The Evolution of Wealth Management: An In-Depth Analysis of Empower’s Financial Ecosystem

The consumer fintech landscape has undergone a massive consolidation over the past decade, shifting from fragmented, single-purpose budgeting apps to comprehensive, institutional-grade wealth management platforms. At the center of this evolution is Empower, a digital financial management tool that allows users to aggregate, track, and analyze 100% of their financial portfolios from a single, unified dashboard.

Formerly known as Personal Capital, the platform has established itself as one of the premier personal finance tools on the market. By offering a robust suite of free tracking utilities alongside premium, hybrid wealth management services, Empower caters to both self-directed retail investors and high-net-worth individuals seeking professional oversight.

This comprehensive report examines the structural realities of the Empower platform, tracking its historical evolution, evaluating its core features through empirical data, analyzing its security and monetization strategies, and assessing its broader implications for the modern retail investor.

1. Main Facts: The Empower Value Proposition

Empower functions primarily as a financial aggregator, utilizing secure APIs to sync disparate accounts into a real-time snapshot of an individual’s net worth and overall financial health. Unlike legacy budgeting software that requires manual transaction entries, Empower relies on automation to pull data from checking accounts, high-yield savings accounts, credit cards, mortgages, personal loans, and complex investment vehicles (such as employer-sponsored 401(k)s, traditional and Roth IRAs, and taxable brokerage accounts).

+-----------------------------------------------------------------------------------+

| EMPOWER PLATFORM |

+-----------------------------------------------------------------------------------+

| [ Aggregation Engine ] <--- APIs (Plaid/Yodlee) <--- Banks, Brokerages, Lenders |

+-----------------------------------------------------------------------------------+

|

+-------------------------------+-------------------------------+

| | |

v v v

[ Cash Flow & Budgeting ] [ Investment Tracking ] [ Financial Planning ]

- Automated Categorization - Real-Time Holdings - Retirement Scenario Builder

- Bill Due Date Alerts - Asset Allocation Engine - Savings Planner (Emergency/Debt)

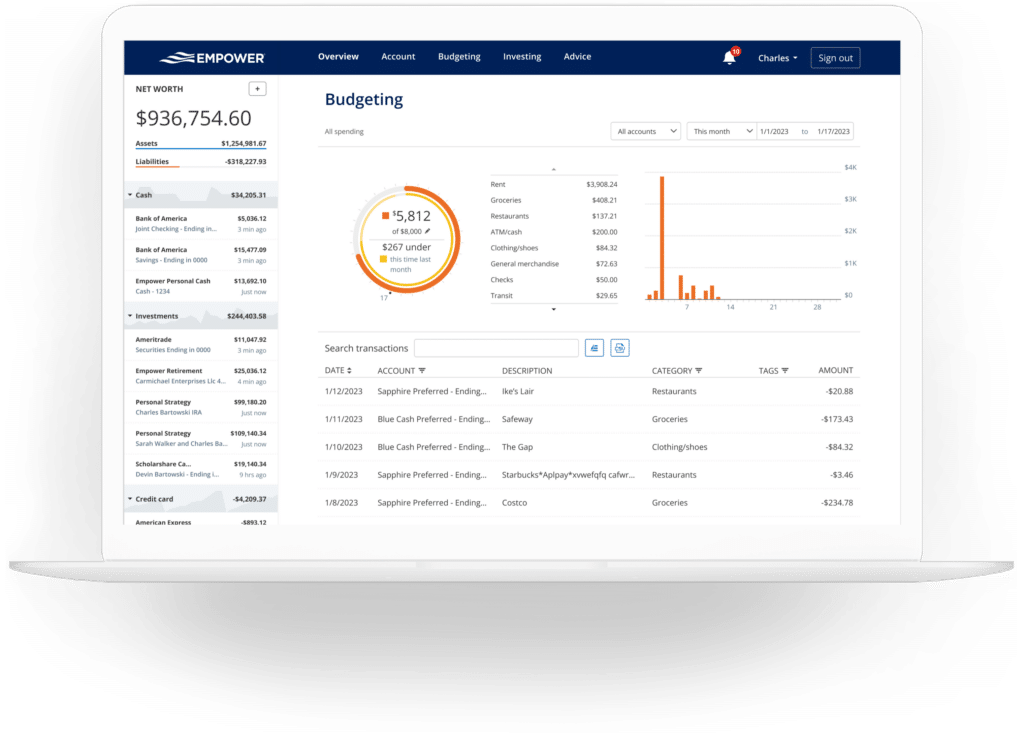

- Custom Transaction Tagging - Retirement Fee Analyzer - Investment Fee CheckupThe core software is divided into three functional pillars:

- Cash Flow and Liability Management: Tracks monthly income, categorizes expenses, and monitors debt payoff schedules.

