The Inflation Paradox: Navigating Economic Resilience and Mounting Price Pressures

The defining narrative of the mid-2026 economic landscape remains a complex interplay between stubborn, broadening inflation and a surprisingly resilient domestic growth engine. As the second quarter draws to a close, investors and policymakers are grappling with a "higher-for-longer" reality. While finalized data from the Bureau of Economic Analysis (BEA) confirms that the U.S. economy gained significant momentum at the start of the year, the latest reports on personal consumption expenditures suggest that the battle against rising costs is far from over. This dichotomy has left equity markets increasingly volatile, as participants recalibrate their expectations for Federal Reserve policy in the months ahead.

1. The Main Facts: An Economy in Tension

At the heart of the current economic environment is a fundamental contradiction: the economy is growing at a pace that exceeds expectations, yet the cost of living continues to erode consumer confidence.

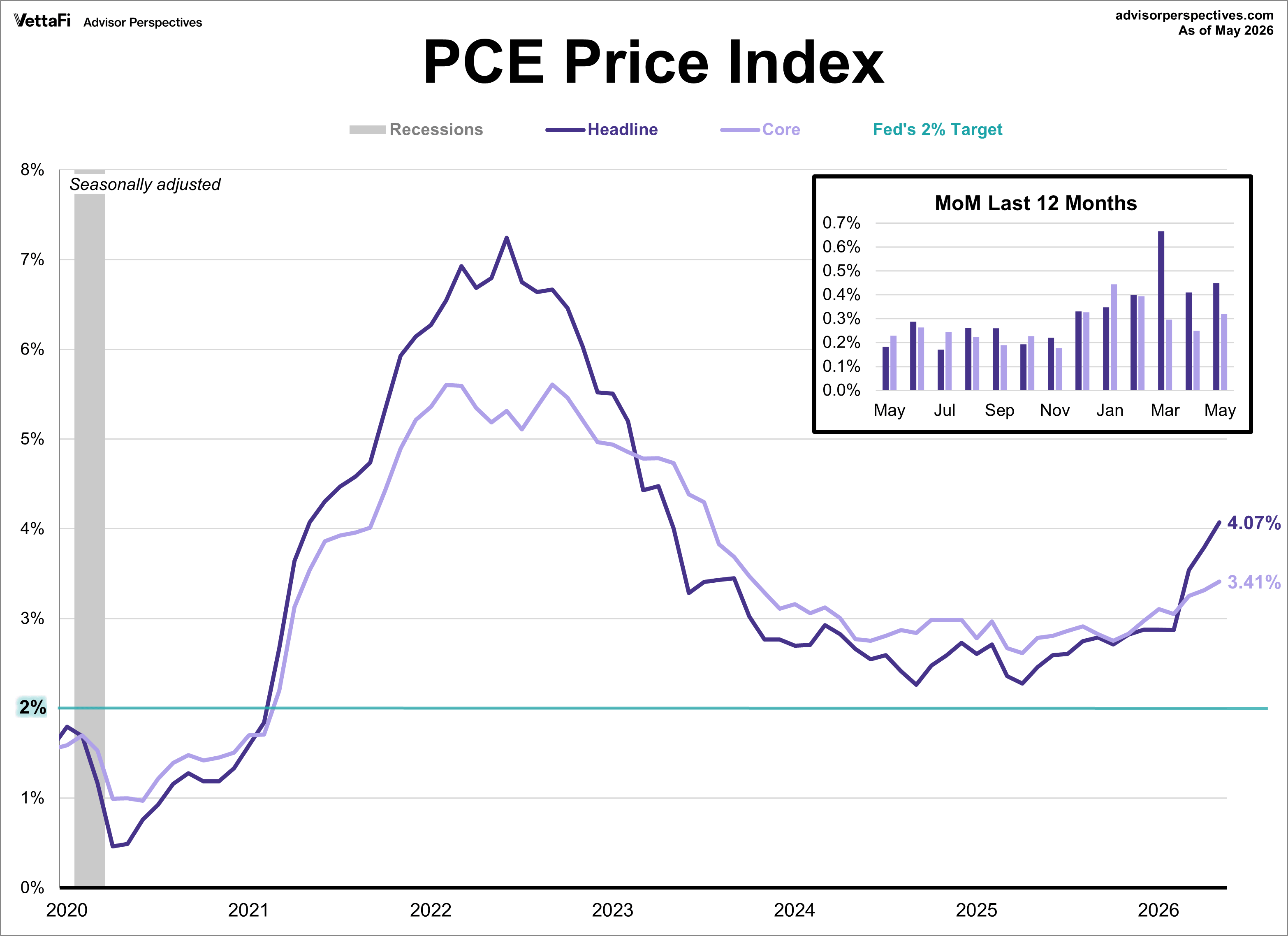

The most recent data from the Personal Consumption Expenditures (PCE) price index—the Federal Reserve’s preferred inflation gauge—reveals that inflation is not merely a temporary artifact of supply chain disruptions, but a persistent force. In May, the headline PCE index rose by 0.4% on a monthly basis, pushing the year-over-year rate to 4.1%. This represents the highest annual pace observed since April 2023. More concerning, perhaps, is the "core" PCE index, which strips away the volatile categories of food and energy. This metric advanced 0.3% in May, reaching an annual rate of 3.4%—the highest level since October 2023.

These figures indicate that price pressures are no longer confined to specific sectors but are instead embedding themselves throughout the broader economy. While geopolitical tensions in the Middle East have been a primary driver of energy-related inflation, the stickiness of core inflation suggests that the underlying demand remains robust, complicating the Federal Reserve’s efforts to return to its 2% target.

2. Chronology of Events: From Q1 Growth to June Sentiment

To understand the current market malaise, one must look at the sequence of data releases that shaped the narrative throughout the second quarter of 2026.

- Early Q2 (April–May): Markets initially hoped for a cooling trend in inflation. However, sustained volatility in energy markets, spurred by Middle Eastern instability, kept headline inflation elevated.

