The Great Fintech Migration: How Legacy Giants Like Quicken are Losing Ground to a New Era of Personal Finance Apps

Main Facts

The landscape of personal financial management (PFM) is undergoing a major structural shift. For over three decades, Quicken was the undisputed titan of home budgeting, helping millions of households manage their ledgers from desktop computers. However, by 2026, the legacy giant—now marketed as Quicken Classic—finds itself increasingly defensive against agile, cloud-native, and mobile-first software applications.

Consumer migration away from desktop-bound platforms is accelerating. This trend is driven by open banking APIs, real-time transaction syncing, automated subscription management, and artificial intelligence. While legacy systems required tedious manual entry and local data backups, modern alternatives offer automated dashboards that integrate every aspect of a user’s financial life—often at a lower cost or entirely free.

Today’s PFM market is highly fragmented, with specialized apps catering to different consumer philosophies:

- Monarch Money and Quicken Simplifi lead the market in premium, collaborative budgeting.

- Empower dominates the free investment and wealth-tracking sector.

- Origin has introduced automated, AI-driven financial planning.

- You Need A Budget (YNAB) maintains a strong hold on zero-based budgeting purists.

This report analyzes this shifting market, examining how these alternatives compare to legacy systems, the historical context of this digital evolution, and the long-term implications for consumer data privacy and wealth management.

Chronology: The Evolution of Personal Financial Software

To understand why legacy platforms are losing market share, it is necessary to examine the history of digital personal finance over the last forty years.

+---------------------------------------------------------------------------------+

| PFM CHRONOLOGY |

+---------------------------------------------------------------------------------+

| 1980s - 1990s: The Desktop Era |

| - Quicken dominates offline home ledgers via local storage and manual entries. |

| |

| 2000s - 2010s: The Cloud & Web Revolution |

| - Mint.com introduces free, ad-supported web syncing. |

| - Personal Capital (now Empower) launches advanced investment dashboards. |

| |

| Late 2010s - Early 2020s: The Subscription Pivot |

| - Quicken transitions to a mandatory annual subscription model. |

| - Open banking platforms (e.g., Plaid) allow secure, real-time bank syncing. |

| |

| 2023 - 2024: The Great Migration Catalyst |

| - Intuit shuts down Mint, leaving millions of users searching for new tools. |

| - Monarch Money, YNAB, and Simplifi experience unprecedented user surges. |

| |

| 2025 - 2026: The AI & Automation Era |

| - AI tools like Origin automate budgeting, tax preparation, and estate planning.|

| - Collaborative, multi-user platforms become standard for modern households. |

+---------------------------------------------------------------------------------+The Desktop Era (1983–2000s)

Quicken was released in the mid-1980s as an offline checkbook balancing tool. It became a household staple by allowing users to manage bank accounts, investments, and small business ledgers from their hard drives. For over twenty years, users purchased physical software discs or digital downloads once every few years, keeping their sensitive financial data entirely local.

The Cloud and Web Revolution (Mid-2000s–2010s)

The launch of Mint.com in 2007 changed the industry by introducing free, web-based aggregation. Instead of manual data entry, Mint linked directly to financial institutions to categorize transactions automatically. Around the same time, Personal Capital (later rebranded as Empower) launched, offering high-net-worth individuals free tools to track investment portfolios, asset allocations, and net worth.

The Subscription Pivot and Open Banking (2016–2022)

Under pressure from cloud-native startups, Quicken shifted from a one-time purchase model to an annual subscription service. This move frustrated long-time users who preferred local, non-recurring software. Concurrently, secure open banking aggregators like Plaid, Finicity, and Yodlee emerged, allowing third-party apps to sync transaction data quickly and securely.

The Great Migration Catalyst (2023–2024)

In late 2023, Intuit announced it would shut down Mint.com and merge its user base into Credit Karma, a move that removed many of Mint’s core budgeting features. This decision displaced millions of users, triggering a massive migration to alternative platforms like Monarch Money, YNAB, and Quicken Simplifi.