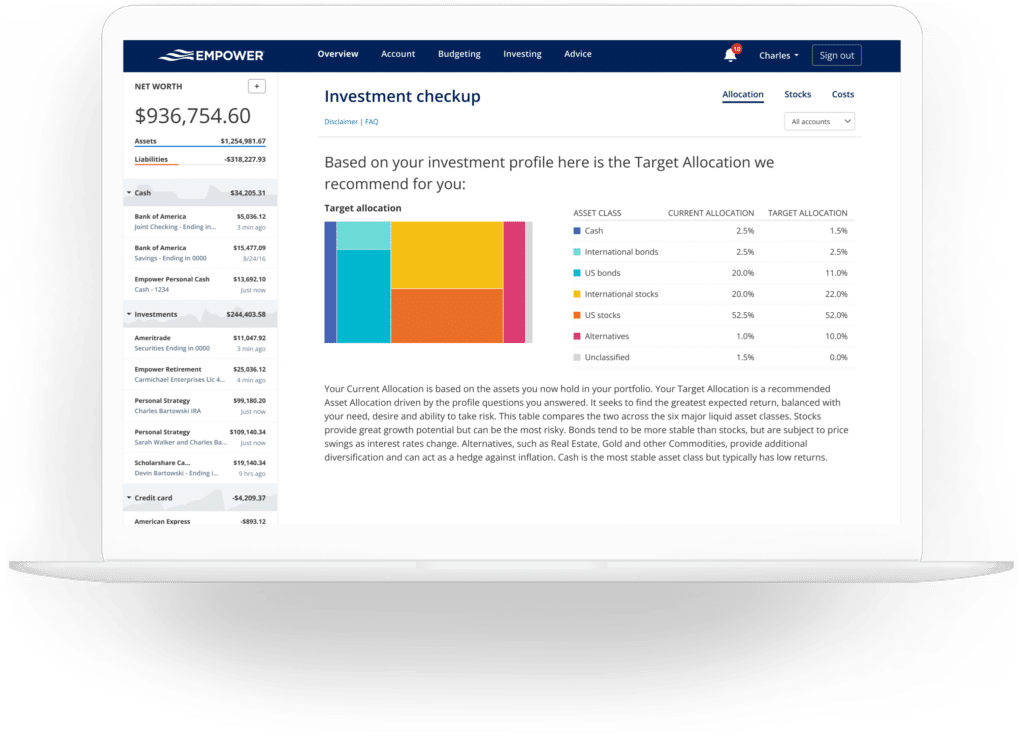

- Investment Optimization: Evaluates portfolio performance, calculates weighted-average expense ratios, and analyzes asset allocation across various classes.

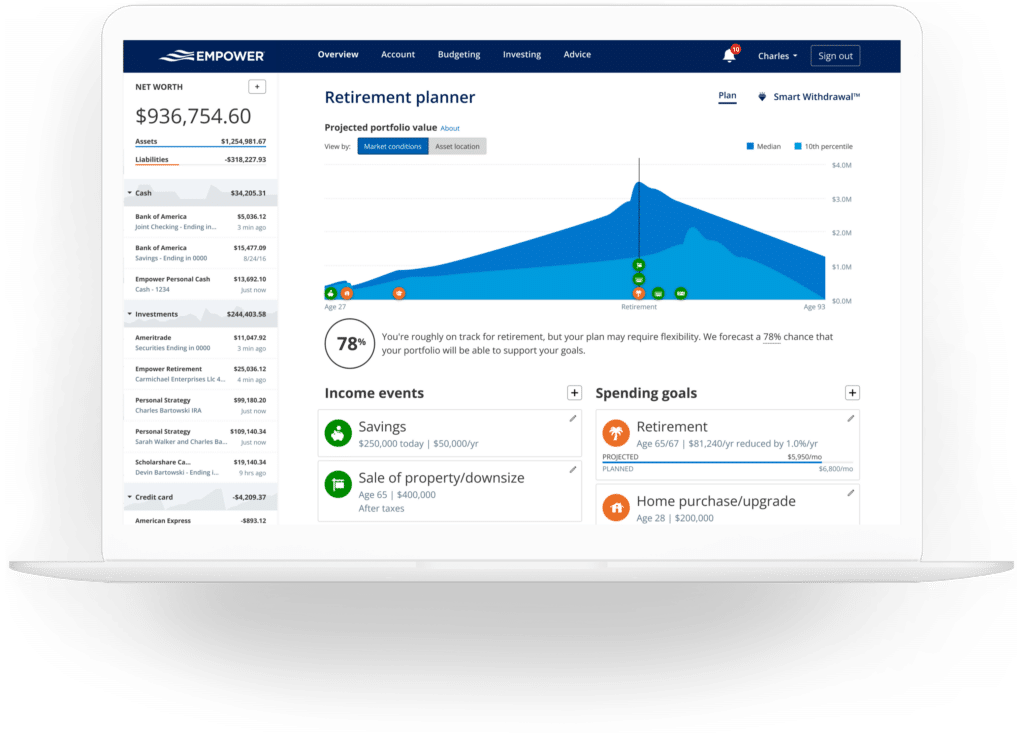

- Retirement and Scenario Planning: Utilizes Monte Carlo simulations to calculate the mathematical probability of a user’s retirement portfolio surviving various market conditions.