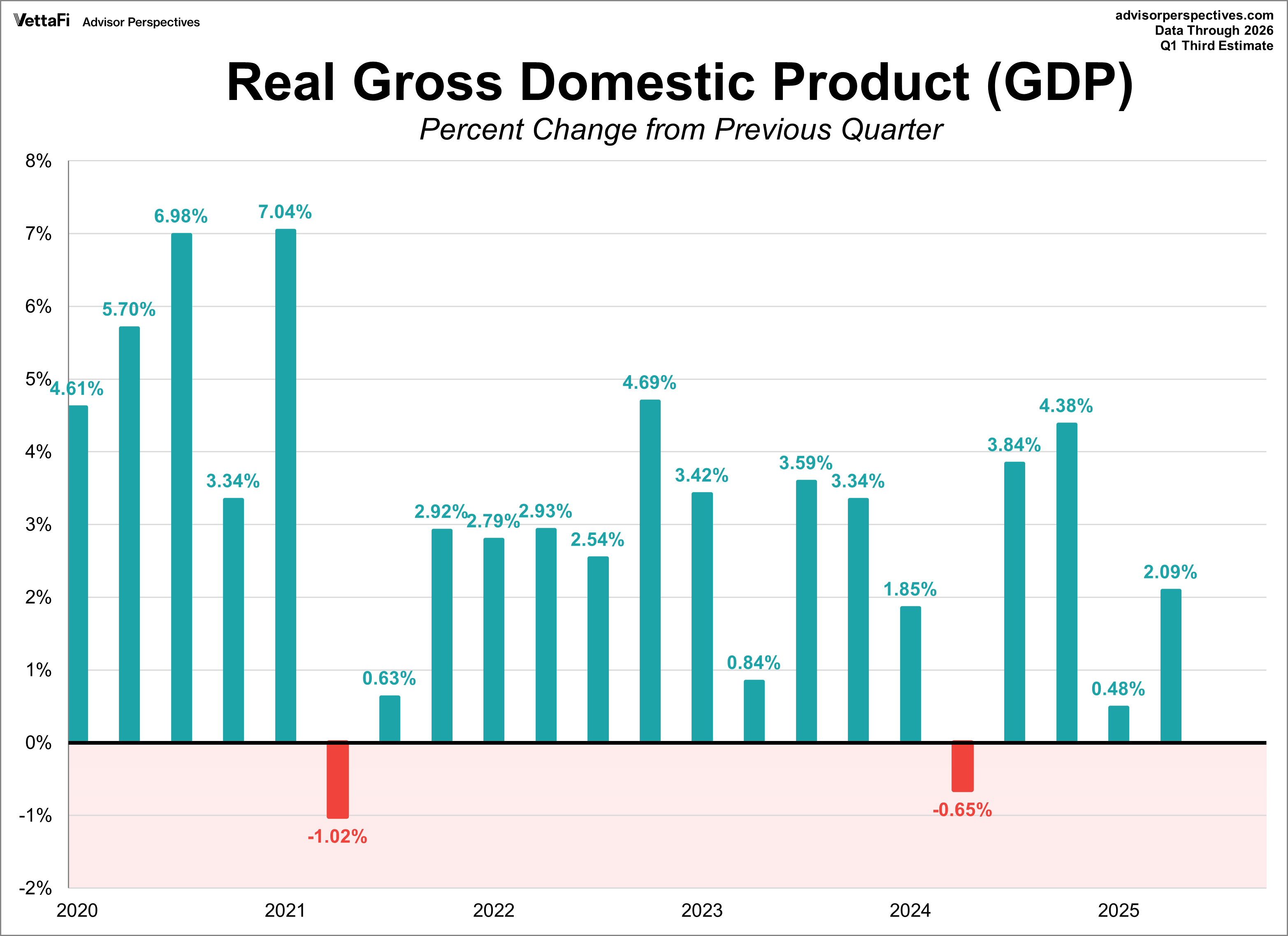

- Mid-June: The BEA released its third estimate for Q1 2026 Gross Domestic Product (GDP). Defying earlier pessimistic forecasts, the economy expanded at a 2.1% annualized rate, a significant leap from the 0.5% growth recorded in the final quarter of 2025. This surge was underpinned by a healthy blend of business investment, exports, and government spending.