The AI and Collaborative Era (2025–2026)

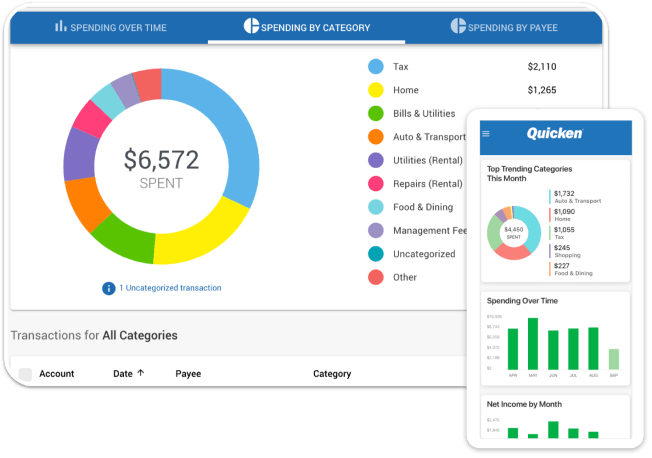

Today, budgeting apps have moved beyond simple transaction logging. Modern platforms feature collaborative logins for couples, predictive cash flow modeling, automated subscription cancellations, and generative AI financial planners that can automatically build budgets, draft wills, and optimize tax strategies.

Supporting Data: Comprehensive Analysis of Leading Alternatives

The modern PFM ecosystem is diverse. Below is a detailed breakdown of the top platforms currently competing for Quicken’s market share, categorized by their primary use cases.

1. Modern Budgeting and Subscription Management

Monarch Money

- App Store Rating: 4.9 (approx. 88,000 reviews)

- Android Rating: 4.8 (approx. 21,200 reviews)

- Pricing: $8.33 per month (billed annually at $99/yr); currently offers a 7-day free trial and a 50% discount on the first year of the Core Plan using promo code ROB50.

- Key Features: Flex Budgets, multi-user collaboration, automated recurring subscription tracking, customizable transaction rules, and asset allocation visualization.