The foundational dashboard is entirely free to use. Empower monetizes its platform by acting as a lead-generation funnel for its proprietary, paid wealth management advisory services, creating a unique hybrid business model that bridges software-as-a-service (SaaS) and traditional financial advisory.

2. Chronology: From Personal Capital to Empower

The trajectory of the platform reflects the broader consolidation trends within the fintech industry. Understanding how the app transitioned from a Silicon Valley startup to an institutional powerhouse is key to understanding its current market positioning.

[2009] Founded as Personal Capital by Bill Harris (Former CEO of Intuit & PayPal)

│

▼

[2010s] Scaled rapidly; pioneered the "hybrid robo-advisor" model

│

▼

[2020] Acquired by Empower Retirement for $1 Billion ($825M upfront, $175M earn-outs)

│

▼

[2023] Completed formal integration; fully rebranded as "Empower"The Genesis of Personal Capital (2009–2019)

Personal Capital was founded in 2009 by a team of financial and technology veterans, including Bill Harris, the former CEO of Intuit and PayPal. The company’s goal was to address the limitations of early personal finance tools like Mint.com. While Mint focused heavily on budgeting and backward-looking cash flow analysis, Personal Capital was designed from the ground up to focus on forward-looking wealth building, investment tracking, and asset allocation.

Throughout the 2010s, Personal Capital grew rapidly, positioning itself as a "hybrid robo-advisor." It combined free, automated portfolio tracking software with access to human financial advisors for clients who met specific asset thresholds.

The Institutional Acquisition (2020)

In June 2020, during a period of rapid digital transformation accelerated by the COVID-19 pandemic, Empower Retirement—the second-largest retirement plan provider in the United States and a subsidiary of Great-West Lifeco—announced an agreement to acquire Personal Capital. The transaction valued the fintech firm at up to $1 billion, comprising $825 million in upfront regulatory capital and up to $175 million in transition- and performance-based earn-outs.

The acquisition was a strategic move by Empower Retirement to bridge the gap between employer-sponsored retirement plans (such as corporate 401(k)s) and retail wealth management. By acquiring Personal Capital, Empower obtained a sophisticated digital engagement platform to offer to its millions of retirement plan participants.

The Rebranding and Integration (2023–Present)

Following the acquisition, the platform underwent a multi-year backend integration. In early 2023, the transition was completed publicly when the Personal Capital brand was retired and the software was officially renamed Empower.

While the interface and underlying algorithm remained largely intact, the rebranding marked the platform’s full absorption into a retirement services giant that administers over $1.4 trillion in assets for more than 18 million joint customers.

3. Supporting Data: Feature Analysis and Technical Specifications

Empower’s market share and high user ratings reflect its strong technical foundation. On mobile platforms, the application maintains highly competitive ratings:

- Apple App Store: 4.8 out of 5 stars (compiled across approximately 366,000 user reviews).

- Google Play Store: 4.0 out of 5 stars (compiled across approximately 29,400 user reviews).

The core appeal of the software lies in its specialized, data-driven tools. Below is an analytical breakdown of these key features.