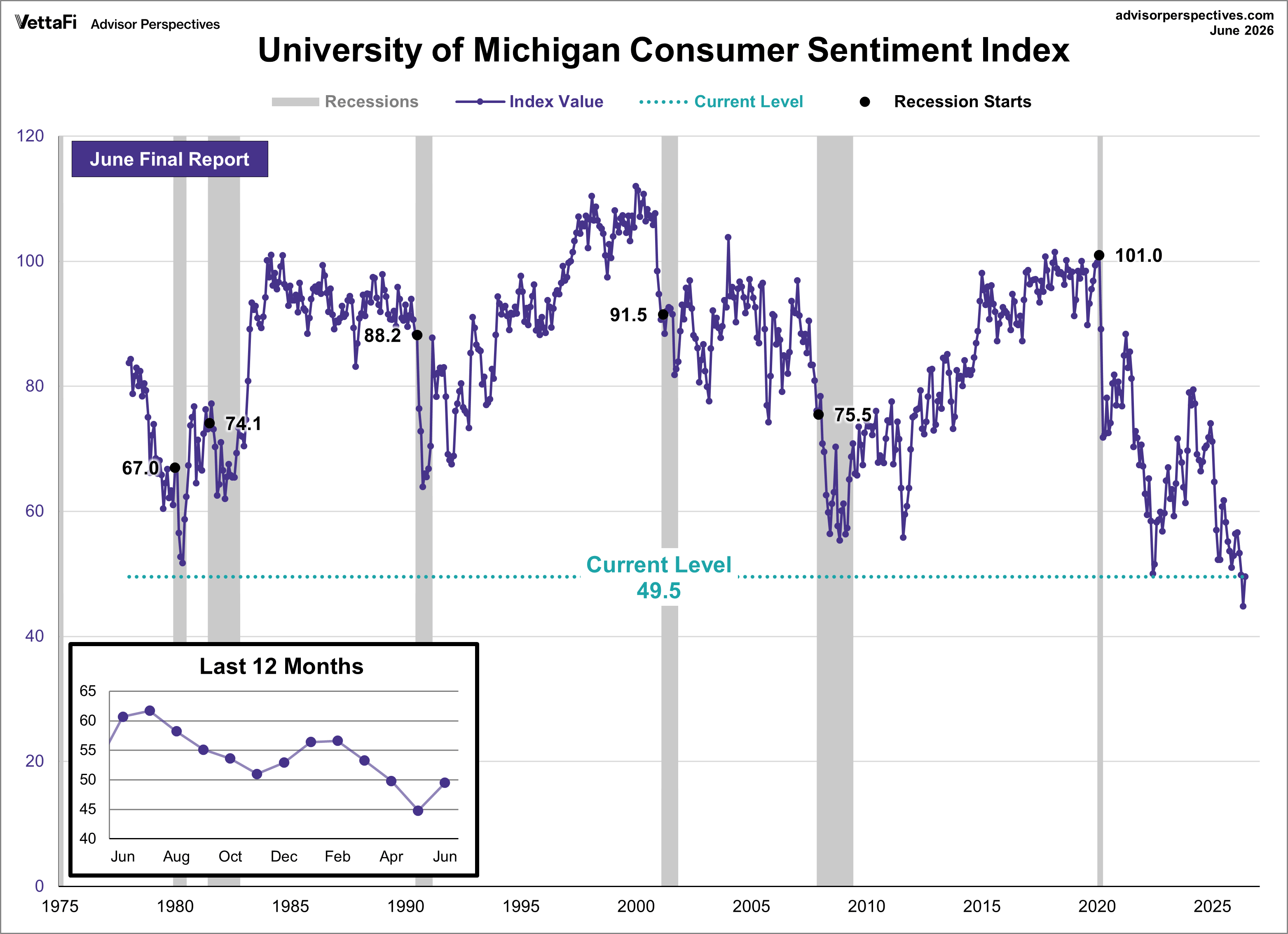

- Late June: The University of Michigan’s Consumer Sentiment Index offered a glimmer of hope, rising to 49.5 in June. This 10.5% rebound from May’s historic low marked the first monthly increase in four months. The catalyst for this improvement was primarily the easing of gasoline prices, which followed