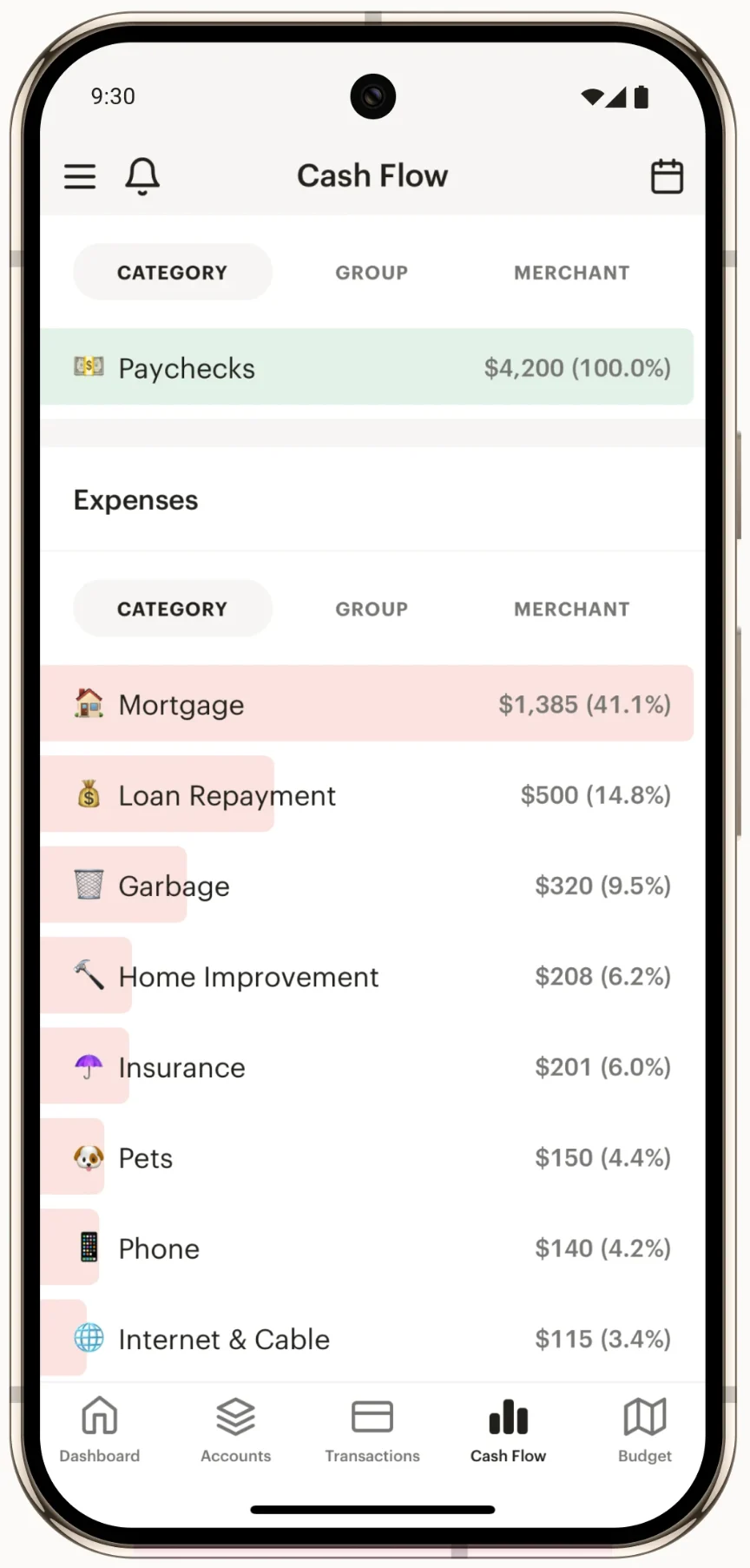

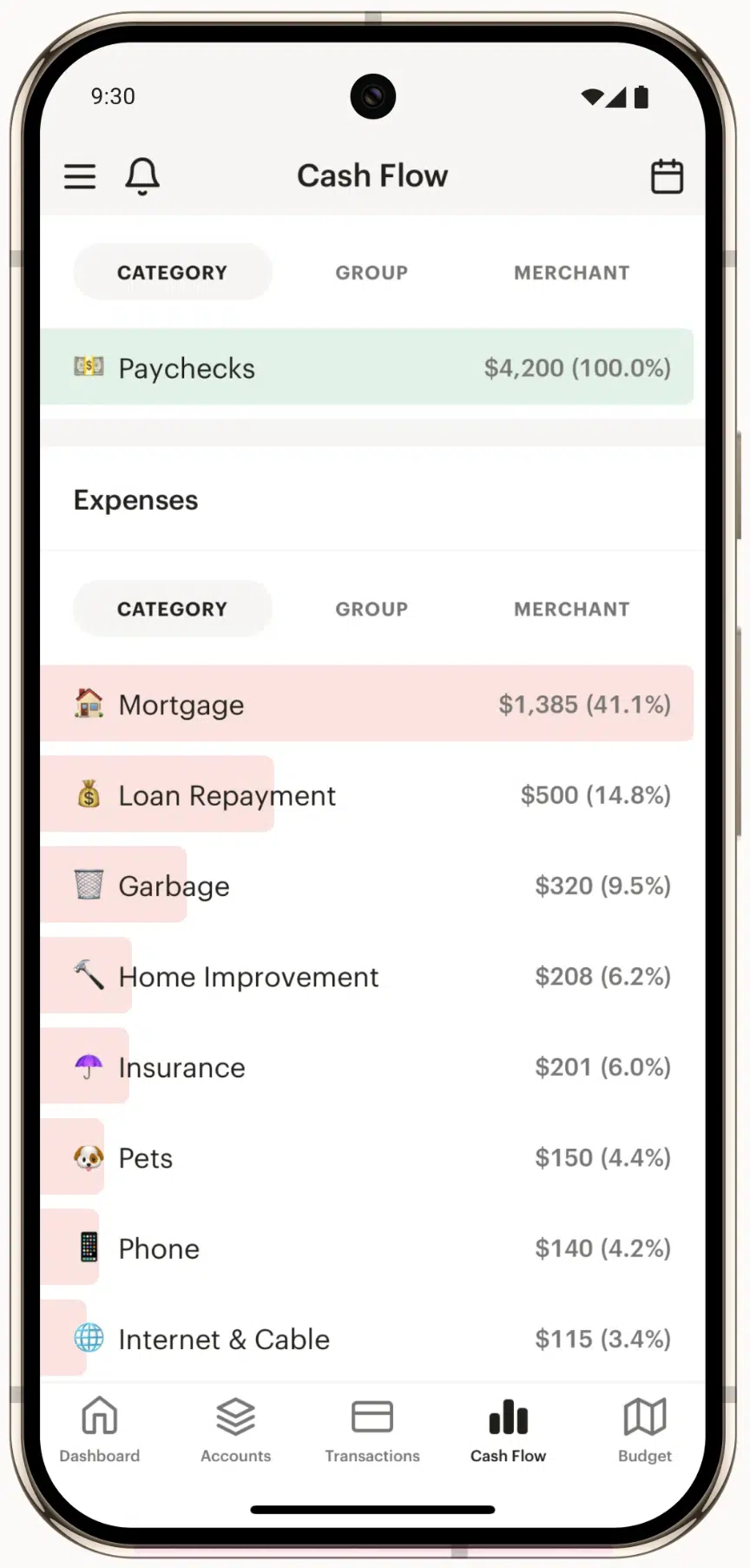

Monarch Money has emerged as a top premium alternative to Quicken. Developed by a team of former Mint product creators, it focuses on modern design and user experience. Unlike older apps, Monarch allows couples to invite a partner to their account with a separate login, making it easy to manage shared finances while maintaining separate bank accounts. Its "Flex Budgets" feature automatically adjusts monthly spending limits based on fluctuating income and irregular expenses.

Quicken Simplifi

- App Store Rating: 4.5 (approx. 9,500 reviews)

- Android Rating: 4.1 (approx. 4,220 reviews)