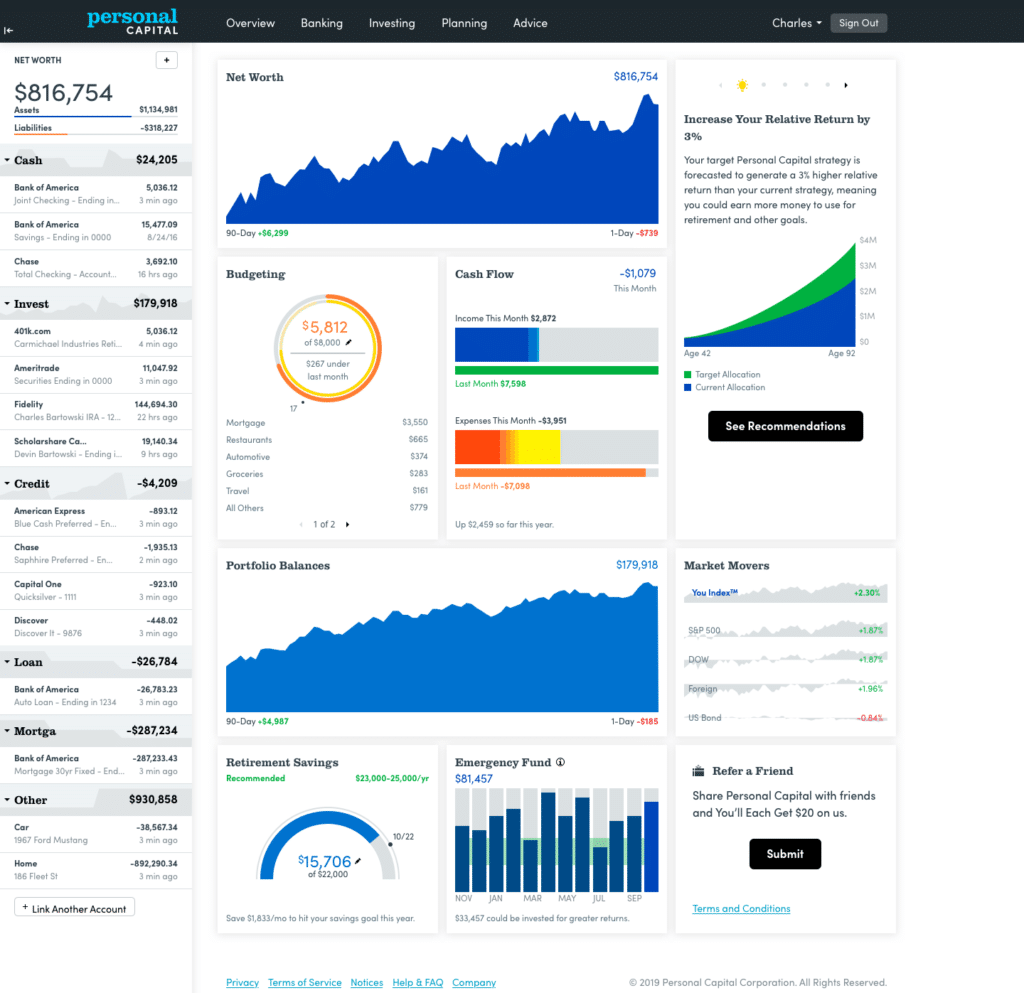

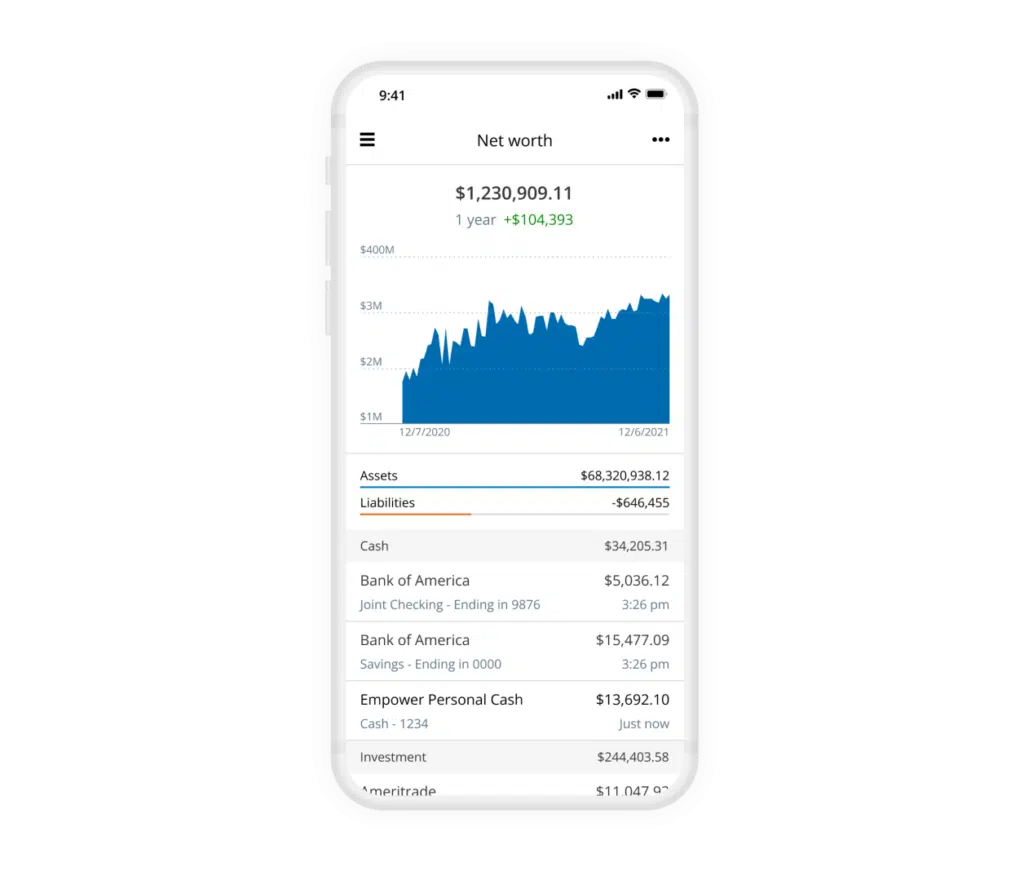

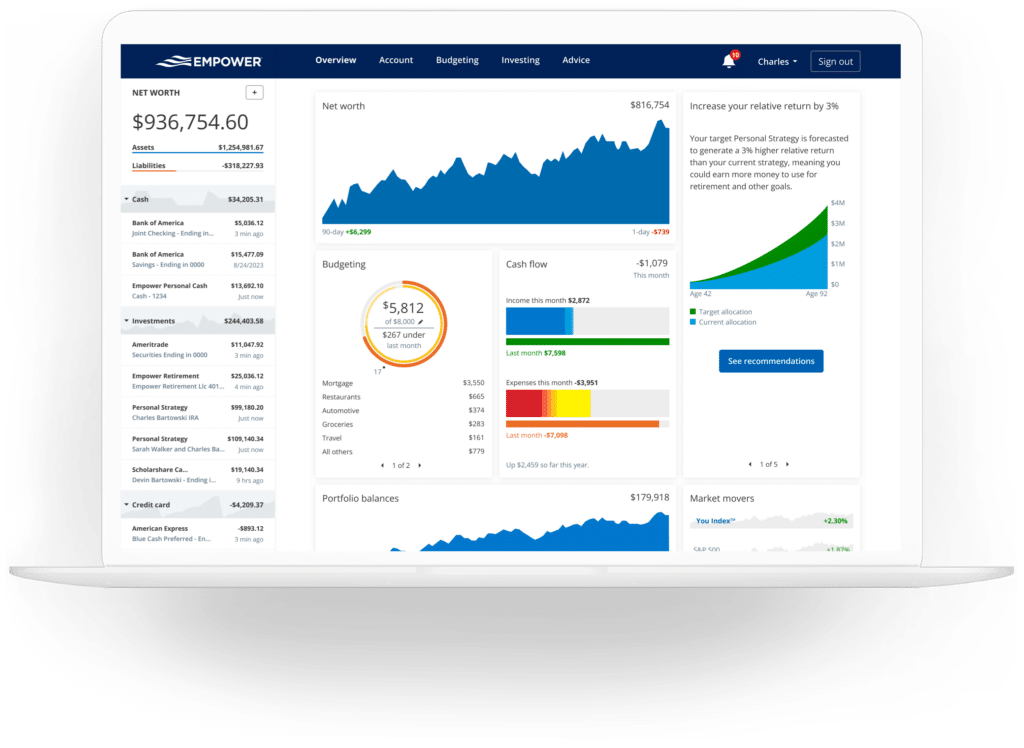

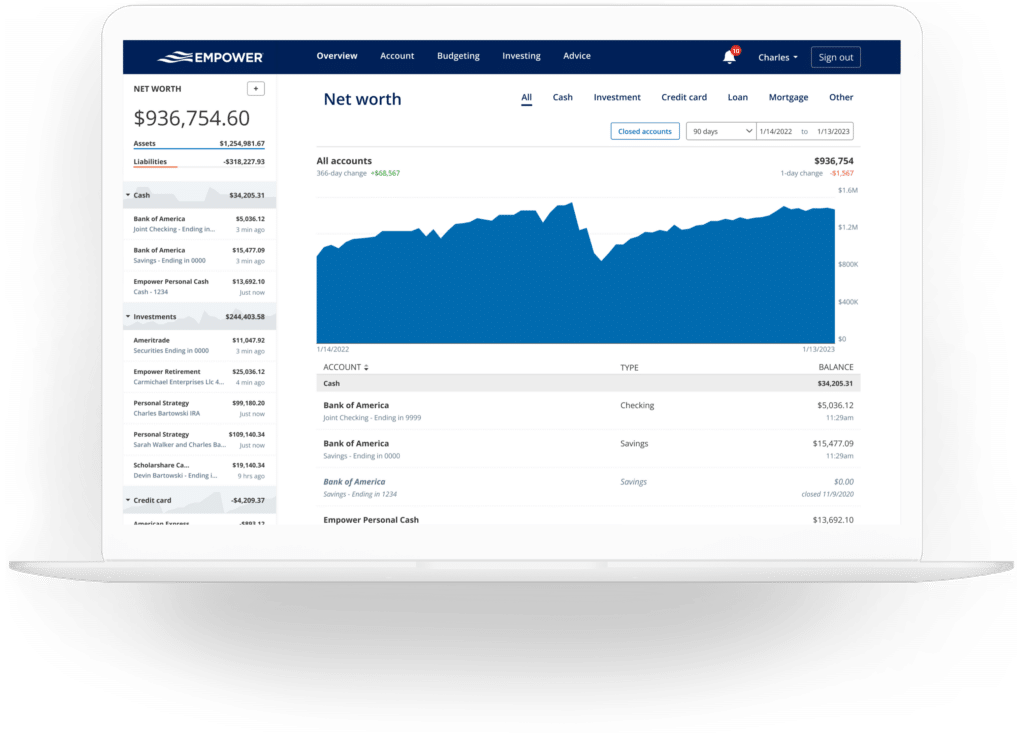

Net Worth and Asset Aggregation

The Net Worth Tracker serves as the anchor of the Empower dashboard. By integrating with aggregation engines like Yodlee and Plaid, the software updates account balances daily.

In addition to liquid and paper assets, the platform allows users to track illiquid assets. Most notably, users can link their primary or secondary real estate holdings directly to the platform. Empower integrates with the Zillow Zestimate API to dynamically adjust estimated property values against prevailing market trends, updating the asset side of the user’s balance sheet automatically.

Net Worth = (Liquid Cash + Brokerage Portfolios + Real Estate [via Zillow]) - (Mortgages + Student Loans + Credit Card Balances)Banking, Cash Flow, and Category Tagging

While Empower is not a traditional zero-based budgeting tool like YNAB (You Need A Budget), it provides comprehensive cash flow oversight.

