Beyond the Credit Score: Navigating the 2026 K-Shaped Lending Paradox

For decades, the consumer lending industry has operated under a singular, golden rule: speed is everything. In the pursuit of the "frictionless" borrower experience, lenders have streamlined digital applications to the point of near-instantaneous decisioning. Yet, as the calendar turned to 2026, the financial services sector finds itself trapped in a profound paradox. While the mandate for growth remains as aggressive as ever, the underlying economic foundation has shifted, rendering the traditional "fast-track" playbook increasingly obsolete.

With auto and credit card delinquencies pressing against levels not seen since the Great Recession, and the once-reliable credit score losing its predictive nuance, lenders are being forced to re-evaluate their entire risk architecture. The modern economy is no longer a monolith; it is "K-shaped," characterized by a widening chasm between those who are thriving and those who are struggling. For institutions attempting to grow safely in this volatile environment, the question is no longer just how to process loans faster, but how to identify the right borrowers to say "yes" to in an increasingly fragmented market.

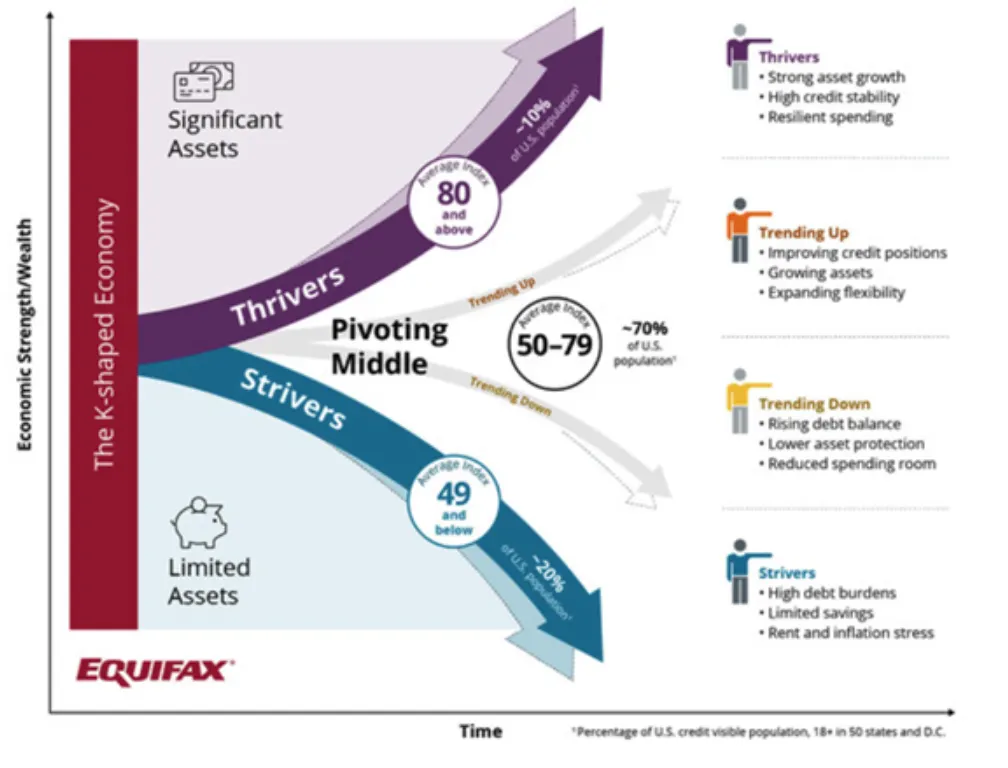

The Shrinking Middle: The Rise of the "Striver"

The economic landscape of 2026 is defined by a distinct divergence. According to recent market analysis from Equifax, the American consumer base is splitting into two clear camps: the "Thrivers" and the "Strivers."

For the past two years, the economic data has shown a consistent trend: the middle class is shrinking, migrating either toward greater financial stability or into a state of precarious volatility. Lenders who continue to focus their underwriting exclusively on the "Thriver" segment—those with pristine credit histories and long-standing stability—are finding themselves in a high-stakes, hyper-competitive environment. With the pool of "easy" credit-worthy applicants dwindling, the competition for these individuals is driving down margins and limiting volume.