- Pricing: $6.99 per month; currently discounted by 50% to $3.49 per month for the first year (billed annually), backed by a 30-day money-back guarantee.

- Key Features: Custom "Spending Plans," calendar-based bill tracking, basic investment tracking, and cash flow projections.

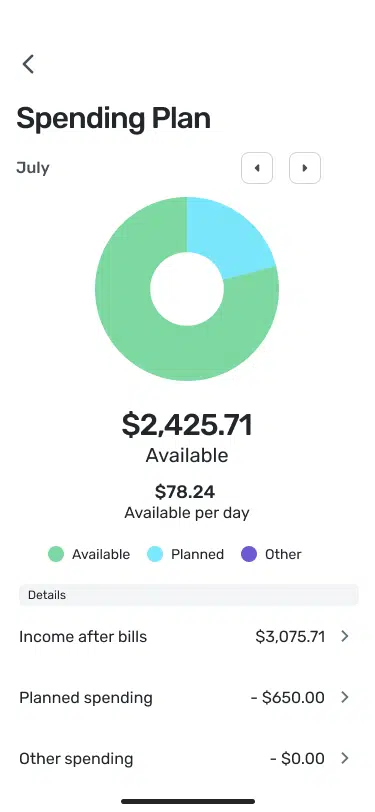

Simplifi is Quicken’s modern, cloud-native response to newer competitors. Originally built as a mobile-first application, it is now available as a web portal. Instead of using rigid traditional categories, Simplifi uses a flexible "Spending Plan" model that calculates how much discretionary income a user has left after accounting for bills, savings goals, and subscription services.