+------------------------------------------------------------------------------------+

| EMPOWER CASH FLOW MONITOR |

+------------------------------------------------------------------------------------+

| |

| INCOME: [======================================] $8,500 (Salary, Dividends) |

| |

| EXPENSES: [========================] $4,200 (Auto-Categorized Outflows) |

| |

| SURPLUS: [==============] $4,300 (Available for Investment/Savings) |

| |

+------------------------------------------------------------------------------------+The system automatically imports transaction histories and assigns them to default categories (e.g., Groceries, Utilities, Home Maintenance).

To accommodate complex accounting, Empower supports custom transaction tagging. For instance, rather than creating a separate top-level category for a specific asset like a swimming pool, a user can assign transactions to "Home Maintenance" and apply a custom tag like [pool]. This allows for granular spending reports without cluttering the master budget ledger.

Cryptocurrency Integration

To accommodate the rise of digital assets, Empower supports cryptocurrency tracking. Rather than requiring users to link private keys or connect cold-storage wallets—which presents significant security risks—Empower utilizes a manual, API-supported tracking ledger.

Users manually input their specific token holdings, quantities, and purchase exchanges. Empower then tracks price fluctuations in real time across thousands of tokens (including Bitcoin, Ethereum, and Litecoin) and hundreds of active cryptocurrency exchanges, integrating these balances directly into the master asset allocation matrix.

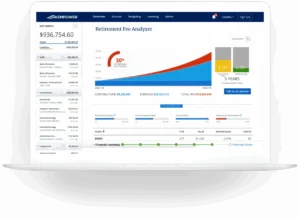

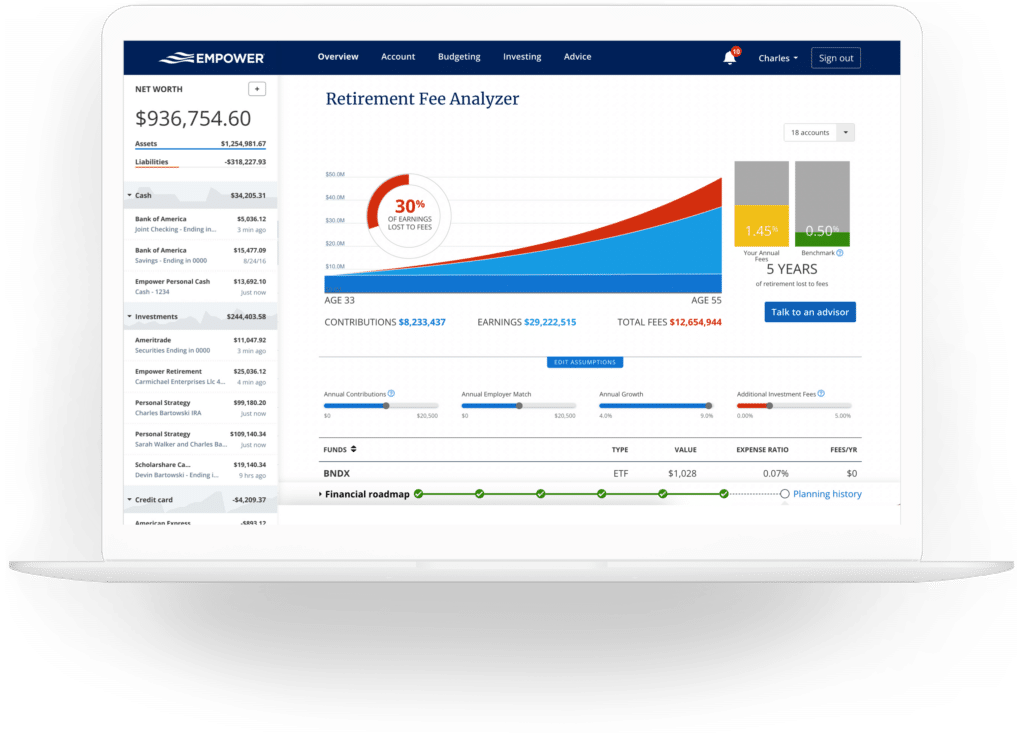

The Retirement Fee Analyzer

One of Empower’s most mathematically impactful features is the Retirement Fee Analyzer. Investment fees can quietly erode portfolio growth over time. A seemingly minor 1.00% annual management fee can consume hundreds of thousands of dollars in potential compounded gains over a multi-decade investing horizon.

+------------------------------------------------------------------------------------+

| PORTFOLIO DRAG OVER TIME (30 YEARS) |

+------------------------------------------------------------------------------------+

| Assumes $500,000 starting balance, 7% annual growth, and 30-year horizon |

| |

| Low-Fee Portfolio (0.06% Fees): [=================================] $3,745,000 |

| |

| High-Fee Portfolio (1.00% Fees): [=======================] $2,830,000 |

| |

| Fee Drag (Lost Wealth): [=========] $915,000 |

| |

+------------------------------------------------------------------------------------+The Fee Analyzer calculates a weighted average expense ratio for all linked retirement and brokerage portfolios. It compares this figure against industry benchmarks and projects the total dollar impact of fees over a set period.