the signing of a regional peace deal in the Middle East.

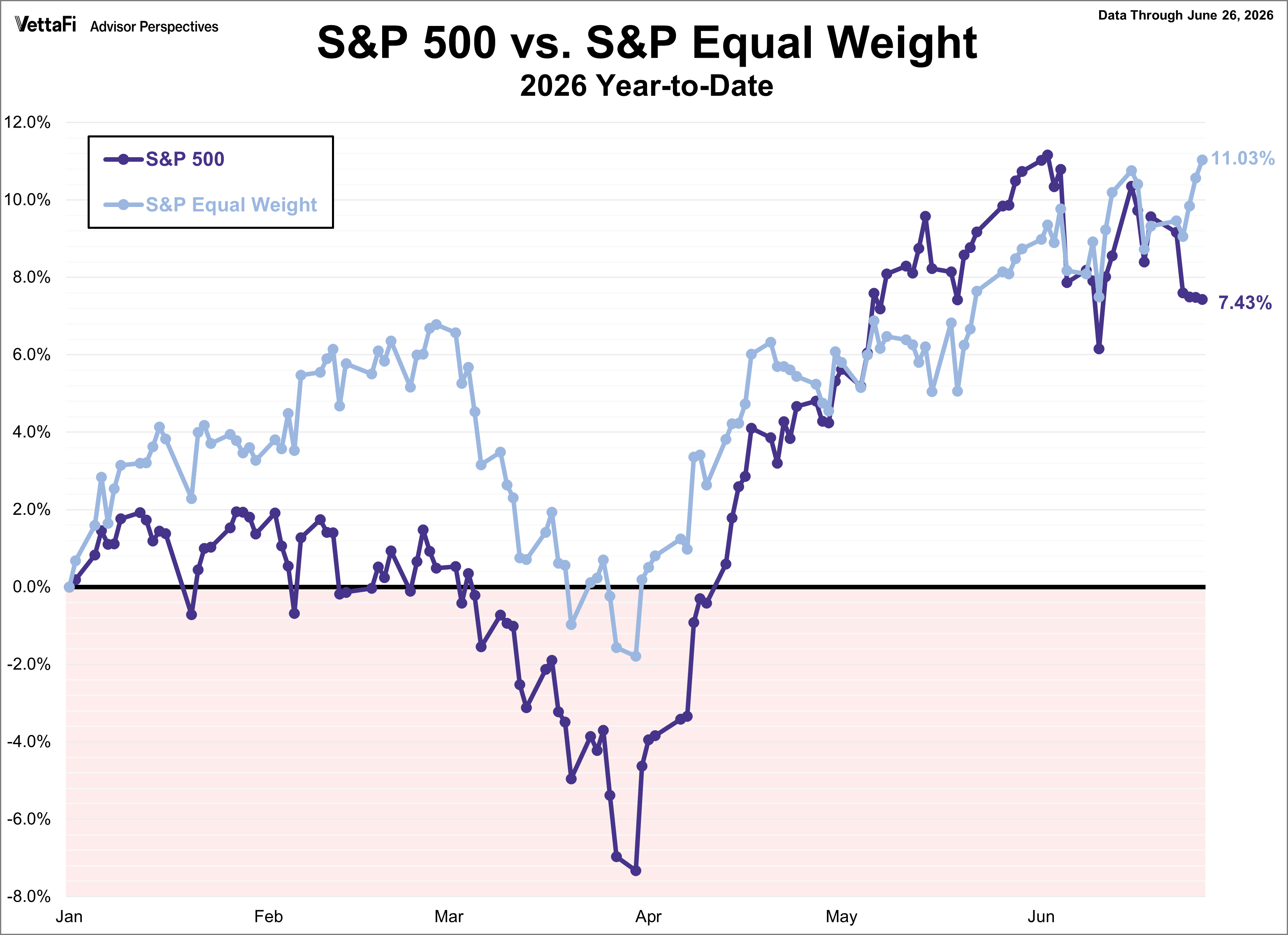

- The Final Week of June: Despite the sentiment boost, equity markets faltered. The S&P 500 endured a continuous daily decline throughout the final week of the month, representing the longest losing streak since August of the previous year.