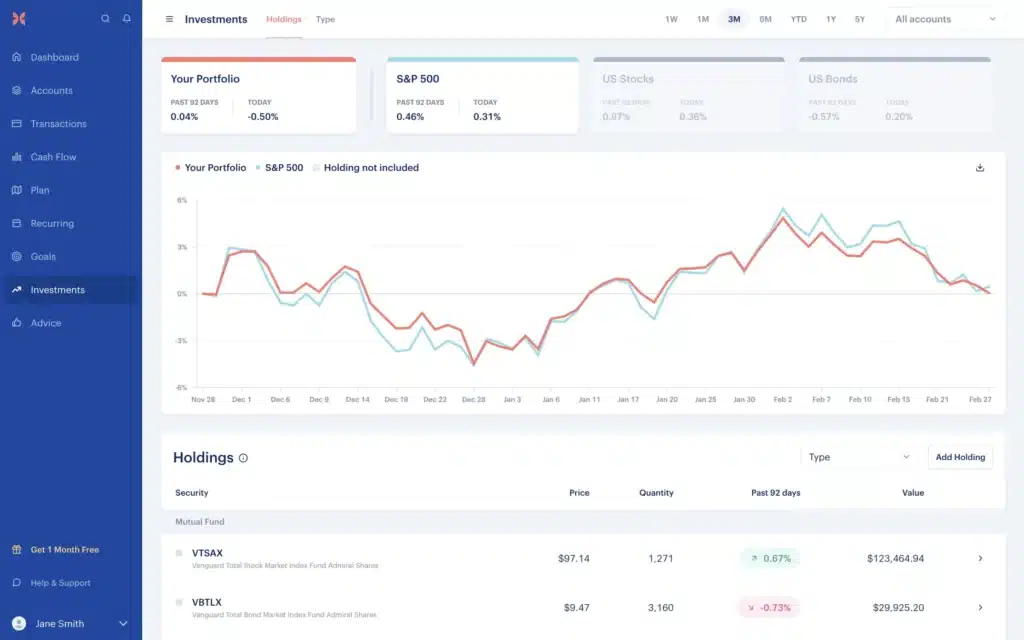

2. Wealth Tracking and Investment Management

+---------------------------------------------------------------------------------+

| EMPOWER PERSONAL DASHBOARD METRICS |

+---------------------------------------------------------------------------------+

| Active Users: Over 3.3 Million |

| Subscription Cost: $0.00 (100% Free) |

| Core Focus: Net Worth, Investment Tracking, & Retirement Planning |

| Key Tool: Retirement Planner (Monte Carlo simulations) |

| Key Tool: Fee Analyzer (uncovers hidden mutual fund fees) |

+---------------------------------------------------------------------------------+Empower (Formerly Personal Capital)

- App Store Rating: 4.8 (approx. 378,000 reviews)

- Pricing: Free.

- Key Features: Investment portfolio tracking, retirement planner, net worth calculator, fee analyzer, and cash flow tracking.

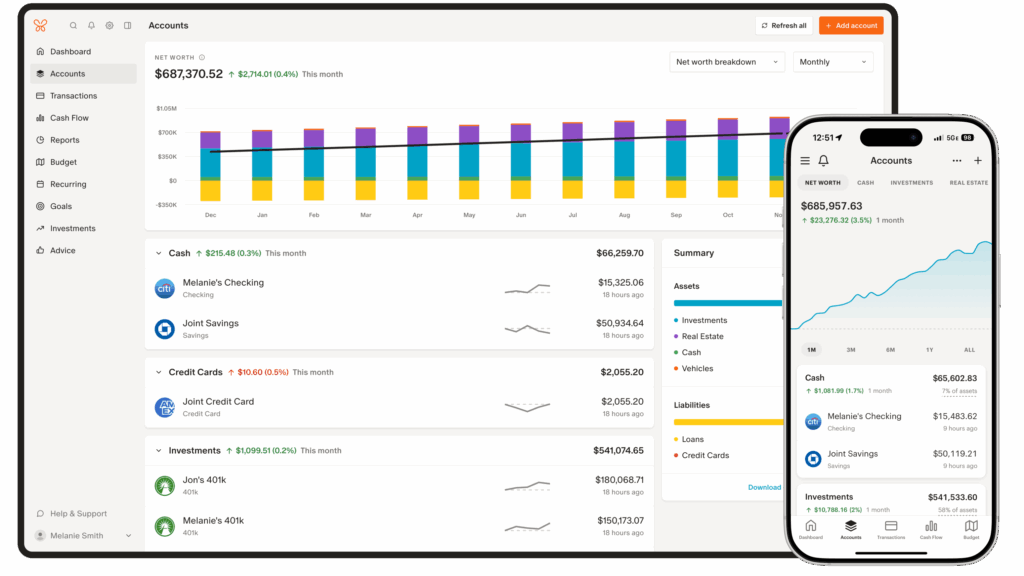

For users who relied on Quicken Premier to manage complex investment portfolios, Empower is a strong free alternative. The platform acts as an automated aggregator for brokerage accounts, retirement accounts (401ks, IRAs), mortgages, and real estate assets via Zillow.