For example, an investor with a highly optimized portfolio of low-cost index funds might register a weighted average expense ratio of just 6 basis points (0.06%). Even at this low rate, on a multi-million dollar portfolio, the Fee Analyzer calculates the exact projected drag—such as $17,865 lost over a seven-year period—helping users find opportunities to switch to lower-cost alternatives.

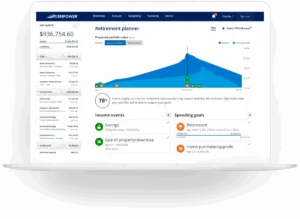

Retirement Planner and Monte Carlo Simulations

The Retirement Planner does not simply project linear growth. Instead, it runs Monte Carlo simulations—typically executing hundreds of randomized trials incorporating historical market volatility, inflation spikes, and economic downturns—to generate a probability percentage of retirement success.

+------------------------------------------------------------------------------------+

| RETIREMENT SCENARIO SIMULATION |

+------------------------------------------------------------------------------------+

| |

| Scenario A: Retire at 60, No Social Security, 3.5% Inflation |

| [========================================] 74% Success Probability |

| |

| Scenario B: Retire at 65, Social Security Included, 3.0% Inflation |

| [======================================================] 92% Success Probability |

| |

+------------------------------------------------------------------------------------+Users can build and compare multiple scenarios side-by-side:

- Adjusting target retirement ages.

- Toggling the inclusion of Social Security payments or pension incomes.

- Altering projected tax brackets and inflation rates.

- Simulating large, one-time future capital outflows (e.g., purchasing a second home or funding a child’s education).

4. Official Responses and Corporate Architecture

Empower’s dual identity as both a free software provider and a wealth management firm often raises questions regarding its monetization strategy and data security practices.

Monetization and Sales Operations

The free financial dashboard serves as a highly effective customer acquisition funnel. Empower’s internal sales team actively monitors registered accounts for users who cross a specific threshold of linkable, investable assets—typically $100,000 or more.

Once this threshold is met, users are contacted by an Empower financial advisor via phone or email to schedule a portfolio review. While these reviews are pitched as free consultations, they are designed to transition the user into Empower’s paid advisory program.

+------------------------------------------------------------------------------------+

| EMPOWER ADVISORY FEE STRUCTURE |

+------------------------------------------------------------------------------------+

| Asset Tier Annual Advisory Fee|

+------------------------------------------------------------------------------------+

| First $1,000,000 0.89%|

| Next $2,000,000 0.79%|

| Next $2,000,000 0.69%|

| Next $5,000,000 0.59%|

| Balances Over $10,000,000 0.49%|

+------------------------------------------------------------------------------------+This tiered pricing structure is competitive with traditional, human-only registered investment advisors (RIAs), which often charge a flat 1.00% of assets under management (AUM). However, it is significantly more expensive than pure robo-advisors like Betterment or Wealthfront, which typically charge 0.25% AUM, or self-directed index-fund investing, which can cost less than 0.05% annually.

Empower has stated that users are under no obligation to use their advisory services. The free financial dashboard remains fully functional for users who opt out of advisory solicitations, and sales outreach can be permanently halted upon direct user request.

Security Protocols and Cryptographic Integrity

Because the dashboard aggregates highly sensitive credentials and financial data, its security architecture is built to meet banking standards.

- AES-256 Encryption: Empower utilizes advanced AES-256 encryption with multi-layer key management. This includes rotating, user-specific keys and cryptographic salts to protect data at rest and in transit.

- Credential Isolation: No individual at Empower has access to a user’s bank or brokerage login credentials. Authentication is handled via secure, tokenized APIs or encrypted third-party aggregators.

- Read-Only Environment: The consumer dashboard is structurally read-only. It is technically impossible to initiate fund transfers, execute trades, or modify account details from the Empower interface, which drastically limits potential losses if a device is compromised.

- Device-Level Authentication: Every new login attempt requires multi-factor authentication (MFA) via SMS, email, or telephone verification. The platform also monitors for login anomalies, alerting users to any access attempts from unrecognized devices or foreign IP addresses.

5. Implications for the Fintech Landscape and Retail Investors

The rise and consolidation of Empower has major implications for both the fintech industry and retail wealth management.

The Demise of Pure-Play Budgeting Apps

For years, the personal finance software space was dominated by simple budgeting tools. However, the market has shifted toward long-term wealth building and net worth tracking.

As consumers demand more robust, automated investment analytics, simple budgeting apps have struggled to retain users without adding investment features. Empower’s ability to offer professional-grade portfolio tools for free has raised the bar for what consumers expect from personal finance software.

The Hybrid Advisory Model

Empower’s success proves the viability of the hybrid advisory model. Pure robo-advisors, which rely entirely on automated algorithms, often struggle to retain clients during major market downturns when investors seek human reassurance. Conversely, traditional human advisors can be expensive and lack modern digital tools.