3. Supporting Data: Beneath the Surface

A deeper analysis of the economic indicators reveals the nuances of the current environment.

The Resilience of GDP

The 2.1% growth rate for Q1 2026 is a testament to the durability of the U.S. consumer and corporate sector. Analysts had originally projected a more sluggish 1.6% expansion. The fact that the economy beat these estimates by half a percentage point suggests that domestic demand remains high, even as interest rates remain elevated. Business investment, in particular, has shown surprising strength, suggesting that companies remain confident enough in the long-term horizon to commit capital despite the macroeconomic headwinds.

The Sentiment Gap

Despite the 10.5% rise in consumer sentiment, the index at 49.5 remains near historic lows. This highlights a critical "sentiment gap." While consumers are relieved by the recent dip in gasoline prices—which dropped below $4 per gallon—they remain deeply concerned about the broader cost of living. This is corroborated by the University of Michigan’s inflation expectations data: while one-year expectations fell from 4.8% to 4.6% and five-year expectations moderated to 3.3%, both figures remain well above the historical norms seen prior to the 2020s.

Market Divergence

The disparity between the S&P 500 (market-cap weighted) and the S&P 500 Equal Weight Index (RSP) tells a story of internal market shifts. While the broader S&P 500 fell 2.0% during the final week of June, the Equal Weight Index rose 1.2%. This suggests that while large-cap growth stocks—which often lead the market—were sold off in anticipation of Fed tightening, investors were rotating capital into smaller components of the index, perhaps seeking value in a high-interest-rate environment.

4. Official Responses and the Fed Outlook

The Federal Reserve finds itself in a precarious position. The combination of strong growth and sticky inflation limits the central bank’s room to maneuver.

According to the CME FedWatch Tool, the market sentiment as of late June is heavily tilted toward a "hold" strategy for the July meeting, with a 70% probability of no change. However, a 30% probability remains for a 25 basis point hike. This indecision reflects the lack of clarity regarding how much "pain" the economy can withstand before growth turns negative.

Looking toward the remainder of the year and into 2027, the prevailing market consensus—as priced into the futures market—suggests a potential rate hike in September followed by an extended pause. The Fed’s messaging remains focused on data dependency, with officials emphasizing that they are prepared to keep rates high for as long as necessary to ensure that inflation does not become structurally embedded in the economy.

5. Implications: Navigating the "Higher-for-Longer" Era

For investors, businesses, and households, the current economic climate carries several long-term implications.

For the Investor

The volatility in the S&P 500 serves as a warning that equity valuations are highly sensitive to inflation prints. As long as inflation remains the "defining narrative," market participants should expect sharp rotations between growth and value sectors. Instruments like the Consumer Discretionary Select Sector SPDR ETF (XLY) are likely to remain tied to the fluctuating sentiment of the average household, making them barometers for the broader economy’s health.

For the Household

While the stabilization of energy prices provides temporary breathing room, the "core" inflation figures suggest that the cost of services, shelter, and non-discretionary items may continue to pinch household budgets. The decline in five-year inflation expectations to 3.3% is a positive signal, indicating that the public believes the Fed will eventually gain control, but it also confirms that the transition to a lower-inflation environment will be a slow, multi-year process.

For Economic Policy

The reliance on GDP growth as a sign of health is currently being challenged by the reality of inflation. Policymakers must now balance the need to prevent an economic recession with the necessity of suppressing price pressures. If the Federal Reserve maintains rates at current levels, the risk of a policy-induced slowdown increases; however, if they pivot too early, they risk a repeat of the stagflationary pressures that defined the late 20th century.

Conclusion

The economy of mid-2026 is a landscape defined by contradictions. It is an economy that refuses to cool down despite restrictive monetary policy, yet it is also one where the average participant feels the weight of increased costs at every turn. As we look toward the second half of the year, the path forward will be dictated by the Fed’s ability to navigate these crosscurrents. The "defining narrative" of inflation is likely to persist until the broadening price pressures seen in the core PCE index show clear, consistent signs of reversal. Until then, caution, volatility, and a "wait-and-see" approach will remain the hallmarks of the financial markets.