While its budgeting tools are less detailed than Monarch’s or YNAB’s, its investment analytics are highly robust. The platform’s retirement planning module runs Monte Carlo simulations to calculate the likelihood of portfolio survival under various market conditions, while its Fee Analyzer highlights hidden management fees in mutual funds and ETFs. Empower funds this free dashboard by cross-selling its premium wealth management services to users with portfolios over $100,000.

3. AI-Powered Financial Ecosystems

Origin

- Pricing: $12.99 per month or $99 per year; currently running a promotional offer of $1 for the first year.

- Key Features: AI-driven budgeting, integrated tax preparation, basic estate planning (wills and trusts), automated robo-advising, and an integrated high-yield savings account (4.52% APY as of late 2025).

Origin represents the next generation of financial technology by integrating AI into every feature. Instead of requiring users to build spreadsheets, Origin’s AI analyzes past transactions to build a budget automatically.

Additionally, Origin offers tax preparation software and estate planning documents (such as basic wills) at no extra charge. This integration makes it a strong competitor to Quicken Classic Premier, which has historically relied on external integrations with TurboTax to offer similar tax-prep features.

4. Specialized and Niche Alternatives

You Need A Budget (YNAB)

- Pricing: $14.99 per month or $109 per year (offers a 34-day free trial).

- Key Features: Zero-based budgeting, envelope method allocation, real-time bank syncing, and goal tracking.

YNAB is designed for users who want active control over their cash flow rather than passive investment tracking. Operating on the envelope budgeting method, YNAB requires users to assign every incoming dollar a specific "job" (e.g., rent, groceries, or savings).

While it lacks robust investment tracking and AI-driven automation, its hands-on approach is highly effective for paying down debt and building savings. However, it remains one of the most expensive pure budgeting apps on the market.

Rocket Money

- Pricing: Free tier available; Premium features cost between $7 and $14 per month (pay-what-you-want model).

- Key Features: Subscription cancellation services, automated bill negotiation, spending charts, and credit score monitoring.

Rocket Money (formerly Truebill) is a strong option for users looking to cut monthly expenses. Beyond traditional transaction categorizing, Rocket Money identifies recurring subscriptions and can negotiate lower rates on utility and telecom bills on the user’s behalf, taking a percentage of the annual savings as a fee.

PocketSmith

- Pricing: Free manual tier; Premium tiers start at $9.95 per month ($7.50 per month billed annually).

- Key Features: Calendar-based budget views, cash flow forecasting up to 30 years, and automatic historical budgeting.

PocketSmith stands out by organizing financial data into a calendar interface. It allows users to schedule upcoming transactions and project their future net worth decades into the future based on their current spending patterns.

CountAbout

- Pricing: Basic Plan is $9.99 per year; Premium Plan (with automatic bank downloads) is $39.99 per year.

- Key Features: Seamless import of legacy Quicken and Mint files (QIF/CSV), receipt attachments, and recurring transaction tracking.

For long-time Quicken users, the biggest obstacle to switching is the potential loss of decades of historical financial data. CountAbout solves this issue by offering a reliable import utility for Quicken data files. This allows users to preserve their financial history while transitioning to a web-based platform.

Summary Comparison Table

| Quicken Alternative | Primary Focus | Cost Structure | Platform Availability | Key Advantage |

|---|---|---|---|---|

| Monarch Money | Premium Budgeting | $8.33/mo (Billed annually) | iOS, Android, Web | Best for couples & collaboration; modern UI |

| Quicken Simplifi | Flexible Spending | $6.99/mo (or $3.49/mo first year) | iOS, Android, Web | Best value for bill & cash flow tracking |

| Empower | Portfolio Tracking | Free | iOS, Android, Web | Best investment analytics & net worth tools |

| Origin | AI-Powered Wealth | $12.99/mo or $99/yr | iOS, Android, Web | Includes free tax prep, estate planning & HYSA |