By combining a robust, self-directed dashboard with on-demand access to human advisors, Empower has created a scalable wealth management model that appeals directly to tech-savvy Gen X and Millennial wealth builders.

The Index Fund Era vs. High AUM Fees

Despite the platform’s high-quality software, the 0.89% AUM fee for its advisory services remains a point of debate among DIY investors. The rise of low-cost index funds and "three-fund portfolios" allows retail investors to manage their own asset allocations for a fraction of the cost of an active manager.

For highly self-directed investors, the optimal strategy is often to use Empower’s free dashboard to track their portfolios, analyze fees, and plan for retirement, while declining the paid advisory services. This allows investors to benefit from the platform’s powerful software without incurring the drag of an ongoing advisory fee.

Summary of Core Platform Features

| Feature Category | Core Utility | Target Audience | Primary Benefit |

|---|---|---|---|

| Net Worth Tracking | Aggregates all assets and liabilities in real time. | All Users | Provides an ongoing, high-level view of financial health. |

| Retirement Fee Analyzer | Identifies high mutual fund fees and advisor drag. | DIY Investors | Reduces portfolio costs to maximize compounding. |

| Retirement Planner | Runs Monte Carlo simulations for retirement readiness. | Pre-Retirees | Validates retirement plans under various market conditions. |

| Cryptocurrency Ledger | Tracks digital tokens manually without security risks. | Multi-Asset Investors | Centralizes crypto alongside traditional assets. |

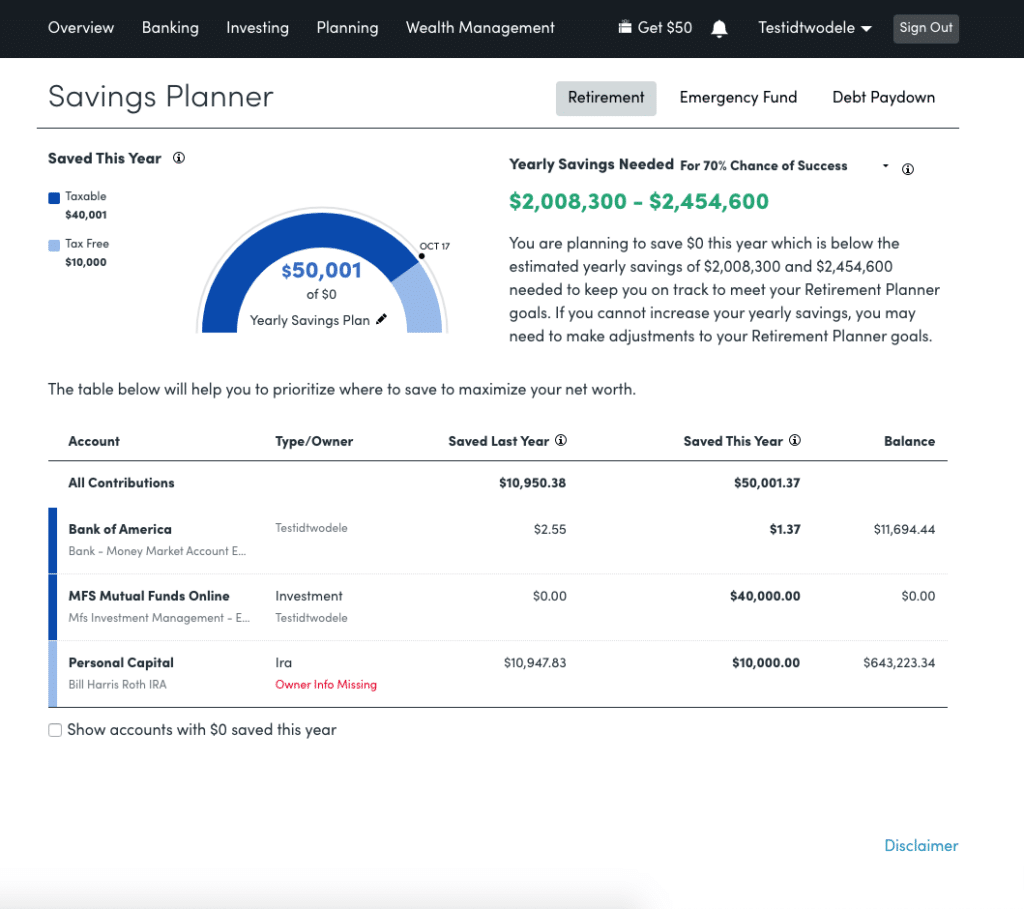

| Savings & Debt Planner | Recommends emergency fund sizes and tracks debt payoff. | Debt-Reducing Households | Accelerates the path to positive net worth. |

Ultimately, Empower is a powerful tool for modern personal finance. By offering advanced portfolio analytics for free, it has democratized wealth tracking, giving retail investors the tools they need to optimize their portfolios, minimize unnecessary fees, and build long-term wealth.