a globally diversified stock portfolio has delivered around 12% annually. Carlson notes, with specificity, that the U.S. stock market has seen an astounding 16.9% per year from the GFC trough.

These figures are remarkable, far outstripping the historical average real returns of 7-10% typically used in conservative financial planning. Carlson candidly admits, "No one builds a financial plan with return assumptions this high. I certainly didn’t." The sheer longevity and magnitude of this bull market defied nearly all expert predictions. As a result, Carlson’s current portfolio value has grown to a size that "didn’t even exist in my range of outcomes" from his original projections.

This unexpected bounty, however, comes with a crucial caveat. Carlson wisely points out, "I’m not smarter because the markets have been going up… it’s not my raw intelligence that increased my portfolio to heights I didn’t plan on 5, 10 and 15 years ago." This profound observation underpins his core message: market performance is largely divorced from individual investor brilliance. Bull markets do not equate to genius, just as bear markets do not signify idiocy. His consistent actions during the GFC – "I bought and I held and everything went straight down" – were the correct ones, irrespective of immediate returns. Similarly, his continued adherence to his strategy during the bull market, rather than active "smart" management, was the true driver of his unexpected success.

Supporting Data: The Psychology and Principles of Sound Investing

Carlson’s narrative resonates deeply with established principles of behavioral finance and long-term investment strategy. The market’s "lumpy" nature is a constant reminder of the difficulty of forecasting and the futility of market timing.

The Pitfalls of Emotional Investing

Behavioral economists, such as Daniel Kahneman and Amos Tversky, have extensively documented the cognitive biases that plague human decision-making, particularly in financial contexts. During bear markets, fear and panic can trigger "loss aversion," leading investors to sell at the worst possible time, locking in losses. Conversely, bull markets often foster "overconfidence" and "recency bias," convincing investors that recent extraordinary returns are sustainable, leading to irrational exuberance and excessive risk-taking.

Carlson’s observation that "Bear markets can make you question your plan. Bull markets can lead to overconfidence" perfectly encapsulates these psychological traps. The temptation to abandon a sound strategy during a downturn, or to chase speculative gains during an upturn, is a powerful emotional impulse. Resisting these urges is paramount for long-term success.

The Power of Diversification and Dollar-Cost Averaging

Carlson’s "dutiful contributions" during the GFC exemplify the power of dollar-cost averaging. By consistently investing a fixed amount over time, regardless of market fluctuations, investors naturally buy more shares when prices are low and fewer when prices are high. This strategy mitigates the risk of mistiming the market and systematically builds wealth over the long term. Coupled with diversification – spreading investments across various asset classes, geographies, and sectors – it forms the bedrock of a robust investment plan designed to weather diverse market conditions.

The Imperative of Long-Term Perspective

The dramatic swings in Carlson’s portfolio performance over two decades underscore the importance of a long-term investment horizon. Short-term market movements are notoriously unpredictable, often driven by sentiment and ephemeral news cycles. However, over extended periods, the underlying growth of economies and corporate earnings tends to assert itself, rewarding patient investors. Carlson’s ability to remain invested through a "ferocious bear market" and then benefit from an "unforeseen bull market" is a testament to the compounding power of time and consistent investment.

Official Responses and Expert Consensus: Reinforcing the Process

The experiences shared by Carlson align perfectly with the consensus among leading financial strategists and fiduciaries. The "official response" from the investment community to the challenges of market volatility and investor psychology is consistently centered on discipline, planning, and humility.

The Value of a Written Investment Policy Statement

Many financial advisors advocate for a written Investment Policy Statement (IPS) or, in Carlson’s simpler rendition, the act of "writing stuff down." This document formalizes an investor’s goals, risk tolerance, asset allocation strategy, and rebalancing rules. Carlson’s personal habit of documenting "Here’s what I’m going to do and why I’m going to do it. Here’s what I think might happen" serves the same critical purpose: it creates a tangible record of one’s rationale, providing a rational anchor when emotions threaten to hijack decision-making.

This practice helps in "being outcome-based" by forcing a focus on controllable actions (the process) rather than uncontrollable results (the market’s performance). It fosters accountability and provides a framework for evaluating deviations, not as failures, but as learning opportunities to refine the process itself.

Embracing Humility and Rejecting Hubris

The financial world often rewards those who demonstrate intellectual humility. As Carlson eloquently states, "Bull markets don’t mean you’re a genius just like bear markets don’t make you an idiot." This perspective is vital for sustainable investing. Attributing success solely to one’s own brilliance during good times can lead to excessive risk-taking and a dangerous underestimation of market forces. Conversely, blaming oneself for poor market performance during downturns can erode confidence and lead to impulsive, detrimental decisions.

Leading figures like Warren Buffett have long championed the virtues of patience, temperament, and a long-term perspective, emphasizing that success in investing is less about IQ and more about emotional control and adherence to a sound framework.

Implications for the Individual Investor: Cultivating Financial Resilience

Carlson’s personal narrative offers profound implications for every individual investor seeking to build lasting wealth.

Prioritizing Emotional Discipline

The greatest battle in investing is often fought within oneself. The temptation to react to daily headlines, market swings, or the perceived wisdom of "gurus" is immense. Carlson’s journey highlights that emotional discipline is not merely a desirable trait; it is a fundamental pillar of investment success. Learning to separate market noise from fundamental trends, and to stick to a predetermined plan even when it feels uncomfortable, is a skill that pays dividends over decades.

The Primacy of "Process Over Outcomes"

This maxim is the cornerstone of Carlson’s message. While outcomes are ultimately what we care about (growing wealth, achieving financial independence), they are largely beyond our direct control. What is within our control is the process: our savings rate, our asset allocation, our diversification, our rebalancing schedule, and our emotional response to market events. By focusing diligently on these controllable inputs, investors maximize their chances of achieving positive outcomes, even if the specific path taken is entirely unforeseen. A well-defined process provides a sturdy framework that can absorb shocks and capitalize on opportunities, irrespective of market sentiment.

Adaptability Within a Framework

While sticking to a plan is crucial, rigidity can also be detrimental. Carlson’s annual review process, where he takes "stock of where you are, where you’ve been and where you’re going," implies a degree of adaptability. This isn’t about market timing; it’s about re-evaluating assumptions and adjusting the plan (e.g., savings rate, risk tolerance) in light of significant life changes or prolonged shifts in the economic environment, while maintaining the core investment strategy. The road markers are there to guide, not to bind.

The Unceasing Journey of Learning and Humility

Investing is a continuous learning experience, and the market is an unforgiving teacher. Carlson’s act of "writing stuff down" is not just about establishing a plan; it’s about creating a personal ledger of assumptions, expectations, and actual outcomes. This reflective practice fosters humility and helps investors learn from both successes and failures, ensuring that neither bull market euphoria nor bear market despair unduly influences future decisions.

In conclusion, Ben Carlson’s reflections offer a powerful antidote to the often-stressful pursuit of financial security. By embracing a disciplined planning process, maintaining emotional fortitude through market extremes, and prioritizing controllable actions over unpredictable outcomes, investors can navigate the inherent lumpiness of financial markets. True financial wisdom lies not in the ability to predict the future, but in the unwavering commitment to a sound strategy, knowing that resilience, not genius, is the ultimate determinant of long-term success.