| YNAB | Zero-Based Budgeting | $14.99/mo or $109/yr | iOS, Android, Web | Highly effective for debt reduction |

| Rocket Money | Bill Optimization | Free tier; $7 to $14/mo Premium | iOS, Android, Web | Automated subscription cancellation services |

| PocketSmith | Financial Forecasting | Free tier; paid plans from $7.50/mo | iOS, Android, Web | Multi-decade calendar cash flow projections |

| CountAbout | Legacy Migration | $9.99 to $39.99/year | iOS, Android, Web | Imports legacy Quicken and Mint data easily |

Official Responses and Market Dynamics

The steady loss of desktop users has forced legacy software companies to adapt. Quicken’s response highlights the challenges of modernizing a legacy desktop platform.

+---------------------------------------------------------------------------------+

| PFM MARKET SHARE RE-ALIGNMENT |

+---------------------------------------------------------------------------------+

| Legacy Desktop (Quicken Classic) |

| - Retains older, high-net-worth users who prefer local offline storage. |

| - Faces declining market share due to complex updates and manual backups. |

| |

| Cloud-Native Platforms (Simplifi, Monarch, Origin) |

| - Rapid adoption among Millennials and Gen Z. |

| - Fueled by Plaid integrations and automated bank feeds. |

| |

| Free Aggregators (Empower) |

| - Captures users who reject subscription-based budgeting apps. |

| - Funded by wealth management services. |

+---------------------------------------------------------------------------------+After being spun off from Intuit in 2016 and acquired by private equity firms (first H.I.G. Capital, and later Aquiline Capital Partners), Quicken realized that its core product, Quicken Classic, had a demographic problem. Its user base skewed older, and younger consumers rejected the concept of manual desktop software installations.

In response, Quicken launched Simplifi to compete with modern, web-first platforms. While Simplifi has helped Quicken retain users who might have otherwise moved to Monarch Money or YNAB, the company faces a delicate balancing act. It must continue to support Quicken Classic for its traditional user base—many of whom require specialized features like rental property management, local QDF file encryption, and advanced tax reporting—while simultaneously investing in cloud-native platforms.

Meanwhile, competitors are capitalizing on Quicken’s subscription-only model. When Quicken removed its one-time purchase option, competitors like Empower positioned themselves as permanent, free alternatives. At the same time, premium platforms like Monarch Money and YNAB justified their subscription fees by committing to ad-free platforms, reassuring privacy-conscious consumers that their financial data would not be monetized.

Implications: The Future of Personal Wealth Management

The transition from offline desktop ledger systems to cloud-native, automated financial apps has significant implications for consumers and the broader financial technology industry.

1. The Trade-off Between Privacy and Convenience

The migration away from Quicken Classic marks the end of completely private financial tracking. Under the legacy model, a user’s financial ledger lived on their local hard drive, safe from cloud data breaches.

Modern alternatives require users to connect their financial accounts to third-party aggregators like Plaid or Yodlee. While these services use bank-grade encryption, storing highly detailed financial data in the cloud introduces new cybersecurity risks.

2. The Rise of Collaborative Financial Management

Traditional desktop PFM software was designed for a single user at a single computer. Modern cloud platforms recognize that household finances are increasingly collaborative.

Features like Monarch Money’s dual-partner logins reflect a cultural shift: modern couples are managing their money as a team, using shared dashboards that combine individual and joint accounts.

3. AI-Driven Financial Planning

The integration of artificial intelligence into apps like Origin points to the future of financial planning. As AI engines improve, budgeting software will move beyond simply tracking past spending.

Instead, these tools will actively optimize cash flow in real-time—automatically moving excess checking balances into high-yield savings accounts, rebalancing investment portfolios to minimize taxes, and identifying cheaper service providers.

Ultimately, the decline of legacy desktop software is more than just a shift in consumer preferences; it represents a fundamental change in how households interact with money. Consumers are choosing convenience, real-time automation, and mobile accessibility over local data ownership. For legacy systems like Quicken, the challenge is clear: modernize completely, or continue to lose ground to a new generation of financial tools.