To achieve sustainable growth, lenders must pivot. The path forward lies in the "Strivers"—the migrating middle and the thin-file population that possess the capacity to repay but lack the historical footprint to qualify under traditional legacy models.

The "No-Score" Myth: A $1 Trillion Misunderstanding

Perhaps the most damaging legacy in modern lending is the "No Score, No Loan" policy. For years, the industry operated on the assumption that a thin credit file or a lack of credit history was synonymous with subprime risk. It was a convenient, albeit flawed, heuristic used to minimize operational overhead.

However, recent data tells a story that defies this conventional wisdom. A comprehensive study of over 9 million card originations conducted by Equifax between 2022 and 2024 revealed that the "unscoreable" population does not perform like the deep subprime borrowers that risk models often assume. In fact, these individuals exhibit performance metrics remarkably similar to the 600–639 credit score band—a "near-prime" category that is often profitable for lenders who know how to price for it.

By auto-declining this segment, lenders are not just being cautious; they are effectively leaving billions of dollars in viable, long-term portfolio growth on the table. The "No-Score" myth has acted as a self-imposed ceiling on institutional expansion, trapping lenders in a cycle of competing for the same shrinking pool of high-FICO applicants.

The Mechanics of Risk: Slicing Through the Noise

The fundamental problem with the traditional credit score is that it is a retrospective measurement. It tells you what a borrower did, but it often fails to account for what a borrower can do today. In the 2026 K-Shaped economy, the gap between a borrower’s past and their current capacity has never been wider.

If two applicants walk into a financial institution, both carrying a 699 credit score, they are often treated as identical risks. Yet, if one of those applicants has a stable, high-income career with documented employment history, while the other is experiencing volatile income fluctuations, the risk profiles are fundamentally different.

The solution is the integration of alternative data. By overlaying income verification, employment tenure, and real-time job stability onto traditional credit files, lenders can peel back the layers of a credit score to reveal the true "capacity" of the individual. This "swap-in" strategy allows institutions to:

- Differentiate "Near-Prime" from "Deep Subprime": Identifying resilient borrowers who were previously invisible.

- Verify High-Income/No-File Applicants: Capturing high-potential customers who lack credit history but have the cash flow to sustain debt.

- Adjust for Macroeconomic Shifts: Rapidly adapting underwriting standards as economic conditions fluctuate for specific employment sectors.

The Case for "Smart Friction"

The term "friction" has long been treated as a dirty word in financial services. Lenders have spent millions of dollars trying to remove every click, every identity check, and every document request from the borrower journey. However, in an era where sophisticated fraud—such as credit washing, loan stacking, and synthetic identity theft—is on the rise, total frictionless lending is a vulnerability.

The industry is now beginning to embrace the concept of "Smart Friction." This is the strategic insertion of friction at the optimal point in the fraud waterfall. By slightly slowing the process at the earliest stage of the application—such as verifying employment through secure, automated channels—lenders can stop bad actors before they consume operational capital or pollute the loan portfolio.

Smart friction is not about making life difficult for the borrower; it is about building a secure, sustainable environment where the "good" borrowers can be approved with confidence, while the "bad" actors are filtered out before they can do damage. It is a shift from reactive security to proactive, intelligent underwriting.

Implications for the Future of Lending

The findings from the recent Equifax webinar, "Decoding Borrower Capacity in the 2026 K-Shaped Economy," highlight a stark reality for industry leaders: the playbook that worked in the 2010s will not work today.

Lenders who refuse to evolve will find themselves increasingly isolated in a contracting segment of the market. Conversely, those who lean into alternative data and "smart friction" will unlock a significant competitive advantage. The ability to look past the 700-score threshold and accurately assess the "Striver" population represents the next great frontier in financial services.

As we navigate the remainder of 2026, the institutions that succeed will be those that view data not merely as a tool for declining applications, but as a bridge to safely expanding them. The "K-Shaped" economy is not a barrier; it is a lens through which the savvy lender can find hidden value.

The data is clear: the opportunity to grow is there, provided lenders are willing to look beyond the score.

For those interested in a deeper analysis of these trends, industry professionals are encouraged to review the full findings from the Equifax webinar, "Beyond the 700 Score," to understand how to build more resilient and profitable portfolios in the modern economic climate.